Reports

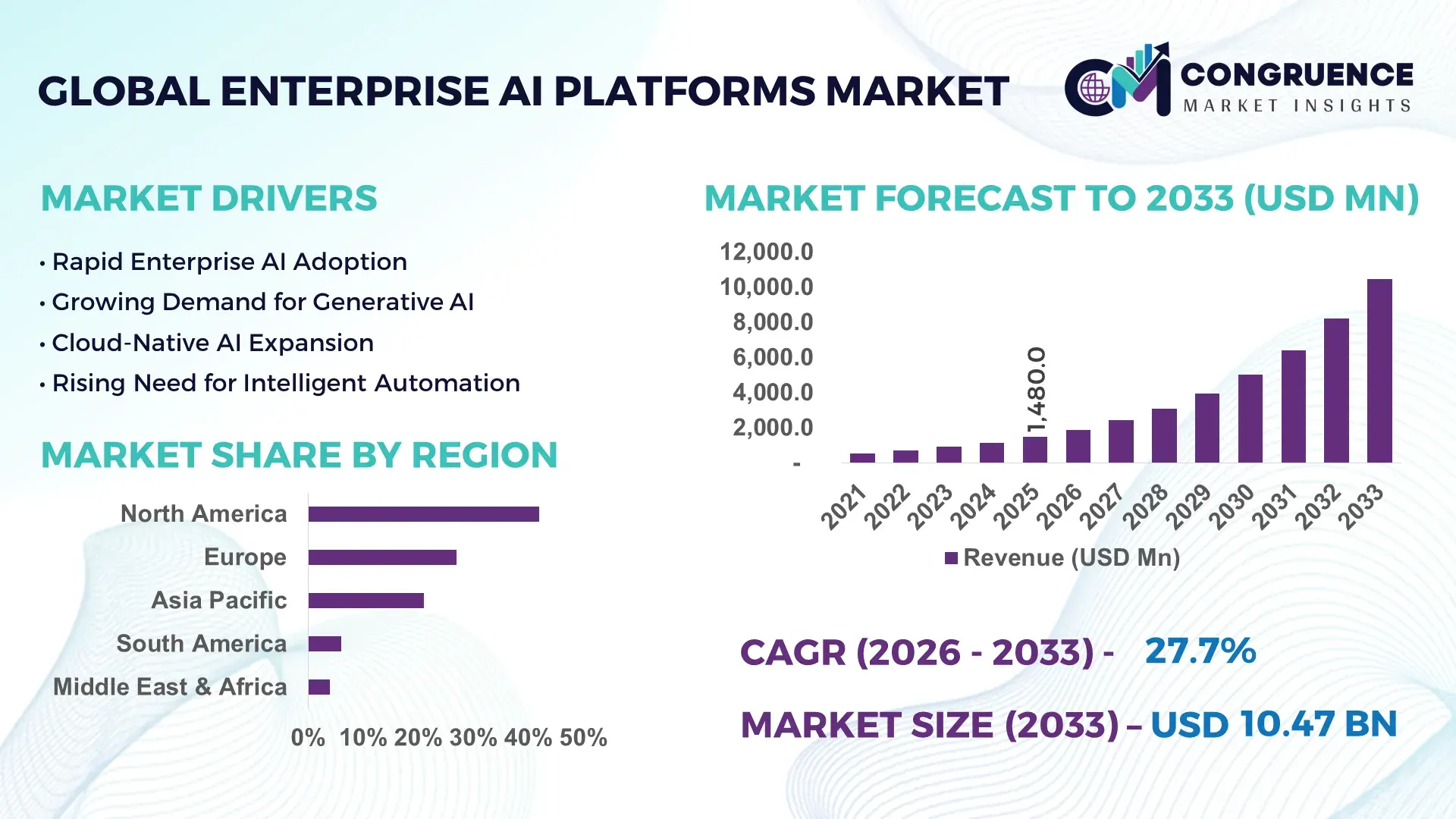

The Global Enterprise AI Platforms Market was valued at USD 1,480.0 Million in 2025 and is anticipated to reach a value of USD 10,466.2 Million by 2033 expanding at a CAGR of 27.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by accelerated enterprise-wide AI adoption for automation, decision intelligence, and scalable deployment of machine learning models across core business functions.

The United States dominates the Enterprise AI Platforms Market with a highly mature ecosystem spanning cloud hyperscalers, enterprise software vendors, and advanced research institutions. In 2025, over 72% of large U.S. enterprises reported active deployment of enterprise AI platforms across at least three business functions, including customer analytics, cybersecurity, and supply chain optimization. The country hosts more than 65% of global AI platform R&D investments, exceeding USD 85 billion annually, with strong concentration in Silicon Valley, Seattle, and Boston. Enterprise AI workloads in the U.S. account for nearly 58% of global AI cloud compute consumption, supported by large-scale data center infrastructure exceeding 11,000 MW capacity. Key industry applications include BFSI risk analytics, healthcare diagnostics, retail personalization, and industrial predictive maintenance, while advancements such as foundation models, MLOps automation, and secure AI governance frameworks are being rapidly commercialized.

Market Size & Growth: Valued at USD 1,480.0 Million in 2025 and projected to reach USD 10,466.2 Million by 2033, expanding at a CAGR of 27.7% due to enterprise-scale AI integration and cloud-native deployments.

Top Growth Drivers: Enterprise AI adoption rate 68%, operational efficiency improvement 32%, data-driven decision accuracy improvement 41%.

Short-Term Forecast: By 2028, enterprise AI platforms are expected to reduce operational costs by 24% through automation and predictive analytics.

Emerging Technologies: Generative AI platforms, automated MLOps pipelines, and multimodal foundation models.

Regional Leaders: North America USD 4,320.0 Million by 2033 with hyperscaler-led adoption; Europe USD 2,980.0 Million driven by regulated AI frameworks; Asia Pacific USD 2,410.0 Million supported by enterprise digitalization.

Consumer/End-User Trends: BFSI, healthcare, and retail enterprises account for over 61% of platform deployments with rising cross-departmental usage.

Pilot or Case Example: In 2024, a U.S.-based retail enterprise improved demand forecast accuracy by 38% using an enterprise AI platform.

Competitive Landscape: Market leader holds ~22% share, followed by IBM, Microsoft, Google, AWS, and SAP.

Regulatory & ESG Impact: AI governance mandates and data privacy regulations influencing secure and explainable AI adoption.

Investment & Funding Patterns: Over USD 120 billion invested globally in enterprise AI platforms and infrastructure since 2022.

Innovation & Future Outlook: Increased integration of AI platforms with ERP, CRM, and industry-specific software ecosystems.

The Enterprise AI Platforms Market serves BFSI with nearly 26% usage, followed by healthcare at 18% and retail at 17%, supported by rapid innovation in generative AI, responsible AI toolkits, and vertical-specific AI models, while regulatory compliance and regional digital transformation initiatives continue to shape consumption and long-term growth.

The Enterprise AI Platforms Market holds strategic relevance as organizations increasingly rely on AI-driven systems to enhance operational resilience, regulatory compliance, and competitive differentiation. Enterprises are shifting from isolated AI models to unified platforms that support data ingestion, model development, deployment, and governance at scale. Generative AI platforms deliver up to 45% improvement in content creation productivity compared to traditional rule-based automation systems, while automated MLOps frameworks reduce model deployment cycles by nearly 60%.

North America dominates in deployment volume due to extensive cloud infrastructure, while Europe leads in responsible AI adoption, with over 64% of enterprises implementing AI governance and explainability tools. By 2028, automated AI lifecycle management is expected to cut model maintenance costs by 30% and improve system uptime by 22%. Enterprises are also aligning AI strategies with ESG commitments, targeting up to 35% reduction in energy consumption per AI workload by 2030 through optimized compute utilization and green data centers.

In 2024, a U.S.-based financial services firm achieved a 41% reduction in fraud detection latency by deploying a unified enterprise AI platform integrating real-time analytics and machine learning pipelines. Looking ahead, the Enterprise AI Platforms Market is positioned as a core pillar enabling scalable innovation, compliance-ready AI deployment, and sustainable enterprise transformation across global industries.

The Enterprise AI Platforms Market dynamics are shaped by rapid enterprise digital transformation, rising data volumes, and the need for scalable AI governance. Organizations are consolidating disparate AI tools into centralized platforms to improve interoperability, security, and operational efficiency. Cloud-native architectures, hybrid deployments, and industry-specific AI platforms are gaining traction as enterprises seek flexibility and compliance alignment. Workforce upskilling, integration with legacy systems, and regional regulatory frameworks continue to influence adoption patterns, while advances in generative AI and automation are expanding platform capabilities across sectors.

Enterprises are accelerating automation initiatives to address labor shortages and operational complexity. Over 70% of large organizations now prioritize AI-driven automation for repetitive and data-intensive tasks, improving process efficiency by up to 34%. Enterprise AI platforms enable centralized orchestration of automation workflows, predictive analytics, and intelligent decision systems, supporting scalable deployment across departments. Increased reliance on real-time insights in finance, logistics, and customer engagement further amplifies demand for robust AI platforms.

Data privacy concerns and integration challenges remain significant restraints. Nearly 48% of enterprises cite difficulties in integrating AI platforms with legacy IT systems and siloed data architectures. Compliance with regional data protection regulations increases implementation complexity, while inconsistent data quality limits AI model performance. These factors slow adoption timelines and require additional investment in data governance and security frameworks.

Vertical-specific AI platforms offer strong growth opportunities by addressing industry-specific requirements. In healthcare, AI platforms supporting diagnostics and patient analytics have improved clinical decision accuracy by 29%. Manufacturing enterprises report 31% reduction in downtime using AI-driven predictive maintenance platforms. Tailored solutions enable faster adoption, improved ROI, and stronger alignment with regulatory and operational needs.

A shortage of skilled AI professionals continues to challenge enterprises, with over 40% reporting insufficient in-house expertise to manage AI platforms effectively. Additionally, implementing robust AI governance frameworks requires cross-functional coordination, increasing deployment complexity. Balancing innovation with ethical AI use and transparency adds further operational challenges for large organizations.

Expansion of Generative AI Integration: Over 62% of enterprise AI platforms now incorporate generative AI capabilities, improving knowledge worker productivity by 44% and reducing content development time by 37%.

Growth of Automated MLOps Platforms: Automated MLOps adoption has increased by 58%, cutting model deployment cycles by 55% and reducing operational errors by 28% across large enterprises.

Rise of Hybrid and Edge AI Deployments: Nearly 46% of enterprises deploy AI platforms in hybrid or edge environments, lowering latency by 33% and improving real-time decision-making efficiency.

Strengthening of Responsible AI Frameworks: Around 61% of enterprises have embedded AI governance and explainability tools into platforms, improving regulatory compliance readiness by 42% and stakeholder trust metrics by 35%.

The Enterprise AI Platforms Market is segmented across type, application, and end-user, reflecting how organizations deploy AI capabilities across technology stacks and business functions. By type, platforms are differentiated based on core AI modality, data processing architecture, and deployment models such as cloud-native, hybrid, and on-premise systems. Application-based segmentation captures how AI platforms are utilized in analytics, automation, decision intelligence, customer engagement, cybersecurity, and predictive operations. End-user segmentation highlights adoption patterns across BFSI, healthcare, retail, manufacturing, IT & telecom, government, and SMEs, each exhibiting distinct maturity levels in AI integration. Large enterprises prioritize scalable governance and MLOps, while mid-sized firms focus on plug-and-play AI tools. Industry adoption is increasingly influenced by regulatory compliance needs, data availability, and digital transformation roadmaps, leading to varied implementation intensity across regions and sectors.

