Reports

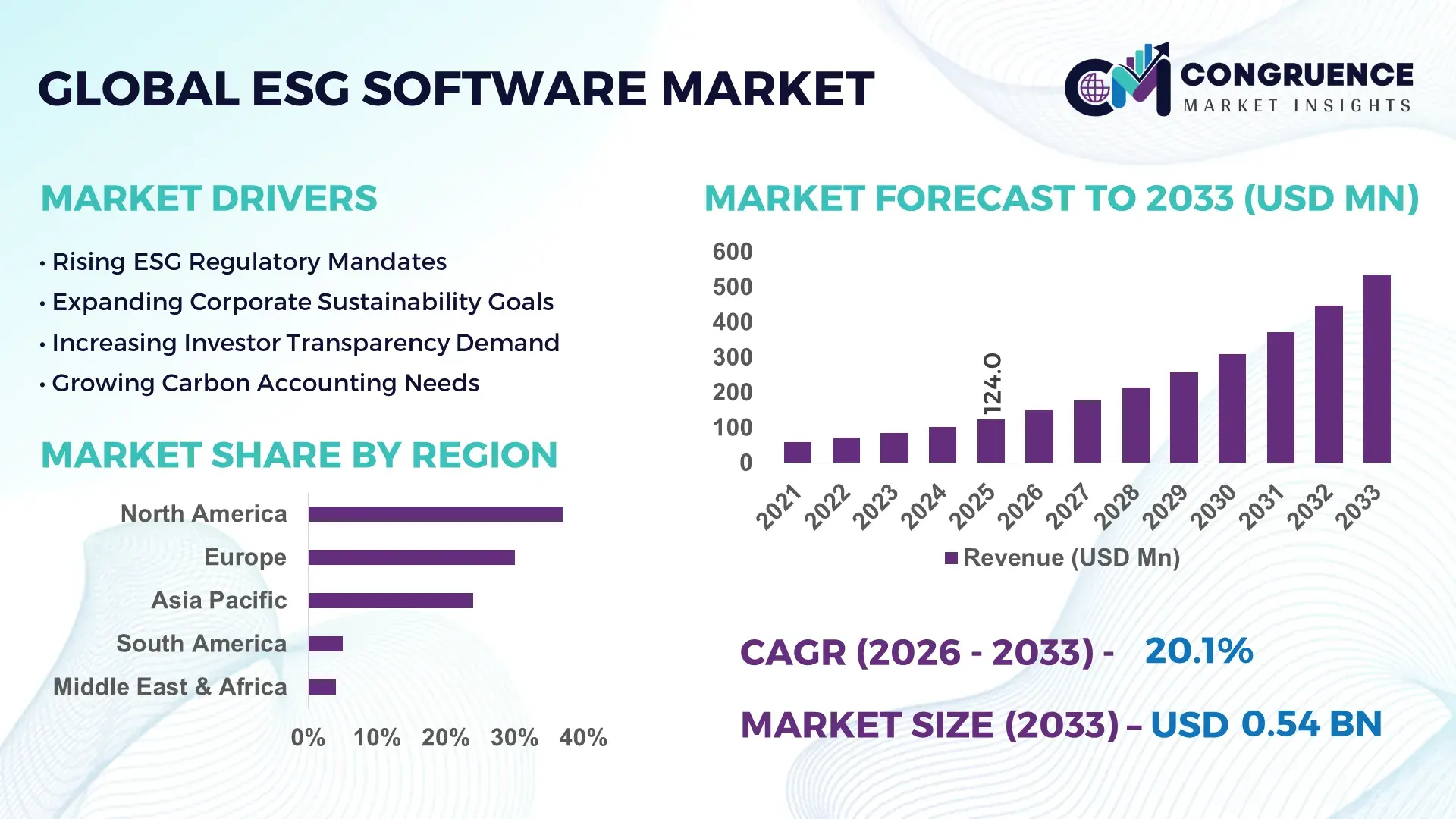

The Global ESG Software Market was valued at USD 124.0 Million in 2025 and is anticipated to reach a value of USD 536.7 Million by 2033 expanding at a CAGR of 20.1% between 2026 and 2033. The market is being propelled by the rapid integration of AI-driven sustainability analytics, automated carbon accounting platforms, and enterprise-wide compliance reporting systems that reduce manual reporting workloads by over 40%. Increasing disclosure mandates, investor scrutiny, and sustainability-linked financing programs are accelerating software adoption across multinational enterprises and mid-sized organizations. Between 2024 and 2026, regulatory frameworks such as the Corporate Sustainability Reporting Directive (CSRD) and climate disclosure initiatives across major economies have transformed ESG reporting from a voluntary activity into a strategic business requirement. The broader digital transformation of supply chains, combined with geopolitical pressure for transparent sourcing and emissions accountability, is further reshaping procurement and reporting processes.

The United States remains the dominant country in the global ESG Software Market, accounting for approximately 34% of worldwide demand. More than 75% of Fortune 500 companies have deployed dedicated ESG reporting or sustainability management platforms, while sustainability-linked investment assets exceed USD 6 trillion in managed exposure. Financial services, manufacturing, technology, and energy sectors collectively represent over 60% of enterprise ESG software deployments. Compared with many emerging economies, enterprise ESG digitization rates are nearly 2.5 times higher in the U.S., supported by advanced cloud infrastructure, AI adoption rates exceeding 68%, and continued investment in environmental performance monitoring systems.

As ESG reporting becomes embedded within corporate decision-making, organizations investing in scalable, automated, and audit-ready software platforms are strengthening compliance readiness, investor confidence, and long-term competitive positioning.

Market Size & Growth: USD 124.0 Million in 2025 reaching USD 536.7 Million by 2033, supported by AI-powered reporting automation and expanding sustainability disclosure requirements.

Top Growth Drivers: AI-based ESG analytics adoption (+48%), regulatory reporting requirements (+42%), and carbon accounting deployment growth (+37%).

Short-Term Forecast: By 2028, ESG reporting cycle times are projected to decline by 35% while audit readiness improves by 30%.

Emerging Technologies: Generative AI, predictive sustainability analytics, and automated emissions tracking are improving reporting accuracy by over 45%.

Regional Leaders: North America (USD 198.6 Million), Europe (USD 171.7 Million), and Asia-Pacific (USD 118.1 Million) driven by digital compliance adoption.

Consumer/End-User Trends: Nearly 68% of large enterprises now integrate ESG metrics into strategic planning and risk management workflows.

Pilot/Case Example: In 2025, enterprise ESG automation projects reduced reporting preparation time by approximately 50% and improved data consistency by 38%.

Competitive Landscape: Leading providers control nearly 34% of market activity, with key participants including Workiva, Enablon, Diligent, Sphera, and Intelex.

Regulatory & ESG Impact: Advanced reporting platforms improve compliance efficiency by 40% under expanding sustainability disclosure frameworks.

Investment & Funding: ESG technology investments exceeded USD 2.4 Billion globally, supported by strategic partnerships and platform expansion initiatives.

Innovation & Future Outlook: AI-enabled decision intelligence, supply-chain sustainability mapping, and real-time ESG monitoring are redefining enterprise sustainability management.

Financial services account for approximately 28% of ESG software demand, followed by manufacturing at 24% and energy & utilities at 18%, reflecting the importance of disclosure-intensive industries. Recent innovation is centered on AI-enabled emissions tracking, automated materiality assessments, and real-time sustainability dashboards that improve reporting accuracy by over 40%. North America contributes nearly 37% of global demand, while Asia-Pacific represents the fastest-expanding adoption base due to rapid enterprise digitization. Regulatory modernization and supply-chain transparency requirements are accelerating software deployment strategies, while integrated ESG intelligence platforms are emerging as the next competitive differentiator. These developments create a strong foundation for deeper strategic market evaluation.

The ESG Software Market is rapidly becoming one of the most strategically important segments within enterprise software because sustainability performance, compliance transparency, and investor accountability are now directly influencing capital allocation, procurement decisions, and corporate valuation. Organizations increasingly view ESG platforms as business-critical systems rather than compliance tools, transforming how environmental, social, and governance data is collected, analyzed, and communicated across global operations.

The market is being reshaped by regulatory pressure, supply-chain transparency requirements, and investor expectations for measurable sustainability outcomes. Global enterprises are accelerating ESG digitization initiatives as reporting complexity expands across multiple jurisdictions and stakeholder groups. This shift is transforming ESG management from periodic reporting into continuous operational monitoring. AI-powered ESG analytics platforms improve reporting efficiency by approximately 45% while reducing compliance management costs by nearly 30% compared to legacy spreadsheet-based systems. This operational advantage is driving widespread technology replacement initiatives among large enterprises seeking higher data accuracy and audit readiness.

North America leads in market volume with approximately 37% of global demand, while Europe leads in compliance-driven innovation, supported by nearly 72% enterprise ESG reporting adoption among large corporations. Over the next two to three years, automated ESG workflows are expected to reduce reporting preparation times by more than 35% while improving disclosure accuracy by 40%.

A strong ESG strategy increasingly functions as a competitive advantage by improving regulatory readiness, reducing operational risk, and strengthening access to sustainability-linked financing. For example, a multinational manufacturing organization implementing AI-driven ESG software reduced manual reporting efforts by 52% while improving audit consistency by 36%. Investment activity is accelerating as software providers expand sustainability intelligence capabilities, acquire specialized analytics firms, and increase capital allocation toward AI-enabled reporting ecosystems. Companies are shifting from standalone compliance solutions toward integrated sustainability management platforms that connect ESG performance with operational and financial outcomes. Organizations that successfully deploy advanced ESG software are not simply optimizing reporting processes; they are building durable competitive advantages through greater transparency, stronger stakeholder trust, improved operational visibility, and superior long-term strategic positioning.

The ESG Software Market is undergoing a structural transformation driven by evolving disclosure requirements, increasing investor scrutiny, and the digitalization of sustainability management processes. Organizations are moving beyond basic reporting frameworks toward integrated ESG intelligence platforms capable of consolidating environmental, social, governance, risk, and compliance data into unified decision-making systems. The market is increasingly influenced by AI-enabled analytics, automated emissions tracking, and real-time reporting capabilities that enhance operational transparency and reduce administrative burdens. Enterprise demand remains concentrated among financial services, manufacturing, energy, and technology sectors where sustainability performance directly influences capital access, stakeholder trust, and regulatory obligations. As global supply chains become more complex and accountability standards intensify, ESG software is evolving into a strategic enterprise technology category that supports governance, resilience, and long-term value creation.

Regulatory expansion remains the strongest growth catalyst for the ESG Software Market. More than 70% of large enterprises now face multiple sustainability reporting obligations across different jurisdictions, forcing organizations to modernize reporting infrastructure. AI-enabled ESG platforms reduce manual data collection efforts by approximately 40% while improving reporting consistency by nearly 35%. The implementation of climate disclosure requirements and supply-chain transparency initiatives has accelerated enterprise software investments, particularly among multinational corporations managing complex vendor ecosystems. This regulatory pressure creates a direct cause-and-effect relationship: stricter reporting obligations increase compliance complexity, which drives software adoption and organizational digitization. In response, companies are expanding ESG technology budgets, forming strategic partnerships with analytics providers, and integrating sustainability reporting into enterprise resource planning environments. The result is a sustained shift from fragmented reporting processes toward centralized ESG management systems capable of supporting continuous compliance and operational visibility.

Data fragmentation remains one of the most significant restraints affecting ESG software implementation. Approximately 58% of organizations continue to manage sustainability data across multiple disconnected systems, creating integration challenges and reporting inconsistencies. Implementation costs can increase by 25–30% when organizations require extensive customization, legacy system integration, and cross-functional workflow redesign. Additionally, varying disclosure frameworks across regions create operational complexity, forcing enterprises to maintain multiple reporting methodologies. The absence of standardized sustainability metrics further complicates scalability and benchmarking efforts. These limitations directly affect deployment timelines, increase operational expenses, and reduce short-term return on investment visibility. To mitigate risks, companies are investing in cloud-native architectures, adopting standardized reporting frameworks, and pursuing strategic partnerships with implementation specialists. Diversified data management strategies are becoming essential for overcoming structural complexity and improving enterprise-wide ESG reporting efficiency.

The next wave of market opportunity is emerging through AI-powered sustainability intelligence, predictive analytics, and supply-chain ESG monitoring. Organizations utilizing advanced analytics platforms have reported up to 45% faster sustainability assessment cycles and approximately 32% improvements in reporting accuracy. Demand for supplier-level ESG visibility is expanding rapidly as over 60% of large enterprises seek deeper sustainability insights across procurement networks. A particularly significant opportunity lies in integrating ESG performance data with financial planning and operational decision-making systems. This creates measurable efficiency gains while strengthening risk management capabilities. Companies are responding by increasing R&D investments, expanding ecosystem partnerships, and developing integrated platforms that combine emissions tracking, governance monitoring, and strategic forecasting. The emerging shift toward real-time sustainability intelligence is redefining competitive advantage and creating new categories of enterprise value.

Scalability remains a major challenge as ESG reporting requirements expand across business units, geographies, and supplier networks. Nearly 65% of organizations report difficulties maintaining data consistency across multiple reporting frameworks, while manual validation processes continue to consume significant operational resources. Reporting complexity can increase by over 35% when companies operate across regions with different sustainability requirements. Growing stakeholder expectations for transparent, auditable disclosures place additional pressure on reporting accuracy and governance standards. These challenges affect long-term reporting reliability, increase compliance risk, and constrain operational scalability. To remain competitive, organizations must invest in automated data governance, AI-assisted validation systems, and integrated reporting architectures. Strategic partnerships, technology innovation, and enterprise-wide ESG standardization are becoming critical requirements for sustaining growth and maintaining stakeholder confidence.

42% Increase in AI-Driven ESG Reporting Automation Reshaping Enterprise Workflows Organizations are rapidly deploying AI-powered ESG reporting systems, with automation usage increasing by 42% across large enterprises. Reporting preparation times have declined by nearly 38%, while data validation accuracy has improved by 33%. Companies are integrating sustainability analytics directly into operational systems, reducing manual intervention and optimizing compliance execution. The shift is forcing software providers to expand AI capabilities and strengthen data governance functions.

35% Growth in Supply-Chain Sustainability Monitoring Redefining Procurement Operations Supplier-level ESG tracking adoption has increased by 35% as organizations seek greater transparency across global sourcing networks. More than 55% of procurement teams now evaluate sustainability metrics during vendor selection processes. Regulatory scrutiny and supply-chain resilience concerns are reshaping procurement strategies, prompting companies to deploy integrated monitoring platforms and establish sustainability performance benchmarks across supplier ecosystems.

48% Expansion in Real-Time ESG Dashboards Optimizing Decision-Making Speed Real-time sustainability intelligence platforms have recorded a 48% increase in enterprise deployment. Organizations report approximately 30% faster executive reporting cycles and 28% improvements in cross-functional visibility. Businesses are restructuring reporting processes around continuous monitoring rather than periodic disclosure, enabling faster response to compliance, operational, and stakeholder requirements while improving strategic coordination.

31% Rise in Subscription-Based ESG Platforms Shifting Software Commercialization Models Subscription-based ESG software adoption has grown by 31%, reflecting enterprise demand for scalable and continuously updated compliance capabilities. Cloud-native deployment rates now exceed 60% among new implementations. Vendors are responding through platform consolidation, strategic partnerships, and integrated service offerings. A non-obvious outcome is that recurring-service models are increasing customer retention while simultaneously accelerating feature innovation and deployment speed.

The ESG Software Market is segmented by type, application, and end-user categories that collectively define adoption patterns and investment priorities. Demand remains concentrated in enterprise-wide reporting and compliance management solutions, reflecting the growing need for centralized sustainability oversight. Approximately 56% of deployments are associated with organizations managing multi-jurisdictional reporting obligations, while nearly 44% focus on operational sustainability performance optimization. Demand is steadily shifting toward integrated platforms capable of combining analytics, compliance management, emissions tracking, and governance oversight within a unified architecture. This transition is influencing software development priorities, enterprise procurement decisions, and long-term technology investment strategies. Organizations increasingly favor scalable solutions that support cross-functional collaboration, real-time visibility, and automated reporting workflows, making segmentation dynamics a critical indicator of future competitive positioning.

The ESG Software Market remains dominated by Cloud-Based ESG Software, accounting for approximately 68% of total deployments in 2025. Its leadership stems from superior scalability, real-time data integration, lower infrastructure requirements, and faster deployment cycles across geographically distributed operations. Large enterprises increasingly favor cloud platforms because they enable centralized ESG reporting, automated regulatory updates, and seamless integration with ERP and sustainability systems. In contrast, On-Premises ESG Software continues to serve organizations with stringent data governance and internal security requirements, representing approximately 32% of market demand. The fastest adoption shift is occurring within cloud-based deployments, with implementation growth exceeding 24% as organizations prioritize operational flexibility and continuous compliance management. Compared with on-premises solutions, cloud platforms reduce implementation timelines by nearly 35% and improve reporting collaboration across business units. As disclosure requirements become more dynamic, software providers are directing product innovation, AI functionality, and analytics development toward cloud-native architectures. Demand is increasingly shifting toward integrated cloud ecosystems, prompting vendors to expand SaaS capabilities, strengthen cybersecurity frameworks, and invest in predictive sustainability analytics. The strategic implication is clear: investment momentum remains concentrated in cloud-based ESG software as enterprises prioritize scalability, automation, and regulatory agility.

• According to a 2025 report by the International Data Corporation (IDC), cloud-based ESG software was adopted by over 70% of large enterprises, resulting in approximately 38% faster reporting cycles and improved sustainability data accuracy, reinforcing its growing strategic importance.

ESG Reporting & Disclosure Management represents the leading application segment with approximately 41% market share, reflecting the growing complexity of sustainability disclosure obligations across global enterprises. Organizations continue to prioritize centralized reporting systems that improve transparency, audit readiness, and stakeholder communication. Demand concentration remains strongest among publicly listed companies, financial institutions, and multinational corporations managing diverse regulatory requirements. The fastest-growing application is Carbon & Emissions Management, expanding at an estimated 26% annual adoption pace as enterprises implement net-zero strategies and operational decarbonization initiatives. Compared with mature reporting applications, carbon management solutions provide deeper operational visibility and measurable sustainability performance tracking. ESG Risk Management, Supply Chain Sustainability Management, and Governance & Compliance Monitoring collectively account for approximately 59% of remaining market demand and are gaining strategic relevance due to increasing investor scrutiny and supplier accountability requirements. Organizations are evolving from compliance-focused deployments toward integrated sustainability intelligence platforms. Vendors are responding through enhanced analytics, AI-enabled forecasting, and real-time emissions tracking capabilities. Demand is clearly shifting toward applications that connect ESG performance with operational decision-making, making advanced sustainability intelligence a critical enterprise capability.

• According to a 2025 report by the Global Reporting Initiative (GRI), ESG reporting and disclosure solutions were deployed across more than 18,000 organizations globally, improving reporting efficiency by approximately 42%, highlighting their rapid operational adoption.

The BFSI sector remains the largest end-user segment, accounting for approximately 29% of ESG Software Market demand. Financial institutions face extensive sustainability disclosure obligations, climate risk assessments, and investor reporting requirements, creating significant dependence on advanced ESG management platforms. Their demand intensity is reinforced by growing expectations for transparent portfolio sustainability reporting and governance oversight. The fastest-growing end-user segment is Manufacturing, where adoption is increasing by approximately 25% as companies seek greater visibility into emissions, supply-chain sustainability, and resource efficiency metrics. Compared with BFSI's compliance-centric adoption, manufacturers focus on operational performance optimization and supplier accountability. Energy & Utilities, IT & Telecom, Healthcare, and other sectors collectively contribute around 71% of total demand and are expanding ESG investments as sustainability performance becomes a competitive differentiator. Enterprise purchasing behavior increasingly favors integrated platforms capable of supporting reporting, analytics, risk management, and emissions monitoring through a single ecosystem. Software providers are responding with industry-specific solutions, subscription-based pricing models, and strategic implementation partnerships. Future demand is expected to shift toward operationally intensive industries where ESG performance directly influences procurement decisions, investor access, and regulatory readiness.

• According to a 2025 report by the World Economic Forum, ESG software adoption among manufacturing organizations increased by 27%, with over 12,000 facilities implementing sustainability management solutions, leading to an average 21% improvement in environmental performance tracking, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 37% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.4% between 2026 and 2033.

North America maintains leadership due to strong enterprise ESG digitization, advanced software infrastructure, and high regulatory preparedness. Europe follows with approximately 30% market share, supported by stringent sustainability disclosure requirements and broad enterprise adoption. Asia-Pacific represents nearly 24% of global demand and is rapidly accelerating as corporations expand sustainability reporting programs and digital compliance initiatives. South America contributes around 5%, while the Middle East & Africa account for 4%, supported by increasing ESG investment activity and modernization programs. Regulatory reforms, supply-chain transparency initiatives, and sustainability-linked financing are driving adoption across all regions. Global software providers are increasingly prioritizing North American scale, European compliance innovation, and Asia-Pacific expansion opportunities to strengthen long-term competitive positioning.

North America represents approximately 37% of global ESG software demand, making it the largest regional market. Financial services, technology, manufacturing, and energy sectors continue driving deployment activity as organizations integrate sustainability metrics into operational and investment decisions. Expanding climate disclosure requirements and stakeholder expectations are reshaping enterprise reporting priorities. More than 72% of large enterprises utilize dedicated ESG management platforms, while AI-enabled sustainability analytics adoption exceeds 60% among new implementations. Organizations increasingly prefer integrated software ecosystems capable of connecting compliance, risk management, and sustainability reporting functions. Vendors are expanding AI capabilities and enterprise integrations to meet evolving customer requirements. The region remains a strategic priority because scale, regulatory readiness, and digital maturity create favorable conditions for long-term software investment.

Europe accounts for approximately 30% of global ESG software demand and remains the most compliance-driven market globally. Countries including Germany, France, and the United Kingdom continue accelerating software adoption as organizations respond to evolving sustainability disclosure frameworks. More than 68% of large enterprises utilize advanced ESG reporting systems, while compliance automation deployment has increased by approximately 34% over recent years. Businesses increasingly prioritize data quality, traceability, and audit readiness to meet regulatory expectations. Software providers are enhancing reporting automation, carbon accounting, and governance monitoring capabilities to support enterprise compliance requirements. The region's emphasis on sustainability governance and transparency is forcing continuous innovation, making Europe a critical market for ESG software advancement and competitive differentiation.

Asia-Pacific accounts for approximately 24% of global ESG software demand and represents the fastest-expanding regional opportunity. China, Japan, India, and Australia are leading adoption as enterprises modernize sustainability reporting and environmental performance management systems. Large-scale industrialization, expanding supply-chain accountability requirements, and accelerated digital transformation are reshaping demand patterns. Enterprise ESG platform deployment has increased by approximately 29%, while sustainability reporting digitization rates have surpassed 50% among large organizations. Businesses prioritize scalable and cost-efficient software capable of supporting regional expansion and compliance needs. Technology vendors continue expanding localized solutions, strategic partnerships, and cloud infrastructure investments. The region is becoming essential for global market expansion because it combines scale, speed, and long-term enterprise digitization momentum.

South America contributes approximately 5% of global ESG software demand, with Brazil and Chile representing the most active markets. Growing investor expectations and sustainability reporting requirements are encouraging organizations to modernize ESG management practices. However, budget limitations, technology integration challenges, and uneven regulatory maturity continue constraining broader adoption. ESG software deployments have increased by approximately 18%, while enterprise sustainability initiatives have expanded by nearly 22% across major industries. Organizations remain highly focused on cost efficiency and measurable business outcomes when selecting software solutions. Vendors are responding through flexible pricing models and localized implementation strategies. The region presents meaningful growth opportunities, though successful expansion requires balancing affordability, scalability, and regulatory adaptation.

The Middle East & Africa region accounts for approximately 4% of global ESG software demand but is experiencing notable momentum. Countries such as the UAE, Saudi Arabia, and South Africa are driving adoption through sustainability initiatives, economic diversification programs, and corporate modernization strategies. ESG platform implementation has increased by approximately 21%, while sustainability-related digital investments have expanded by nearly 25%. Organizations in energy, infrastructure, construction, and financial services sectors are increasingly integrating ESG reporting into enterprise operations. Strategic partnerships, technology investments, and government-supported sustainability programs are accelerating market development. Businesses increasingly prioritize long-term transparency and operational resilience, positioning the region as an emerging strategic destination for ESG software expansion.

United States – 34% Market Share: Leads globally due to extensive enterprise adoption, strong sustainability disclosure requirements, and advanced digital infrastructure.

Germany – 11% Market Share: Benefits from rigorous sustainability regulations, strong industrial participation, and widespread enterprise investment in compliance and reporting technologies.

The ESG Software Market is characterized by intense competition between global platform leaders such as Workiva, Sphera, Diligent, Intelex, and Novisto, and specialized regional sustainability reporting providers competing through customization and regulatory expertise. The top five players collectively control approximately 42% of market activity, reflecting a moderately consolidated structure where platform capability increasingly outweighs price competition.

Competition is centered on AI-driven analytics, reporting automation, compliance coverage, and integration depth. Advanced ESG automation platforms reduce reporting workloads by nearly 40%, while cloud-native systems improve deployment efficiency by approximately 35% compared with legacy architectures. Large vendors are aggressively expanding through acquisitions, ecosystem partnerships, and vertical integration strategies that combine ESG reporting, risk management, and sustainability intelligence into unified platforms.

The competitive landscape is rapidly shifting toward AI-enabled sustainability intelligence and real-time disclosure management. Regulatory complexity is accelerating consolidation as enterprises favor scalable platforms with multi-framework compliance capabilities. The primary entry barrier remains enterprise-grade data integration and regulatory expertise. Winning requires superior automation, audit-ready data governance, deep compliance coverage, and scalable AI-driven decision intelligence rather than standalone reporting functionality.

Sphera

Diligent

Novisto

Intelex Technologies

Enablon

Cority

Benchmark ESG

EcoVadis

NAVEX

VelocityEHS

OneTrust

Position Green

Greenly

AI-driven sustainability intelligence has become the most influential technology layer within the ESG Software Market. More than 62% of new enterprise deployments now include AI-powered reporting automation, materiality analysis, or emissions forecasting capabilities. These systems improve reporting accuracy by approximately 40% while reducing manual compliance workloads by nearly 35%. Organizations increasingly deploy AI models to automate disclosure mapping, supplier risk assessment, and sustainability benchmarking across multiple reporting frameworks.

Cloud-native ESG platforms continue replacing legacy on-premises systems as enterprises prioritize scalability and regulatory agility. Compared with traditional spreadsheet-based reporting environments, integrated cloud platforms improve data accessibility by nearly 45% and accelerate reporting cycles by approximately 38%. Real-time sustainability dashboards and API-based enterprise integrations are becoming standard requirements among multinational organizations seeking continuous ESG monitoring.

A major disruptive shift is occurring through generative AI and predictive sustainability analytics. Advanced platforms now automate disclosure drafting, identify reporting inconsistencies, and forecast climate-related operational risks. Companies with mature ESG analytics environments report approximately 30% faster executive decision-making and stronger compliance preparedness. Large enterprises and financial institutions benefit most because they manage highly complex reporting structures and stakeholder requirements.

Between 2026 and 2028, ESG software technology will increasingly converge with enterprise risk management, supply-chain intelligence, and financial planning systems. Organizations acting early on AI-enabled sustainability ecosystems will secure stronger operational visibility, regulatory resilience, and long-term competitive differentiation as reporting complexity continues expanding globally.

January 2024 – Sphera acquired SupplyShift to strengthen supply-chain sustainability intelligence and supplier traceability capabilities. The transaction expanded access to a network of more than 100,000 suppliers, significantly improving ESG visibility across procurement ecosystems and strengthening enterprise risk management capabilities. [Supply Chain Expansion] Source: www.sphera.com

March 2025 – Novisto partnered with GIST Impact to launch advanced double materiality assessment capabilities powered by impact valuation data and AI-driven sustainability intelligence. The collaboration enhanced climate-risk analysis and sustainability reporting coverage, helping enterprises align with more than 30 reporting taxonomies. [Materiality Intelligence]

May 2025 – Novisto secured USD 27 million in Series C funding to accelerate global ESG software expansion across Europe, APAC, and the Middle East. The investment supports platform scaling, AI development, and enterprise sustainability reporting modernization amid increasing regulatory complexity. [Global Scaling Push]

September 2025 – Workiva introduced agentic AI capabilities within its sustainability, finance, and governance platform, enabling automated disclosure analysis and reporting workflows. The company reported that nearly two-thirds of practitioners still struggle with governance-quality data, making automation a major operational advantage. [Agentic ESG Automation]

This ESG Software Market report provides comprehensive coverage across deployment models, enterprise applications, end-user industries, regional demand patterns, and emerging sustainability intelligence technologies. The analysis evaluates cloud-based and on-premises platforms, ESG reporting systems, carbon management solutions, governance monitoring tools, supply-chain sustainability applications, and integrated compliance management ecosystems. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, enabling detailed comparison of adoption dynamics, regulatory influence, and enterprise deployment strategies.

The report delivers extensive analytical depth through evaluation of more than 10 major technology providers, multiple application environments, and region-specific adoption patterns. Approximately 68% of current deployments are concentrated within cloud-native environments, while over 60% of large-enterprise implementations increasingly integrate AI-driven analytics and reporting automation. The study also assesses supplier transparency platforms, predictive sustainability intelligence systems, and real-time ESG monitoring technologies that are reshaping enterprise sustainability operations.

From a strategic perspective, the report supports investment planning, market entry evaluation, product positioning, partnership development, and competitive benchmarking. It highlights emerging technology categories, evolving enterprise purchasing behavior, and forward-looking adoption shifts expected between 2026 and 2033, helping decision-makers identify high-priority growth opportunities, technology investment areas, and long-term competitive positioning strategies within the evolving ESG software ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 124.0 Million |

| Market Revenue (2033) | USD 536.7 Million |

| CAGR (2026–2033) | 20.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Workiva; Sphera; Diligent; Novisto; Intelex Technologies; Enablon; Cority; Benchmark ESG; EcoVadis; NAVEX; VelocityEHS; OneTrust; Position Green; Greenly |

| Customization & Pricing | Available on Request (10% Customization Free) |