Reports

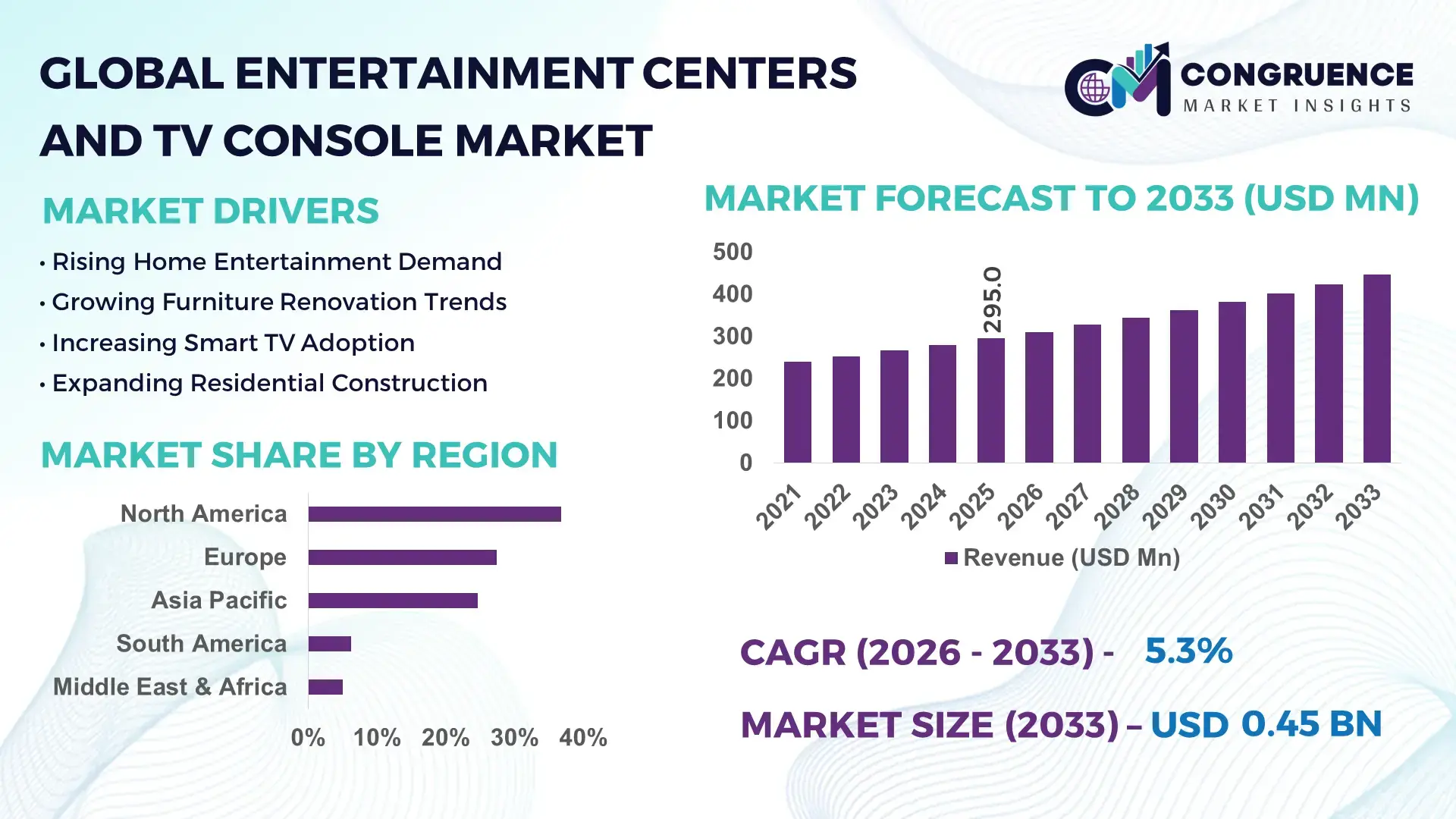

The Global Entertainment Centers and TV Console Market was valued at USD 295.0 Million in 2025 and is anticipated to reach a value of USD 445.9 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033. Growth is driven by rising adoption of large-format smart TVs above 65 inches, expanding home entertainment investments, and increasing demand for multifunctional storage-integrated furniture across residential and hospitality environments.

The United States dominates the market with approximately 31% of global demand, supported by over 82% smart TV household penetration and sustained residential renovation spending exceeding USD 500 billion annually. China follows with nearly 24% market participation, leveraging large-scale furniture manufacturing clusters and export capabilities. Following post-pandemic home improvement trends and supply-chain diversification initiatives, U.S. premium console adoption outpaces China by nearly 18%, while China maintains a production cost advantage exceeding 20% across major furniture categories.

Strategically, manufacturers that combine modular design, premium materials, and integrated smart-home compatibility are securing stronger positioning in high-value consumer segments.

Market Size & Growth: USD 295.0 Million in 2025, projected to reach USD 445.9 Million by 2033 at 5.3% CAGR, supported by rising 65-inch+ TV installations and premium home entertainment upgrades.

Top Growth Drivers: Smart TV penetration (+82%), residential remodeling activity (+11%), and multifunctional furniture adoption (+16%) continue accelerating purchasing decisions.

Short-Term Forecast: By 2028, modular manufacturing and digital inventory systems are expected to reduce fulfillment lead times by nearly 15%.

Emerging Technologies: AI-assisted room planning, AR-based furniture visualization, and advanced engineered wood materials improve consumer engagement and product customization.

Regional Leaders: North America (~USD 125 Million), Asia-Pacific (~USD 94 Million), and Europe (~USD 78 Million) benefit from premium furniture demand, urban housing growth, and omnichannel retail expansion.

Consumer/End-User Trends: More than 58% of buyers prioritize integrated cable management, hidden storage, and space-optimized entertainment furniture.

Pilot/Case Example: In 2024, major furniture retailers deploying AR visualization tools reported up to 22% higher online conversion rates.

Competitive Landscape: Top manufacturers collectively control approximately 35% of global sales, with key participants including Ashley Furniture, IKEA, Sauder, Bush Furniture, and Walker Edison.

Regulatory & ESG Impact: Sustainable wood sourcing initiatives increased certified-material utilization by over 28% across leading manufacturers.

Investment & Funding: More than USD 1.2 Billion in furniture manufacturing modernization and retail digitization investments supported capacity expansion and supply-chain resilience.

Innovation & Future Outlook: Smart-home-compatible consoles, modular configurations, and customizable premium designs are reshaping competitive differentiation globally.

The Entertainment Centers and TV Console Market continues to evolve through increasing demand from residential renovation projects, premium living spaces, and integrated smart-home environments. Manufacturers are introducing modular storage systems, engineered wood composites, and AR-enabled product visualization platforms to enhance customer engagement. Nearly 37% of new product launches now emphasize multifunctionality and space optimization. Simultaneously, global supply-chain realignment and localized sourcing strategies are strengthening production flexibility and inventory efficiency, creating a foundation for broader strategic market development.

The market is becoming strategically important as furniture manufacturers, retailers, and home improvement brands compete to capture rising consumer spending linked to connected living environments. The convergence of larger television formats, smart-home ecosystems, and multifunctional interior design preferences is transforming entertainment furniture from a basic furnishing category into a value-added consumer product segment. Supply-chain restructuring across Asia and North America is further influencing sourcing, manufacturing, and distribution strategies.

Technology adoption is creating measurable competitive advantages. AR-powered visualization platforms improve online purchase conversion rates by approximately 20–25% compared with traditional catalog-based selling methods, while automated manufacturing systems reduce production waste by nearly 15%. The United States leads premium product adoption and customization demand, whereas China maintains significant advantages in manufacturing scale and component sourcing efficiency. These differences are shaping distinct investment priorities across global markets.

Companies are increasingly deploying modular product portfolios and expanding direct-to-consumer channels to improve margins and customer retention. For example, leading furniture brands now integrate cable management systems, adjustable shelving, and smart-device compatibility into premium console offerings. Over the next two to three years, online furniture purchases are expected to account for more than 35% of category transactions, encouraging further investments in digital merchandising, logistics partnerships, and localized fulfillment networks. Organizations that align product innovation with operational agility will strengthen long-term competitive positioning.

The accelerating shift toward immersive home entertainment environments is strengthening demand for advanced entertainment centers and TV consoles. More than 82% of households in the United States now own smart TVs, while installations of televisions larger than 65 inches have increased by over 14% annually. As consumers invest in connected devices, gaming systems, and streaming infrastructure, furniture requirements increasingly emphasize storage integration, cable management, and modular functionality. The post-pandemic residential renovation cycle continues to support category expansion, particularly in suburban housing markets. In response, manufacturers are introducing configurable designs, premium finishes, and smart-home-compatible furniture solutions. A notable strategic insight is that multifunctionality now influences purchasing decisions more strongly than aesthetic preferences alone, prompting companies to prioritize product innovation and premium differentiation strategies.

Price fluctuations across engineered wood, MDF panels, hardware components, and logistics services continue to pressure industry profitability. Material input costs in major furniture manufacturing markets have experienced fluctuations exceeding 12% over recent procurement cycles, while international freight costs remain approximately 18% above pre-disruption benchmarks in several trade corridors. Dependence on concentrated supplier networks in China and Southeast Asia increases exposure to trade policy changes and shipping delays. These factors create challenges for inventory planning, pricing stability, and margin protection. To mitigate risks, manufacturers are diversifying sourcing networks, expanding regional supplier partnerships, and increasing local production capacity. An important operational insight is that firms with diversified procurement structures are achieving faster fulfillment consistency and stronger pricing resilience than competitors dependent on single-country supply chains.

The integration of connected technologies and digital commerce platforms is creating substantial market opportunities. More than 58% of consumers now research furniture purchases online before visiting stores, while AR-enabled shopping tools improve engagement rates by nearly 30%. Emerging innovations include wireless charging integration, IoT-compatible storage systems, and app-assisted furniture configuration platforms. Countries such as India and Vietnam are experiencing rapid growth in organized furniture retail, supported by urbanization rates exceeding 35% and expanding middle-income populations. Manufacturers are increasing investments in digital showrooms, product customization software, and strategic retail partnerships to capture these opportunities. A non-obvious advantage lies in data-driven product development, where consumer interaction analytics help optimize inventory planning and accelerate product launch cycles.

As the market shifts toward omnichannel distribution, maintaining operational consistency across physical stores, online platforms, and direct-to-consumer channels presents a growing challenge. Nearly 40% of furniture returns are associated with dimensional mismatches, assembly issues, or customer expectation gaps. Product customization demand has increased by approximately 22%, creating additional complexity in manufacturing workflows and inventory management. Large-format entertainment furniture also faces transportation efficiency constraints due to packaging size and handling requirements. Companies must invest in digital configuration tools, logistics optimization systems, and advanced forecasting capabilities to address these issues. A key strategic challenge is balancing customization with scalable production efficiency, as organizations that fail to standardize core components risk higher costs, longer lead times, and reduced competitiveness in increasingly sophisticated consumer markets.

Smart Integration Reshapes Designs Manufacturers are embedding wireless charging pads, concealed cable-routing systems, and smart-device docking modules into premium entertainment centers. Nearly 34% of newly launched products now feature integrated connectivity functions, while demand for smart-home-compatible furniture has increased by approximately 21% over the past two years. The expansion of connected living ecosystems is accelerating product redesign cycles, prompting companies to establish technology partnerships and develop modular platforms that support evolving consumer electronics without complete furniture replacement.

Modular Configurations Gain Momentum Consumer preference is shifting toward adaptable entertainment furniture capable of serving multiple room layouts and device configurations. Modular product sales have risen by nearly 27%, while urban apartment households account for over 40% of purchases in several major markets. Rising residential space constraints and changing housing patterns are driving adoption. Companies are responding by restructuring product portfolios around interchangeable storage units, adjustable shelving systems, and flat-pack manufacturing processes that reduce logistics costs by approximately 15%.

Localized Sourcing Strategies Expand Supply-chain diversification remains a significant operational priority following global logistics disruptions and trade-policy uncertainty. More than 30% of large furniture manufacturers have expanded regional supplier networks, reducing dependency on single-country sourcing models. Procurement lead times have improved by nearly 18% in localized production programs. A non-obvious impact is greater flexibility in managing seasonal inventory fluctuations, encouraging manufacturers to invest in nearshore partnerships, automated warehousing systems, and regional assembly capabilities.

Digital Furniture Commerce Accelerates Advanced visualization technologies are transforming purchasing workflows across the entertainment furniture category. Retailers deploying AR-based room planning tools report conversion improvements exceeding 22%, while online furniture transactions now represent approximately 35% of category sales. Labor shortages in physical retail and rising consumer preference for digital shopping experiences continue to reinforce this transition. Companies are scaling omnichannel platforms, integrating AI-assisted product recommendations, and enhancing fulfillment networks to shorten delivery timelines and improve customer retention.

Traditional Entertainment Centers remain the leading segment, accounting for approximately 41% of market demand due to superior storage capacity, integrated component organization, and suitability for large-screen home entertainment installations. Consumers continue to prefer full-scale entertainment units in detached housing environments where space constraints are less significant. Their ability to consolidate gaming consoles, audio systems, streaming devices, and decorative storage within a single structure supports sustained adoption. Manufacturers are strengthening this segment through premium materials, modular shelving enhancements, and smart-home compatibility features designed to increase long-term product relevance. TV Consoles represent the fastest-growing type, supported by increasing urbanization and demand for minimalist interior design concepts. Adoption within apartment-based households has increased by nearly 24%, while wall-mounted television installations have grown by approximately 19% across developed markets. Corner TV Stands maintain strategic relevance in compact living spaces, whereas Floating Entertainment Units are gaining traction among premium consumers seeking contemporary aesthetics and optimized floor utilization. Companies are increasingly prioritizing lightweight engineered materials, flat-pack construction, and customizable configurations to address evolving consumer preferences and maximize operational efficiency.

Residential applications represent the largest segment, contributing nearly 68% of total market demand due to ongoing home renovation activity, expanding smart-TV ownership, and increased investment in personalized entertainment spaces. Homeowners increasingly prioritize furniture solutions featuring storage optimization, cable management, and compatibility with connected entertainment ecosystems. The segment benefits from strong replacement cycles and growing adoption of larger television formats, particularly in North America and China. Manufacturers continue expanding product variety, customization options, and direct-to-consumer channels to strengthen household market penetration. Hospitality & Leisure Facilities constitute the fastest-growing application segment as hotels, serviced apartments, and premium vacation properties invest in upgraded guest-room entertainment infrastructure. Procurement activity within this segment has increased by approximately 18%, supported by property modernization programs and elevated guest experience requirements. Commercial Spaces maintain stable demand through office lounges, executive facilities, and employee engagement environments, while Institutional Facilities are gradually adopting durable entertainment furniture for healthcare, education, and community environments. Companies are responding with commercial-grade product lines, improved durability specifications, and project-based installation partnerships that address operational requirements across diverse deployment settings.

Households remain the dominant end-user group, accounting for approximately 72% of overall purchasing activity due to high deployment volumes, replacement demand, and continued investment in home entertainment environments. Growing ownership of smart televisions, gaming systems, and streaming devices is increasing demand for multifunctional entertainment furniture. Premium household purchases have expanded by nearly 16%, particularly among consumers seeking integrated storage, aesthetic enhancement, and smart-home compatibility. Manufacturers are responding through personalized product offerings, online configuration tools, and expanded omnichannel retail strategies designed to improve engagement and conversion rates. Hospitality Operators represent the fastest-growing end-user segment as accommodation providers modernize guest environments and differentiate service offerings. Procurement volumes among hotel chains and serviced apartment operators have increased by approximately 20%, supported by renovation programs and evolving customer expectations. Corporate Offices maintain demand for executive lounges, collaborative spaces, and employee recreation areas, while Institutional Buyers continue selective adoption in healthcare, educational, and public-sector environments. Companies are increasingly developing segment-specific product portfolios, volume-based pricing models, and strategic installation partnerships to strengthen market positioning and secure long-term procurement contracts.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America maintained market leadership through strong consumer spending on home improvement, high smart-TV penetration, and mature furniture retail infrastructure. The region represented approximately 36.8% of global demand, supported by widespread adoption of televisions exceeding 65 inches and growing investment in multifunctional living spaces. More than 58% of premium furniture purchases in the region now prioritize integrated storage and cable-management functionality. Retailers continue expanding AR-enabled product visualization and omnichannel fulfillment capabilities, improving customer conversion rates and inventory efficiency. Strategic partnerships between furniture manufacturers and home improvement retailers are accelerating product distribution while reducing fulfillment timelines by nearly 15%, strengthening operational competitiveness across the region.

United States Market Outlook: The United States serves as the primary growth engine for the regional market due to its large residential renovation sector, advanced retail ecosystem, and high smart-home adoption rates. More than 82% of households own at least one smart TV, creating sustained demand for entertainment furniture upgrades. Manufacturers increasingly focus on modular product lines, direct-to-consumer sales models, and premium customization options. Continued investment in digital commerce infrastructure and localized warehousing networks is improving delivery performance and supporting stronger consumer engagement across both urban and suburban markets.

Europe represents a significant share of global demand, supported by premium furniture consumption, sustainable sourcing initiatives, and growing preference for minimalist interior design. Approximately 27.4% of market activity is concentrated within the region, where certified wood utilization and circular-economy principles increasingly influence purchasing decisions. Furniture producers are integrating recycled materials and low-emission manufacturing processes into production workflows. More than 30% of major furniture suppliers have expanded regional sourcing partnerships to strengthen supply-chain resilience. Simultaneously, digital product configuration tools are streamlining procurement and reducing inventory complexity, allowing manufacturers to respond more efficiently to changing consumer preferences.

Germany Market Outlook: Germany remains the region’s most strategically important market due to its strong furniture manufacturing base, advanced logistics infrastructure, and leadership in sustainable production practices. The country accounts for a substantial share of European furniture exports and continues investing in automated production systems. Nearly 45% of furniture manufacturers have expanded digital manufacturing capabilities to improve production flexibility and reduce material waste. Strong consumer preference for durable, multifunctional furniture further supports demand for premium entertainment centers and technologically integrated TV console solutions.

Asia-Pacific is emerging as the fastest-expanding regional market, supported by large-scale furniture manufacturing ecosystems, rising urbanization, and expanding middle-income populations. The region contributes approximately 24.6% of global demand while accounting for a significantly larger share of furniture production capacity. Urban housing development and growing adoption of compact living solutions continue driving demand for modular and space-efficient entertainment furniture. Furniture exports from major manufacturing hubs remain strong, while localized production investments are improving operational flexibility. More than 35% of new furniture capacity additions announced across key manufacturing economies are focused on automation and export competitiveness.

China Market Outlook: China remains the dominant force within Asia-Pacific due to its extensive manufacturing infrastructure, integrated supplier networks, and global export leadership. The country produces a significant share of the world’s furniture output and benefits from strong economies of scale across engineered wood, hardware, and assembly operations. More than 50% of large furniture producers have adopted advanced automation technologies to improve production efficiency and quality consistency. Growing domestic demand for premium living-room furniture and smart-home-compatible products further strengthens China's strategic position within the market.

South America continues to experience steady market expansion as urban households invest in residential modernization and improved home entertainment environments. The region accounts for approximately 6.2% of global demand, with purchasing activity concentrated in metropolitan centers. Demand is increasingly driven by multifunctional furniture capable of maximizing space utilization within apartment-based housing. Retail modernization and e-commerce adoption are improving product accessibility, although logistics limitations and import dependency continue influencing pricing structures. Several manufacturers have expanded local assembly operations to reduce transportation costs and improve responsiveness to market demand, supporting stronger regional competitiveness.

Brazil Market Outlook: Brazil represents the largest and most influential market within South America, supported by its sizable consumer base and established furniture manufacturing sector. Residential renovation activity and rising adoption of digital retail channels are strengthening demand for entertainment furniture products. More than 40% of furniture purchases in major urban areas now involve online research before purchase decisions. Domestic manufacturers are increasing investments in localized production, product customization, and omnichannel distribution strategies to improve market penetration and reduce exposure to international supply-chain disruptions.

The Middle East & Africa market is supported by residential development projects, premium housing investments, and increasing consumer interest in modern living environments. The region contributes approximately 5.0% of global demand, with growth concentrated in countries pursuing large-scale urban development initiatives. High-end residential projects are driving demand for premium entertainment furniture, while retail sector modernization improves product availability. Investment in logistics infrastructure and organized retail channels is enhancing distribution efficiency. Several regional furniture distributors have expanded strategic partnerships with international manufacturers to strengthen product portfolios and improve market accessibility.

Saudi Arabia Market Outlook: Saudi Arabia remains the most strategically significant market within the region due to extensive residential development programs, expanding retail infrastructure, and ongoing economic diversification initiatives. Large-scale housing projects and smart-city investments are creating favorable conditions for furniture demand. More than 60% of new residential developments incorporate modern interior design standards that emphasize multifunctional living spaces. Retailers are expanding premium furniture offerings, while international manufacturers continue strengthening local partnerships and distribution networks to capitalize on rising consumer spending and modernization-driven purchasing activity.

The market is characterized by competition between global furniture leaders such as Ashley Furniture, IKEA, Sauder, Bush Furniture, and Walker Edison, versus regional manufacturers competing on pricing, localized production, and faster fulfillment. The top five players collectively account for approximately 34%–38% of global market activity, creating a moderately fragmented competitive structure. Competition is centered on customization, supply-chain efficiency, omnichannel retail capabilities, and modular product innovation. Companies deploying AR-based visualization tools report conversion improvements exceeding 20%, while flat-pack logistics models reduce transportation costs by nearly 15%. Premium brands compete through design integration and smart-home compatibility, whereas cost leaders focus on manufacturing scale and sourcing efficiency. Market participants are expanding retail footprints, strengthening supplier partnerships, and investing in digital commerce ecosystems. Ashley continues expanding international distribution networks, while IKEA is increasing planning-focused retail formats and modular product offerings. Supply-chain diversification and localized sourcing have become key competitive differentiators. The competitive shift is moving from product-only differentiation toward integrated customer experience and operational agility. Success increasingly depends on scalable manufacturing, rapid fulfillment, digital engagement, and adaptable product portfolios that align with evolving residential living patterns.

IKEA

Sauder Furniture

Bush Furniture

Walker Edison

Hülsta

Hooker Furnishings

Dorel Home

Whalen Furniture

Ameriwood Home

FLEXSTEEL Industries

Bernhardt Furniture Company

Lexington Home Brands

Riverside Furniture

Technology adoption is increasingly shaping product development and purchasing behavior across the entertainment furniture industry. AR-based room visualization platforms, AI-assisted furniture planning tools, and digital configuration systems are becoming standard features among leading retailers. More than 35% of online furniture buyers now interact with visualization tools before purchasing, while retailers using these technologies report conversion improvements exceeding 20%. These capabilities reduce product-return risks, improve buying confidence, and strengthen customer engagement throughout the purchasing process.

Emerging technologies are focused on smart functionality and manufacturing efficiency. Wireless charging integration, concealed connectivity hubs, automated cable-management systems, and IoT-compatible furniture components are gaining traction within premium product categories. Compared with conventional furniture manufacturing workflows, automated CNC production systems improve material utilization by approximately 12% and reduce fabrication errors by nearly 18%. Companies with advanced automation capabilities benefit from shorter production cycles, improved consistency, and stronger margin protection. Premium manufacturers and large-scale retailers are currently capturing the greatest advantages from these technological investments.

Between 2026 and 2028, competitive differentiation will increasingly depend on digital integration and production intelligence. AI-driven demand forecasting can improve inventory accuracy by nearly 15%, while modular manufacturing platforms reduce product development timelines by approximately 20% compared with traditional fixed-design approaches. Companies adopting smart design ecosystems, advanced visualization platforms, and automated production technologies will strengthen responsiveness, improve operational flexibility, and secure long-term competitive advantages as consumer expectations continue evolving.

April 2025 – IKEA launched the STOCKHOLM 2025 collection featuring 96 furniture and home furnishing products, its largest STOCKHOLM release to date. The expansion strengthened IKEA’s premium living-room portfolio and enhanced positioning in design-focused furniture categories globally. Source: www.ikea.com

June 2025 – Ashley Furniture opened its largest retail location in Las Vegas, combining an 88,000-square-foot showroom with a 218,000-square-foot warehouse. The facility exceeds the company’s average showroom footprint by approximately 57,000 square feet, strengthening fulfillment capacity and customer reach.

October 2024 – Sauder showcased new furniture concepts, technologies, and product innovations during its 90th anniversary exhibition at High Point Market. The initiative reinforced the company’s leadership in ready-to-assemble furniture and accelerated commercialization of next-generation furniture solutions.

April 2025 – IKEA introduced its first Plan & Order Point format in India through a 740-square-meter Bengaluru facility focused on personalized home planning and installation services. The initiative expands customer engagement capabilities while supporting localized furniture purchasing workflows.

The report provides comprehensive analysis of entertainment centers and TV console products across major types, applications, and end-user categories. Coverage includes entertainment centers, TV consoles, corner TV stands, and floating entertainment units, alongside demand evaluation across residential, hospitality, commercial, and institutional environments. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global market activity. The study also evaluates purchasing behavior, deployment patterns, retail channel evolution, and product innovation trends influencing market development.

The report further examines emerging technologies including AR-enabled visualization, AI-assisted furniture planning, modular manufacturing systems, and smart-home-compatible furniture integration. Analysis incorporates competitive positioning across leading manufacturers, operational benchmarking, supply-chain transformation, sourcing strategies, and digital commerce adoption. With over one-third of new product launches emphasizing multifunctionality and space optimization, the report supports investment planning, expansion prioritization, partnership evaluation, product development strategies, and long-term competitive decision-making across the 2026–2033 strategic planning horizon.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 295.0 Million |

| Market Revenue (2033) | USD 445.9 Million |

| CAGR (2026–2033) | 5.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ashley Furniture Industries; IKEA; Sauder Furniture; Bush Furniture; Walker Edison; Hülsta; Hooker Furnishings; Dorel Home; Whalen Furniture; Ameriwood Home; FLEXSTEEL Industries; Bernhardt Furniture Company; Lexington Home Brands; Riverside Furniture |

| Customization & Pricing | Available on Request (10% Customization Free) |