Reports

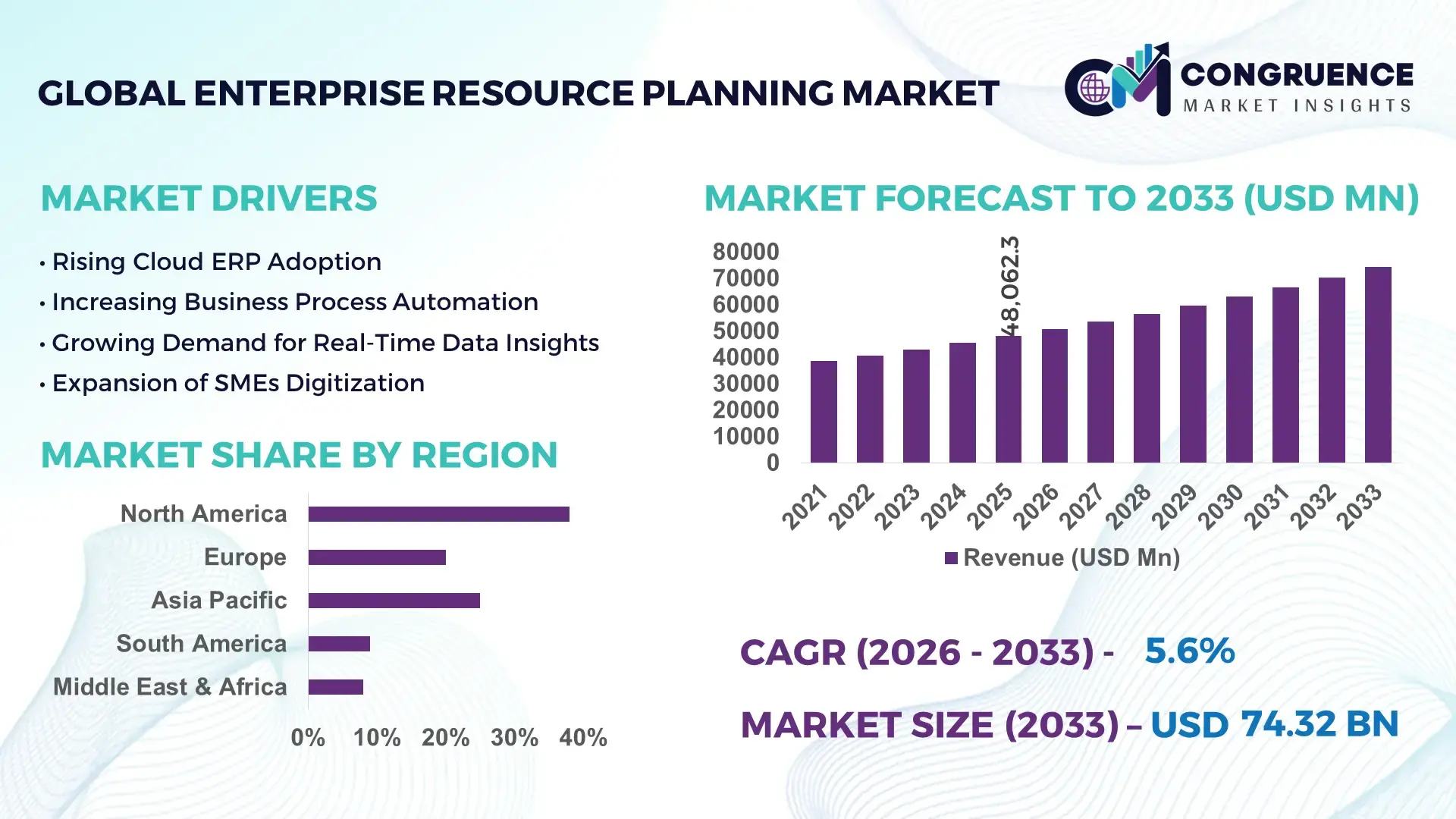

The Global Enterprise Resource Planning Market was valued at USD 48062.3 Million in 2025 and is anticipated to reach a value of USD 74321.83 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. This growth is driven by increasing enterprise demand for integrated business management solutions and real-time data analytics.

The United States continues to demonstrate strong operational scale in the enterprise resource planning ecosystem, supported by robust cloud infrastructure and enterprise IT spending exceeding USD 1.5 trillion annually. Over 72% of large enterprises in the country have already implemented advanced ERP platforms, with manufacturing, healthcare, and retail sectors accounting for more than 65% of deployments. Additionally, nearly 58% of mid-sized firms are transitioning toward cloud-based ERP environments to enhance operational agility. Investment in AI-driven ERP solutions has increased by over 40% since 2022, enabling predictive analytics and automation capabilities. The country’s ERP landscape is further strengthened by continuous R&D expenditure exceeding USD 300 billion annually in enterprise technologies, accelerating innovation in intelligent workflow management and system integration.

Market Size & Growth: Valued at USD 48062.3 Million in 2025, projected to reach USD 74321.83 Million by 2033 at a CAGR of 5.6%, driven by enterprise digital transformation initiatives.

Top Growth Drivers: Cloud ERP adoption (68%), automation efficiency gains (45%), data-driven decision-making demand (52%).

Short-Term Forecast: By 2028, ERP implementation is expected to reduce operational costs by up to 30% and improve workflow efficiency by 25%.

Emerging Technologies: AI-enabled ERP systems, machine learning analytics, and IoT-integrated enterprise platforms.

Regional Leaders: North America (USD 28 Billion by 2033, high cloud adoption), Europe (USD 19 Billion by 2033, compliance-driven ERP usage), Asia-Pacific (USD 21 Billion by 2033, SME digitization surge).

Consumer/End-User Trends: Manufacturing and BFSI sectors contribute over 50% of ERP adoption, with SMEs increasing adoption by 35% annually.

Pilot or Case Example: In 2024, a global logistics firm improved operational efficiency by 27% through AI-integrated ERP deployment.

Competitive Landscape: Market leader holds approximately 22% share, followed by major players such as Oracle, SAP, Microsoft, Infor, and Epicor.

Regulatory & ESG Impact: Increasing compliance mandates and ESG reporting requirements are driving ERP adoption for transparency and traceability.

Investment & Funding Patterns: Over USD 15 Billion invested in ERP innovation and cloud migration projects globally since 2023.

Innovation & Future Outlook: Integration of predictive analytics, blockchain for supply chain transparency, and low-code ERP customization tools.

The enterprise resource planning market is witnessing strong demand across manufacturing, retail, healthcare, and financial services, collectively contributing over 70% of total ERP deployments. Cloud-based ERP solutions now account for nearly 60% of new installations, reflecting a shift toward scalable and cost-efficient platforms. Regulatory compliance requirements, particularly in Europe and North America, are pushing organizations to adopt ERP systems with integrated audit and reporting capabilities. Additionally, sustainability initiatives are encouraging the use of ERP platforms to monitor carbon emissions and resource utilization. Emerging trends such as industry-specific ERP customization and AI-powered automation are expected to redefine enterprise workflows, enhancing productivity and strategic decision-making capabilities.

The enterprise resource planning market holds significant strategic relevance as organizations increasingly prioritize integrated digital ecosystems to streamline operations and improve decision-making accuracy. Advanced AI-driven ERP platforms deliver up to 35% improvement in process efficiency compared to traditional on-premise ERP systems, enabling enterprises to manage complex workflows with greater precision. North America dominates in volume due to high enterprise IT spending, while Asia-Pacific leads in adoption growth with over 62% of SMEs transitioning to cloud-based ERP solutions.

By 2028, AI-powered automation within ERP systems is expected to reduce manual data processing efforts by nearly 40%, significantly enhancing productivity across industries. Companies are also aligning ERP implementations with ESG goals, committing to measurable improvements such as 25% reduction in energy consumption through optimized resource planning by 2030. These sustainability-driven ERP solutions are becoming critical in sectors like manufacturing and logistics, where environmental compliance is increasingly stringent.

In 2024, a leading European manufacturing firm achieved a 28% reduction in operational downtime through the implementation of predictive maintenance modules within its ERP system. Such micro-level transformations highlight the growing importance of intelligent ERP frameworks in improving operational resilience. Additionally, the integration of blockchain technology for supply chain transparency and low-code development tools for ERP customization is opening new avenues for innovation. As enterprises continue to embrace digital transformation, the enterprise resource planning market is positioned as a foundational pillar supporting resilience, regulatory compliance, and sustainable business growth in an increasingly complex global economy.

The rapid adoption of cloud-based enterprise resource planning systems is a primary driver of market expansion, with over 65% of new ERP deployments now cloud-enabled. Cloud ERP platforms reduce infrastructure costs by up to 40% while offering scalability and flexibility, making them particularly attractive to SMEs. Enterprises leveraging cloud ERP report a 20–30% improvement in operational efficiency due to real-time data accessibility and seamless integration across departments. Additionally, cloud-based solutions enable remote workforce management, which has become essential in hybrid work environments. The ability to deploy updates and security patches automatically further enhances system reliability, contributing to increased adoption across industries such as retail, manufacturing, and logistics.

Despite strong growth prospects, high implementation and customization costs remain a significant barrier to ERP adoption, particularly for small and mid-sized enterprises. Initial deployment expenses, including licensing, integration, and employee training, can exceed USD 500,000 for large-scale systems. Furthermore, customization requirements to align ERP platforms with specific business processes often lead to extended deployment timelines and increased costs. Approximately 45% of ERP projects experience budget overruns due to unforeseen integration complexities. Additionally, legacy system migration poses technical challenges, resulting in operational disruptions and data inconsistencies. These financial and technical constraints limit adoption rates in cost-sensitive markets, particularly in developing economies.

The ongoing wave of digital transformation presents substantial opportunities for the enterprise resource planning market, particularly in emerging economies where ERP adoption remains underpenetrated. Over 70% of organizations globally have initiated digital transformation strategies, creating strong demand for integrated ERP solutions. The rise of industry-specific ERP platforms tailored for sectors such as healthcare, retail, and manufacturing is opening new revenue streams. Additionally, the integration of AI and machine learning enables predictive analytics, improving demand forecasting accuracy by up to 35%. The growing adoption of mobile ERP applications is further expanding market reach, allowing real-time access to business data. Government initiatives promoting digital infrastructure development are also supporting ERP adoption among SMEs.

Data security concerns and integration complexities continue to challenge the enterprise resource planning market, particularly as organizations handle increasing volumes of sensitive business data. Cybersecurity threats targeting ERP systems have risen by over 30% in recent years, necessitating robust security frameworks and compliance measures. Additionally, integrating ERP platforms with existing legacy systems and third-party applications can be highly complex, often requiring specialized expertise and extended implementation timelines. Approximately 50% of enterprises report difficulties in achieving seamless system interoperability, leading to inefficiencies and data silos. Regulatory requirements related to data protection and privacy further complicate ERP deployments, particularly in regions with stringent compliance standards.

• Accelerated Cloud ERP Adoption Across Enterprises (65% Deployment Growth):

Cloud-based enterprise resource planning systems are witnessing accelerated adoption, with over 65% of new ERP deployments now cloud-native. Approximately 72% of organizations report improved operational visibility after migrating to cloud ERP platforms, while infrastructure costs are reduced by nearly 35%. Large enterprises are increasingly shifting mission-critical workloads to hybrid cloud ERP models, with adoption rising by 48% since 2022. Additionally, over 60% of SMEs prefer subscription-based ERP models due to lower upfront costs and faster implementation cycles, enabling deployment timelines to shrink by up to 30%. This shift is significantly transforming enterprise IT strategies globally.

• Integration of Artificial Intelligence and Predictive Analytics (40% Efficiency Gains):

The integration of artificial intelligence and machine learning into ERP platforms is enhancing decision-making capabilities, with enterprises reporting up to 40% improvement in process efficiency. Around 58% of ERP users now utilize AI-driven analytics for demand forecasting, reducing forecasting errors by nearly 25%. Predictive maintenance modules embedded within ERP systems have decreased equipment downtime by 30% in manufacturing sectors. Furthermore, nearly 50% of enterprises are investing in AI-enabled automation features, allowing real-time data insights and proactive risk management, thereby strengthening operational resilience across industries.

• Rise of Industry-Specific ERP Solutions (52% Adoption in Key Sectors):

Industry-specific ERP solutions are gaining traction, with approximately 52% of enterprises opting for customized platforms tailored to sector-specific requirements. Manufacturing and healthcare sectors collectively account for over 45% of these specialized deployments, driven by compliance and operational complexity. Retail ERP systems have improved inventory accuracy by 28%, while healthcare ERP solutions have enhanced patient data management efficiency by 33%. Additionally, sector-focused ERP implementations reduce customization costs by nearly 20% compared to generic ERP systems, making them increasingly attractive for enterprises seeking optimized workflows.

• Expansion of Mobile and Remote ERP Accessibility (70% Workforce Utilization):

Mobile-enabled ERP solutions are rapidly expanding, with nearly 70% of enterprise users accessing ERP systems through mobile devices for real-time decision-making. Remote ERP accessibility has increased workforce productivity by 25%, particularly in logistics and field service industries. Approximately 55% of organizations have deployed mobile ERP applications to support hybrid work environments, ensuring seamless access to enterprise data. Moreover, mobile ERP usage has improved response times by 30% in supply chain operations, enabling faster coordination and improved service delivery across geographically distributed teams.

The enterprise resource planning market segmentation is structured across types, applications, and end-user industries, reflecting diverse enterprise requirements and digital maturity levels. By type, cloud-based ERP solutions dominate due to scalability and lower infrastructure costs, while on-premise systems maintain relevance in highly regulated sectors requiring strict data control. By application, finance and accounting functions lead ERP utilization, accounting for over 30% of deployments, followed by supply chain management and human resource management. From an end-user perspective, manufacturing remains the largest adopter, contributing approximately 35% of total ERP usage, driven by demand for production planning and inventory optimization. Additionally, small and medium enterprises are emerging as a key growth segment, with adoption rates increasing by over 25% annually due to affordable cloud ERP offerings and government-backed digitalization initiatives.

The enterprise resource planning market by type is primarily segmented into cloud-based ERP, on-premise ERP, and hybrid ERP systems. Cloud-based ERP currently leads the segment, accounting for approximately 62% of total adoption due to its scalability, cost efficiency, and rapid deployment capabilities. Organizations adopting cloud ERP report up to 35% reduction in IT infrastructure costs and a 30% improvement in system accessibility across departments. In comparison, on-premise ERP systems hold around 28% of the market, primarily used by large enterprises in regulated industries such as banking and healthcare, where data security and compliance are critical. Hybrid ERP solutions, combining cloud and on-premise features, represent the remaining 10% and are gaining traction among enterprises transitioning from legacy systems. Cloud ERP is also the fastest-growing segment, expanding at an estimated rate exceeding 12% annually, driven by increased adoption among SMEs and the need for remote accessibility. Meanwhile, hybrid ERP adoption is accelerating due to its flexibility in integrating legacy systems with modern cloud functionalities.

In terms of application, the enterprise resource planning market is segmented into finance and accounting, supply chain management, human resource management, customer relationship management, and others. Finance and accounting applications dominate the segment, contributing approximately 32% of ERP usage due to the need for real-time financial reporting, compliance management, and audit readiness. Supply chain management follows with around 25% adoption, driven by increasing demand for inventory optimization and logistics efficiency. Human resource management accounts for nearly 18%, supporting workforce planning and payroll automation. Supply chain management applications are the fastest-growing segment, with an estimated growth rate of over 11% annually, fueled by global supply chain disruptions and the need for real-time tracking and predictive analytics. Customer relationship management and other applications collectively contribute approximately 25% of the market, focusing on enhancing customer engagement and operational integration.

The enterprise resource planning market by end-user is categorized into manufacturing, retail, healthcare, BFSI, IT and telecom, and others. Manufacturing remains the leading end-user segment, accounting for approximately 35% of total ERP adoption, driven by the need for production planning, inventory control, and quality management. Retail and BFSI sectors follow, contributing around 20% and 15% respectively, leveraging ERP systems for customer analytics, financial management, and compliance tracking. The fastest-growing end-user segment is healthcare, with an estimated growth rate exceeding 13% annually, supported by increasing digitalization of patient records and regulatory compliance requirements. IT and telecom sectors, along with other industries, collectively account for nearly 30% of ERP usage, utilizing ERP platforms for resource allocation and project management. Adoption among SMEs across various industries has increased by over 28%, reflecting a broader shift toward digital enterprise solutions.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America’s dominance is supported by over 72% enterprise-level ERP adoption across large organizations and more than 60% cloud ERP penetration among SMEs. Europe follows with approximately 27% share, driven by strict regulatory compliance requirements and digital transformation initiatives across industries. Asia-Pacific holds nearly 25% of the market, with over 65% of enterprises in countries like China and India investing in ERP modernization projects. South America and the Middle East & Africa collectively contribute around 10%, with ERP adoption increasing by over 30% in mid-sized enterprises. Regional demand is also influenced by sector-specific growth, where manufacturing contributes over 35% of ERP usage globally, while BFSI and retail sectors together account for nearly 40% of deployments.

How are advanced enterprise digitization strategies shaping ERP adoption patterns?

North America holds approximately 38% of the global enterprise resource planning market share, driven by strong adoption across industries such as healthcare, BFSI, and manufacturing, which together account for over 65% of ERP deployments. The region benefits from advanced IT infrastructure, with over 70% of enterprises using cloud-based ERP solutions. Regulatory frameworks such as data protection mandates and financial reporting standards are pushing companies to adopt integrated ERP systems for compliance and transparency. Technological advancements including AI-enabled analytics and automation tools have improved operational efficiency by up to 30% across enterprises. A key player in the region has expanded its cloud ERP offerings, enabling over 15,000 enterprises to transition from legacy systems. Consumer behavior reflects high demand for real-time data access, with nearly 68% of enterprises prioritizing ERP systems for predictive analytics and strategic decision-making.

What factors are accelerating adoption of compliant and sustainable ERP systems?

Europe accounts for nearly 27% of the enterprise resource planning market, with leading countries such as Germany, the United Kingdom, and France contributing over 60% of regional demand. Regulatory bodies enforcing strict data privacy and sustainability standards have led to a 45% increase in ERP adoption for compliance management. Over 58% of enterprises in Europe utilize ERP systems to meet environmental reporting requirements and ESG targets. Emerging technologies such as AI-driven analytics and blockchain integration are being adopted by more than 40% of large organizations. A prominent regional ERP vendor has introduced industry-specific platforms that improved operational efficiency by 25% for manufacturing firms. Consumer behavior in this region emphasizes transparency and compliance, with over 62% of enterprises prioritizing ERP solutions that support audit trails and regulatory reporting.

How is rapid industrial expansion influencing ERP deployment strategies?

Asia-Pacific ranks as the fastest-growing region in the enterprise resource planning market, contributing approximately 25% of global demand. Key countries such as China, India, and Japan collectively account for over 70% of regional ERP consumption. Rapid industrialization and infrastructure development have led to a 55% increase in ERP adoption among manufacturing enterprises. Additionally, more than 65% of SMEs in the region are adopting cloud-based ERP systems to enhance scalability and reduce costs. Innovation hubs in countries like India and China are driving ERP advancements, with AI and IoT integration improving operational efficiency by up to 35%. A regional technology provider recently enabled over 10,000 SMEs to adopt mobile ERP platforms, significantly improving workflow automation. Consumer behavior is influenced by the growth of e-commerce, with over 60% of businesses requiring ERP solutions for supply chain optimization and real-time analytics.

What role do localization and digital policies play in ERP adoption growth?

South America represents approximately 6% of the global enterprise resource planning market, with Brazil and Argentina accounting for over 70% of regional demand. Infrastructure development and growth in the energy and manufacturing sectors have increased ERP adoption by nearly 28% among enterprises. Government initiatives promoting digital transformation and favorable trade policies have supported ERP deployment across SMEs, with adoption rates rising by 32% in recent years. Localization requirements, including language and regulatory compliance, are influencing ERP customization strategies. A regional ERP vendor has developed localized solutions that improved operational efficiency by 20% for mid-sized enterprises. Consumer behavior in this region reflects a strong preference for cost-effective and adaptable ERP platforms, particularly among SMEs seeking to streamline operations.

How are infrastructure investments and digital modernization shaping ERP demand?

The Middle East & Africa region contributes approximately 4% of the enterprise resource planning market, with key growth observed in countries such as the UAE and South Africa. Demand is primarily driven by sectors such as oil & gas, construction, and logistics, which collectively account for over 50% of ERP deployments. Technological modernization initiatives have led to a 35% increase in ERP adoption, particularly in cloud-based solutions. Government-backed digital transformation programs and trade partnerships are further accelerating market growth. A regional technology firm has implemented ERP systems across large-scale infrastructure projects, improving project efficiency by 22%. Consumer behavior in this region emphasizes scalability and integration, with over 55% of enterprises prioritizing ERP platforms that support multi-site operations and real-time data management.

United States – 34% market share in the Enterprise Resource Planning market, driven by high enterprise IT spending and widespread cloud ERP adoption.

China – 18% market share in the Enterprise Resource Planning market, supported by rapid industrialization and increasing SME digital transformation initiatives.

The enterprise resource planning market is moderately consolidated, with the top five companies collectively accounting for approximately 55% of the global market share. The competitive landscape includes over 150 active vendors ranging from global technology leaders to specialized regional providers. Market leaders are focusing on strategic initiatives such as cloud migration, AI integration, and industry-specific ERP solutions to strengthen their positions. Over 60% of leading vendors have launched AI-enabled ERP platforms to enhance predictive analytics and automation capabilities.

Partnerships and acquisitions remain a key strategy, with more than 40 major mergers and collaborations recorded since 2022 to expand product portfolios and geographic reach. Product innovation is also accelerating, with nearly 50% of vendors investing in low-code and no-code ERP customization tools to meet evolving enterprise demands. Additionally, cloud ERP solutions account for over 65% of new product launches, reflecting the shift toward scalable and flexible deployment models.

Competitive differentiation is increasingly driven by technological capabilities, with companies focusing on integrating blockchain, IoT, and advanced analytics into ERP systems. Regional players are also gaining traction by offering cost-effective and localized solutions, particularly in emerging markets. The market continues to evolve as vendors compete on innovation, pricing strategies, and customer-centric solutions to capture a larger share of enterprise digital transformation investments.

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

Epicor Software Corporation

Sage Group plc

Workday Inc.

IFS AB

Unit4

Acumatica Inc.

The enterprise resource planning market is undergoing rapid transformation driven by advanced digital technologies that enhance operational efficiency, data integration, and decision-making accuracy. Artificial intelligence and machine learning are now embedded in over 55% of modern ERP platforms, enabling predictive analytics, automated workflows, and intelligent forecasting. These technologies have reduced manual processing efforts by up to 40% and improved demand forecasting accuracy by nearly 30%, particularly in manufacturing and retail sectors. Additionally, natural language processing capabilities are being integrated into ERP systems, allowing users to interact with enterprise data through conversational interfaces, improving accessibility and user experience.

Cloud computing remains a cornerstone technology, with more than 65% of ERP deployments now cloud-based. Hybrid cloud architectures are gaining traction, adopted by approximately 35% of large enterprises to balance flexibility with data control. These cloud-based ERP systems offer scalability, real-time updates, and seamless integration with third-party applications, reducing IT maintenance costs by up to 30%. Furthermore, edge computing is emerging as a complementary technology, particularly in industrial applications, where real-time data processing reduces latency by over 20% in production environments.

The integration of Internet of Things (IoT) technology into ERP platforms is also expanding, with nearly 50% of manufacturing firms leveraging IoT-enabled ERP systems for real-time equipment monitoring and predictive maintenance. This integration has resulted in a 25% reduction in equipment downtime and improved asset utilization rates. Blockchain technology is being increasingly explored for supply chain transparency, with pilot implementations showing up to 35% improvement in traceability and data integrity across multi-tier supply networks.

Low-code and no-code development platforms are further revolutionizing ERP customization, with over 45% of organizations adopting these tools to reduce development time by nearly 60%. This enables faster deployment of tailored ERP solutions aligned with specific business processes. Additionally, cybersecurity technologies are becoming integral, as ERP systems handle sensitive enterprise data. Advanced encryption and multi-factor authentication protocols are now implemented in over 70% of ERP solutions, addressing rising cybersecurity threats. These technological advancements collectively position ERP systems as intelligent, scalable, and secure platforms supporting enterprise digital transformation.

• In March 2025, SAP SE expanded its cloud ERP portfolio by enhancing SAP S/4HANA Cloud with advanced AI-driven automation features, enabling enterprises to improve financial close processes by up to 30% and streamline supply chain planning through real-time analytics. Source: www.sap.com

• In October 2024, Oracle Corporation announced new generative AI capabilities within Oracle Fusion Cloud ERP, integrating over 50 AI use cases across finance, procurement, and HR functions, significantly improving operational productivity and reducing manual intervention across enterprise workflows. Source: www.oracle.com

• In April 2025, Microsoft Corporation strengthened its Dynamics 365 ERP suite by introducing Copilot-powered AI assistants, enabling automated reporting and data insights, with early enterprise deployments reporting productivity improvements of up to 25% in finance and operations teams. Source: www.microsoft.com

• In November 2024, Workday Inc. launched AI-powered financial management enhancements within its ERP platform, enabling predictive planning and anomaly detection, which improved forecasting accuracy by nearly 28% for enterprise users across global operations. Source: www.workday.com

The scope of the enterprise resource planning market report encompasses a comprehensive evaluation of key segments, technologies, applications, and regional dynamics shaping the industry. The report analyzes multiple ERP deployment types, including cloud-based, on-premise, and hybrid systems, with cloud ERP accounting for over 60% of new implementations due to its scalability and cost-efficiency. It further examines application areas such as finance and accounting, supply chain management, human resource management, and customer relationship management, which collectively represent more than 80% of ERP usage across industries.

From an industry perspective, the report covers major end-user sectors including manufacturing, retail, healthcare, BFSI, and IT & telecom, with manufacturing alone contributing approximately 35% of ERP adoption due to its complex operational requirements. The report also evaluates SME adoption trends, highlighting that over 65% of small and mid-sized enterprises are transitioning toward digital ERP platforms to improve operational efficiency and data-driven decision-making.

Geographically, the report provides in-depth insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in adoption rates, regulatory environments, and technological maturity. It includes analysis of over 25 key countries, representing more than 85% of global ERP demand. The scope further extends to emerging technologies such as artificial intelligence, IoT, blockchain, and low-code platforms, which are being adopted by over 50% of enterprises to enhance system capabilities.

Additionally, the report examines competitive dynamics, covering more than 150 active ERP vendors and analyzing innovation trends, strategic partnerships, and product developments. It also highlights niche segments such as mobile ERP and industry-specific solutions, which are gaining traction with adoption rates exceeding 40% in targeted sectors. This broad and structured scope ensures a detailed understanding of the enterprise resource planning market landscape for informed business decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SAP SE, Oracle Corporation, Microsoft Corporation, Infor Inc., Epicor Software Corporation, Sage Group plc, Workday Inc., IFS AB, Unit4, Acumatica Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |