Reports

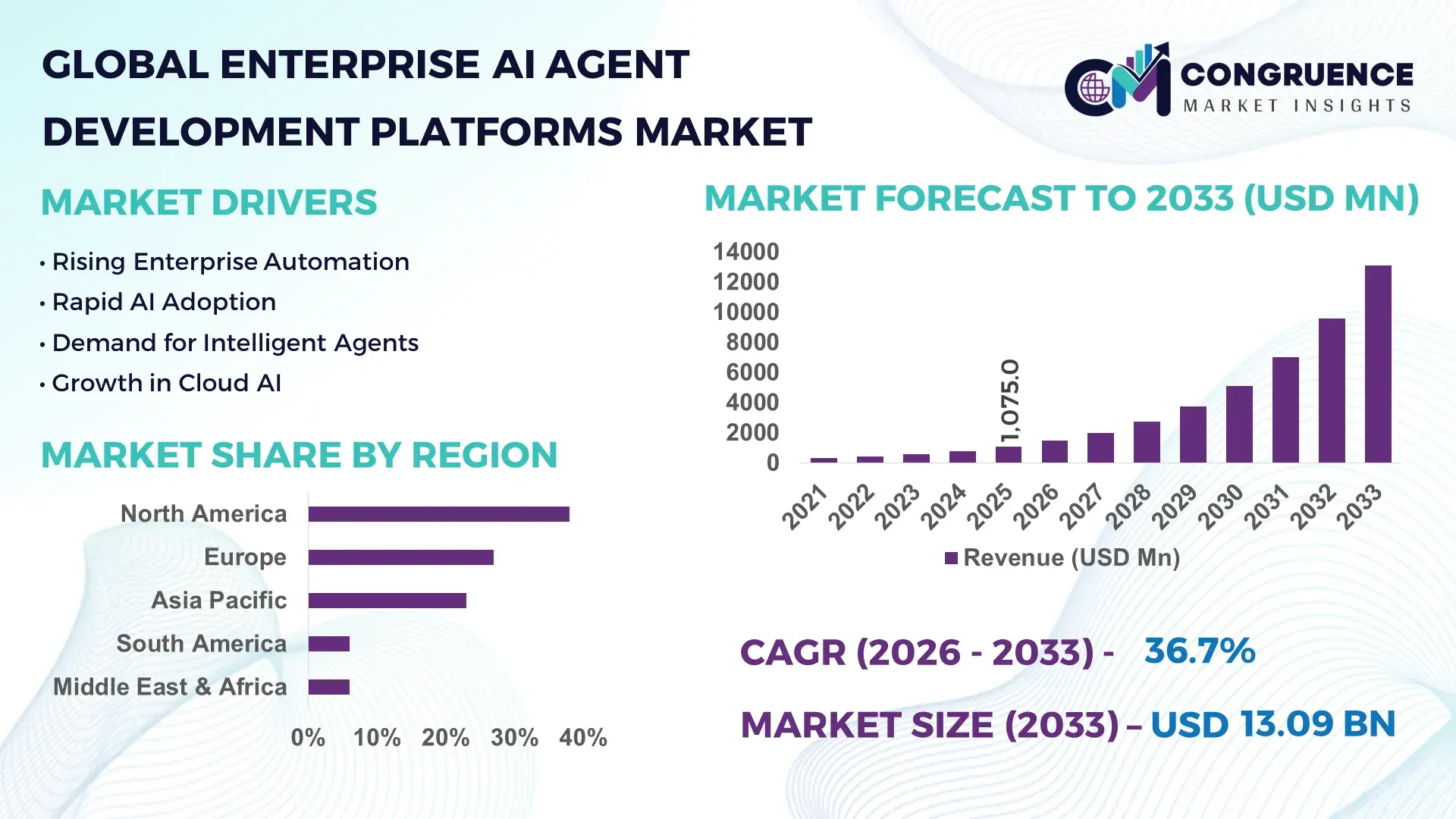

The Global Enterprise AI Agent Development Platforms Market was valued at USD 1,075.0 Million in 2025 and is anticipated to reach a value of USD 13,085.6 Million by 2033 expanding at a CAGR of 36.67% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rapid enterprise adoption of autonomous AI agents for workflow automation, decision intelligence, and productivity optimization across industries.

The United States remains the dominant country in the Enterprise AI Agent Development Platforms Market, supported by strong enterprise AI spending exceeding USD 120 billion annually and over 65% of Fortune 500 companies actively deploying AI-driven automation systems. More than 58% of large enterprises in the U.S. have adopted AI agent frameworks for customer service, IT operations, and cybersecurity applications. The country hosts over 40% of global AI startups, with significant investments in agentic AI platforms, including multi-agent orchestration systems and autonomous decision engines. Additionally, U.S.-based cloud infrastructure supports over 70% of enterprise AI workloads globally, enabling scalable deployment of AI agents across sectors such as finance, healthcare, and retail. Advanced R&D initiatives and enterprise-grade AI model deployment capabilities further strengthen the country’s position in production capacity and technological innovation.

Market Size & Growth: USD 1,075.0 Million (2025) to USD 13,085.6 Million (2033) at 36.67% CAGR, driven by enterprise demand for intelligent automation and autonomous decision systems.

Top Growth Drivers: 68% enterprise AI adoption rate, 45% workflow efficiency improvement, 52% reduction in manual task dependency.

Short-Term Forecast: By 2028, enterprises are expected to achieve up to 40% operational cost reduction through AI agent deployment.

Emerging Technologies: Multi-agent systems, large language model (LLM) orchestration, autonomous workflow engines.

Regional Leaders: North America (~USD 5.2 Billion by 2033, strong enterprise AI integration), Europe (~USD 3.4 Billion, regulatory-driven adoption), Asia-Pacific (~USD 2.9 Billion, rapid digital transformation).

Consumer/End-User Trends: Over 60% of enterprises are prioritizing AI agents for customer support, IT automation, and analytics-driven decision-making.

Pilot or Case Example: In 2025, a global bank deployed AI agents reducing customer query resolution time by 35% and improving service efficiency by 28%.

Competitive Landscape: Market leader holds ~22% share; key players include Microsoft, Google, IBM, Amazon Web Services, and Salesforce.

Regulatory & ESG Impact: AI governance frameworks and data compliance regulations are influencing over 48% of enterprise AI deployment strategies.

Investment & Funding Patterns: Over USD 18 billion invested in AI agent startups and enterprise AI platforms between 2023–2025.

Innovation & Future Outlook: Integration of autonomous agents with enterprise SaaS ecosystems and real-time analytics platforms is accelerating digital transformation initiatives.

Enterprise AI Agent Development Platforms are increasingly utilized across BFSI (28%), IT & telecom (24%), and healthcare (18%), supported by innovations in autonomous orchestration, low-code AI development tools, and real-time decision engines. Regulatory frameworks around AI transparency and data privacy are shaping deployment strategies, while North America leads in consumption and Asia-Pacific demonstrates the fastest adoption momentum. Future growth is influenced by scalable multi-agent architectures and enterprise-grade AI governance models.

The Enterprise AI Agent Development Platforms Market is emerging as a strategic enabler of enterprise-wide automation, intelligent decision-making, and scalable digital transformation. Organizations are increasingly integrating AI agents into mission-critical operations, where autonomous systems can execute tasks, analyze complex datasets, and optimize workflows without continuous human intervention. Compared to traditional rule-based automation systems, AI agent platforms powered by large language models deliver up to 55% improvement in decision accuracy and 45% faster execution times, significantly enhancing enterprise productivity.

From a regional perspective, North America dominates in volume due to high enterprise AI spending and infrastructure maturity, while Asia-Pacific leads in adoption with over 62% of enterprises actively piloting or deploying AI agent-based systems across sectors such as manufacturing, e-commerce, and fintech. This divergence reflects a shift toward scalable AI deployment in emerging markets alongside established innovation hubs.

In the short term, by 2028, autonomous AI agents are expected to improve enterprise process efficiency by over 42%, particularly in IT operations, customer engagement, and supply chain optimization. Organizations are also aligning AI deployment with ESG objectives, committing to measurable improvements such as 30% reduction in energy-intensive manual processes and increased use of energy-efficient cloud infrastructure by 2030.

A micro-scenario illustrates this trajectory: in 2025, a U.S.-based technology firm implemented multi-agent orchestration systems, achieving a 38% reduction in operational downtime and a 33% improvement in incident response time. Such outcomes demonstrate the tangible value of AI agent platforms in real-world enterprise settings.

Looking ahead, the Enterprise AI Agent Development Platforms Market is positioned as a critical pillar of operational resilience, regulatory compliance, and sustainable growth. Its evolution will be driven by advancements in autonomous intelligence, enterprise integration capabilities, and responsible AI governance frameworks.

The Enterprise AI Agent Development Platforms Market is shaped by rapid technological innovation, increasing enterprise demand for intelligent automation, and the growing complexity of digital ecosystems. Organizations are shifting from traditional automation tools to AI-driven agent platforms capable of autonomous decision-making, contextual reasoning, and multi-system integration. Approximately 65% of enterprises are now investing in AI-driven workflow automation, reflecting a strong transition toward intelligent enterprise operations. The integration of large language models and real-time analytics has significantly enhanced the capability of AI agents to manage complex tasks across industries such as BFSI, healthcare, and retail. Additionally, the expansion of cloud infrastructure and API-driven ecosystems is enabling scalable deployment of AI agents across distributed environments. However, concerns related to data security, governance, and interoperability continue to influence adoption strategies. Market dynamics are further shaped by regulatory developments, enterprise digital transformation initiatives, and increasing investments in AI innovation.

The increasing need for intelligent automation across enterprises is a primary driver of the Enterprise AI Agent Development Platforms Market. Over 70% of organizations report significant productivity gains through automation technologies, with AI agents enabling end-to-end process execution without human intervention. Enterprises are leveraging AI agents to automate customer support, IT operations, financial analysis, and supply chain management, leading to efficiency improvements of up to 45%. Additionally, more than 60% of enterprises are prioritizing AI adoption as part of their digital transformation strategies. AI agents reduce manual workload, enhance decision-making accuracy, and enable real-time response capabilities. The integration of natural language processing and machine learning models further enhances the adaptability of AI agents across dynamic business environments. As enterprises continue to focus on cost optimization and operational efficiency, demand for scalable and intelligent AI agent platforms is expected to increase significantly.

Data privacy and security concerns remain a critical restraint in the Enterprise AI Agent Development Platforms Market. Approximately 48% of enterprises cite data security risks as a major barrier to adopting AI-driven systems. AI agents require access to large volumes of enterprise data, including sensitive customer and operational information, increasing the risk of data breaches and unauthorized access. Regulatory frameworks such as GDPR and other data protection laws impose strict compliance requirements, limiting the deployment of AI agents in certain sectors. Additionally, concerns about AI model transparency and explainability impact enterprise trust in autonomous systems. Over 40% of organizations report challenges in ensuring secure integration of AI agents with existing IT infrastructure. These factors create hesitation among enterprises, particularly in highly regulated industries such as finance and healthcare, thereby restraining market growth.

The ongoing wave of enterprise digital transformation presents significant opportunities for the Enterprise AI Agent Development Platforms Market. Over 65% of global enterprises are investing in digital transformation initiatives, creating demand for advanced AI-driven solutions. AI agent platforms enable organizations to modernize legacy systems, enhance operational efficiency, and improve customer experience. The adoption of cloud computing and API-based architectures facilitates seamless integration of AI agents into enterprise workflows. Additionally, the rise of low-code and no-code AI development platforms is democratizing access to AI technologies, allowing non-technical users to deploy AI agents. Emerging applications in predictive analytics, autonomous decision-making, and real-time monitoring further expand market opportunities. As enterprises continue to prioritize innovation and agility, AI agent platforms are expected to play a crucial role in driving digital transformation initiatives.

Integration complexity and high implementation costs pose significant challenges to the Enterprise AI Agent Development Platforms Market. Approximately 42% of enterprises report difficulties in integrating AI agents with existing legacy systems and IT infrastructure. The deployment of AI agent platforms requires significant investment in technology, infrastructure, and skilled workforce, creating barriers for small and medium-sized enterprises. Additionally, the complexity of configuring multi-agent systems and ensuring interoperability across diverse platforms adds to implementation challenges. Enterprises also face challenges in maintaining and updating AI models, requiring continuous monitoring and optimization. The lack of standardized frameworks and interoperability protocols further complicates integration efforts. These challenges can delay deployment timelines and increase operational costs, impacting overall market adoption.

Rapid Enterprise Adoption of Multi-Agent Systems: Over 62% of large enterprises have shifted from single-agent models to multi-agent orchestration frameworks, enabling parallel task execution and improving operational efficiency by up to 48%. Multi-agent systems are increasingly deployed in IT service management and financial analytics.

Expansion of Low-Code AI Development Platforms: Nearly 54% of enterprises are adopting low-code or no-code AI agent platforms, reducing development time by 40% and enabling broader participation from non-technical teams in AI deployment processes.

Integration with Large Language Models (LLMs): Around 67% of AI agent platforms now incorporate LLM-based reasoning capabilities, improving contextual understanding and decision accuracy by over 50% in enterprise applications such as customer support and knowledge management.

Growing Use in Real-Time Decision Intelligence: Approximately 58% of enterprises are deploying AI agents for real-time analytics and decision-making, resulting in a 35% reduction in response time and a 30% improvement in operational agility across industries.

The Enterprise AI Agent Development Platforms Market is segmented based on type, application, and end-user, reflecting the diverse deployment models and industry-specific use cases of AI agent technologies. Platform types range from low-code development environments to advanced multi-agent orchestration systems, catering to varying enterprise needs. Applications span across customer service automation, IT operations, data analytics, and process optimization, with increasing adoption in real-time decision-making scenarios. End-users include BFSI, healthcare, IT & telecom, retail, and manufacturing sectors, each leveraging AI agents to enhance efficiency and competitiveness. Approximately 60% of enterprises focus on customer-facing applications, while backend automation accounts for a significant portion of deployments. The segmentation highlights the growing importance of scalable, flexible, and industry-specific AI solutions in driving enterprise adoption.

The Enterprise AI Agent Development Platforms Market by type includes Low-Code/No-Code Platforms, Multi-Agent Orchestration Platforms, Single-Agent Development Platforms, and Custom AI Frameworks. Multi-agent orchestration platforms currently lead the market, accounting for approximately 38% of adoption due to their ability to manage complex workflows and enable collaboration between multiple AI agents. Low-code/no-code platforms follow with around 27% share, driven by ease of deployment and reduced development time. However, low-code platforms represent the fastest-growing segment with an expected growth rate exceeding 40% annually, as enterprises increasingly prioritize accessibility and rapid prototyping capabilities. Single-agent platforms and custom frameworks collectively contribute around 35%, serving niche use cases requiring specialized AI configurations.

A 2025 enterprise technology study highlighted that over 45% of global organizations implemented multi-agent systems to automate cross-functional workflows, significantly improving operational coordination and reducing manual intervention.

Applications of Enterprise AI Agent Development Platforms include Customer Support Automation, IT Operations Management, Sales & Marketing Automation, Financial Analysis, and Supply Chain Optimization. Customer support automation dominates with approximately 32% share, as enterprises deploy AI agents to handle high volumes of queries and improve response efficiency. IT operations management follows at 25%, driven by the need for automated incident detection and resolution. Sales and marketing automation is the fastest-growing segment with an expected growth rate above 38%, supported by increasing demand for personalized customer engagement and predictive analytics. Other applications collectively account for around 43%, highlighting diverse use cases across industries. In 2025, more than 41% of enterprises globally reported piloting AI agent systems for customer experience platforms, while over 55% of organizations indicated improved customer satisfaction through AI-driven interactions.

A 2025 global enterprise survey reported that AI-powered customer support agents handled over 60% of routine service requests, significantly reducing human workload and improving response times.

Key end-users in the Enterprise AI Agent Development Platforms Market include BFSI, IT & Telecom, Healthcare, Retail, and Manufacturing. The BFSI sector leads with approximately 28% share, leveraging AI agents for fraud detection, risk assessment, and customer service automation. IT & Telecom follows at 24%, driven by demand for automated network management and IT service optimization. Healthcare is the fastest-growing segment, with adoption expected to grow at over 39% annually due to increasing use of AI in diagnostics and patient management. Other sectors, including retail and manufacturing, collectively contribute around 48%, utilizing AI agents for inventory management, demand forecasting, and operational efficiency. In 2025, more than 38% of enterprises reported deploying AI agents across multiple departments, while 52% of IT organizations integrated AI agents into core operational workflows.

A 2025 industry report indicated that AI adoption in the BFSI sector enabled over 500 financial institutions to enhance fraud detection accuracy and reduce processing time significantly through autonomous AI systems.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 39.2% between 2026 and 2033.

North America’s leadership is supported by over 65% enterprise AI adoption rates and more than 70% of global cloud-based AI workloads being processed within the region. Europe follows with approximately 27% market share, driven by strong regulatory frameworks and increasing demand for explainable AI systems across industries such as finance and healthcare. Asia-Pacific holds around 23% share, with rapid digitalization across China, India, and Japan, where over 58% of enterprises are actively piloting AI agents. South America and the Middle East & Africa collectively account for nearly 12%, with growing investments in digital infrastructure and enterprise automation. The global landscape is characterized by increasing enterprise spending on AI, which exceeds USD 300 billion annually, and over 60% of organizations prioritizing AI-driven automation strategies. Regional variations in infrastructure maturity, regulatory environments, and enterprise adoption patterns significantly influence market growth trajectories.

North America holds approximately 38% of the Enterprise AI Agent Development Platforms Market, driven by strong adoption across BFSI, healthcare, and IT sectors. Over 68% of enterprises in this region have integrated AI agents into at least one business function, particularly in customer service automation and cybersecurity. Government support, including AI research funding exceeding USD 30 billion annually, has accelerated innovation and deployment. Regulatory frameworks focusing on responsible AI and data governance are shaping enterprise strategies. Technological advancements such as multi-agent orchestration and LLM-based enterprise platforms are widely adopted, with over 72% of enterprises leveraging cloud-based AI solutions. A notable example includes Microsoft integrating AI agents into enterprise productivity tools, enabling automated workflows and improving operational efficiency by over 35%. Consumer behavior reflects higher adoption in finance and healthcare sectors, where AI-driven decision-making and automation are critical for operational scalability.

Europe accounts for approximately 27% of the Enterprise AI Agent Development Platforms Market, with key markets including Germany, the UK, and France leading adoption. Over 55% of enterprises in these countries have implemented AI-driven automation solutions. The region is heavily influenced by regulatory bodies such as the European Commission, which promotes ethical AI use and compliance through initiatives like the AI Act. Sustainability and ESG goals are driving demand for energy-efficient AI systems, with over 40% of enterprises prioritizing green AI deployments. Emerging technologies such as explainable AI and privacy-preserving machine learning are widely adopted. A notable regional player, SAP, is actively developing AI-driven enterprise solutions, enabling automation in supply chain and financial operations. Consumer behavior in Europe emphasizes transparency and compliance, leading to increased demand for interpretable AI agent platforms across regulated industries.

Asia-Pacific ranks as the fastest-growing region and holds approximately 23% of the Enterprise AI Agent Development Platforms Market. Key countries such as China, India, and Japan are leading consumption, with over 60% of enterprises in these markets actively investing in AI technologies. The region benefits from rapid expansion in digital infrastructure, including 5G networks and cloud computing, supporting scalable AI deployments. Innovation hubs in cities like Beijing, Bangalore, and Tokyo are driving advancements in AI research and development. Alibaba Cloud, for example, is investing heavily in AI agent platforms to support enterprise automation across e-commerce and logistics sectors. Consumer behavior in Asia-Pacific is heavily influenced by mobile-first ecosystems, with over 70% of enterprises focusing on AI integration in digital platforms, particularly in e-commerce and fintech applications.

South America holds approximately 6% of the Enterprise AI Agent Development Platforms Market, with Brazil and Argentina being key contributors. Over 45% of enterprises in these countries are investing in AI-driven automation to improve operational efficiency. Infrastructure development in cloud computing and data centers is expanding, supporting AI adoption across industries such as banking, retail, and media. Government initiatives promoting digital transformation and innovation are encouraging enterprise adoption of AI technologies. A regional example includes MercadoLibre leveraging AI agents to optimize logistics and customer service operations, improving delivery efficiency by over 30%. Consumer behavior in South America shows strong demand for localized AI solutions, particularly in language processing and customer engagement platforms, reflecting diverse linguistic and cultural requirements.

The Middle East & Africa region accounts for approximately 6% of the Enterprise AI Agent Development Platforms Market, driven by increasing demand in sectors such as oil & gas, construction, and financial services. Countries like the UAE and South Africa are leading adoption, with over 50% of large enterprises investing in AI-driven solutions. Technological modernization initiatives, including smart city projects and digital transformation programs, are accelerating AI deployment. Governments are actively promoting AI adoption through national strategies and partnerships with global technology providers. A notable example includes G42 in the UAE developing advanced AI platforms for enterprise applications, enhancing operational efficiency across industries. Consumer behavior in the region reflects growing interest in automation and digital services, particularly in urban areas, where AI-driven solutions are improving service delivery and business operations.

United States– 34% Market share: Due to strong enterprise AI adoption, advanced cloud infrastructure, and high R&D investment levels.

China– 18% Market share: Driven by large-scale digital transformation, government-backed AI initiatives, and rapid enterprise adoption across industries.

The Enterprise AI Agent Development Platforms Market is moderately fragmented, with over 120 active global competitors ranging from large technology firms to specialized AI startups. The top five companies collectively account for approximately 48% of the total market share, indicating a competitive yet innovation-driven environment. Leading players are focusing on strategic initiatives such as partnerships, acquisitions, and product innovation to strengthen their market positions. Over 60% of major companies have launched AI agent-based enterprise solutions within the past two years, highlighting the rapid pace of innovation.

Key competitive strategies include integration of large language models, development of multi-agent orchestration platforms, and expansion of cloud-based AI ecosystems. Companies are also investing heavily in R&D, with annual spending exceeding USD 50 billion collectively across top players. Mergers and acquisitions activity has increased by over 35% between 2023 and 2025, reflecting consolidation trends and the need for technological capabilities. Additionally, over 70% of market participants are focusing on vertical-specific AI solutions tailored to industries such as healthcare, finance, and retail. The competitive landscape is further influenced by the growing importance of AI governance, data security, and compliance, which are shaping product development and market strategies.

IBM

Amazon Web Services

Salesforce

Oracle

SAP

NVIDIA

OpenAI

Anthropic

DataRobot

C3.ai

H2O.ai

Baidu

The Enterprise AI Agent Development Platforms Market is driven by rapid advancements in artificial intelligence technologies, particularly in large language models (LLMs), multi-agent systems, and real-time data processing frameworks. Over 67% of enterprise AI platforms now integrate LLMs to enhance contextual understanding and decision-making capabilities. These models enable AI agents to process unstructured data, including text, voice, and images, improving automation across complex enterprise workflows.

Multi-agent orchestration is another critical technological advancement, with approximately 62% of enterprises adopting systems that allow multiple AI agents to collaborate and execute tasks simultaneously. This approach enhances scalability and efficiency, enabling enterprises to manage large-scale operations with minimal human intervention. Additionally, low-code and no-code AI development platforms are gaining traction, with over 54% of organizations adopting these tools to accelerate deployment and reduce reliance on specialized technical expertise.

Cloud computing and edge AI are also transforming the market, with more than 70% of AI workloads being deployed on cloud-based platforms. Edge AI is enabling real-time data processing, reducing latency by up to 40% in applications such as IoT and industrial automation. Furthermore, advancements in explainable AI and privacy-preserving technologies are addressing regulatory concerns, with over 48% of enterprises prioritizing transparency and data security in AI deployments.

Integration of AI agents with enterprise software ecosystems, including ERP and CRM platforms, is becoming increasingly common, with over 60% of organizations leveraging AI for business process optimization. Emerging technologies such as reinforcement learning and autonomous decision engines are expected to further enhance the capabilities of AI agent platforms, enabling more sophisticated and adaptive enterprise applications.

• In November 2025, Microsoft announced new enterprise AI agent capabilities within Microsoft 365 Copilot, including “Agent 365” and “Work IQ,” enabling organizations to build, manage, and deploy custom AI agents integrated with enterprise data. Over 90% of Fortune 500 companies are already using Copilot-based solutions. Source: www.microsoft.com

• In May 2025, Microsoft at its Build conference introduced advancements toward an “agentic web,” expanding AI agents across Azure, Windows, and GitHub. The update included autonomous coding agents and enterprise workflow automation features, significantly enhancing cross-platform AI agent deployment capabilities.

• In April 2025, Microsoft introduced enhanced AI-powered agents in Microsoft 365 Copilot Chat, focused on enterprise collaboration, project management, and data analytics. These agents enable automated workflows and improve enterprise productivity by supporting real-time decision-making processes.

• In March 2025, Microsoft expanded its AI agent ecosystem within Microsoft Fabric by introducing data agents that allow business users to independently analyze enterprise data. These agents reduce reliance on data analysts and enable self-service analytics across enterprise environments.

The Enterprise AI Agent Development Platforms Market Report provides a comprehensive analysis of key market segments, technologies, applications, and regional dynamics shaping the industry. The report covers multiple platform types, including low-code/no-code solutions, multi-agent orchestration systems, and custom AI frameworks, offering insights into their adoption patterns and enterprise use cases. It also evaluates application areas such as customer support automation, IT operations, financial analytics, and supply chain optimization, which collectively account for over 80% of enterprise AI agent deployments.

Geographically, the report analyzes five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting regional adoption trends, infrastructure development, and enterprise AI investment levels. It includes detailed insights into key countries, where over 60% of enterprises are actively investing in AI-driven automation solutions. The report further explores industry-specific adoption across sectors such as BFSI, healthcare, IT & telecom, retail, and manufacturing, which together represent more than 75% of total market demand.

In addition, the report examines technological advancements, including integration of large language models, multi-agent systems, and cloud-based AI platforms, which are driving innovation in the market. It also addresses regulatory frameworks, data privacy concerns, and ESG considerations influencing enterprise AI adoption. Emerging trends such as real-time decision intelligence, autonomous workflows, and scalable AI architectures are analyzed to provide forward-looking insights. Overall, the report offers a detailed and structured view of the market, enabling decision-makers to identify growth opportunities, assess competitive dynamics, and develop strategic initiatives aligned with evolving industry trends.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,075.0 Million |

| Market Revenue (2033) | USD 13,085.6 Million |

| CAGR (2026–2033) | 36.67% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft; Google; IBM; Amazon Web Services; Salesforce; Oracle; SAP; NVIDIA; OpenAI; Anthropic; DataRobot; C3.ai; H2O.ai; Baidu |

| Customization & Pricing | Available on Request (10% Customization Free) |