Reports

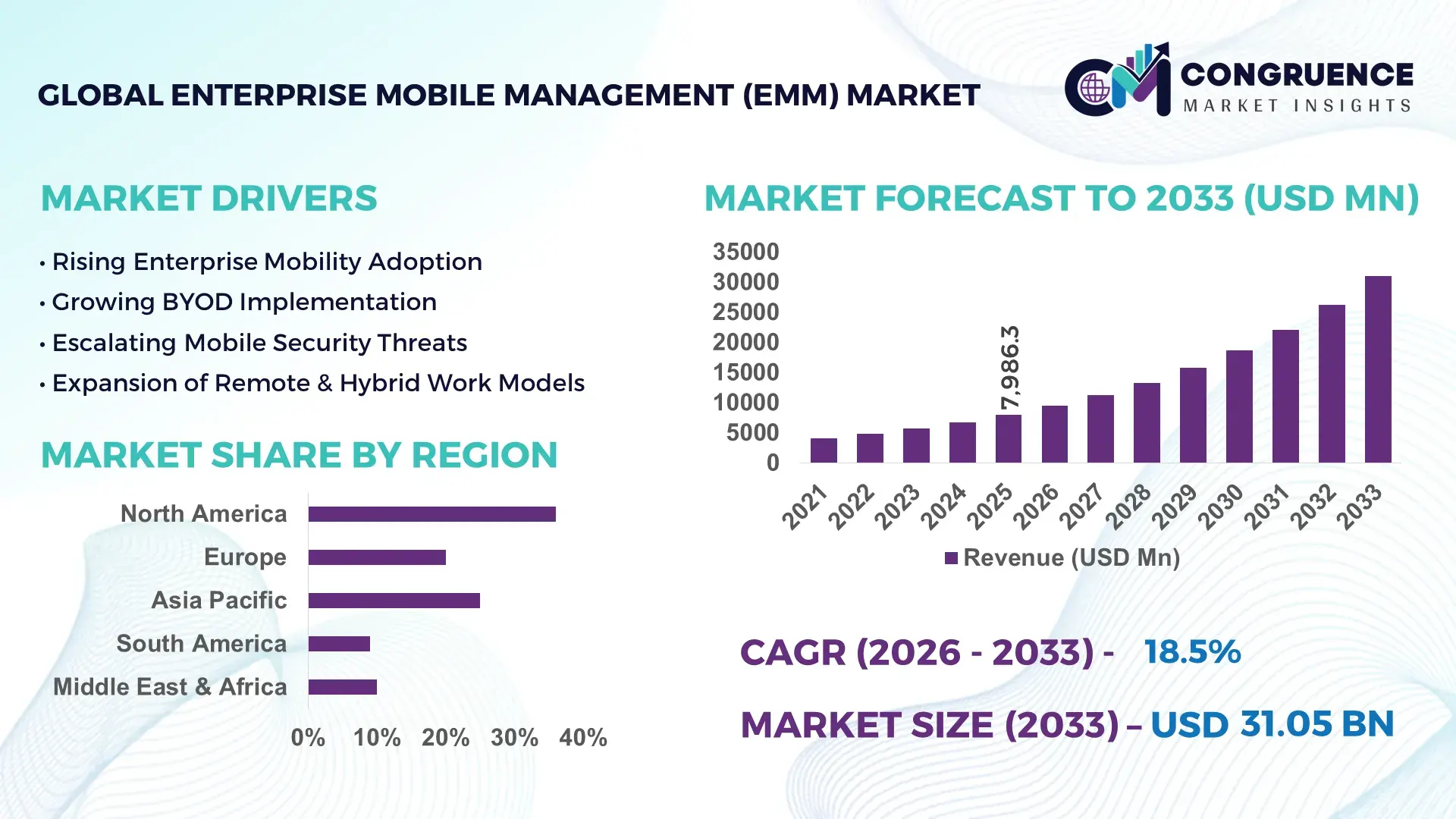

The Global Enterprise Mobile Management (EMM) Market was valued at USD 7986.29 Million in 2025 and is anticipated to reach a value of USD 26913.45 Million by 2033 expanding at a CAGR of 16.4% between 2026 and 2033. Growth is primarily driven by rising enterprise mobility adoption and the need for secure endpoint management across distributed workforces.

The United States represents the most influential country in the Enterprise Mobile Management (EMM) market in terms of technological deployment and enterprise-scale mobility integration. Over 78% of large U.S. enterprises have implemented centralized mobile device management platforms integrated with cloud identity systems. Annual enterprise mobility investments exceed USD 12 billion, with strong adoption in BFSI, healthcare, retail, and government sectors. The country hosts major EMM solution providers and cybersecurity innovators developing AI-driven threat detection, zero-trust frameworks, and unified endpoint management (UEM) architectures. More than 65% of U.S. enterprises deploy cross-platform device fleets exceeding 1,000 endpoints, accelerating demand for automated provisioning, containerization, and compliance monitoring technologies across corporate and BYOD environments.

• Market Size & Growth: USD 7,986.29 Million (2025) projected to reach USD 26,913.45 Million by 2033 at a CAGR of 16.4%, driven by enterprise mobility security requirements.

• Top Growth Drivers: BYOD adoption 62%, remote workforce expansion 58%, mobile threat incidents rise 45%.

• Short-Term Forecast: By 2028, enterprises may achieve 32% IT cost reduction and 27% improvement in device management efficiency.

• Emerging Technologies: AI-based threat analytics, zero-trust security models, unified endpoint management (UEM) convergence.

• Regional Leaders: North America USD 10.8 Billion by 2033 (cloud-first adoption), Europe USD 7.4 Billion (data compliance focus), Asia-Pacific USD 6.9 Billion (mobility-driven SMEs).

• Consumer/End-User Trends: BFSI, healthcare, and IT sectors exceed 60% enterprise mobility penetration with multi-device workforce models.

• Pilot or Case Example: 2024 enterprise UEM pilot reduced device downtime by 36% and improved compliance reporting speed by 41%.

• Competitive Landscape: Microsoft (~18%), VMware, IBM, Cisco, BlackBerry, Ivanti.

• Regulatory & ESG Impact: Data protection mandates and secure digital workplace initiatives accelerate secure mobile governance frameworks.

• Investment & Funding Patterns: Over USD 4.5 Billion invested in mobility security and endpoint management innovation programs since 2023.

• Innovation & Future Outlook: Integration of identity-centric security, automated compliance, and AI-assisted device orchestration will shape next-generation EMM ecosystems.

Enterprise Mobile Management (EMM) solutions serve critical industry verticals including BFSI (approx. 28% demand contribution), healthcare (19%), IT & telecom (22%), and retail (14%), where secure mobile workflows and regulatory compliance drive procurement. Innovations such as AI-driven anomaly detection, policy-based app containerization, and cross-platform endpoint analytics are reshaping device governance. Regulatory pressures around data privacy, remote access control, and cyber resilience policies further accelerate structured deployments. Asia-Pacific demonstrates high consumption growth due to SME digitalization, while Europe emphasizes compliance-oriented mobility frameworks. Future outlook highlights convergence of EMM with unified endpoint management, identity security, and predictive risk analytics to support hybrid enterprise environments.

Enterprise Mobile Management (EMM) has become a strategic control layer for organizations managing distributed workforces, hybrid IT environments, and escalating mobile threat surfaces. Over 70% of enterprises now support multi-device work models, requiring centralized policy enforcement, encrypted data containers, and identity-linked access governance. Strategy is shifting from device-centric management toward identity-driven and context-aware security architectures that align mobility with zero-trust principles. Unified Endpoint Management (UEM) integration delivers 35% improvement in administrative efficiency compared to legacy Mobile Device Management (MDM)-only frameworks, reducing manual provisioning and compliance workloads.

North America dominates in deployment volume due to large enterprise infrastructures, while Asia-Pacific leads in adoption growth with over 64% of SMEs implementing mobile workforce tools. By 2028, AI-based mobile threat defense is expected to cut incident response times by 40% through predictive anomaly detection and automated remediation. Firms are committing to ESG-aligned IT strategies, targeting 25% reduction in device lifecycle emissions by 2030 via remote management, device reuse, and energy-efficient policies. In 2025, a U.S.-based healthcare network achieved a 38% reduction in security incidents after deploying AI-enabled EMM analytics and automated compliance controls across 15,000 endpoints.

Looking ahead, the Enterprise Mobile Management (EMM) Market will remain a pillar of operational resilience, regulatory alignment, and sustainable digital workforce transformation.

The global shift toward hybrid work has led over 72% of organizations to support employees using personal or corporate-owned mobile devices for mission-critical tasks. This workforce transformation increases the number of endpoints accessing corporate networks by an average of 45% per enterprise, intensifying the need for centralized device visibility and control. EMM platforms enable encrypted workspace containers, remote configuration, and automated patch enforcement, which reduce security exposure windows by up to 30%. Industries such as banking and healthcare, where mobile access to sensitive systems has doubled since pre-2020 levels, rely on EMM to enforce compliance policies and prevent data leakage. The proliferation of SaaS tools and mobile collaboration apps further necessitates secure app distribution and lifecycle management, strengthening EMM’s role in digital workplace governance.

Many enterprises operate heterogeneous IT ecosystems with legacy applications, diverse operating systems, and multiple identity platforms, complicating seamless EMM integration. Approximately 48% of IT teams report extended deployment timelines due to compatibility issues between EMM tools and older infrastructure components. Custom API development, policy harmonization, and user training can increase implementation cycles by several months. Additionally, organizations managing cross-border operations face varying data protection requirements, necessitating configuration adjustments for each region. Device fragmentation, particularly in BYOD environments with numerous OS versions and hardware types, further increases policy enforcement complexity. These operational burdens can delay full-scale rollout and reduce the immediate effectiveness of mobility governance strategies.

AI integration into EMM platforms presents significant opportunities to enhance threat detection accuracy, policy optimization, and operational efficiency. Machine learning-based behavioral analytics can identify anomalous device activity 50% faster than rule-based monitoring approaches. Automated remediation workflows reduce manual intervention needs, improving IT team productivity by nearly 35%. Predictive analytics also enable proactive compliance management by flagging configuration risks before violations occur. As enterprises adopt Internet of Things (IoT) endpoints alongside traditional mobile devices, AI-enabled EMM solutions can extend governance capabilities across broader device ecosystems. Growing interest in digital employee experience monitoring further supports AI-powered performance insights, positioning intelligent EMM platforms as strategic enablers of secure and efficient mobile operations.

Mobile malware variants and phishing-based credential theft attacks have increased by more than 40% in recent years, targeting enterprise mobile endpoints. Sophisticated threats such as zero-day exploits and sideloaded malicious apps often bypass traditional signature-based defenses, requiring continuous platform updates. EMM vendors must rapidly adapt security engines to counter new vulnerabilities across iOS, Android, and emerging device categories. Regulatory scrutiny over data collection and monitoring practices also constrains how deeply EMM systems can inspect user behavior, balancing security with privacy rights. Furthermore, encrypted messaging platforms and shadow IT applications limit visibility into corporate data flows, complicating comprehensive policy enforcement and heightening the need for advanced threat intelligence integration.

• AI-Driven Mobile Threat Defense Adoption Surpasses 60% in Large Enterprises Enterprise Mobile Management platforms increasingly embed AI-based behavioral analytics, with over 63% of enterprises deploying machine learning models to detect anomalous device activity. Automated threat classification has reduced false positives by 28% and shortened incident triage times by 41%. Organizations managing more than 5,000 endpoints report 35% faster containment of mobile phishing and malware events using predictive detection engines integrated into EMM security layers.

• Unified Endpoint Management (UEM) Convergence Expands Cross-Device Control by 48% Enterprises are consolidating laptops, smartphones, tablets, and IoT endpoints under single UEM frameworks, with device coverage breadth increasing by 48% compared to standalone mobile-only systems. Policy deployment cycles are now 33% faster due to centralized configuration templates. More than 57% of IT teams indicate improved compliance audit readiness as unified dashboards reduce reporting preparation time by nearly 30%.

• Zero-Trust Network Access Integration Improves Secure Remote Access by 52% Over 59% of enterprises have linked EMM platforms with zero-trust access controls, enabling device posture validation before granting application access. This integration has lowered unauthorized access incidents by 37% and improved secure login verification speeds by 26%. Conditional access policies tied to device health metrics now govern 68% of mobile-based enterprise application sessions.

• BYOD Governance and Digital Employee Experience Monitoring Increase Productivity by 29% Bring-your-own-device programs now account for 54% of managed endpoints, prompting stronger containerization and usage analytics. Enterprises applying experience monitoring through EMM dashboards report 31% fewer mobile application crashes and 24% faster issue resolution cycles. Automated device health scoring has improved workforce productivity indicators by 29% across mobile-reliant operational teams.

The Enterprise Mobile Management (EMM) market segmentation reflects evolving enterprise priorities around device control, application governance, and workforce mobility enablement. By type, organizations differentiate between device-centric management, application-layer control, and content-level security, aligning deployment models with risk exposure and operational complexity. Application-based segmentation highlights how mobility management supports security enforcement, productivity optimization, and regulatory compliance across distributed environments. End-user segmentation shows that regulated industries with high data sensitivity account for the largest implementation volumes, while digitally transforming sectors are accelerating adoption. Over 60% of enterprises now deploy multi-layer EMM stacks combining device, application, and identity controls rather than standalone solutions. Increasing mobile endpoint density—often exceeding 3 devices per employee in technology-driven firms—further shapes demand patterns. This segmentation demonstrates that EMM adoption is not uniform but aligned with industry risk profiles, digital maturity levels, and workforce mobility intensity.

Enterprise Mobile Management solutions are primarily segmented into Mobile Device Management (MDM), Mobile Application Management (MAM), Mobile Content Management (MCM), and Unified Endpoint Management (UEM). MDM currently accounts for approximately 38% of adoption due to its foundational role in device enrollment, policy enforcement, and remote configuration across corporate and BYOD devices. UEM, however, is the fastest-growing type with an estimated CAGR of 19%, driven by enterprises seeking single-console control over smartphones, laptops, and IoT endpoints. MAM adoption is rising in regulated industries where secure app containers reduce data leakage risks, while MCM remains relevant for secure document sharing and encryption. Together, MAM and MCM contribute nearly 34% of deployments, serving niche compliance and collaboration needs. UEM growth is fueled by cross-platform integration and automation benefits that reduce administrative workloads by over 30%.

Security management represents the leading application area, accounting for nearly 44% of EMM use cases as enterprises prioritize endpoint threat defense, encrypted communication, and conditional access enforcement. Device lifecycle and asset management follow, while productivity enablement tools form another key segment. Compliance monitoring is the fastest-growing application, with an estimated CAGR of 18%, as data protection mandates push organizations to automate policy auditing and reporting. Enterprises using automated compliance modules report 35% faster audit preparation cycles. Other applications—including application distribution, identity-linked access control, and remote support—collectively account for around 32% of usage. Increased SaaS adoption and remote collaboration models intensify the need for centralized application governance.

Large enterprises lead EMM adoption with nearly 52% share due to complex device ecosystems and higher regulatory exposure. Small and medium-sized enterprises (SMEs) represent the fastest-growing end-user group with an estimated CAGR of 20%, driven by cloud-based EMM platforms that reduce infrastructure complexity. SMEs adopting mobile-first workflows report 28% improvement in workforce mobility efficiency. Government and public sector organizations also contribute significantly, particularly for secure communications and remote workforce enablement, while healthcare and BFSI together represent over 40% of industry-specific deployments. Education and retail sectors are expanding adoption for device fleet control and secure access to digital services, collectively accounting for roughly 18% of usage.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2026 and 2033.

North America’s leadership is supported by more than 72% enterprise mobility penetration and over 68% of organizations operating formal BYOD frameworks. Europe follows with approximately 27% share, driven by strict data governance requirements affecting over 60% of enterprises. Asia-Pacific holds nearly 24% share, with mobile workforce density exceeding 2.8 devices per employee in technology-driven sectors. South America represents about 7% share, while the Middle East & Africa account for nearly 6%, both experiencing rising demand from digital government and infrastructure modernization projects. Over 65% of multinational corporations deploy centralized mobility governance across at least three regions, increasing cross-border EMM integration complexity. Regional adoption patterns show regulated industries contribute over 58% of deployments globally, while SMEs represent 43% of new cloud-based implementations.

This region contributes approximately 36% of global Enterprise Mobile Management (EMM) deployments, supported by strong enterprise IT budgets and early adoption of zero-trust security models. Key demand originates from healthcare, BFSI, and government sectors, where more than 70% of organizations enforce encrypted mobile access policies. Data protection mandates and federal cybersecurity modernization programs encourage secure endpoint governance frameworks. Over 66% of enterprises integrate EMM with identity and access management systems to enable conditional access. Cloud-first digital transformation strategies have increased SaaS-based mobility management adoption by 48% since 2022. A major enterprise software provider headquartered in the region expanded AI-powered endpoint analytics capabilities to manage over 100 million devices globally. Enterprise users here prioritize productivity and compliance, with finance and healthcare professionals demonstrating the highest secure mobile app utilization rates.

Europe accounts for roughly 27% of Enterprise Mobile Management (EMM) adoption, with Germany, the UK, and France leading regional deployments. Data protection regulations influence more than 65% of corporate mobility policies, driving demand for encrypted containers and strict device-level monitoring. Sustainability and digital sovereignty initiatives also affect procurement strategies. Nearly 58% of European enterprises have adopted unified endpoint controls to support hybrid workforce models. Emerging technologies such as AI-based policy automation and device risk scoring are gaining traction, improving audit readiness by about 30%. A regional cybersecurity vendor strengthened its mobile threat defense portfolio to support cross-border compliance management. Enterprises demonstrate cautious but structured adoption behavior, with regulatory adherence shaping purchasing decisions more strongly than rapid feature expansion.

Asia-Pacific represents nearly 24% of global EMM demand and ranks highest in growth momentum. China, India, and Japan are the largest consuming countries, together contributing over 70% of regional deployments. Expanding digital infrastructure and 5G coverage—now exceeding 65% population reach in advanced economies—support enterprise mobility initiatives. Technology hubs and innovation corridors promote AI integration into mobile device analytics. A regional technology services provider recently scaled endpoint management support for over 50,000 enterprise clients adopting cloud-based governance tools. Enterprises show strong preference for mobile productivity tools, with e-commerce, fintech, and IT services sectors leading adoption. BYOD prevalence exceeds 60% in several emerging economies, reinforcing the need for secure app containerization and remote compliance controls.

South America contributes close to 7% of the global Enterprise Mobile Management (EMM) landscape, with Brazil and Argentina as principal markets. Infrastructure modernization and expanding digital banking ecosystems increase secure mobility demand. Over 52% of large enterprises in the region have adopted centralized device monitoring tools. Government digital service programs encourage cloud adoption, indirectly boosting enterprise mobility security requirements. Trade digitization initiatives have improved cross-border data exchange controls. A regional IT integrator expanded managed mobility services to support over 3,000 corporate clients across financial and telecom sectors. Consumer behavior emphasizes mobile application usage, particularly in media and fintech industries, driving demand for secure app lifecycle governance.

The Middle East & Africa region holds about 6% share of global Enterprise Mobile Management (EMM) deployments, led by the UAE and South Africa. Demand is strong in oil & gas, construction, and government sectors undergoing digital modernization. Over 49% of enterprises in advanced economies within the region implement remote device provisioning systems. Smart city initiatives and national digitization strategies promote secure mobile infrastructure. Regulatory frameworks increasingly mandate data localization and secure access controls. A regional telecom solutions provider enhanced enterprise mobility security services for energy and logistics clients managing large field workforces. Enterprises emphasize operational continuity, with field mobility and secure remote access as top priorities.

United States Enterprise Mobile Management (EMM) Market – 31% share – Strong enterprise IT infrastructure, high multi-device workforce penetration, and advanced cybersecurity integration drive leadership.

China Enterprise Mobile Management (EMM) Market – 18% share – Large-scale enterprise mobility adoption and rapid digital workplace expansion across technology and manufacturing sectors.

The Enterprise Mobile Management (EMM) market is moderately consolidated, with over 120 active competitors globally, including multinational software providers, cybersecurity firms, and cloud solution vendors. The top five companies—Microsoft, VMware, IBM, Cisco, and BlackBerry—together account for approximately 62% of total market deployments, reflecting significant influence over product innovation and enterprise adoption. Competition is driven by strategic initiatives such as AI-integrated endpoint analytics, cloud-based unified management solutions, and automated compliance reporting tools. Over 48% of leading vendors have entered partnerships with cloud service providers to enhance platform scalability and security features. Recent product launches emphasize zero-trust access, containerized application management, and cross-platform device orchestration. Regional specialization is notable, with North American firms dominating large enterprise solutions while Asia-Pacific players focus on SME mobility and BYOD adoption. Mergers and acquisitions are reshaping competitive dynamics, with at least 15 integration deals completed between 2023 and 2025 to consolidate security offerings and expand AI-driven EMM capabilities. Innovation trends, including predictive device analytics and mobile threat intelligence, are increasingly differentiating market leaders from smaller providers. Overall, the market environment incentivizes rapid technological upgrades, strategic alliances, and regional expansion to maintain competitive positioning.

Cisco

BlackBerry

Ivanti

MobileIron

Citrix Systems

Sophos

SOTI

ManageEngine

Jamf

The Enterprise Mobile Management (EMM) market is heavily shaped by both current and emerging technologies that enhance security, efficiency, and user experience across mobile ecosystems. AI-powered threat analytics has become a critical capability, with over 61% of large enterprises deploying machine learning models to detect anomalous device behavior and prevent mobile phishing, malware, and ransomware attacks. Automated policy enforcement tools reduce administrative workloads by up to 35%, while predictive analytics identify high-risk devices before security incidents occur.

Unified Endpoint Management (UEM) platforms are increasingly replacing standalone Mobile Device Management (MDM) and Mobile Application Management (MAM) tools, enabling centralized control over smartphones, laptops, tablets, and IoT devices. In 2025, more than 57% of enterprises with distributed workforces adopted UEM frameworks to streamline device enrollment, app deployment, and compliance reporting. Integration with identity and access management systems allows conditional access based on device health, user role, and location, improving secure login efficiency by 26%.

Emerging technologies such as zero-trust network access, containerized application management, and AI-based compliance monitoring are further influencing market dynamics. Over 54% of enterprises now deploy containerized workspace environments to segregate corporate and personal data on BYOD devices, reducing the risk of data leakage. Additionally, mobile endpoint orchestration leveraging cloud-based automation has accelerated provisioning and update cycles by 33%, supporting hybrid workforce mobility and reducing IT intervention needs.

Other technological trends shaping the Enterprise Mobile Management (EMM) landscape include 5G-enabled remote device connectivity, blockchain-based identity verification, and advanced analytics for digital employee experience monitoring. Enterprises implementing these solutions report a 28–36% improvement in operational efficiency and policy compliance, underscoring the strategic importance of technology adoption in sustaining secure, productive mobile environments.

• In March 2025, Microsoft launched a major update to Microsoft Intune, extending AI-assisted remediation and unified policy frameworks across Windows, macOS, iOS, and Android devices, improving automated compliance enforcement and cross-platform governance.

• In January 2025, SOTI introduced SOTI VPN within its EMM platform MobiControl using WireGuard technology, providing always‑on encrypted device connectivity for retail environments and strengthening mobile data protection.

• In April 2025, VMware expanded Workspace ONE with enhanced AI‑driven automation and zero‑trust security capabilities designed to improve device onboarding efficiency and adaptive access controls across mobile and multi‑OS endpoints.

• In October 2025, Stratix Corporation acquired Mobility CG to broaden its Enterprise Mobile Management (EMM) and managed mobility services in North America, integrating logistics and device lifecycle expertise to support healthcare, retail, and government sectors.

The scope of the Enterprise Mobile Management (EMM) Market Report encompasses a comprehensive examination of solutions that enable organizations to manage, secure, and optimize mobile devices, applications, and associated data across enterprise environments. It covers core and extended EMM functionalities including Mobile Device Management (MDM), Mobile Application Management (MAM), Mobile Content Management (MCM), and Unified Endpoint Management (UEM), reflecting how enterprises administer heterogeneous fleets of smartphones, tablets, laptops, and IoT endpoints under centralized governance frameworks. The report evaluates technology layers such as AI‑powered threat analytics, zero‑trust access integration, cloud‑native automation, and containerized application enforcement, highlighting measurable impacts like improved compliance readiness and reduced security incidents.

Geographically, the analysis spans major regional markets including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing deployment volumes, regulatory influences, and consumer behavior variations. Applications addressed range from security management and productivity enablement to asset lifecycle administration and compliance monitoring across key industry verticals such as BFSI, healthcare, government, IT services, and retail. The report outlines how digital transformation strategies and mobile workforce policies influence segment adoption, and profiles emerging niches like wearable management and IoT‑enabled mobility controls. It also identifies ecosystem dynamics such as vendor partnerships, platform integrations, and innovation trends that shape competitive positioning, providing decision‑makers with strategic insights into technology adoption patterns and functional priorities within the evolving Enterprise Mobile Management landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

16.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft, VMware, IBM, Cisco, BlackBerry, Ivanti, MobileIron, Citrix Systems, Sophos, SOTI, ManageEngine, Jamf |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |