Reports

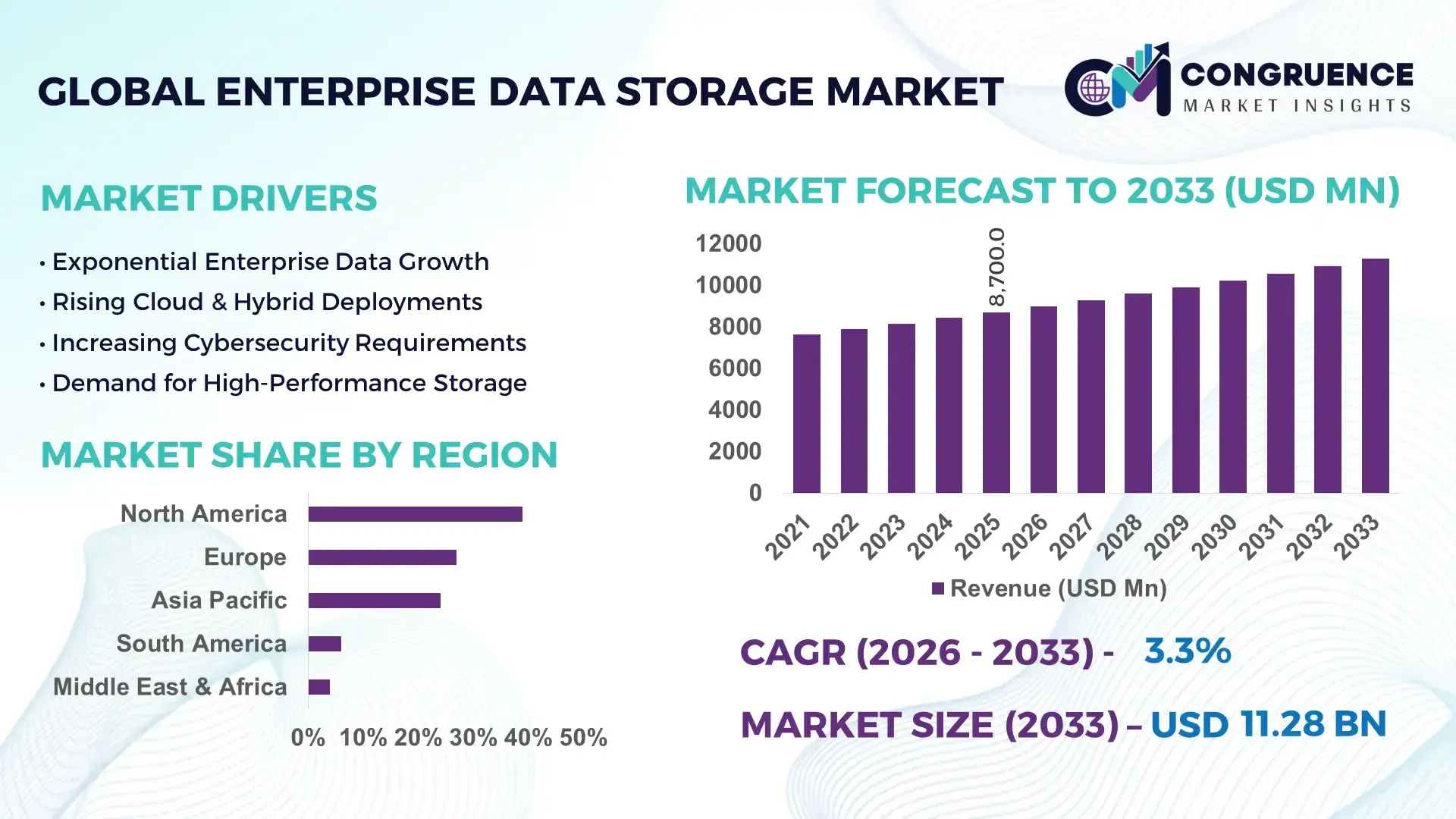

The Global Enterprise Data Storage Market was valued at USD 8,700.0 Million in 2025 and is anticipated to reach a value of USD 11,280.3 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by exponential enterprise data generation, expansion of hybrid cloud infrastructures, and rising compliance-driven archival requirements across industries.

