Reports

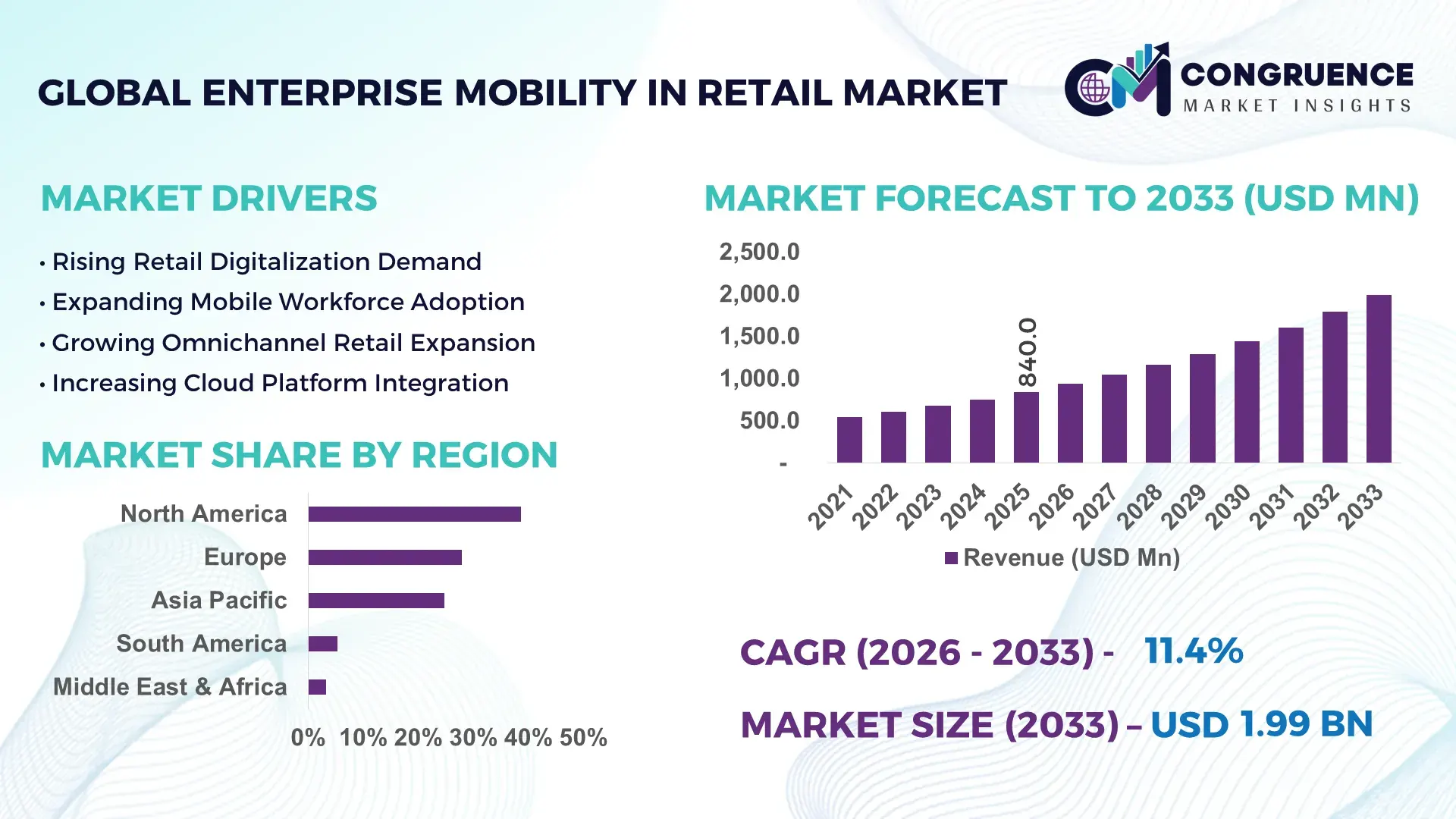

The Global Enterprise Mobility in Retail Market was valued at USD 840.0 Million in 2025 and is anticipated to reach a value of USD 1,992.3 Million by 2033 expanding at a CAGR of 11.4% between 2026 and 2033. Growth is being accelerated by rapid deployment of AI-enabled mobile POS systems, cloud-based workforce management platforms, and omnichannel retail operations that improve inventory visibility and real-time customer engagement.

The United States dominates the global Enterprise Mobility in Retail Market with approximately 36% market share, supported by widespread enterprise mobility deployment across retail chains, over 92% smartphone penetration, and multi-billion-dollar investments in AI-driven retail modernization. Compared with Germany, where enterprise mobility adoption is expanding through Industry 4.0-enabled retail networks, U.S. retailers deploy larger-scale cloud mobility ecosystems, reinforced by digital supply-chain restructuring following post-pandemic operational transformation.

This leadership reinforces North America's position as the preferred destination for enterprise mobility investments, platform innovation, and large-scale retail digital transformation strategies.

Market Size & Growth: USD 840.0 Million in 2025, reaching USD 1,992.3 Million by 2033 at 11.4% CAGR, driven by AI-powered mobile retail operations and omnichannel commerce.

Top Growth Drivers: Cloud mobility deployment (68%), mobile POS adoption (61%), and AI-enabled workforce productivity improvements (42%).

Short-Term Forecast: By 2028, retailers are expected to reduce checkout times by 35% and improve inventory accuracy by 25% through enterprise mobility platforms.

Emerging Technologies: AI analytics, edge computing, and 5G connectivity are enabling faster mobile decision-making and seamless store operations.

Regional Leaders: North America (~USD 760 Million), Europe (~USD 520 Million), and Asia-Pacific (~USD 470 Million) lead through cloud retail expansion and digital supply-chain modernization.

Consumer/End-User Trends: Nearly 70% of organized retailers prioritize mobile-first employee workflows to enhance in-store customer experience.

Pilot/Case Example: In 2025, enterprise mobile workforce deployment improved order fulfillment efficiency by approximately 28% across large retail distribution networks.

Competitive Landscape: Microsoft holds roughly 18% market presence alongside IBM, Oracle, SAP, Zebra Technologies, and VMware through advanced enterprise mobility ecosystems.

Regulatory & ESG Impact: Digital documentation and mobile workflows reduce paper consumption by nearly 40%, supporting enterprise sustainability initiatives and compliance.

Investment & Funding: More than USD 3 billion has been directed toward retail mobility software, cloud partnerships, and platform expansion amid global supply-chain digitalization.

Innovation & Future Outlook: AI copilots, predictive inventory management, and unified mobile commerce platforms are strengthening next-generation retail competitiveness.

Enterprise Mobility in Retail Market demand is expanding across omnichannel retail, warehouse operations, mobile point-of-sale, and field workforce management. AI-powered device management, secure cloud mobility platforms, and real-time analytics are improving operational responsiveness, while nearly 60% of enterprise retailers are prioritizing unified mobility ecosystems. Continued retail supply-chain optimization and stronger cybersecurity requirements are accelerating enterprise-wide digital workplace transformation, setting the stage for broader strategic adoption.

Enterprise mobility has become a strategic priority as retailers compete through faster customer engagement, connected store operations, and real-time inventory visibility. The ongoing restructuring of global retail supply chains and rapid digitalization of physical stores are encouraging enterprises to modernize legacy systems with mobile-first platforms that support agile decision-making, workforce collaboration, and seamless omnichannel fulfillment.

Compared with conventional desktop-based retail management, AI-enabled mobile enterprise platforms reduce operational processing time by nearly 30% while improving inventory accuracy by approximately 25% through real-time synchronization. North America leads large-scale enterprise deployments across national retail chains, whereas Asia-Pacific is recording faster adoption among expanding organized retailers driven by mobile commerce and cloud infrastructure investments. Over the next two to three years, enterprise adoption of unified mobility platforms is expected to exceed 70% among large retail organizations.

Retailers are increasingly deploying mobile applications for shelf management, click-and-collect coordination, and workforce scheduling. Major companies are strengthening strategic partnerships with cloud providers, cybersecurity specialists, and AI software vendors to accelerate implementation while improving operational resilience. Organizations that integrate enterprise mobility with intelligent analytics and scalable cloud ecosystems will secure stronger competitive positioning, higher operational efficiency, and greater long-term adaptability in an increasingly digital retail environment.

Retail enterprises are expanding enterprise mobility platforms to unify store operations, inventory visibility, and customer engagement across physical and digital channels. More than 72% of large retailers have adopted mobile workforce applications, while AI-enabled mobile inventory solutions improve stock accuracy by nearly 30% and reduce replenishment delays by approximately 25%. In the United States, post-pandemic retail supply-chain restructuring has accelerated investment in cloud-native mobility ecosystems that integrate warehouse, logistics, and point-of-sale operations. This operational shift enables faster fulfillment and data-driven decision-making. Leading companies are responding through strategic cloud partnerships, AI-powered mobility platforms, and enterprise device management investments, creating scalable digital retail infrastructures that strengthen operational resilience while enhancing customer experience and workforce productivity.

A significant share of retail organizations continue to operate fragmented legacy ERP and POS environments, limiting seamless enterprise mobility deployment. Around 45% of mid-sized retailers report interoperability challenges, while integration projects increase implementation costs by nearly 20% and extend deployment timelines by approximately 30%. In Japan, many established retail chains face modernization constraints because legacy store systems remain deeply embedded within daily operations. These infrastructure limitations reduce scalability, delay digital transformation initiatives, and increase operational complexity across multi-store networks. Companies are mitigating these constraints through phased cloud migration, localized systems integration partnerships, API-based architecture modernization, and long-term software support agreements that reduce deployment risk while improving compatibility across enterprise technology ecosystems.

The next phase of enterprise mobility is shifting toward intelligent automation that combines AI, edge computing, and predictive analytics for frontline retail operations. AI-assisted mobile workflows can improve employee productivity by over 35%, while predictive inventory applications reduce stock shortages by nearly 28%. In India, government-backed digital infrastructure expansion and rapid organized retail growth are accelerating enterprise cloud adoption across large retail chains. Companies are increasing investment in AI-powered mobile assistants, computer vision-enabled store operations, and ecosystem partnerships with cloud providers to create connected retail environments. A less obvious opportunity lies in integrating mobility platforms with sustainability reporting and energy management systems, enabling retailers to optimize operational efficiency while strengthening regulatory compliance and ESG performance.

As enterprise mobility platforms become central to retail operations, cybersecurity and large-scale deployment consistency have emerged as critical execution challenges. Nearly 68% of retailers identify endpoint security as a primary operational concern, while mobile-based cyber incidents have increased by approximately 32% with expanding cloud-connected retail networks. In the United Kingdom, stricter data protection requirements are increasing compliance obligations for retailers managing customer and workforce information across mobile environments. Security vulnerabilities, inconsistent device management, and shortages of enterprise mobility specialists can delay implementation and weaken operational continuity. Companies must strengthen zero-trust security frameworks, expand identity management capabilities, invest in continuous employee training, and establish long-term cybersecurity partnerships to ensure scalable, resilient, and competitive enterprise mobility deployments.

AI-Driven Store Workforce Mobility Retailers are embedding AI-enabled mobility platforms into frontline workflows to improve task execution, inventory visibility, and associate productivity. More than 58% of large retail chains now deploy AI-assisted mobile task management, while mobile-first workforce scheduling has improved labor utilization by nearly 20%. Rising labor shortages and wage pressure are accelerating handheld deployment across stores. Companies are responding by integrating predictive analytics, digital work instructions, and multilingual mobile interfaces, reducing task completion time while improving customer service consistency across distributed retail operations.

Unified Omnichannel Operations Expansion Retail enterprises are consolidating point-of-sale, order fulfillment, and customer engagement onto unified mobile platforms. Nearly 64% of enterprise retailers have expanded mobile-enabled click-and-collect workflows, while mobile order visibility has shortened fulfillment cycles by approximately 27%. Growing omnichannel demand and supply-chain volatility are driving this operational shift. Vendors are expanding cloud-native mobility suites, strengthening ERP integration, and forming technology partnerships that enable faster inventory synchronization across stores, warehouses, and fulfillment hubs.

Edge Security and Device Governance Enterprise mobility strategies increasingly prioritize zero-trust security and centralized endpoint management as mobile endpoints continue to multiply. Around 61% of retailers have adopted unified endpoint management platforms, while biometric authentication deployment has increased by nearly 35% since 2025. Tightening privacy regulations and growing cyber risks are prompting retailers to automate device provisioning, compliance monitoring, and remote security controls. Companies are scaling managed mobility services to reduce operational downtime while maintaining secure access across geographically dispersed retail locations.

Purpose-Built Mobility Ecosystems Retailers are replacing fragmented mobile applications with integrated enterprise mobility ecosystems supporting inventory, payments, merchandising, and supplier collaboration through a single interface. Approximately 46% of new mobility deployments now utilize low-code customization, while mobile process automation has reduced manual administrative activities by nearly 22%. A less obvious trend is the growing use of mobility analytics to optimize store layouts based on associate movement patterns. Technology providers are expanding ecosystem partnerships and modular deployment models that accelerate implementation while minimizing operational disruption.

Cloud-based enterprise mobility solutions remain the leading type, accounting for approximately 68% of enterprise deployments due to superior scalability, centralized management, and seamless integration with retail ERP, CRM, and inventory systems. Cloud deployment enables real-time application updates, simplified device administration, and lower infrastructure costs, making it particularly attractive for multi-store retailers. On-premises solutions continue serving organizations with stringent data governance requirements, especially among established retailers operating legacy infrastructure. Hybrid deployment models represent the fastest-growing segment, expanding rapidly as enterprises balance cloud flexibility with localized security and operational continuity. Retail technology providers are expanding hybrid architecture capabilities, API integration, and managed migration services to support phased modernization initiatives. Nearly 42% of new enterprise implementations now incorporate hybrid deployment strategies, while over 55% of retailers prioritize interoperability during mobility platform selection. Investment priorities continue shifting toward unified cloud management, edge synchronization, and resilient deployment architectures that minimize business disruption while supporting future digital transformation initiatives.

Inventory management represents the leading application as retailers increasingly depend on mobile devices for stock visibility, replenishment, barcode scanning, and warehouse coordination. Mobile inventory applications now support nearly 65% of enterprise store operations, reducing stock discrepancies while improving replenishment accuracy. Point-of-sale applications remain widely deployed for customer transactions, whereas workforce management solutions continue expanding across large retail networks. Customer engagement applications, including assisted selling and personalized promotions, are emerging as the fastest-growing segment as retailers focus on improving omnichannel shopping experiences. Retail organizations continue integrating mobile applications across merchandising, fulfillment, customer service, and payment workflows through unified enterprise platforms. Nearly 48% of retailers have expanded mobile-assisted selling capabilities, while mobile fulfillment coordination has improved order processing efficiency by approximately 24%. Vendors are enhancing application interoperability, AI-enabled workflow automation, and real-time analytics to strengthen operational responsiveness while supporting evolving omnichannel business models.

Large retail enterprises remain the dominant end-user segment because of extensive store networks, complex supply chains, and significant investments in enterprise-wide digital transformation. This segment represents nearly 70% of enterprise mobility deployments, supported by higher IT budgets and continuous modernization initiatives. Small and medium-sized retailers are the fastest-growing end-user group as cloud-based subscription platforms lower deployment costs and simplify implementation. Franchise operators and specialty retail chains continue increasing adoption to standardize operations across geographically distributed locations. Solution providers are introducing scalable pricing models, industry-specific mobility packages, and managed deployment services tailored to different enterprise sizes. Nearly 44% of new mobility contracts now target mid-sized retailers seeking integrated workforce and inventory platforms, while ecosystem partnerships have expanded deployment flexibility across independent retail groups. Competitive positioning increasingly depends on rapid implementation, customization, and seamless integration with existing retail technology ecosystems.

North America accounted for the largest market share at 38.7% in 2025 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

North America continues to lead the Enterprise Mobility in Retail market due to extensive digital transformation initiatives, widespread adoption of cloud-native retail platforms, and strong investment in AI-powered workforce mobility solutions. The region contributes nearly 38.7% of global market revenue, supported by high penetration of handheld POS devices, mobile inventory management systems, and omnichannel fulfillment platforms. Major retailers continue expanding mobile-first store operations to improve customer engagement and operational efficiency. In 2025, several leading retail enterprises accelerated enterprise mobility deployments by integrating AI-assisted inventory monitoring and mobile workforce applications across more than 5,000 retail locations, strengthening real-time operational visibility while reducing fulfillment cycle times.

United States Market Outlook: The United States remains the largest contributor to regional growth due to its highly digitized retail ecosystem, advanced cloud infrastructure, and strong enterprise technology spending. Large retailers continue deploying enterprise mobility platforms across stores, warehouses, and fulfillment centers to improve workforce productivity and customer experience. More than 80% of Tier-1 retail chains have implemented mobile workforce or handheld retail management solutions, while ongoing investments in AI-enabled analytics, 5G connectivity, and edge computing continue enhancing enterprise mobility capabilities throughout the retail value chain.

Europe is experiencing sustained growth in enterprise mobility adoption as retailers modernize store operations, strengthen omnichannel capabilities, and comply with evolving digital governance requirements. The region accounts for approximately 27.9% of the global market, supported by widespread implementation of mobile payment systems, workforce collaboration platforms, and cloud-based inventory management solutions. Large retail groups continue investing in connected store infrastructure to improve operational resilience and customer engagement. During 2025, multiple European retail organizations expanded enterprise mobility initiatives through cloud migration and smart device deployment programs, enabling mobile operational management across thousands of retail outlets while improving inventory accuracy and employee productivity.

Germany Market Outlook: Germany serves as the region's most strategically important market owing to its strong retail infrastructure, advanced enterprise software adoption, and leadership in industrial digitalization. Leading retailers continue investing in mobile POS systems, warehouse mobility solutions, and AI-enabled inventory optimization platforms to streamline operations. More than 70% of large retail enterprises have adopted integrated enterprise mobility technologies to support omnichannel fulfillment, while continued investments in cloud infrastructure and secure enterprise connectivity strengthen long-term market expansion.

Asia-Pacific represents the fastest-evolving regional market, supported by expanding organized retail, widespread smartphone adoption, and accelerated enterprise digitalization across emerging and developed economies. The region accounts for approximately 24.8% of the global market, with retailers increasingly deploying mobile POS systems, warehouse mobility platforms, and AI-enabled inventory management tools. Strong cloud adoption and expanding 5G infrastructure continue enabling real-time retail operations across large store networks. In 2025, leading retailers and technology providers expanded enterprise mobility deployments across more than 12,000 retail outlets throughout Asia-Pacific, strengthening workforce productivity, improving omnichannel fulfillment efficiency, and enhancing customer engagement through integrated mobile retail ecosystems.

China Market Outlook: China remains the region's largest market due to its extensive retail infrastructure, mature digital commerce ecosystem, and strong government support for digital transformation. Major retailers continue integrating enterprise mobility with AI, IoT, and cloud-based operational platforms to optimize inventory visibility and customer service. More than 85% of large organized retailers have deployed mobile workforce management or smart retail technologies, while continuous investment in nationwide 5G networks and intelligent logistics infrastructure reinforces enterprise-scale mobility adoption across physical and digital retail channels.

South America is steadily expanding enterprise mobility adoption as retailers modernize operations to improve customer experience and supply chain visibility. The region contributes nearly 5.3% of the global market, with investments focused on mobile inventory management, digital payment solutions, and workforce productivity applications. Large retail groups are prioritizing cloud-based mobility platforms to support omnichannel fulfillment while improving operational efficiency across distributed store networks. During 2025, several regional retailers expanded enterprise mobility initiatives through partnerships with cloud technology providers, enabling connected retail operations across more than 2,000 stores despite continuing infrastructure disparities and varying enterprise digital maturity across countries.

Brazil Market Outlook: Brazil dominates the regional market through its large organized retail sector, expanding cloud adoption, and increasing enterprise investment in digital operations. Leading retailers continue implementing mobile POS devices, warehouse mobility solutions, and AI-assisted inventory management systems to improve operational responsiveness. The country's rapidly expanding digital payment ecosystem and widespread smartphone penetration support enterprise mobility integration, while major retail organizations continue modernizing nationwide store networks with connected mobile technologies that enhance employee productivity and customer engagement.

The Middle East & Africa market is progressing through sustained investments in digital infrastructure, smart city initiatives, and retail modernization programs. The region accounts for approximately 3.3% of the global market, with enterprise mobility adoption increasing across organized retail, supermarkets, and large shopping centers. Retailers are implementing mobile workforce management, cloud-based inventory systems, and digital customer engagement platforms to strengthen operational performance. In 2025, multiple retail modernization initiatives supported deployment of enterprise mobility solutions across over 1,500 commercial retail locations, reflecting continued investment in connected retail ecosystems despite uneven digital infrastructure across several developing markets.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption owing to its advanced digital infrastructure, smart government initiatives, and highly developed retail sector. Large retail enterprises continue deploying cloud-enabled mobility platforms, mobile checkout technologies, and AI-supported workforce management solutions to enhance operational efficiency. Strong investment in smart retail developments and high enterprise cloud utilization provide a favorable environment for enterprise mobility expansion, while modern shopping destinations increasingly integrate connected digital technologies to deliver seamless omnichannel retail experiences.

Enterprise mobility in retail is led by Microsoft, Zebra Technologies, Honeywell, SOTI, VMware, and Ivanti, with cloud-platform providers competing against rugged-device OEMs while enterprise mobility management specialists challenge integrated ecosystem vendors. The top five players collectively control approximately 58% of the global market, reflecting moderate concentration. Competition is driven by AI-enabled mobility, unified endpoint management, device lifecycle services, and seamless cloud integration rather than price alone. AI-powered workflow automation improves frontline productivity by nearly 25%, while centralized device management lowers support costs by around 20%. Global vendors strengthen positions through strategic partnerships, retail-specific platform expansion, and vertical integration of hardware, software, and managed services. Regional providers compete through faster deployment, localized customization, and lower implementation costs. The competitive shift favors AI-native, cloud-first platforms over standalone mobility software. High switching costs, cybersecurity compliance, and enterprise integration remain key entry barriers. Winning requires scalable platforms, proven retail expertise, rapid innovation, and ecosystem partnerships.

Zebra Technologies

Honeywell

VMware

SOTI

Ivanti

IBM

Cisco Systems

SAP

Oracle

Samsung Electronics

Panasonic Connect

Enterprise mobility in retail is increasingly powered by AI-enabled mobile computing, unified endpoint management (UEM), cloud-native mobility platforms, edge computing, RFID, and 5G connectivity. Retailers are integrating mobile POS, digital inventory, computer vision, and predictive analytics into a single mobility ecosystem. AI-assisted task management improves workforce productivity by approximately 20%, while cloud-based device management reduces administration effort by nearly 30%. More than 65% of large retailers are deploying centralized mobility management platforms to support distributed store operations and real-time decision-making.

Modern AI-enabled mobility platforms outperform conventional device-centric systems by delivering nearly 35% faster issue resolution, automated security enforcement, and continuous software updates. Retailers adopting integrated hardware-software ecosystems gain stronger operational visibility, lower downtime, and faster rollout of new digital services. Global technology vendors benefit most through scalable cloud architectures and broad partner ecosystems, while retailers achieve higher inventory accuracy and improved customer engagement.

Between 2026 and 2028, autonomous device management, generative AI assistants, digital twins, and edge AI will reshape enterprise mobility deployments. Organizations investing early in intelligent mobility platforms will strengthen operational resilience, reduce support costs, accelerate omnichannel execution, and build lasting competitive differentiation as retail technology ecosystems become increasingly software-defined.

January 2025 – Zebra Technologies introduced Zebra Companion and the Mobile Computing AI Suite for retail frontline operations, adding multimodal AI agents and vision AI capabilities. The platform supports organizations operating in more than 100 countries, strengthening intelligent store productivity and workforce automation. Source: www.zebra.com

January 2025 – Honeywell partnered with Verizon to launch a bundled enterprise mobility service combining rugged devices, lifecycle management, and 5G connectivity into a single managed offering, reducing procurement complexity through one unified contract, improving deployment speed and operational resilience.

August 2025 – SOTI announced a strategic partnership with Advantech, integrating SOTI MobiControl and XSight across four operating systems (Android, iOS, Windows, Linux), expanding enterprise mobility management for smart retail and strengthening scalable edge-device lifecycle management.

January 2026 – Business Wire reported Zebra Technologies expanded its AI-powered retail portfolio at NRF 2026, showcasing intelligent hardware, software, and automation solutions supporting 80% of Fortune 500 customers, reinforcing its leadership in connected frontline retail operations.

The report provides comprehensive coverage of enterprise mobility solutions across hardware, software, cloud platforms, enterprise mobility management, mobile POS, inventory mobility, analytics, and managed services. It evaluates deployment across supermarkets, specialty retailers, convenience stores, department stores, and omnichannel retailers while assessing adoption trends throughout North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The study also examines AI-enabled mobility, RFID, 5G, edge computing, cloud integration, and unified endpoint management, with adoption levels exceeding 65% among large retail enterprises in advanced markets.

The analysis supports strategic planning between 2026 and 2033 through detailed segmentation by type, application, end-user, and region, alongside competitive benchmarking covering major global technology providers. It highlights deployment patterns, digital transformation priorities, ecosystem partnerships, emerging retail mobility applications, and investment opportunities, enabling stakeholders to strengthen competitive positioning, prioritize expansion strategies, evaluate technology readiness, and identify high-potential niche segments across evolving retail mobility ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 840.0 Million |

| Market Revenue (2033) | USD 1,992.3 Million |

| CAGR (2026–2033) | 11.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft; Zebra Technologies; Honeywell; VMware; SOTI; Ivanti; IBM; Cisco Systems; SAP; Oracle; Samsung Electronics; Panasonic Connect |

| Customization & Pricing | Available on Request (10% Customization Free) |