Enterprise AI platforms are broadly categorized into vision-language models, audio-text systems, video-language models, and other specialized AI architectures such as tabular AI, graph AI, and agentic AI systems. Vision-language models currently lead the market with 42% share, driven by strong enterprise demand for document intelligence, image-based inspection, and multimodal search in banking, logistics, and healthcare. Their ability to process unstructured data at scale has made them the default choice for automation-heavy workflows. Audio-text systems hold 25% share, primarily used in call center analytics, transcription, and compliance monitoring in regulated industries such as BFSI and legal services. Adoption is steady but more task-specific compared to vision-based systems. Video-language models are the fastest-growing segment at ~31% CAGR, fueled by rising demand for automated video analytics, surveillance intelligence, smart manufacturing monitoring, and media content tagging. Enterprises are increasingly using these models for safety compliance, predictive maintenance, and real-time anomaly detection in industrial environments. Other AI platform types—including tabular AI, knowledge graphs, and agent-based AI—collectively account for 33% share, serving niche but high-value use cases such as financial risk modeling, supply chain optimization, and autonomous workflow orchestration.

• In 2025, a major global streaming platform deployed advanced video-language models to auto-generate scene summaries and accessibility captions for millions of hours of content, significantly improving usability for visually impaired users.

Enterprise AI platforms are applied across business analytics, customer experience (CX), cybersecurity, operations & supply chain, healthcare diagnostics, and intelligent automation. Business analytics and decision intelligence lead with 38% share, as enterprises rely on AI platforms to integrate real-time data, predictive modeling, and scenario planning for strategic decision-making. Customer experience (CX) automation is the fastest-growing application at ~29% CAGR, driven by AI chatbots, sentiment analysis, and personalized recommendation engines that reduce service costs and enhance engagement. Cybersecurity applications account for roughly 16% share, leveraging AI for threat detection, anomaly monitoring, and fraud prevention. Healthcare diagnostics and clinical analytics contribute 14% share, with growing integration of AI models into hospital information systems. Operations and supply chain applications make up the remaining 32%, supporting demand forecasting, inventory optimization, and predictive maintenance. In 2025, over 38% of enterprises globally reported piloting enterprise AI platforms for customer experience automation. In the U.S., 42% of hospitals are testing AI models that integrate radiology imaging with electronic health records for faster diagnosis.

• In 2025, AI-powered diagnostic systems were deployed across a large network of hospitals to assist in early detection of cardiovascular diseases, improving screening accuracy for millions of patients.

Large enterprises are the leading adopters of Enterprise AI Platforms with 45% share, as they possess the infrastructure, data maturity, and investment capacity to scale AI across departments such as finance, operations, and compliance. SMEs represent the fastest-growing end-user segment at ~28% CAGR, driven by the rise of low-code/no-code AI platforms, cloud-based pricing models, and managed AI services that lower adoption barriers. Among industry users, BFSI holds ~22% share, leveraging AI for fraud detection, credit risk modeling, and automated compliance. Healthcare accounts for 18%, focusing on diagnostics, patient analytics, and clinical decision support. Retail contributes 17%, using AI for personalization, demand forecasting, and supply chain optimization. Manufacturing, IT & telecom, and government collectively make up the remaining 43%, with strong use cases in predictive maintenance, network optimization, and smart governance. Over 60% of Gen Z consumers show higher trust in brands using AI-powered multimodal chatbots for customer support. More than 35% of manufacturing firms now deploy AI platforms for predictive maintenance and quality control.

• In 2025, a global retail group expanded AI-driven inventory and demand planning across 500+ stores, significantly reducing stockouts and improving supply chain efficiency.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 29% between 2026 and 2033.

North America’s leadership is supported by more than 11,000 MW of hyperscale data center capacity, over 65% of global enterprise AI R&D investment concentration, and high adoption across BFSI, healthcare, and retail. Europe follows with roughly 27% share in 2025, driven by strong regulatory frameworks, AI governance requirements, and rapid digital transformation in Germany, the UK, and France. Asia-Pacific holds around 21% share but leads in volume expansion due to cloud infrastructure rollouts, manufacturing digitization, and large-scale AI adoption in China, India, Japan, and South Korea. South America contributes about 6% share, with rising enterprise automation in Brazil and Argentina, while the Middle East & Africa collectively represent nearly 4%, fueled by smart city initiatives, oil & gas analytics, and digital government programs in the UAE and Saudi Arabia.

North America commands approximately 42% of the global Enterprise AI Platforms Market, underpinned by deep cloud penetration, advanced data infrastructure, and strong enterprise AI maturity. BFSI and healthcare remain the most active adopters, with more than 70% of large banks using AI platforms for fraud detection, risk analytics, and compliance automation, while around 42% of U.S. hospitals are piloting AI models that integrate imaging with patient records. Government support has strengthened through national AI strategies, federal funding for AI research, and stricter data governance standards that push enterprises toward compliant, explainable AI platforms. Technological momentum is driven by large-scale deployment of generative AI, automated MLOps, and secure enterprise AI sandboxes within regulated industries. Local platform providers are expanding industry-specific AI modules—for example, U.S.-based vendors are building sector-tailored tools for supply chain forecasting and clinical decision support. Consumer behavior reflects higher trust in AI-enabled services, particularly in healthcare and finance, where automated decision systems are increasingly accepted when paired with transparency and auditability.

Europe holds roughly 27% of the market, with Germany, the UK, and France acting as core innovation hubs for industrial and enterprise AI. German manufacturers are embedding AI platforms into Industry 4.0 factories for predictive maintenance and quality inspection, while the UK leads in AI for financial services and public sector automation. The European Union’s AI Act and GDPR compliance requirements are shaping demand for explainable, auditable, and secure AI platforms, pushing enterprises toward governance-first solutions. Sustainability initiatives such as green data centers and energy-efficient AI computing are influencing procurement decisions, with many firms targeting significant reductions in data center carbon intensity. Adoption of edge AI, digital twins, and multilingual AI systems is accelerating across automotive, logistics, and public services. A notable regional trend is the rise of European AI platform firms offering privacy-by-design architectures tailored to local regulations. Consumer and enterprise behavior shows a preference for transparent AI systems, where regulatory pressure directly increases demand for explainable enterprise AI platforms across highly regulated sectors.

Asia-Pacific ranks as the fastest-expanding region by volume, led by China, India, and Japan as top consumers of enterprise AI platforms. China’s large-scale cloud infrastructure, smart manufacturing initiatives, and government-backed AI programs are accelerating adoption in industrial automation and logistics analytics. India is witnessing rapid enterprise uptake driven by IT services, fintech innovation, and growing digital public infrastructure, while Japan focuses on robotics, predictive maintenance, and AI-driven quality control in manufacturing. Regional tech hubs such as Shenzhen, Bengaluru, and Tokyo are fostering innovation through startup ecosystems and corporate R&D investments. Expanding 5G networks and edge computing deployments are enabling real-time AI use cases in retail, transportation, and smart cities. Local platform providers are developing bilingual and multilingual AI systems tailored for regional enterprise needs. Consumer behavior is heavily influenced by e-commerce and mobile-first AI applications, leading enterprises to prioritize AI-driven personalization, chatbot automation, and supply chain optimization across digital commerce platforms.

South America accounts for about 6% of the global market, with Brazil and Argentina as the primary adopters. Brazil leads regional demand due to its expanding digital economy, strong fintech ecosystem, and growing use of AI in banking, retail, and agritech. Argentina is emerging as a software and AI services hub, contributing to enterprise automation and analytics adoption. Energy and infrastructure sectors are increasingly deploying AI platforms for predictive maintenance, grid optimization, and asset monitoring. Governments are introducing digital transformation policies and tax incentives to encourage AI adoption among SMEs and public institutions. Cloud data center investments are improving connectivity and lowering deployment barriers for enterprises. Local technology firms are building AI-driven language processing solutions tailored to Portuguese and Spanish markets. Consumer and enterprise behavior is closely tied to media, content localization, and multilingual AI applications, driving demand for enterprise AI platforms capable of handling regional language diversity at scale.

The Middle East & Africa region holds around 4% of the market, with strongest demand coming from UAE, Saudi Arabia, and South Africa. Oil & gas companies are deploying AI platforms for predictive maintenance, reservoir analytics, and operational safety monitoring. The construction and smart city sectors are adopting AI-driven project management, traffic optimization, and infrastructure monitoring systems. Governments in the UAE and Saudi Arabia are investing heavily in AI-driven public services, cloud infrastructure, and digital governance initiatives. Regional data localization laws and strategic trade partnerships are shaping enterprise AI deployment strategies. South Africa is emerging as a regional hub for AI research and enterprise analytics, particularly in telecommunications and financial services. Local technology firms are developing Arabic-language AI solutions for government and enterprise applications. Consumer behavior reflects growing trust in AI-enabled digital services, particularly in smart city utilities, banking, and public administration.

United States – 38% Market Share: High enterprise AI maturity, massive cloud infrastructure, and strong demand from BFSI and healthcare.

China – 17% Market Share: Large-scale manufacturing digitization, state-backed AI programs, and rapid industrial automation.

The competitive environment in the Enterprise AI Platforms Market is dynamic and increasingly strategic, with over 100 active competitors globally ranging from hyperscale cloud providers to specialized AI platform developers and systems integrators. While the market exhibits signs of both consolidation and fragmentation, the combined share of the top 5 companies—Microsoft, IBM, Google Cloud, AWS, and Salesforce—is approximately 58%, indicating that leading incumbents retain significant influence. These key players have differentiated positions: Microsoft’s integrated ecosystem and governance tools are widely adopted across regulated sectors, IBM’s watsonx portfolio emphasizes secure, scalable enterprise workflows, and Google’s Gemini-based enterprise offerings accelerate data-driven automation at scale. AWS anchors its position through breadth of services and deep infrastructure investments exceeding $100 billion in cloud and AI data center capacity, enabling robust support for enterprise workloads. Salesforce’s AI agent hub is driving adoption among CRM-centric enterprises.

Competition is shaped by strategic partnerships and co-innovation agreements—for example, recent collaborations between Snowflake and OpenAI, and Databricks and OpenAI, reflect ecosystem expansion beyond traditional vendor boundaries. Innovation trends include agent-orchestration frameworks, secure multi-tenant generative AI services, and hybrid AI deployments, as well as vertical-tailored AI modules for industries like finance, healthcare, and supply chain. The battle for enterprise mindshare also involves open-standard protocols and platforms emphasizing interoperability, explainability, and governance, which are increasingly required by enterprise buyers.

IBM

Google Cloud

Amazon Web Services

Salesforce

Databricks

Oracle

SAP

DataRobot

Infosys Nia

Tata Consultancy Services (TCS)

Cohere

LightOn

UiPath

Enterprise AI Platforms are being shaped by a blend of current and emerging technologies that enhance performance, scalability, and usability for business professionals. A dominant trend is the shift from monolithic, single-purpose AI systems to multi-agent, orchestrated workflows that enable autonomous agents to collaborate in solving complex enterprise tasks such as automated ERP processes, fraud detection, and customer support optimization. Advances in large language models (LLMs)—including enterprise-tuned architectures—are now embedded into core platforms, enabling natural language querying, summarization, decision support, and contextual analytics without requiring extensive coding expertise.

Hybrid AI architectures combining cloud and edge AI are expanding, enabling real-time processing close to data sources in sectors such as manufacturing, logistics, and telecom, reducing latency by up to 30–40% compared to centralized deployments. The emergence of foundation model orchestration frameworks is also significant, allowing organizations to manage and govern multiple models simultaneously, improving operational insights and reducing risk exposure. Security-centric innovations such as fully homomorphic encryption (FHE) and privacy-preserving data analytics are gaining traction to meet enterprise compliance requirements while enabling sensitive data processing.

Another important technological shift is the adoption of standardization protocols that unify workflows across different AI systems, promoting interoperability and seamless integration with existing enterprise software stacks. Specialized accelerators and custom silicon are also being integrated into enterprise AI service offerings to support high-performance training and inference at scale. Decision-makers are increasingly prioritizing modular, explainable AI components that support governance, ethical considerations, and auditability, reflecting enterprise risk management and regulatory compliance imperatives.

• In September 2025, Databricks announced a strategic partnership with OpenAI to integrate GPT-5 and other advanced models into its platform, enabling over 20,000 enterprise customers to build tailored AI applications and accelerating Databricks’ competitive stance. Source: www.reuters.com

• In October 2025, Salesforce expanded partnerships with OpenAI and Anthropic to enhance its Agentforce 360 platform, embedding advanced AI models across CRM, analytics, and automated workflows for enterprise users. Source: www.reuters.com

• In 2025, Infosys announced a collaboration with AWS to fast-track generative AI adoption, integrating industry-specific solutions with AWS developer tools to support AI transformation across manufacturing, telecom, and financial services. Source: www.timesofindia.indiatimes.com

• In February 2026, Snowflake entered a $200 million AI partnership with OpenAI to embed advanced models into its AI Data Cloud platform, enabling natural language data interactions for over 12,600 enterprise customers globally. Source: www.reuters.com

The Enterprise AI Platforms Market Report encompasses a comprehensive examination of technology categories, enterprise applications, regional dynamics, and adoption behaviors within the global AI ecosystem. It covers key segments including platform types—such as LLM-based platforms, multi-agent orchestration systems, cloud-native AI frameworks, hybrid deployments, and edge-integrated solutions—providing insights into how these technologies support analytics, automation, compliance, and decision support across business functions. On the application front, the report analyzes use cases in customer experience, cybersecurity, business intelligence, operations, supply chain optimization, healthcare diagnostics, and financial risk management, highlighting data on normalized adoption rates, deployment patterns, and sector-specific performance benchmarks.

Geographical segmentation includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing unique infrastructure capabilities, regulatory environments, and enterprise behaviors that influence platform uptake. Technology focus areas span foundational models, explainable AI frameworks, privacy-preserving analytics, MLOps tooling, and integration mechanisms with existing enterprise software stacks. The report also captures end-user insights for large enterprises, SMEs, and sector verticals, outlining the distinctive needs and adoption preferences within BFSI, retail, healthcare, manufacturing, and government segments. Strategic considerations such as innovation clusters, partner ecosystems, and compliance frameworks are evaluated to aid decision-makers in planning investments, assessing competitive landscapes, and prioritizing technology roadmaps. The scope further extends to emerging sub-segments like domain-specific AI stacks, AI governance solutions, and specialized vertical platforms, offering a holistic view of enterprise AI platform evolution and practical implications for business transformation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,480.0 Million |

| Market Revenue (2033) | USD 10,466.2 Million |

| CAGR (2026–2033) | 27.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft Azure AI Platform, Amazon Bedrock, CoreWeave, IBM, Google Cloud, Amazon Web Services, Salesforce, Databricks, Oracle, SAP, DataRobot, Infosys Nia, Tata Consultancy Services (TCS), Cohere, LightOn, UiPath |

| Customization & Pricing | Available on Request (10% Customization Free) |