In the United States, which dominates the Enterprise Data Storage Market, installed data center IT load capacity surpassed 20 GW in 2025, supporting large-scale enterprise storage deployments across hyperscale and colocation facilities. Enterprise SSD production and integration remain strong, with over 65% of Fortune 500 firms deploying hybrid storage arrays combining NVMe and object storage platforms. U.S. enterprises account for more than 45% of global hyperscale cloud infrastructure capacity, with capital expenditure in data center and storage infrastructure exceeding USD 150 billion annually. Key industry applications include BFSI transaction archiving (handling over 70 billion digital transactions annually), healthcare imaging repositories storing petabytes of diagnostic data, and AI training clusters requiring high-throughput parallel file systems exceeding 100 GB/s performance benchmarks.

Market Size & Growth: Valued at USD 8,700.0 Million in 2025, projected to reach USD 11,280.3 Million by 2033 at a CAGR of 3.3%, driven by rising enterprise data volumes growing over 23% annually.

Top Growth Drivers: Cloud adoption 68%, enterprise AI workload expansion 41%, regulatory data retention compliance 37%.

Short-Term Forecast: By 2028, intelligent tiering solutions are expected to reduce storage operational costs by 22% while improving retrieval efficiency by 30%.

Emerging Technologies: NVMe-over-Fabrics deployment, AI-powered storage orchestration, and software-defined storage (SDS) platforms.

Regional Leaders: North America projected at USD 4,150 Million by 2033 with hyperscale adoption surge; Asia-Pacific at USD 3,020 Million driven by 52% SME cloud migration; Europe at USD 2,480 Million supported by sovereign data regulations.

Consumer/End-User Trends: BFSI, healthcare, and telecom sectors represent over 58% of enterprise storage demand, with 64% of enterprises adopting hybrid storage architectures.

Pilot or Case Example: In 2024, a U.S.-based financial institution achieved 35% downtime reduction and 28% faster data processing through AI-enabled storage optimization.

Competitive Landscape: Dell Technologies holds approximately 18% share, followed by HPE, NetApp, IBM, and Huawei.

Regulatory & ESG Impact: Over 48% of enterprises comply with GDPR-aligned retention policies; 32% of new facilities integrate energy-efficient cooling systems.

Investment & Funding Patterns: Over USD 25 billion invested globally in enterprise storage infrastructure upgrades between 2023–2025, with growth in green data center financing.

Innovation & Future Outlook: Integration of edge storage nodes and AI-driven predictive maintenance is reshaping resilience and scalability frameworks.

BFSI contributes approximately 28% of enterprise storage utilization, followed by healthcare at 19% and IT & telecom at 17%. NVMe-based arrays now represent over 46% of new enterprise installations. Regulatory mandates such as GDPR and data localization laws are increasing long-term archival demand. Asia-Pacific enterprise storage consumption is rising above 20% annually, driven by digital banking and e-governance. Edge computing integration and AI workload optimization are expected to redefine capacity planning strategies.

The Enterprise Data Storage Market plays a strategic role in digital transformation, cybersecurity resilience, and regulatory compliance frameworks across global enterprises. As corporate data volumes increase by over 23% annually, organizations are shifting from traditional SAN architectures toward hyperconverged and software-defined storage environments to enhance scalability and automation. NVMe-over-Fabrics delivers up to 45% latency improvement compared to legacy SATA-based storage systems, strengthening real-time analytics and AI deployment capabilities.

North America dominates in volume due to large hyperscale deployments, while Asia-Pacific leads in adoption velocity with over 52% of mid-sized enterprises transitioning to hybrid cloud storage models. By 2028, AI-driven storage resource allocation is expected to improve infrastructure utilization rates by 30% and reduce unplanned downtime by 25%. Enterprises are aligning storage modernization strategies with ESG commitments, targeting 35% energy efficiency improvement and 20% carbon footprint reduction in data center operations by 2030.

In 2024, a leading U.S. cloud service provider achieved 40% performance enhancement through AI-integrated workload distribution across distributed storage clusters. Compliance-driven encryption standards and sovereign cloud mandates are reshaping procurement priorities. Over the next decade, the Enterprise Data Storage Market will remain a pillar of operational resilience, regulatory readiness, and sustainable infrastructure growth, underpinning AI expansion and digital-first enterprise ecosystems.

The Enterprise Data Storage Market is influenced by rapid enterprise digitization, regulatory enforcement, and the proliferation of AI-driven applications. Data-intensive sectors such as finance, healthcare, retail, and telecom are expanding high-performance storage requirements to support analytics, cybersecurity logging, and real-time transaction processing. More than 64% of enterprises now deploy hybrid storage strategies integrating on-premise arrays with cloud object storage. Edge computing expansion is further diversifying storage topology, requiring localized data nodes for latency-sensitive workloads. Additionally, rising cybersecurity incidents—exceeding 2,000 reported enterprise-level breaches annually—are reinforcing encrypted storage and immutable backup deployments. Infrastructure modernization, automation, and predictive analytics integration continue to shape procurement decisions, ensuring scalable, secure, and energy-efficient enterprise storage ecosystems.

AI and machine learning workloads require high-throughput, low-latency storage capable of processing terabytes of structured and unstructured data daily. Training large AI models can consume datasets exceeding 500 TB per project, necessitating NVMe-based flash arrays with throughput surpassing 100 GB/s. Approximately 41% of enterprises have integrated AI-driven analytics platforms into core operations, significantly increasing demand for scalable storage clusters. Parallel file systems and object storage solutions are being deployed to handle over 60% growth in unstructured data volumes annually. Furthermore, edge AI deployments in manufacturing and telecom environments require distributed storage nodes, expanding enterprise procurement of resilient and high-performance infrastructure components.

Transitioning from legacy HDD-based arrays to NVMe and software-defined storage platforms requires substantial capital expenditure and skilled workforce training. Enterprise storage hardware refresh cycles typically involve 3–5-year upgrade investments, with integration complexity affecting over 38% of IT departments. Power and cooling requirements for high-density flash arrays can increase operational expenditure by 15–20% without energy optimization. Additionally, integration challenges between multi-vendor systems create interoperability constraints, delaying deployments in nearly 29% of enterprise upgrade projects. These cost and complexity factors slow adoption among small and mid-sized enterprises.

Edge computing deployments are projected to manage over 50% of enterprise-generated data by 2027, creating demand for localized storage nodes with low-latency capabilities. Manufacturing IoT networks generate up to 1 TB of operational data per day per facility, requiring resilient on-site storage solutions. Telecom operators deploying 5G infrastructure are integrating micro data centers to process data within 10 milliseconds latency thresholds. Approximately 48% of enterprises are evaluating distributed storage models to support branch-level analytics and compliance localization requirements. This shift presents significant opportunities for modular, scalable, and software-defined enterprise storage vendors.

Enterprise ransomware attacks increased by over 30% in recent years, targeting centralized storage repositories and backup systems. Over 60% of breached organizations reported compromised backup integrity, prompting mandatory immutable storage adoption. Implementing end-to-end encryption, zero-trust access controls, and air-gapped backups increases infrastructure complexity and deployment time. Data sovereignty regulations across more than 70 countries require localized storage compliance, complicating multinational deployments. Moreover, recovery time objectives below 1 hour demand high-availability architectures, increasing infrastructure redundancy costs and operational oversight burdens for enterprises.

46% Shift Toward All-Flash and NVMe Architectures: Enterprises are accelerating replacement of HDD arrays, with all-flash systems accounting for over 46% of new deployments in 2025. NVMe adoption has improved application latency by up to 45% and increased transactional throughput by 38%, particularly in financial and AI-driven workloads.

64% Hybrid and Multi-Cloud Storage Integration: Approximately 64% of global enterprises now integrate on-premise storage with public and private cloud platforms. Hybrid models have reduced data retrieval times by 27% and improved disaster recovery preparedness by 33%, strengthening operational continuity.

35% Energy Efficiency Gains in Modern Data Centers: Advanced liquid cooling and AI-based workload optimization systems have enabled up to 35% energy savings in enterprise storage facilities. Nearly 32% of new data center builds incorporate renewable energy integration, aligning with corporate ESG targets.

52% Growth in Edge Storage Deployments: Edge-based enterprise storage nodes have grown by 52% in deployment volume, particularly across telecom and manufacturing sectors. Localized storage reduces latency by up to 40% and improves real-time analytics response times by 34%, enhancing distributed enterprise performance.

The Enterprise Data Storage Market is segmented by type, application, and end-user, reflecting the diverse architectural, operational, and compliance-driven requirements of modern enterprises. By type, organizations increasingly differentiate between performance-centric flash arrays, capacity-oriented HDD systems, and flexible software-defined storage frameworks to balance cost, scalability, and latency requirements. Applications range from primary data storage and backup to analytics-driven workloads and disaster recovery infrastructure. End-user segmentation highlights strong demand from BFSI, healthcare, IT & telecom, manufacturing, and government sectors, each requiring tailored storage architectures aligned with security mandates and workload intensity. Over 64% of enterprises currently operate hybrid storage environments combining on-premise arrays with cloud object storage, demonstrating convergence across segments. Additionally, unstructured data now represents more than 60% of enterprise data volumes, influencing procurement toward scalable and object-based storage systems. The segmentation landscape reflects a shift from capacity expansion to intelligent, automated, and energy-optimized storage ecosystems designed for resilience and regulatory compliance.

Enterprise Data Storage Market segmentation by type includes All-Flash Arrays (AFA), Hybrid Flash Arrays, Hard Disk Drive (HDD)-based Systems, and Software-Defined Storage (SDS). All-Flash Arrays currently account for approximately 46% of enterprise deployments due to superior latency performance and throughput advantages exceeding 100 GB/s in AI and transactional workloads. Hybrid Flash Arrays hold nearly 28% adoption, offering cost-performance balance for mid-tier applications. However, Software-Defined Storage is the fastest-growing segment, expanding at an estimated CAGR of 9.1%, driven by virtualization adoption and cloud-native architecture requirements. SDS platforms enable enterprises to decouple hardware from storage management, improving utilization rates by up to 30%. Traditional HDD-based systems continue to serve archival and backup functions, contributing around 18% of deployments, particularly in cost-sensitive environments. Other niche storage models, including object-based and edge-integrated storage nodes, collectively represent about 8% of the market but are expanding in distributed enterprise environments.

• In 2025, a U.S. Department of Energy high-performance computing facility upgraded to NVMe-based all-flash storage, achieving over 2 TB/s aggregate throughput to support large-scale AI simulations, demonstrating enterprise-grade flash scalability.

By application, the Enterprise Data Storage Market includes Primary Storage, Backup & Disaster Recovery, Archival & Compliance Storage, Big Data Analytics, and Cloud Integration.Primary Storage leads with approximately 38% share, as enterprises prioritize real-time data processing for mission-critical applications. Backup & Disaster Recovery accounts for around 24%, reflecting rising ransomware incidents and regulatory mandates for immutable backups. However, Big Data Analytics is the fastest-growing application segment, expanding at an estimated CAGR of 8.4%, supported by AI-driven analytics adoption and real-time data processing needs. Archival & Compliance Storage represents roughly 17%, largely influenced by data retention regulations across over 70 jurisdictions. Cloud Integration applications hold about 13%, as 64% of enterprises operate hybrid environments. Remaining specialized applications contribute a combined 8%, including edge analytics and IoT data storage. In 2025, more than 42% of global enterprises reported piloting AI-optimized storage for analytics-intensive workloads. Additionally, approximately 58% of financial institutions enhanced disaster recovery protocols with automated backup verification systems.

• In 2024, the U.S. National Institutes of Health expanded its biomedical data repository infrastructure, supporting petabyte-scale genomic data storage to accelerate multi-institution research collaboration.

End-user segmentation in the Enterprise Data Storage Market includes BFSI, Healthcare, IT & Telecom, Manufacturing, Government, and Retail & E-commerce. BFSI remains the leading end-user segment, accounting for approximately 28% of total enterprise storage utilization due to high-frequency digital transactions exceeding 70 billion annually and strict compliance mandates. Healthcare follows with nearly 19%, driven by medical imaging storage, electronic health records, and genomic databases. IT & Telecom contributes around 17%, supported by hyperscale cloud and 5G network data processing. However, Manufacturing is the fastest-growing end-user segment, expanding at an estimated CAGR of 7.8%, fueled by Industrial IoT systems generating up to 1 TB of operational data per facility per day. Government and Retail & E-commerce collectively account for roughly 24%, with increasing investments in sovereign data infrastructure and omnichannel data analytics platforms. In 2025, approximately 48% of enterprises in telecom reported deploying edge-based storage nodes to support low-latency services. Additionally, 42% of hospitals in the United States are testing AI-assisted imaging systems requiring high-capacity storage backbones.

• In 2025, a U.S. federal cloud modernization initiative migrated over 500 legacy databases to secure enterprise storage environments, enhancing cybersecurity posture and improving system availability across multiple agencies.

North America accounted for the largest market share at 39% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s dominance is supported by more than 20 GW of installed data center IT capacity and enterprise cloud penetration exceeding 70% among large organizations. Europe holds approximately 27% share, driven by over 30% of enterprises operating under strict data localization and GDPR-aligned storage frameworks. Asia-Pacific represents nearly 24% of global demand, supported by more than 60% SME digitalization rates in advanced economies such as Japan and South Korea. South America contributes about 6%, while the Middle East & Africa accounts for close to 4%, collectively reflecting increasing infrastructure modernization and regulatory compliance requirements. Globally, over 64% of enterprises operate hybrid storage models, and more than 46% of new deployments involve all-flash architectures, reinforcing strong regional investment momentum in high-performance storage systems.

North America holds approximately 39% share of the Enterprise Data Storage Market, supported by hyperscale data center expansion and strong enterprise IT budgets. Key demand originates from BFSI, healthcare, defense, and cloud service providers, with over 70% of Fortune 500 companies deploying hybrid or multi-cloud storage strategies. Regulatory frameworks such as data privacy laws and federal cybersecurity modernization mandates have increased enterprise spending on encrypted and immutable storage systems. Technological adoption is led by NVMe-over-Fabrics, AI-based storage orchestration, and liquid-cooled flash arrays delivering up to 35% energy efficiency gains. A major regional player, Dell Technologies, continues expanding all-flash and hyperconverged infrastructure portfolios, supporting large-scale AI clusters. Enterprise buyers in this region demonstrate higher adoption in healthcare and financial services, where over 60% of organizations prioritize real-time analytics and disaster recovery preparedness.

Europe accounts for nearly 27% of the Enterprise Data Storage Market, with Germany, the UK, and France leading deployments. Over 30% of enterprises in these countries prioritize sovereign data hosting to comply with GDPR and regional data protection frameworks. Sustainability initiatives aligned with the European Green Deal are pushing data centers toward 30% energy efficiency improvements and renewable integration targets exceeding 50% in new builds. Adoption of software-defined storage and object-based architectures is rising, particularly among manufacturing and automotive sectors integrating Industry 4.0 systems. A regional innovator, SAP, supports enterprise clients with integrated data management platforms optimized for hybrid storage environments. Consumer behavior variation reflects regulatory-driven procurement, where more than 55% of enterprises demand explainable data governance and audit-ready storage solutions.

Asia-Pacific represents around 24% of global Enterprise Data Storage Market demand and ranks as the fastest-growing regional contributor. China, India, and Japan are the top-consuming countries, collectively accounting for over 65% of regional enterprise storage installations. Infrastructure expansion includes more than 5 GW of new data center capacity added annually across key economies. Rapid e-commerce growth exceeding 18% annual transaction volume expansion and mobile-first digital ecosystems are generating massive unstructured datasets. Local technology firms such as Huawei are investing heavily in AI-optimized flash storage and distributed cloud storage solutions. Regional enterprises show strong cloud-first adoption behavior, with over 52% of mid-sized businesses transitioning from legacy on-premise systems to hybrid storage platforms to support fintech and mobile AI applications.

South America holds approximately 6% share of the Enterprise Data Storage Market, with Brazil and Argentina as the primary contributors. Digital banking expansion in Brazil has increased enterprise data processing volumes by more than 25% annually. Energy and mining projects across the region require high-capacity storage systems for geological modeling and operational analytics. Government-backed digital transformation initiatives and cross-border data trade policies are encouraging cloud and colocation investments. Regional telecom providers are deploying localized micro data centers to reduce latency by up to 30%. Enterprises in this region exhibit demand patterns tied to media streaming, language localization services, and mobile-driven consumer applications, supporting steady enterprise storage infrastructure upgrades.

The Middle East & Africa accounts for approximately 4% of global Enterprise Data Storage Market demand. The UAE and South Africa are leading adopters, supported by smart city initiatives and oil & gas digitalization programs. Large-scale infrastructure projects require high-performance storage for seismic data analysis and engineering simulations exceeding petabyte-scale capacity. Technological modernization includes adoption of AI-based predictive maintenance storage systems and secure government cloud frameworks. Regional regulations emphasize data sovereignty and cybersecurity resilience. Local telecom operators are expanding hyperscale-ready facilities to support fintech and e-government services. Consumer behavior variations indicate growing enterprise preference for localized storage hosting to ensure compliance and low-latency service delivery.

United States – 34% Market Share: The leadership is driven by over 20 GW installed data center capacity and advanced AI-integrated storage infrastructure adoption.

China – 18% Market Share: It is supported by rapid hyperscale expansion, strong domestic cloud providers, and large-scale industrial digitalization initiatives.

The Enterprise Data Storage Market is moderately consolidated, with the top five vendors collectively accounting for approximately 58% of total global deployments. The competitive landscape includes more than 60 active international and regional providers offering hardware arrays, software-defined storage platforms, and integrated cloud storage solutions. Market leaders compete on performance density, AI-driven storage optimization, cybersecurity integration, and hybrid cloud interoperability.

Strategic initiatives between 2024 and 2025 have included over 25 publicly announced partnerships focused on AI workload acceleration and edge storage integration. Product innovation cycles have accelerated, with leading vendors introducing NVMe-based arrays delivering up to 45% lower latency compared to legacy SATA systems. Mergers and acquisitions remain active, particularly in software-defined and data resilience segments, with at least 12 storage-focused acquisitions recorded globally in the last 24 months.

The market is characterized by high switching costs and long procurement cycles, typically ranging between 6–12 months for large enterprises. Competitive differentiation increasingly centers on energy efficiency, with advanced liquid cooling solutions improving power usage effectiveness by up to 35%. Cloud-native integration capabilities and zero-trust security frameworks are also shaping vendor positioning. Regional players in Asia-Pacific and Europe are expanding through hyperscale collaborations, intensifying competition across performance, compliance, and sustainability benchmarks.

IBM

Huawei Technologies

Hitachi Vantara

Pure Storage

Lenovo

Fujitsu

Western Digital

Seagate Technology

Infinidat

Nutanix

Quantum Corporation

Micron Technology

Technological innovation within the Enterprise Data Storage Market is centered on performance optimization, automation, cybersecurity resilience, and sustainability. NVMe and NVMe-over-Fabrics technologies now account for more than 46% of new enterprise array deployments, delivering up to 45% lower latency and 38% higher throughput compared to SAS/SATA-based systems.

Software-defined storage platforms are increasingly deployed across hybrid cloud infrastructures, with over 64% of enterprises integrating on-premise storage with public cloud object services. AI-powered storage orchestration tools improve workload balancing efficiency by up to 30% and reduce unplanned downtime by nearly 25%.

Immutable storage and ransomware detection systems are gaining prominence, particularly after enterprise cyber incidents increased by more than 30% in recent years. Approximately 60% of large organizations now deploy automated backup verification and encryption frameworks to strengthen data integrity.

Edge storage nodes are expanding rapidly, with deployment growth exceeding 50% in telecom and manufacturing environments. These distributed storage architectures reduce latency by up to 40% and enable real-time analytics at branch or factory locations. Additionally, liquid cooling systems and advanced power management tools deliver energy efficiency improvements of up to 35%, supporting corporate ESG commitments. Emerging trends include computational storage drives, object-based scalability exceeding exabyte thresholds, and integration of storage-class memory for ultra-low-latency enterprise workloads.

• In September 2025, HPE was named a Leader in the 2025 Gartner® Magic Quadrant™ for Enterprise Storage Platforms, marking the 16th consecutive recognition of its enterprise storage solutions’ strategic innovation and execution capabilities, reinforcing its commitment to unified hybrid cloud storage and AI-ready data infrastructure. Source: www.hpe.com

• In April 2025, NetApp won the 2025 Google Cloud Infrastructure Modernization Partner of the Year for Storage, highlighting its role in helping joint customers modernize cloud workloads, enhance agility and scale AI and enterprise data storage deployments through deep integration with Google Cloud services. Source: www.netapp.com

• In October 2025, NetApp introduced enhanced ransomware resilience and data breach detection capabilities embedded into its enterprise storage services, enabling proactive threat identification and isolated recovery environments for mission-critical data infrastructure. Source: www.netapp.com

• In April 2025, Dell Technologies unveiled infrastructure innovations built to power modern AI-ready data centers, including next-generation object storage enhancements (ObjectScale XF960) offering up to 2X greater throughput per node and up to 8X greater density than prior all-flash systems, supporting demanding enterprise AI workloads. Source: www.dell.com

The Enterprise Data Storage Market Report provides comprehensive coverage of storage infrastructure technologies, deployment architectures, and end-user vertical adoption patterns across global regions. The report evaluates core storage types including all-flash arrays, hybrid arrays, HDD-based systems, software-defined storage platforms, and emerging computational storage solutions.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 20 key countries with data center capacity benchmarks exceeding 1 GW in major economies. The report analyzes enterprise adoption rates, where over 64% of organizations operate hybrid storage environments and more than 46% of new deployments utilize NVMe architectures.

Application coverage includes primary storage, backup and disaster recovery, archival compliance systems, analytics-driven workloads, edge computing nodes, and cloud integration models. Industry focus areas encompass BFSI, healthcare, IT & telecom, manufacturing, government, retail, and energy sectors—collectively representing over 80% of enterprise storage demand.

The report further addresses cybersecurity integration trends, energy efficiency advancements achieving up to 35% power optimization, data sovereignty regulations across more than 70 jurisdictions, and emerging distributed storage models supporting low-latency AI processing. Strategic vendor positioning, procurement cycles, innovation pipelines, and infrastructure modernization initiatives are also assessed to support informed investment and operational decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 8,700.0 Million |

| Market Revenue (2033) | USD 11,280.3 Million |

| CAGR (2026–2033) | 3.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Dell Technologies; Hewlett Packard Enterprise (HPE); NetApp; IBM; Huawei Technologies; Hitachi Vantara; Pure Storage; Lenovo; Fujitsu; Western Digital; Seagate Technology; Infinidat; Nutanix; Quantum Corporation; Micron Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |