Reports

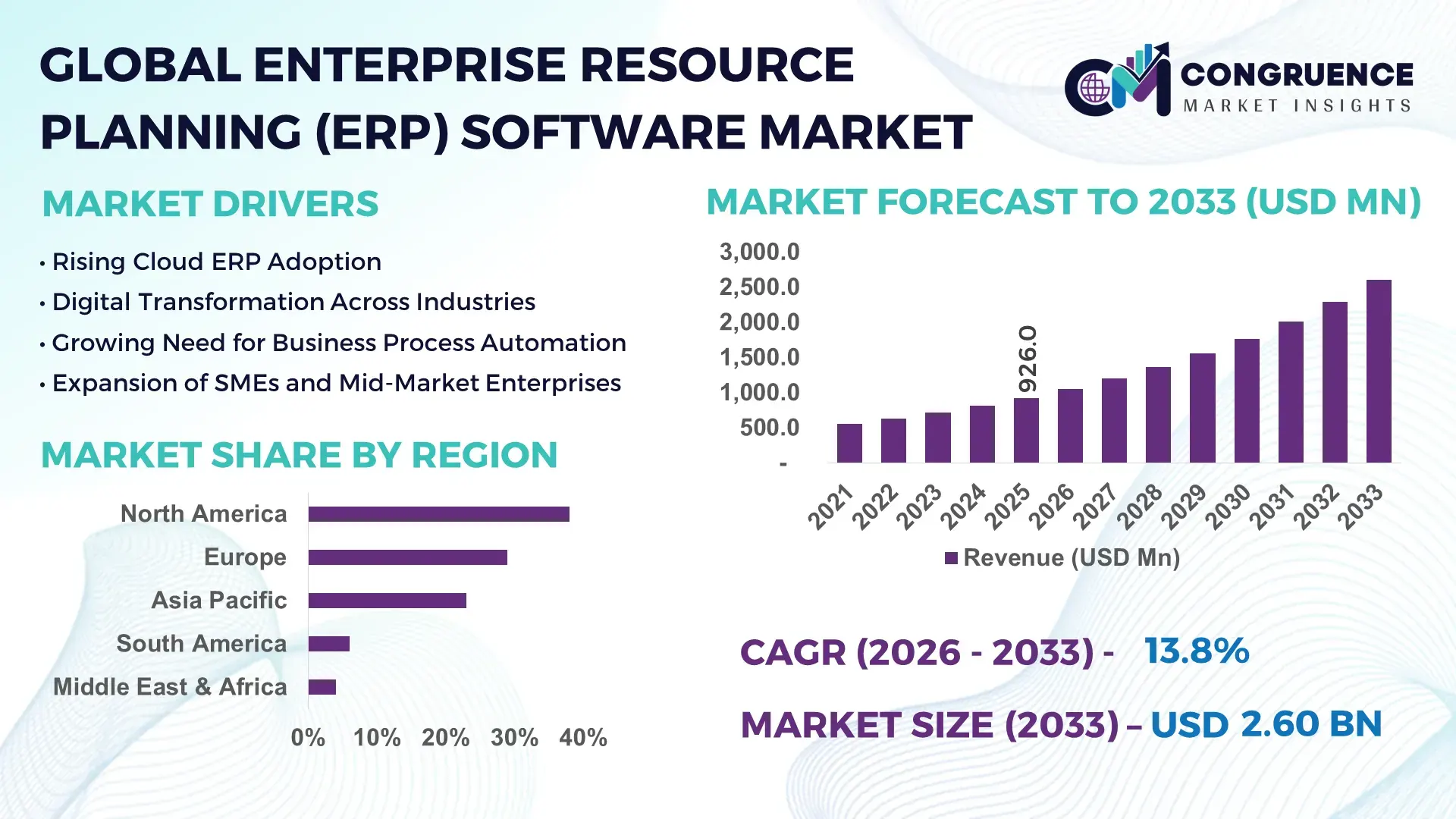

The Global Enterprise Resource Planning (ERP) Software Market was valued at USD 926.0 Million in 2025 and is anticipated to reach a value of USD 2,604.6 Million by 2033 expanding at a CAGR of 13.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by accelerated digital transformation initiatives and the rising need for integrated, real-time enterprise data management across industries.

The United States represents the dominant country in the Enterprise Resource Planning (ERP) Software Market, supported by strong enterprise digital infrastructure and sustained technology investment. In 2025, over 68% of large U.S.-based enterprises actively deployed multi-module ERP platforms across finance, supply chain, and human resources. Annual enterprise software investment exceeded USD 120 billion, with ERP accounting for a significant portion of cloud migration budgets. Manufacturing, healthcare, and retail collectively represented more than 55% of ERP application deployments. The U.S. also leads in advanced ERP capabilities, with over 60% of deployments integrating AI-driven analytics, automation, and predictive planning tools, alongside widespread adoption of SaaS-based ERP architectures.

Market Size & Growth: Valued at USD 926.0 Million in 2025, projected to reach USD 2,604.6 Million by 2033, expanding at a CAGR of 13.8%, driven by cloud-first enterprise transformation.

Top Growth Drivers: Cloud ERP adoption at 72%, process automation efficiency gains of 35%, real-time analytics utilization rising by 48%.

Short-Term Forecast: By 2028, ERP-enabled process optimization is expected to reduce enterprise operational costs by 22%.

Emerging Technologies: AI-powered ERP analytics, low-code customization platforms, embedded machine learning forecasting.

Regional Leaders: North America projected at USD 980.0 Million by 2033 with AI integration focus; Europe at USD 720.0 Million emphasizing compliance-driven ERP; Asia Pacific at USD 650.0 Million driven by SME cloud adoption.

Consumer/End-User Trends: Manufacturing and retail enterprises account for over 45% of active ERP deployments with rising SME usage.

Pilot or Case Example: In 2024, a U.S.-based manufacturer reduced supply chain downtime by 31% through AI-enabled ERP deployment.

Competitive Landscape: SAP leads with ~23% share, followed by Oracle, Microsoft, Infor, and Workday.

Regulatory & ESG Impact: Data localization and ESG reporting mandates increased ERP compliance module adoption by 28%.

Investment & Funding Patterns: Over USD 18 billion invested globally in ERP innovation and cloud migration initiatives.

Innovation & Future Outlook: Deep ERP integration with AI, IoT, and digital twins is reshaping enterprise decision-making.

Enterprise Resource Planning (ERP) Software Market solutions support manufacturing (32%), retail (21%), healthcare (14%), and BFSI (13%) sectors. Recent innovations include AI-driven demand forecasting, industry-specific ERP modules, and embedded ESG reporting tools. Regulatory digitization mandates, regional cloud adoption, and automation-driven productivity gains continue to shape usage patterns, while future growth is driven by intelligent, modular, and scalable ERP architectures.

The Enterprise Resource Planning (ERP) Software Market plays a critical strategic role in enabling enterprises to achieve operational resilience, regulatory compliance, and scalable growth. Modern cloud-based ERP platforms deliver up to 40% faster deployment compared to traditional on-premise systems, while AI-enabled ERP analytics delivers 28% improvement in forecasting accuracy compared to rule-based legacy systems. North America dominates in deployment volume, while Europe leads in compliance-driven adoption with over 62% of enterprises using ERP for regulatory reporting. By 2028, embedded AI and automation in ERP platforms are expected to improve supply chain responsiveness by 30% and reduce manual processing errors by 35%. ESG compliance is increasingly integrated, with enterprises committing to 25% reductions in reporting time and 20% improvements in sustainability data accuracy by 2030. In 2024, a German manufacturing firm achieved a 27% inventory optimization improvement through predictive ERP analytics. Looking ahead, the Enterprise Resource Planning (ERP) Software Market will remain a foundational pillar supporting enterprise agility, digital compliance, and sustainable long-term growth across global industries.

The Enterprise Resource Planning (ERP) Software Market is shaped by enterprise-wide digitalization, increasing system interoperability requirements, and rising data-driven decision-making needs. Organizations are consolidating fragmented IT systems into unified ERP platforms to enhance visibility, governance, and efficiency. Cloud deployment, subscription-based pricing, and modular functionality are redefining procurement strategies, particularly among SMEs. Integration with AI, IoT, and advanced analytics continues to elevate ERP from transactional systems to strategic intelligence platforms. Meanwhile, regulatory compliance requirements and cybersecurity priorities influence ERP architecture design and deployment models across regions.

Enterprises increasingly rely on ERP platforms to unify finance, operations, and supply chain data across geographies. Over 70% of organizations report improved cross-functional coordination after ERP implementation. Automation of procurement, inventory, and financial workflows has reduced manual effort by up to 40%, improving productivity and accuracy. Digital-first strategies across manufacturing, retail, and healthcare continue to accelerate ERP adoption, particularly cloud-based solutions that support scalability and remote operations.

ERP deployment often involves complex system integration, data migration, and change management. Nearly 38% of enterprises report project delays due to legacy system incompatibility. Customization and training requirements increase implementation timelines, while cybersecurity concerns elevate compliance costs. These challenges particularly impact small and mid-sized enterprises with limited IT resources.

AI-enabled ERP systems unlock predictive insights across demand planning, financial forecasting, and asset management. Enterprises using AI-integrated ERP report 25% improvement in planning accuracy and 30% faster decision cycles. Growing adoption of low-code platforms further enables customization without extensive development costs, expanding ERP accessibility across industries.

ERP systems centralize sensitive enterprise data, increasing exposure to cybersecurity risks. Over 45% of organizations cite data protection compliance as a critical ERP challenge. Regional data sovereignty regulations require localized data hosting, complicating global ERP deployments and increasing operational complexity for multinational enterprises.

Accelerated Cloud ERP Migration: Over 74% of new ERP deployments in 2025 were cloud-based, reducing infrastructure costs by 32% and enabling 24/7 system accessibility for global operations.

AI-Embedded ERP Analytics: AI-driven ERP modules improved demand forecasting accuracy by 29% and reduced supply chain disruptions by 26% through predictive analytics and anomaly detection.

Modular ERP Architecture Adoption: Nearly 58% of enterprises adopted modular ERP solutions, allowing phased implementation and reducing deployment timelines by 34%.

Industry-Specific ERP Customization: Vertical-focused ERP solutions increased adoption by 41% in manufacturing and healthcare, delivering compliance accuracy improvements of 23% and workflow efficiency gains of 28%.

The Enterprise Resource Planning (ERP) Software Market is segmented based on type, application, and end-user, reflecting varied enterprise requirements, deployment strategies, and operational priorities. By type, organizations differentiate ERP platforms according to deployment architecture and functional scope, with cloud-based and modular systems gaining prominence due to scalability and flexibility advantages. Application-based segmentation highlights ERP usage across core business functions such as finance, supply chain, human resources, and manufacturing operations, where real-time data integration and process automation are critical. End-user segmentation further illustrates adoption differences between large enterprises, small and medium-sized enterprises (SMEs), and industry verticals such as manufacturing, retail, healthcare, and BFSI. Decision-makers increasingly evaluate ERP solutions based on interoperability, customization capability, and industry alignment, making segmentation a key determinant of purchasing behavior and long-term platform value.

The ERP Software Market by type includes cloud-based ERP, on-premise ERP, and hybrid ERP solutions. Cloud-based ERP currently accounts for approximately 61% of overall adoption, driven by faster deployment cycles, subscription-based cost models, and remote accessibility. On-premise ERP systems represent around 24%, remaining relevant in highly regulated industries that require full data control. Hybrid ERP solutions, combining cloud scalability with on-premise security, account for the remaining 15% and are often adopted by large enterprises managing legacy systems.

Cloud-based ERP is also the fastest-growing type, expanding at an estimated 15.2% CAGR, supported by multi-tenant architectures, continuous updates, and native AI integration. On-premise ERP growth remains moderate, while hybrid ERP adoption is rising steadily among enterprises transitioning legacy infrastructure. Collectively, non-cloud ERP types contribute 39% of total deployments, serving niche compliance and customization needs.

In 2025, a national public-sector digitization program implemented a cloud-based ERP platform across more than 200 government agencies, standardizing procurement and financial workflows and reducing processing delays by over 25%.

By application, finance and accounting ERP modules lead with nearly 34% of total usage, as enterprises prioritize unified financial reporting, compliance automation, and cost visibility. Supply chain and inventory management applications follow at 27%, reflecting the need for real-time logistics coordination and demand planning. Human resource management ERP applications account for 18%, supporting workforce analytics and payroll automation.

Supply chain-focused ERP applications are the fastest-growing, with adoption increasing at an estimated 14.6% CAGR, driven by global trade volatility and the need for predictive planning tools. Manufacturing execution and CRM-integrated ERP modules collectively contribute 21%, addressing production scheduling and customer engagement requirements.

Consumer adoption trends indicate that in 2025, over 41% of global enterprises piloted ERP-integrated analytics for supply chain optimization, while 58% of digitally mature firms embedded ERP insights directly into executive dashboards.

In 2024, a multinational retail network deployed ERP-driven supply chain optimization across 1,500 outlets, improving inventory turnover by 19% and reducing stockouts by 23%.

Large enterprises dominate ERP adoption, accounting for approximately 57% of deployments, due to complex multi-location operations and higher IT budgets. SMEs represent 31%, increasingly adopting cloud ERP to replace fragmented accounting and operations tools. Public sector and non-profit organizations contribute the remaining 12%, focusing on transparency and compliance.

SMEs are the fastest-growing end-user group, with ERP adoption expanding at an estimated 16.1% CAGR, fueled by affordable SaaS pricing and pre-configured industry templates. Manufacturing enterprises show adoption rates exceeding 68%, while retail and logistics sectors report ERP penetration of 54% and 49%, respectively. In 2025, more than 36% of SMEs globally reported using ERP platforms to automate at least three core business functions.

In 2025, a nationwide SME modernization initiative enabled over 600 mid-sized manufacturers to deploy ERP systems, resulting in an average 21% improvement in order fulfillment efficiency.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.4% between 2026 and 2033.

Europe followed North America with a 29% share, driven by strong regulatory-led digital transformation, while Asia-Pacific held 23%, supported by rapid enterprise digitization and SME adoption. South America accounted for 6%, reflecting steady modernization across key industries, and the Middle East & Africa represented the remaining 4%, supported by government-led digital infrastructure programs. Collectively, these regional shares total 100%, reflecting a balanced global distribution shaped by enterprise maturity levels, regulatory frameworks, and technology investment intensity across regions.

North America holds approximately 38% of the global Enterprise Resource Planning (ERP) Software Market, supported by high enterprise IT spending and early adoption of cloud technologies. Key demand is driven by healthcare, BFSI, manufacturing, and retail sectors, where over 65% of large enterprises operate multi-module ERP systems. Regulatory initiatives supporting digital records, financial transparency, and cybersecurity compliance continue to reinforce adoption. Technological advancements include widespread integration of AI-driven analytics and automation, with nearly 60% of ERP deployments incorporating predictive features. Local players and system integrators are expanding industry-specific ERP configurations, while regional consumer behavior shows higher ERP penetration in healthcare and finance compared to other sectors.

Europe accounts for nearly 29% of the global ERP software landscape, with Germany, the UK, and France leading adoption. Regulatory frameworks related to data protection, financial reporting, and sustainability reporting have increased ERP deployment across enterprises, particularly in manufacturing and public services. Over 58% of European enterprises use ERP systems to manage compliance workflows. Adoption of cloud and hybrid ERP models is accelerating, with explainable and auditable system designs gaining importance. Regional players are focusing on modular ERP solutions aligned with ESG and reporting standards. Consumer behavior reflects strong demand for transparency-driven and regulation-compliant ERP platforms.

Asia-Pacific holds approximately 23% of the global market and ranks as the fastest-growing region by adoption momentum. China, India, and Japan collectively account for over 70% of regional ERP usage. Rapid industrialization, expanding manufacturing bases, and rising SME digitalization are key growth enablers. Nearly 46% of new ERP deployments in the region are cloud-native, driven by cost efficiency and scalability. Innovation hubs across India and Southeast Asia are fostering ERP customization for e-commerce and logistics. Regional consumer behavior highlights strong demand driven by mobile-first enterprise operations and digitally enabled supply chains.

South America represents about 6% of the global ERP software market, with Brazil and Argentina as leading adopters. ERP demand is driven by infrastructure development, energy, retail, and manufacturing sectors. Government-backed digital tax systems and trade compliance requirements have accelerated ERP adoption, particularly among mid-sized enterprises. Around 42% of enterprises in the region use ERP platforms primarily for financial and inventory management. Local vendors focus on language localization and sector-specific customization. Consumer behavior indicates demand closely tied to media, retail, and cross-border trade operations.

The Middle East & Africa region accounts for approximately 4% of global ERP adoption. Demand is concentrated in oil & gas, construction, public administration, and utilities. The UAE and South Africa together represent over 55% of regional ERP deployments. National digital transformation programs and cross-border trade partnerships are encouraging ERP adoption, particularly cloud-based solutions. Local system integrators are delivering ERP platforms tailored to regulatory and language requirements. Regional consumer behavior reflects growing interest in ERP systems that support project-based operations and compliance tracking.

United States – 31% Market Share: Strong enterprise IT investment, high cloud ERP penetration, and advanced digital infrastructure.

Germany – 14% Market Share: High manufacturing digitization levels and regulatory-driven adoption across industrial enterprises.

The Enterprise Resource Planning (ERP) Software Market exhibits a moderately consolidated competitive environment with a broad mix of established global vendors and rising challengers. There are dozens of active competitors ranging from large multinational corporations to specialized ERP innovators, collectively serving millions of enterprises worldwide. The market’s top players hold a combined share of approximately 22.3% of total ERP deployments when measured by revenue-based market share estimations, with Oracle (~6.63%), SAP (~6.57%), Microsoft Dynamics (~4.0%), Workday (~2.5%), and Sage (~2.3%) among the leading contributors to this collective share.

This competitive field is shaped by strategic initiatives such as AI-powered feature rollouts, enhanced cloud-native platforms, and expanded industry-specific solutions. Major vendors like Oracle and Microsoft are deepening integration with generative AI and predictive analytics to address evolving enterprise needs for automation and real-time insights. SAP’s continued enhancements to SAP S/4HANA and cloud migration programs illustrate sustained product innovation, while mid-sized players such as Odoo and IFS demonstrate rapid ARR and cloud revenue growth, signaling dynamic market movement.

Partnerships, platform expansions, and ecosystem development are further intensifying competition. For example, integrations with major cloud providers and AI services enhance ERP scalability and functionality. Regional players and specialized ERP vendors contribute niche capabilities that challenge larger incumbents in targeted segments such as manufacturing and service industries. Overall, the competitive landscape reflects high innovation velocity, strategic collaboration, and differentiated value propositions that influence enterprise adoption decisions globally.

Workday, Inc.

Sage Group plc

Infor

Acumatica, Inc.

Epicor Software Corporation

IFS AB

Odoo

Deltek

HashMicro

Cegid

Unit4

Current and emerging technologies are profoundly reshaping the Enterprise Resource Planning (ERP) Software Market, accelerating digital transformation and operational resilience across global enterprises. Cloud-native architectures dominate implementations, with over 65% of ERP deployments supported as SaaS-based solutions due to their scalability, rapid upgrades, and remote access advantages. These platforms integrate real-time analytics, machine learning, and AI-driven automation to optimize workflows across finance, supply chain, HR, and customer engagement. ERP systems increasingly embed AI copilots and predictive modeling tools that support automated forecasting, anomaly detection, and intelligent decision support, significantly reducing manual intervention and increasing process efficiency.

Emerging technologies such as low-code/no-code development environments are enabling organizations to rapidly customize ERP workflows without extensive IT overhead, fostering agility and faster time-to-value. Mobile-first ERP interfaces are also on the rise, allowing field users to perform critical functions such as inventory updates and approvals on the go, reflecting broader trends in decentralized workforces. Integration with Internet of Things (IoT) sensors enhances ERP visibility in manufacturing and logistics by providing real-time asset and production data. Additionally, emerging blockchain frameworks are being evaluated to enhance transactional security, auditability, and supply chain traceability within ERP ecosystems.

AI-driven data governance frameworks, such as retrieval-augmented generation (RAG) systems and generative business process agents, are being explored to improve data quality, automated workflows, and regulatory compliance in complex enterprise environments. These advancements yield measurable improvements in query accuracy, processing speed, and uptime, reinforcing ERP’s role as a strategic intelligence platform. Collectively, these technologies elevate ERP systems from traditional transaction engines to integrated, intelligent platforms that support predictive operations, compliance, and continuous innovation.

• In December 2025, Zoho announced the launch of Zoho ERP tailored for India’s fast-scaling businesses, integrating finance, HR, inventory, and supply chain workflows into one unified platform designed for mid-sized and large enterprises, enhancing operational cohesion and digital transformation efforts. Source: www.economictimes.com

• In 2025, Oracle was recognized as having surpassed SAP in ERP application leadership, reporting ~6.63% market share, marking a significant competitive shift among major ERP vendors worldwide. Source: www.techzine.eu

• In 2025, global cloud ERP market momentum continued, with the market reaching an estimated $48.63 billion in scale, reflecting broad enterprise adoption of cloud-native ERP architectures and supporting platforms. Source: www.erp.today

• In 2024–2025, leading ERP vendors including Oracle, SAP, Microsoft, Infor, and Epicor expanded AI and automation features within ERP suites, such as AI-powered planning tools, natural language interfaces, and embedded analytics that improve user productivity and system intelligence. Source: www.forbes.com

The Enterprise Resource Planning (ERP) Software Market Report provides a comprehensive overview of technologies, segments, and regional dynamics shaping this strategic software domain. The report covers segmentation by deployment type (cloud, on-premise, hybrid), functional modules (finance, supply chain, HR, CRM), and industry vertical applications (manufacturing, healthcare, retail, BFSI, public sector). It examines how cloud-native solutions dominate deployments and how hybrid frameworks support enterprises with specific data sovereignty requirements and legacy integration needs. Geographic scope includes insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing demand drivers, consumer behavior, and regulatory influences across these markets.

In addition to core segments, the report highlights emerging niche areas such as AI-embedded ERP solutions, low-code customization platforms, mobile-first and IoT-integrated ERP interfaces, and industry-specific adaptations tailored to discrete manufacturing, healthcare operations, and logistics management. It explores trends in enterprise digital transformation strategies, examining how ERP systems enable real-time operational visibility, automation, and compliance across complex multi-site operations. The report also analyzes competitive strategies of global and regional players, including product enhancements, partnerships, and innovation pipelines that influence market positioning. Designed for business professionals and decision-makers, the scope emphasizes practical insights into ERP adoption patterns, technology integrations, and forward-looking market developments without focusing solely on historical performance, enabling stakeholders to align ERP investments with strategic business objectives.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 926.0 Million |

| Market Revenue (2033) | USD 2,604.6 Million |

| CAGR (2026–2033) | 13.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Oracle Corporation, SAP SE, Microsoft Corporation, Workday, Inc., Sage Group plc, Infor, Acumatica, Inc., Epicor Software Corporation, IFS AB,Odoo, Deltek, HashMicro, Cegid, Unit4 |

| Customization & Pricing | Available on Request (10% Customization Free) |