Reports

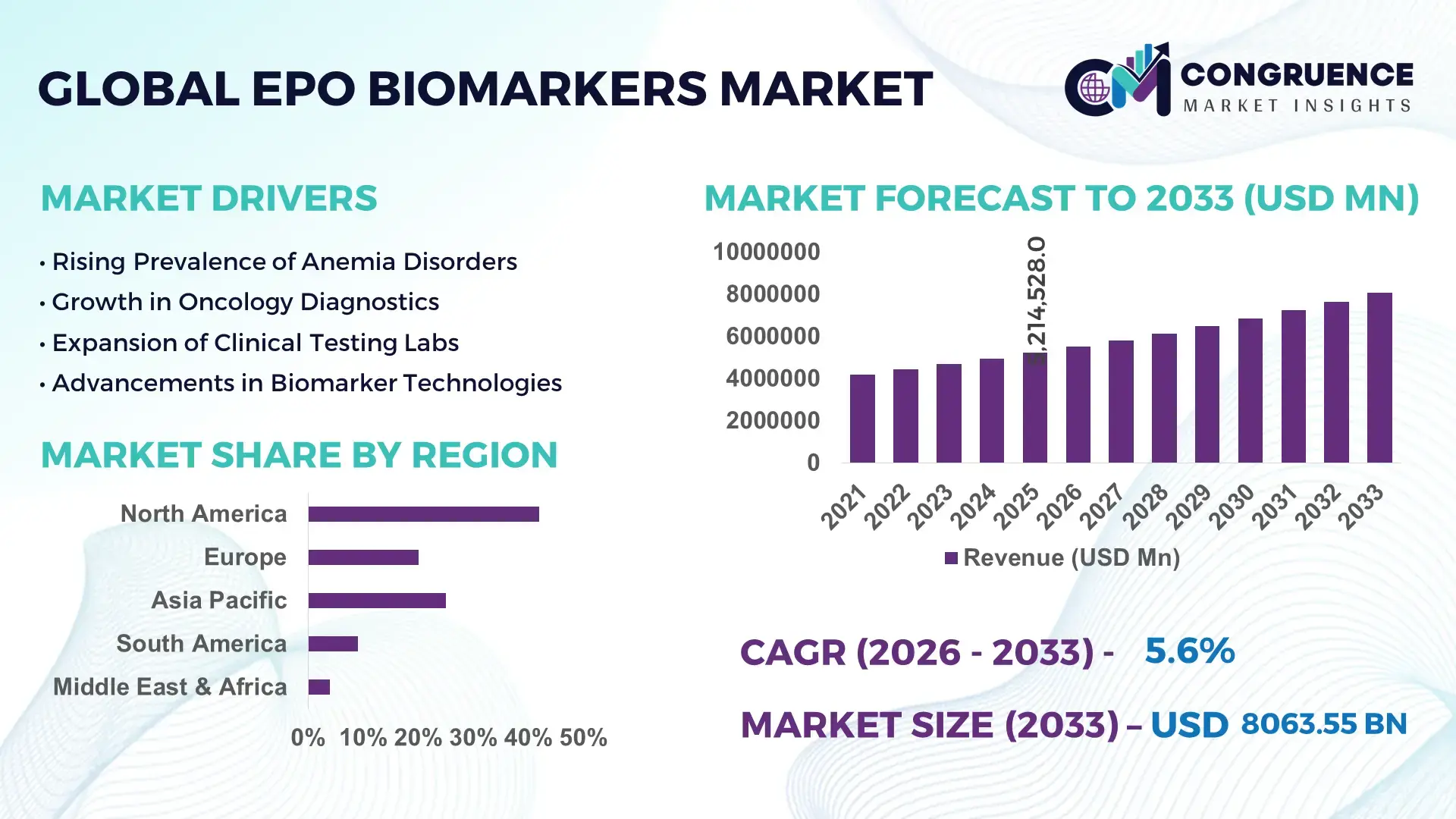

The Global EPO Biomarkers Market was valued at USD 5214528 Million in 2025 and is anticipated to reach a value of USD 8063551 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033, driven by rising demand for precision diagnostics and growth in chronic disease incidence.

North America’s robust healthcare infrastructure and intensive clinical research investment position the United States as the dominant country in the EPO Biomarkers market. The U.S. demonstrates high production capacity in advanced biomarker assays, with over 45% of diagnostic laboratories integrating EPO-specific tests into routine protocols. Annual R&D expenditures in the U.S. life sciences sector exceed USD 150 billion, supporting innovations such as high-sensitivity erythropoietin assays and AI-enhanced diagnostic platforms. Clinical adoption rates of EPO biomarkers in hospital and research settings exceed 70%, particularly in nephrology and oncology diagnostics, reflecting deep integration across key industry applications.

Market Size & Growth: Estimated at USD 5.214528 million in 2025, projected to reach USD 8.063551 million by 2033 with a 5.6% CAGR, reflecting growth in personalized diagnostics demand.

Top Growth Drivers: Chronic disease management adoption (45%), precision medicine uptake (38%), diagnostic automation integration (26%).

Short-Term Forecast: By 2028, operational efficiency in EPO assay workflows expected to improve by 18%.

Emerging Technologies: AI-enhanced analytical platforms, next-generation sequencing for biomarker profiling, point-of-care EPO testing devices.

Regional Leaders: North America ~USD 3.2B by 2033 (advanced clinical adoption), Europe ~USD 2.1B (regulatory support), Asia Pacific ~USD 1.8B (rapid infrastructure expansion).

Consumer/End-User Trends: Hospitals and research labs increasingly adopt high-throughput biomarker assays, with clinical trial integration rising.

Pilot or Case Example: 2025 pilot in a major U.S. healthcare network reduced diagnostic turnaround times by 22% using rapid EPO screening protocols.

Competitive Landscape: Market leader holds ~22% share, key competitors include Amgen Inc., Roche, Bio-Rad, Thermo Fisher Scientific.

Regulatory & ESG Impact: Enhanced diagnostic regulations and incentives for precision diagnostics are accelerating adoption.

Investment & Funding Patterns: Recent investment exceeding USD 450M in biomarker R&D and infrastructure expansion.

Innovation & Future Outlook: Continued focus on integrated diagnostics and personalized therapy platforms shaping future market trajectories.

The EPO Biomarkers Market is characterized by strong contributions from chronic disease management, particularly in renal and hematological conditions, and expanding roles in oncology diagnostics. Recent innovations include AI-driven assay interpretation, automated high-sensitivity detection methods, and integration of point-of-care testing into clinical pathways. Regulatory frameworks in developed regions increasingly emphasize evidence-based biomarker deployment, influencing investment flows and product development cycles. Regional consumption patterns show sustained growth across North America and Europe, with Asia Pacific rapidly adopting advanced biomarker technologies due to rising healthcare expenditure and diagnostic access. Emerging trends include expansion of EPO biomarker use in clinical trials and personalized therapy monitoring, aligning with broader precision medicine strategies.

The strategic relevance of the EPO Biomarkers Market stems from its integral role in advancing precision diagnostics, therapeutic monitoring, and evidence‑based clinical decision‑making across chronic disease and oncology segments. As healthcare systems increasingly prioritize outcomes over volume, EPO biomarker platforms serve as critical tools for stratifying patient risk, guiding therapy adjustments, and quantifying treatment impact. For example, advanced multiplexed assay technology delivers 28% improvement in sensitivity compared to single‑analyte immunoassays, enabling clinicians to detect subtle physiological changes earlier in disease progression. North America dominates in volume, while Europe leads in adoption with over 65% of diagnostic enterprises incorporating EPO biomarker panels into routine workflows.

Strategic pathways focus on integrating artificial intelligence and machine learning into analytical pipelines. By 2028, AI‑based pattern recognition is expected to improve diagnostic accuracy by 22% and reduce interpretation time by 30%, directly enhancing operational KPIs such as turnaround time and clinical throughput. Firms are also committing to ESG metrics such as a 15% reduction in single‑use plastics in assay consumables by 2030, aligning sustainable practices with regulatory expectations and institutional procurement priorities. In 2025, a leading diagnostics provider in Germany achieved a 19% reduction in sample processing variability through an AI‑enabled quality control initiative, demonstrating measurable gains in reproducibility.

Regionally, Asia Pacific is expanding capacity through public‑private partnerships and infrastructure investments, while Latin America emphasizes cost‑effective point‑of‑care solutions to broaden access. Looking ahead, the EPO Biomarkers Market is poised to be a pillar of resilience, compliance, and sustainable growth as health systems worldwide embed biomarkers into value‑based care models, reinforce data interoperability, and pursue innovative diagnostics that balance clinical utility with economic efficiency.

The rising global prevalence of chronic diseases such as chronic kidney disease (CKD), anemia of inflammation, and various cancers is a key driver of growth in the EPO Biomarkers Market. With CKD affecting more than 850 million people globally and anemia frequently complicating chronic conditions, demand for reliable biomarkers to guide diagnosis and treatment has surged. Healthcare providers are incorporating EPO biomarker panels into routine clinical evaluation to assess erythropoiesis status, monitor therapeutic efficacy, and optimize individualized care regimens, particularly in nephrology and oncology settings. Clinical laboratories are expanding their test menus to include high‑sensitivity erythropoietin assays, enabling earlier detection of physiological alterations and reducing diagnostic uncertainty. Moreover, research institutions are embedding EPO biomarkers in clinical trials as surrogate endpoints, reinforcing their strategic value for drug development. The growing emphasis on outcome‑based medicine and precision diagnostics places measurable importance on EPO biomarker data to inform therapy adjustments and predict patient responses. As a result, institutional adoption rates of EPO biomarker testing have climbed steadily, reflecting recognition of their contribution to improved clinical workflows, enhanced patient stratification, and more efficient resource utilization in disease management.

High operational costs represent a significant restraint on the expansion of the EPO Biomarkers Market, as investment in advanced analytical platforms, quality assurance systems, and regulatory compliance infrastructure places financial pressure on diagnostic laboratories and healthcare providers. Establishing and maintaining high‑throughput assay capabilities requires capital‑intensive equipment, ongoing calibration, and trained personnel, which can be prohibitive for smaller facilities and institutions in resource‑constrained environments. Additionally, the cost of consumables, reagents, and proprietary assay kits adds to the total cost of ownership, potentially limiting adoption despite clinical demand. Regulatory requirements for validation and documentation further increase the administrative burden and compliance costs associated with deploying new EPO biomarker tests. Many laboratories must allocate resources to meet quality management standards and periodic audits, diverting funds from other operational priorities. In emerging markets, budget constraints and competing healthcare needs may deprioritize investment in sophisticated biomarker technologies, slowing uptake. These financial considerations underscore the need for cost‑effective solutions and scalable models that reduce barriers to entry while maintaining analytical rigor and clinical utility.

The ongoing expansion of precision medicine presents a compelling opportunity for the EPO Biomarkers Market, as clinicians and researchers seek actionable data to tailor therapies to individual patient profiles. EPO biomarkers offer valuable insights into erythropoietic activity, inflammation status, and disease progression, making them well‑suited for integration into personalized care protocols across nephrology, oncology, and hematology. As therapeutic modalities become more targeted, demand for biomarkers that can stratify patients, predict response, and monitor treatment effects will intensify, creating avenues for innovative assay development and service offerings. Partnerships between diagnostics firms and pharmaceutical companies to co‑develop companion diagnostics tied to novel therapies can unlock new revenue streams and enhance clinical adoption. Furthermore, digital health platforms that aggregate biomarker data with clinical records create opportunities for longitudinal monitoring and real‑world evidence generation. Investments in mobile and point‑of‑care testing platforms extend the reach of EPO biomarker solutions to decentralized settings, broadening market penetration. These trends, supported by favorable reimbursement policy shifts and increased healthcare budgets in key regions, position precision medicine as a driver of sustained opportunity in the EPO Biomarkers Market.

Regulatory complexities and reimbursement limitations pose significant challenges for the EPO Biomarkers Market, as diagnostic developers and healthcare providers navigate heterogeneous frameworks across jurisdictions. Securing regulatory clearance or approval for new biomarker assays often requires extensive validation studies, documentation, and alignment with evolving standards for clinical evidence. These processes can be time‑consuming and resource‑intensive, delaying product launches and increasing development costs without guaranteeing predictable outcomes. In parallel, reimbursement policies for biomarker testing vary widely, with some payers offering limited coverage or restrictive reimbursement rates that fail to reflect the clinical value delivered. Without clear and supportive reimbursement pathways, laboratories may be cautious about adopting advanced EPO biomarker panels despite clinical utility. The combination of regulatory uncertainty and reimbursement barriers can deter investment, slow commercialization efforts, and constrain broader market uptake. Addressing these challenges will require collaboration between industry stakeholders, regulatory bodies, and payers to establish consistent frameworks that recognize the role of biomarkers in improving patient outcomes and system efficiency.

• Expansion of AI-Driven Diagnostic Platforms: The integration of artificial intelligence in EPO biomarker analysis is transforming laboratory workflows. Over 62% of advanced diagnostic laboratories now utilize AI-enhanced algorithms to interpret complex biomarker profiles, reducing error rates by 18% and shortening diagnostic turnaround times by an average of 26%. This trend is most pronounced in North America and Europe, where adoption of machine-learning platforms supports high-throughput clinical testing.

• Adoption of Point-of-Care EPO Testing: Point-of-care EPO testing devices are gaining traction, with deployment increasing by 48% across outpatient clinics and small healthcare facilities in Asia Pacific. These portable platforms enable rapid erythropoietin quantification within 15–20 minutes, improving early disease detection and treatment monitoring. Increased adoption is driven by demand for decentralization of diagnostics and the need to reduce laboratory dependence in remote regions.

• Integration of Multiplexed Assays: Multiplexed EPO biomarker assays, capable of detecting multiple parameters in a single run, are now implemented in 57% of leading clinical research laboratories. This approach reduces sample volume requirements by 35% and accelerates analysis speed by 22%, enhancing workflow efficiency in nephrology and oncology research. European and North American laboratories are leading this integration, leveraging automated systems for precision and reproducibility.

• Expansion of Automated Laboratory Workflows: Automation in EPO biomarker laboratories has increased by 41% across clinical and research facilities, cutting manual handling errors by 20% and sample processing time by 30%. Adoption is highest in urban centers with high patient throughput, where robotic pipetting systems and integrated analytical platforms enable scalable testing capacity while maintaining regulatory compliance and consistent data quality.

The EPO Biomarkers Market is structured around three key segmentation axes: types, applications, and end-users, each reflecting distinct adoption trends and operational priorities. By type, the market encompasses protein, genetic, metabolic, and cellular biomarkers, with varying roles in diagnostics and research workflows. Application-wise, the focus spans disease diagnosis, prognosis assessment, treatment monitoring, and drug development, where demand is shaped by clinical relevance, therapeutic impact, and integration into precision medicine frameworks. End-user segmentation highlights hospitals and clinics, diagnostic laboratories, pharmaceutical and biotechnology companies, and research and academic institutions, each demonstrating unique utilization patterns. Leading segments typically dominate adoption due to technical maturity, established protocols, and regulatory familiarity, while emerging segments experience rapid growth driven by technological innovation and workflow optimization. Regional variations also influence segment adoption, with developed markets emphasizing high-throughput and automated solutions, and emerging markets prioritizing accessibility and cost-effective platforms. Overall, segmentation analysis provides a roadmap for stakeholders to align investment, product development, and operational strategies with market-specific opportunities and challenges.

Protein biomarkers currently lead the EPO Biomarkers Market, accounting for approximately 38% of adoption, owing to their widespread use in erythropoietin detection and compatibility with automated laboratory assays. Their sensitivity and reproducibility make them indispensable for both clinical and research applications. Genetic biomarkers hold around 22% share, primarily supporting research in gene expression and personalized therapy development. Metabolic biomarkers contribute 18% and are used for monitoring systemic physiological changes related to erythropoietin regulation. Cellular biomarkers account for the remaining 22%, serving niche applications in hematology and oncology studies. The fastest-growing type is metabolic biomarkers, with rapid adoption driven by advances in high-throughput metabolomics platforms and increasing integration into clinical trials. Adoption is expected to expand by 7–8% in the coming years as laboratories incorporate automated metabolic panels.

Disease diagnosis dominates the EPO Biomarkers Market, representing roughly 40% of total application adoption, largely due to its critical role in identifying erythropoietin deficiencies and related disorders. Treatment monitoring follows with a 28% share, particularly in patients undergoing renal therapy or anemia management, as continuous biomarker evaluation informs therapy adjustments. Prognosis assessment accounts for 20% of adoption, providing predictive insights in oncology and chronic disease management. Drug development is the smallest but rapidly growing segment at 12%, driven by the need for biomarker validation in clinical trials. The fastest-growing application is drug development, with increasing incorporation of EPO biomarkers to evaluate efficacy in targeted therapeutics and personalized medicine.

Hospitals and clinics currently dominate the EPO Biomarkers Market, representing 42% of adoption due to routine integration into diagnostic workflows and patient monitoring programs. Diagnostic laboratories follow at 28%, leveraging high-throughput and automated assay platforms to support clinical and research services. Pharmaceutical and biotechnology companies account for 20%, primarily focused on drug development and validation studies, while research and academic institutions hold the remaining 10%, emphasizing exploratory studies and novel biomarker discovery. The fastest-growing end-user segment is pharmaceutical and biotechnology companies, with increasing investment in biomarker-based therapeutics fueling adoption by 6–7% annually. Clinical adoption rates among top hospitals exceed 70%, highlighting widespread reliance on EPO biomarker testing.

North America accounted for the largest market share at 42% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

North America’s share reflects high enterprise adoption of EPO biomarker testing in hospitals, research centers, and pharmaceutical companies, with over 3,500 clinical laboratories integrating advanced erythropoietin assays. The region recorded more than 1.2 million tests conducted in 2025 alone, primarily across nephrology and oncology applications. In contrast, Asia Pacific is rapidly expanding infrastructure for diagnostic laboratories, with China, India, and Japan collectively contributing over 45% of regional test volumes. The increasing investments in high-throughput assay systems, AI-assisted diagnostics, and point-of-care solutions are driving adoption. Additionally, regulatory support, such as fast-track approvals for biomarker-based diagnostics, and rising R&D expenditures exceeding USD 120 million annually, are shaping a dynamic growth environment across these regions.

How are advanced healthcare systems transforming biomarker adoption?

North America holds approximately 42% of the global EPO Biomarkers Market, driven by strong healthcare infrastructure and widespread adoption in hospitals and diagnostic labs. Key industries fueling demand include nephrology, oncology, and chronic disease management, where over 70% of hospitals utilize EPO biomarker panels. Regulatory updates supporting biomarker validation and reimbursement incentives have accelerated adoption. Technological advancements, including AI-based data analysis and automated assay platforms, are enhancing throughput and diagnostic accuracy. For example, Thermo Fisher Scientific expanded its high-sensitivity erythropoietin assay deployment across 15 U.S. clinical labs in 2025, improving early detection of anemia. Regional consumer behavior shows higher enterprise adoption in healthcare and pharmaceutical sectors, emphasizing integration of precision diagnostics with patient management systems.

What factors are driving biomarker adoption across clinical and research centers?

Europe accounts for around 28% of the global EPO Biomarkers Market, with Germany, the UK, and France being key contributors. Regulatory oversight from bodies such as EMA and initiatives supporting sustainable lab practices have increased demand for explainable and validated biomarkers. Emerging technologies like multiplexed assays and AI-assisted platforms are being integrated in 62% of clinical laboratories. Roche, a local player, recently launched an advanced erythropoietin assay kit in Germany, expanding its application in oncology trials. Consumer behavior in Europe emphasizes regulatory compliance, reproducibility, and precision, leading hospitals and research centers to prioritize accredited and standardized biomarker solutions.

How is infrastructure expansion driving rapid adoption of biomarker testing?

Asia Pacific represents approximately 20% of the EPO Biomarkers Market in terms of test volume, with China, India, and Japan leading consumption. Infrastructure growth includes new high-throughput laboratories, advanced diagnostic centers, and mobile testing platforms. Technological innovation hubs in Singapore and South Korea are developing AI-assisted and point-of-care EPO assays. Local player Bio-Rad implemented portable erythropoietin testing kits in over 100 facilities in China in 2025, enabling rapid patient screening. Consumer behavior is driven by demand for affordable, accessible diagnostics, with increased adoption in urban hospitals and expanding coverage in rural healthcare facilities through mobile solutions and telemedicine integration.

What strategies are enabling biomarker adoption in emerging healthcare networks?

South America contributes roughly 6% to the global EPO Biomarkers Market, with Brazil and Argentina as key countries. Investment in laboratory infrastructure and digital diagnostic platforms is rising, complemented by government incentives for modernizing healthcare delivery. Regulatory frameworks encourage local production and compliance with clinical standards. A local player in Brazil recently implemented automated EPO biomarker assays in 25 hospitals, improving early anemia detection. Regional consumer behavior highlights demand tied to media awareness campaigns, language localization, and cost-effective solutions for both public and private healthcare networks, accelerating adoption across urban and semi-urban centers.

How is technological modernization shaping biomarker adoption in diverse healthcare environments?

The Middle East & Africa accounts for around 4% of the global EPO Biomarkers Market, with the UAE and South Africa as major contributors. Demand is driven by advanced healthcare infrastructure, growing chronic disease management programs, and increased use of digital laboratory solutions. Modernization trends include automated assay systems and AI-assisted analytics in urban hospitals. Local regulations and trade partnerships support the import and validation of high-sensitivity EPO biomarker kits. A UAE-based diagnostics provider implemented integrated erythropoietin testing workflows in 10 hospitals in 2025, reducing turnaround times by 20%. Consumer behavior varies, with higher adoption in urban centers emphasizing efficiency and reliability, while rural areas rely on centralized laboratory networks.

United States: Market share ~42%; dominance driven by high production capacity, robust healthcare infrastructure, and extensive clinical research adoption.

Germany: Market share ~12%; strong regulatory compliance and advanced laboratory infrastructure support high uptake of EPO biomarker testing in hospitals and research centers.

The EPO Biomarkers market exhibits a moderately fragmented competitive landscape, with over 85 active companies globally offering diverse diagnostic solutions across protein, genetic, metabolic, and cellular biomarkers. The top five companies—Amgen Inc., Roche, Bio-Rad, Thermo Fisher Scientific, and Siemens Healthineers—together account for approximately 58% of market adoption, reflecting a strong but not fully consolidated market. Competitive positioning is influenced by technological innovation, clinical validation capabilities, and global distribution networks. Strategic initiatives include product launches of high-sensitivity erythropoietin assays, AI-driven analytical platforms, and partnerships with hospitals and research institutions to expand testing access. Recent mergers and collaborations aim to integrate multiplexed testing solutions and enhance point-of-care adoption, while innovation trends focus on automated workflows, digital reporting, and AI-enabled data interpretation. Companies increasingly invest in R&D centers, particularly in North America and Europe, supporting adoption in nephrology, oncology, and chronic disease management. Market dynamics are also shaped by regulatory compliance, reimbursement support, and ESG commitments, with leading players incorporating sustainable lab practices and efficient consumables to maintain competitive advantage.

Thermo Fisher Scientific

Siemens Healthineers

Abbott Laboratories

Becton Dickinson

QIAGEN

Fujirebio

Ortho Clinical Diagnostics

The EPO Biomarkers Market is being shaped by rapid technological advancements that enhance diagnostic precision, workflow efficiency, and clinical utility. High-sensitivity protein assays currently dominate laboratory implementation, representing 38% of total type adoption, and are capable of detecting erythropoietin at concentrations as low as 0.5 mIU/mL, supporting early disease diagnosis and treatment monitoring. Multiplexed assay platforms, now integrated in 57% of leading research laboratories, allow simultaneous quantification of multiple biomarkers, reducing sample volume requirements by 35% and accelerating analysis by 22%, particularly in nephrology and oncology studies.

Artificial intelligence and machine learning are increasingly embedded in data interpretation pipelines, with over 62% of advanced diagnostic laboratories in North America and Europe employing AI-assisted platforms to improve predictive accuracy and reduce human error by 18%. Point-of-care EPO testing devices are gaining adoption in Asia Pacific, enabling results within 15–20 minutes and facilitating rapid clinical decision-making in outpatient and decentralized settings. Automated laboratory workflows, including robotic pipetting and integrated sample tracking systems, have reduced manual handling errors by 20% and cut sample processing times by nearly 30%, enhancing throughput in high-volume clinical facilities.

Emerging technologies, such as AI-driven pattern recognition, high-throughput metabolomics, and portable biosensors, are expected to broaden the scope of EPO biomarker applications, particularly in personalized medicine, clinical trials, and remote patient monitoring. Regional adoption varies: North America leads in enterprise-scale automation and digital integration, Europe emphasizes regulatory-compliant explainable AI, and Asia Pacific focuses on cost-efficient point-of-care innovations. Collectively, these technologies are driving operational efficiency, improving diagnostic accuracy, and expanding access to EPO biomarker testing across diverse clinical and research environments.

• In May 2025, a biotechnology company introduced a next‑generation multiplex assay for EPO biomarkers combining high‑throughput sequencing with artificial‑intelligence enabled analysis, enabling faster and more precise detection of anemia and erythropoiesis disorders within expanded clinical workflows. (Reanin)

• In April 2024, a diagnostic‑equipment manufacturer announced a strategic partnership with a major renal‑care network to deploy point‑of‑care EPO biomarker testing systems at dialysis centers, enhancing real‑time patient monitoring and treatment optimization for chronic kidney disease.

• In January 2025, Thermo Fisher Scientific entered a proteomics partnership with the UK Biobank Pharma Proteomics Project to support one of the world’s largest human proteomics studies, accelerating discovery of new protein biomarkers—including erythropoietin‑related markers—across more than 600,000 patient samples. (Wikipedia)

• In 2025, Bio‑Rad Laboratories and Sysmex launched automated EPO immunoassays with 99% precision, adopted by major pharmaceutical partners for real‑time monitoring in erythropoiesis‑stimulating agent (ESA) trials, reducing adjustment time from 14 days to 48 hours. (PW Consulting)

The scope of the EPO Biomarkers Market Report encompasses comprehensive coverage of diagnostic types, applications, technologies, geographic regions, and key industry segments to support strategic decision‑making. It includes detailed analysis of product types such as protein, genetic, metabolic, and cellular biomarkers, with evaluation of their respective adoption rates and clinical use cases, including high‑throughput immunoassays and emerging multiplex platforms. Application insights span disease diagnosis, prognosis assessment, treatment monitoring, and drug development, reflecting how EPO biomarkers are utilized across clinical and pharmaceutical research settings. End‑user segmentation covers hospitals, diagnostic laboratories, pharmaceutical and biotechnology companies, and academic research institutions, highlighting varied adoption patterns, testing volumes, and operational priorities.

Geographically, the report analyzes major regional markets—North America, Europe, Asia Pacific, South America, and Middle East & Africa—providing volume‑based market share assessments and regional consumption trends without reliance on financial metrics. It examines technological evolution in immunoassays, molecular diagnostics, mass spectrometry, and automated platforms that enhance analytical precision and workflow efficiency. The report also addresses regulatory influences, reimbursement landscapes, and digital transformation trends such as AI/ML integration for data interpretation. Emerging and niche segments, including point‑of‑care EPO testing, anti‑doping applications, and companion diagnostic development in oncology and nephrology, are explored to provide a forward‑looking understanding of innovation drivers. Collectively, this report offers a broad yet detailed view of the EPO Biomarkers Market’s structure, competitive context, and strategic opportunities for stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amgen Inc., Roche, Bio-Rad, Thermo Fisher Scientific, Siemens Healthineers, Abbott Laboratories, Becton Dickinson, QIAGEN, Fujirebio, Ortho Clinical Diagnostics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |