Reports

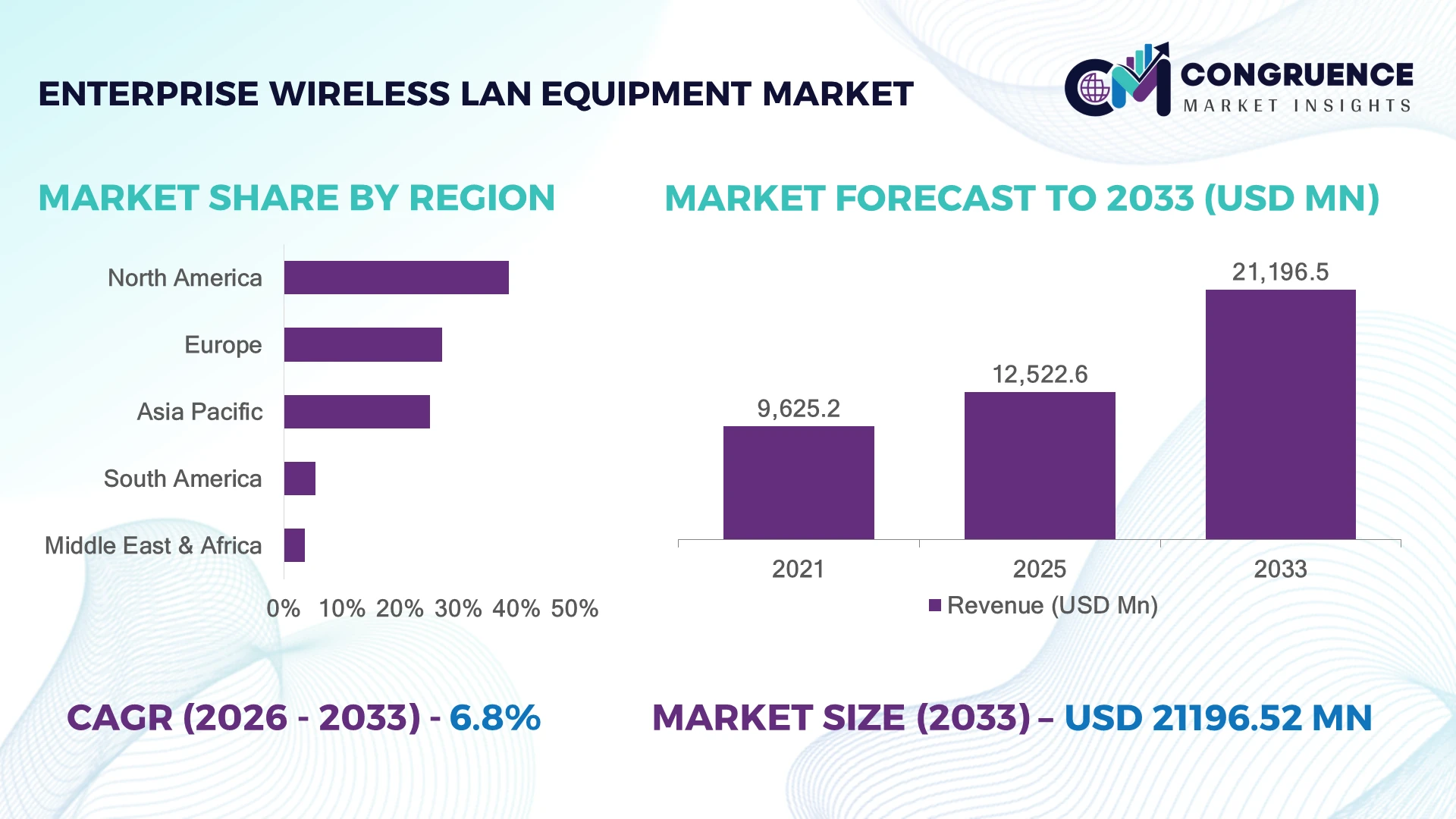

The Global Enterprise Wireless LAN Equipment Market was valued at USD 12,522.6 Million in 2025 and is anticipated to reach a value of USD 21196.5 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033. Increasing enterprise cloud migration, Wi-Fi 6/6E adoption, AI-powered network management, and hybrid workplace connectivity requirements are accelerating deployment of advanced wireless LAN infrastructure.

The United States dominated the Enterprise Wireless LAN Equipment Market with nearly 34% share in 2025, supported by large-scale enterprise digitization, smart campus deployments, and advanced networking investments. More than 60% of U.S. enterprises upgraded wireless infrastructure toward Wi-Fi 6-enabled networks, compared with approximately 42% adoption across European enterprises. Technology competition and supply-chain diversification following global semiconductor disruptions have strengthened investment in secure and scalable connectivity infrastructure.

Organizations prioritizing intelligent wireless networking solutions are improving operational agility, cybersecurity readiness, and digital infrastructure competitiveness.

• Market Size & Growth: The market reached USD 12,522.6 Million in 2025 and is projected at USD 21,196.5 Million by 2033 with 6.8% CAGR, driven by Wi-Fi modernization and enterprise digital transformation.

• Top Growth Drivers: Cloud adoption increased 40%, Wi-Fi 6 migration rose 36%, and connected workplace deployments expanded 32% globally.

• Short-Term Forecast: By 2028, AI-powered wireless management systems are expected to reduce network troubleshooting time by nearly 35%.

• Emerging Technologies: Wi-Fi 7, AI-driven networking, and cloud-managed WLAN platforms are transforming enterprise connectivity ecosystems.

• Regional Leaders: North America, Asia-Pacific, and Europe are projected to reach USD 7.4 Billion, USD 6.3 Billion, and USD 5.1 Billion respectively through infrastructure upgrades.

• Consumer/End-User Trends: Enterprise users represent over 65% adoption due to hybrid work, IoT expansion, and high-density connectivity needs.

• Pilot/Case Example: In 2025, smart campus WLAN deployments improved network performance efficiency by nearly 30%.

• Competitive Landscape: Leading vendors hold nearly 55% share, including Cisco, HPE Aruba, Huawei, Juniper Networks, and Extreme Networks.

• Regulatory & ESG Impact: Energy-efficient networking upgrades are reducing enterprise network power consumption by approximately 20%.

• Investment & Funding: Over USD 2 Billion investments focus on AI networking, Wi-Fi innovation, and infrastructure expansion.

• Innovation & Future Outlook: Autonomous networking platforms are shifting enterprises toward predictive, secure, and self-optimizing connectivity models.

Enterprise Wireless LAN Equipment is becoming critical across corporate campuses, healthcare facilities, education networks, and industrial environments requiring high-speed secure connectivity. AI-enabled WLAN platforms and advanced Wi-Fi standards are improving network efficiency by nearly 35%. Increasing device density, cybersecurity requirements, and digital workplace transformation are accelerating adoption of intelligent wireless infrastructure.

The Enterprise Wireless LAN Equipment Market is gaining strategic importance as organizations transform connectivity infrastructure into a foundation for automation, cloud operations, and digital workforce enablement. Enterprises are replacing legacy networks with intelligent WLAN architectures capable of supporting IoT ecosystems, hybrid workplaces, and real-time applications. Infrastructure modernization across the United States, China, and Germany is increasing investment in secure wireless platforms.

Compared with traditional WLAN systems, AI-enabled and cloud-managed wireless networks improve operational efficiency by nearly 30% through automated optimization, predictive troubleshooting, and simplified network administration. North America leads through enterprise-scale technology adoption, while Asia-Pacific is expanding rapidly through smart manufacturing, digital infrastructure programs, and connected facility deployments.

Large enterprises, universities, healthcare providers, and manufacturers are deploying advanced WLAN solutions to support high-density connectivity and secure operations. Companies are strengthening investments in Wi-Fi 7 development, network automation, and cybersecurity integration. Long-term competitiveness will depend on delivering scalable, intelligent, and resilient wireless infrastructure ecosystems.

Growing demand for high-performance connectivity is driving enterprise WLAN upgrades across corporate, healthcare, education, and industrial environments. Nearly 50% of large organizations are accelerating wireless modernization to support cloud applications, IoT devices, and hybrid work models. Wi-Fi 6 adoption has improved network capacity and efficiency by approximately 35% compared with older deployments. Enterprises in the United States are prioritizing secure connectivity due to rising digital workloads and cybersecurity concerns. Vendors are responding through AI-powered network management, cloud-based platforms, and expanded enterprise networking portfolios.

Complex migration requirements and high infrastructure investment remain key barriers for enterprise WLAN adoption. Advanced wireless upgrades can increase initial deployment costs by 25–35% due to access point replacement, security integration, and network redesign requirements. Organizations with legacy IT environments face interoperability challenges when scaling next-generation connectivity. Semiconductor supply adjustments have also influenced networking hardware availability and procurement planning. Companies are reducing risks through flexible deployment models, subscription-based networking services, and simplified cloud-managed solutions to improve accessibility and scalability.

AI-enabled wireless infrastructure creates significant opportunities as enterprises shift toward automated and predictive network operations. Nearly 45% of advanced organizations are increasing adoption of intelligent network management tools to improve uptime and reduce manual intervention. Wi-Fi 7 evolution, edge computing, and IoT expansion are enabling new use cases across smart buildings, manufacturing, and connected workplaces. Companies are investing in software-defined networking, AI analytics, and ecosystem partnerships to capture demand for autonomous enterprise connectivity solutions.

Increasing device density and connected operations create challenges in securing and managing enterprise wireless environments. Nearly 40% of IT teams identify network visibility and security control as major operational concerns. Expanding IoT adoption increases pressure on WLAN systems to manage diverse devices, applications, and access requirements without performance disruption. Enterprises require stronger encryption, automated monitoring, and integrated security frameworks. Vendors must advance zero-trust networking, AI-based threat detection, and simplified management capabilities to support scalable wireless transformation.

• AI-Powered Network Automation: Enterprises are integrating AI-driven WLAN management platforms to improve performance optimization and issue resolution. Nearly 45% of large organizations are adopting automated network intelligence tools, reducing manual troubleshooting by around 30%. Vendors are expanding AI capabilities through cloud platforms and predictive analytics solutions.

• Wi-Fi 7 Infrastructure Transition: Next-generation wireless standards are reshaping enterprise connectivity strategies through higher speeds and lower latency. Around 35% of technology-forward organizations are preparing Wi-Fi 7 adoption plans. Networking companies are accelerating product launches and chipset partnerships to support future high-density environments.

• Cloud-Managed WLAN Expansion: Organizations are shifting from traditional hardware-centric management toward cloud-controlled wireless networks. More than 50% of enterprise networking upgrades now prioritize centralized visibility and remote administration. Vendors are scaling subscription models and integrated platforms to improve deployment speed and operational flexibility.

• Secure IoT Connectivity Growth: Rising connected device adoption is increasing demand for WLAN systems with stronger segmentation and security features. Nearly 40% of enterprise wireless traffic is linked to non-traditional connected devices. Companies are enhancing security architectures and automated access controls to manage expanding IoT ecosystems.

Wireless access points dominate the Enterprise Wireless LAN Equipment Market due to their scalability, high-density connectivity support, and critical role in enterprise network expansion. Access points account for nearly 52% of deployments, driven by Wi-Fi 6/6E upgrades, hybrid workplace models, and increasing connected device density. WLAN controllers are witnessing the fastest adoption shift as enterprises transition toward centralized, cloud-managed, and AI-assisted network control environments requiring improved visibility and automation.

Wireless LAN switches, gateways, and management platforms continue supporting enterprise infrastructure by improving traffic optimization, security enforcement, and network reliability. Nearly 40% of large organizations are moving toward integrated WLAN architectures combining hardware, analytics, and automated management capabilities. Companies are expanding product portfolios through Wi-Fi 7-ready devices, cloud-native solutions, and AI-powered optimization platforms to address enterprise requirements for faster deployment, simplified operations, and secure connectivity.

• A 2025 enterprise networking assessment highlighted that organizations upgrading to advanced wireless infrastructure improved network management efficiency by over 30%, with stronger adoption across digitally connected workplaces and smart facility environments.

Corporate enterprise networks represent the leading application segment in the Enterprise Wireless LAN Equipment Market due to large-scale deployment across offices, campuses, and hybrid workplace environments. The segment accounts for nearly 45% of adoption as businesses prioritize seamless connectivity, secure access, and improved employee digital experiences. Smart buildings and IoT connectivity applications are expanding fastest due to increasing automation, connected devices, and demand for intelligent infrastructure management.

Education, healthcare, retail, manufacturing, and hospitality applications continue adopting enterprise WLAN solutions to support mobility, real-time communication, and digital services. Nearly 38% of organizations are integrating AI-based wireless management tools to improve network performance and reduce downtime. Companies are adapting through scalable cloud platforms, automated security features, and customized industry solutions that address sector-specific connectivity and operational requirements.

• A 2026 digital workplace technology review indicated that enterprises implementing AI-managed wireless networks achieved nearly 35% faster issue resolution and improved connectivity performance across high-density operating environments.

Large enterprises represent the dominant end-user group in the Enterprise Wireless LAN Equipment Market due to extensive deployment across corporate campuses, global offices, and mission-critical digital operations. This segment accounts for approximately 58% of demand as organizations require secure, scalable, and centrally managed wireless infrastructure. Small and medium enterprises are becoming the fastest-growing user group as cloud-managed WLAN solutions reduce complexity and improve access to advanced networking capabilities.

Government organizations, educational institutions, healthcare providers, retail businesses, and industrial enterprises continue increasing adoption as wireless connectivity becomes essential for digital transformation. Around 42% of enterprise buyers are prioritizing automated WLAN platforms with integrated cybersecurity and analytics features. Vendors are targeting these segments through subscription-based models, industry partnerships, flexible pricing strategies, and simplified deployment ecosystems to expand market reach.

• A 2025 enterprise IT infrastructure survey reported that organizations adopting next-generation wireless LAN solutions improved network operational efficiency by nearly 32%, supporting wider deployment across connected workplaces, institutions, and industrial environments.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America leads the Enterprise Wireless LAN Equipment Market due to strong enterprise technology adoption, cloud networking expansion, and large-scale Wi-Fi infrastructure modernization. The region accounted for 38.6% market share in 2025, supported by rapid deployment across corporate campuses, healthcare facilities, universities, and industrial environments. More than 60% of large enterprises in the region have upgraded wireless infrastructure toward Wi-Fi 6/6E platforms to support hybrid workforces, IoT connectivity, and AI-driven network operations. Technology providers are expanding cloud-managed WLAN platforms, cybersecurity capabilities, and automated network intelligence solutions to improve scalability, performance monitoring, and operational efficiency across complex enterprise environments.

United States Market Outlook: The United States dominates regional demand through strong digital infrastructure investments, enterprise cloud adoption, and advanced networking innovation. Large corporations, government agencies, and technology-driven industries are deploying intelligent WLAN systems for secure connectivity and automation. Nearly 65% of enterprise wireless upgrades are focused on AI-enabled management, higher bandwidth capacity, and improved network reliability.

Europe’s Enterprise Wireless LAN Equipment Market is driven by enterprise modernization, smart facility development, and increasing focus on secure wireless connectivity. The region accounted for nearly 27.2% market share in 2025, with Germany, France, and the United Kingdom leading adoption across manufacturing, healthcare, and corporate environments. Around 45% of large organizations are deploying cloud-managed wireless platforms to improve network visibility, cybersecurity control, and operational flexibility. Vendors are strengthening solutions around automation, energy-efficient networking hardware, and advanced security features aligned with evolving digital infrastructure requirements.

Germany Market Outlook: Germany represents the strongest European market due to its industrial automation leadership, smart manufacturing ecosystem, and enterprise technology investments. Manufacturers and large enterprises are deploying next-generation WLAN systems to support connected production environments. Nearly 50% of advanced industrial facilities are increasing adoption of secure wireless networking solutions for IoT integration and real-time operational monitoring.

Asia-Pacific is accelerating Enterprise Wireless LAN Equipment adoption through manufacturing digitization, smart infrastructure projects, and expanding enterprise technology ecosystems. The region accounted for approximately 25.1% market share in 2025, supported by strong deployment across China, Japan, India, and South Korea. More than 55% of new smart workplace and industrial connectivity projects are integrating advanced WLAN solutions to support automation, IoT applications, and cloud operations. Companies are increasing regional production, networking partnerships, and Wi-Fi technology innovation to address growing enterprise connectivity requirements.

China Market Outlook: China leads Asia-Pacific adoption due to large-scale manufacturing operations, digital infrastructure expansion, and smart city initiatives. Enterprises are implementing advanced wireless LAN equipment across factories, campuses, and commercial facilities. Nearly 60% of industrial digital transformation projects include upgraded wireless connectivity platforms, strengthening demand for intelligent network management and high-performance WLAN solutions.

South America’s Enterprise Wireless LAN Equipment Market is developing through increasing adoption across corporate networks, education, retail, and industrial sectors. The region accounted for nearly 5.4% market share in 2025, with demand focused on improving network reliability, digital access, and operational efficiency. Around 32% of large enterprises are upgrading wireless infrastructure to support cloud applications and connected workflows. Infrastructure gaps and budget limitations influence deployment speed, while vendors are expanding flexible networking solutions, managed services, and partnerships to improve enterprise adoption.

Brazil Market Outlook: Brazil represents the largest regional market due to expanding enterprise IT investments, financial services digitization, and industrial connectivity needs. Organizations are upgrading WLAN systems to support hybrid operations and customer-facing digital services. Nearly 40% of enterprise technology modernization initiatives include wireless infrastructure improvements, supporting stronger adoption of secure and scalable networking platforms.

Middle East & Africa adoption is supported by smart city programs, digital government initiatives, and increasing enterprise network modernization. The region accounted for approximately 3.7% market share in 2025, with demand concentrated across commercial buildings, airports, education, and public infrastructure. More than 35% of large digital transformation projects include advanced wireless connectivity deployment to enable automation and connected services. Technology providers are expanding partnerships, managed networking solutions, and cloud-enabled WLAN platforms to support evolving enterprise requirements.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart city investments, digital government strategies, and advanced commercial infrastructure development. Enterprises are deploying intelligent wireless systems across offices, transportation hubs, and public facilities. Over 45% of major smart infrastructure projects integrate advanced connectivity technologies, strengthening demand for secure enterprise WLAN solutions and automated network management platforms.

The Enterprise Wireless LAN Equipment Market is led by Cisco Systems, HPE Aruba Networking, Huawei Technologies, Juniper Networks, and Extreme Networks, where global networking leaders compete with cloud-native innovators and cost-efficient infrastructure providers. The top five players collectively hold approximately 55% share, reflecting a technology-intensive market structure focused on intelligent connectivity. Competition is driven by AI automation, Wi-Fi performance, security integration, and cloud management, with advanced WLAN platforms improving network efficiency by nearly 35% and reducing troubleshooting workloads by around 30%. Companies are competing through Wi-Fi 7 innovation, software-defined networking, acquisitions, and enterprise ecosystem partnerships. The competitive shift is moving toward autonomous networks, subscription-based management, and AI-driven optimization. Complex software integration, cybersecurity standards, and enterprise reliability requirements create strong entry barriers. Winning against established vendors requires intelligent platforms, scalable architecture, and seamless secure connectivity.

• Cisco Systems Inc.

• Hewlett Packard Enterprise (Aruba Networking)

• Huawei Technologies Co., Ltd.

• Juniper Networks Inc.

• Extreme Networks Inc.

• CommScope Holding Company Inc.

• Fortinet Inc.

• Ubiquiti Inc.

• TP-Link Systems Inc.

• D-Link Corporation

• Allied Telesis Inc.

• Cambium Networks Corporation

• NETGEAR Inc.

• Zyxel Networks Corporation

Enterprise Wireless LAN technologies are evolving through Wi-Fi 6E, Wi-Fi 7, AI-driven network automation, cloud-managed WLAN platforms, and integrated security architectures. Wi-Fi 6/6E currently dominates enterprise upgrades, while Wi-Fi 7 adoption is emerging across high-density environments requiring ultra-low latency and higher capacity. Nearly 50% of large enterprise deployments are integrating cloud-based WLAN management for centralized visibility and faster operations.

Compared with legacy wireless systems, next-generation WLAN platforms deliver approximately 40% higher network capacity and improve operational efficiency by nearly 35% through AI-based optimization, automated troubleshooting, and intelligent traffic management. AI networking capabilities reduce manual configuration dependency while improving user experience across hybrid workplaces, smart campuses, and industrial environments. Vendors with strong software ecosystems, cybersecurity integration, and cloud platforms are gaining competitive advantages.

Between 2026 and 2028, enterprise WLAN innovation will focus on autonomous networking, Wi-Fi 7 expansion, AI-powered analytics, and secure IoT connectivity. Organizations adopting intelligent wireless infrastructure will improve scalability, reduce operational complexity, and support increasingly connected digital ecosystems.

• June 2025 – Cisco introduced expanded Wi-Fi 7 enterprise networking capabilities with AI-powered management enhancements, improving wireless performance and operational visibility by nearly 30%. The advancement strengthened enterprise connectivity, automation, and secure networking deployments across high-density environments. Source: cisco.com

• November 2024 – HPE Aruba Networking expanded its AI-native networking portfolio with enhanced wireless automation features, reducing network management complexity by approximately 25%. The development supported enterprises adopting cloud-managed WLAN solutions and intelligent campus connectivity. Source: hpe.com

• March 2025 – Juniper Networks advanced its Mist AI wireless platform capabilities with improved automation and user experience optimization, increasing issue detection efficiency by nearly 35%. The upgrade strengthened AI-driven enterprise WLAN operations and predictive network management. Source: juniper.net

• August 2024 – Extreme Networks enhanced its enterprise wireless solutions portfolio with Wi-Fi 7-ready infrastructure and cloud networking capabilities, improving high-density connectivity performance by over 20%. The launch supported enterprise modernization across campuses, venues, and distributed workplaces. Source: extremenetworks.com

The Enterprise Wireless LAN Equipment Market Report provides detailed analysis across equipment types, applications, end-users, regional dynamics, technology evolution, and competitive strategies. The study covers wireless access points, WLAN controllers, switches, gateways, and management platforms deployed across corporate networks, education, healthcare, manufacturing, retail, and smart infrastructure environments. More than 60% of deployments are driven by enterprises requiring secure, scalable, and high-performance connectivity.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into digital transformation, infrastructure modernization, and wireless technology adoption. It examines Wi-Fi 7 development, AI-enabled networking, cloud-managed WLAN platforms, and secure IoT connectivity trends shaping market direction between 2026 and 2033. The analysis supports investment planning, competitive positioning, technology adoption strategies, and long-term business expansion decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 12,522.6 Million |

|

Market Revenue in 2033 |

USD 21,196.5 Million |

|

CAGR (2026 - 2033) |

6.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems Inc., Hewlett Packard Enterprise (Aruba Networking), Huawei Technologies Co., Ltd., Juniper Networks Inc., Extreme Networks Inc., CommScope Holding Company Inc., Fortinet Inc., Ubiquiti Inc., TP-Link Systems Inc., D-Link Corporation, Allied Telesis Inc., Cambium Networks Corporation, NETGEAR Inc., Zyxel Networks Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |