Reports

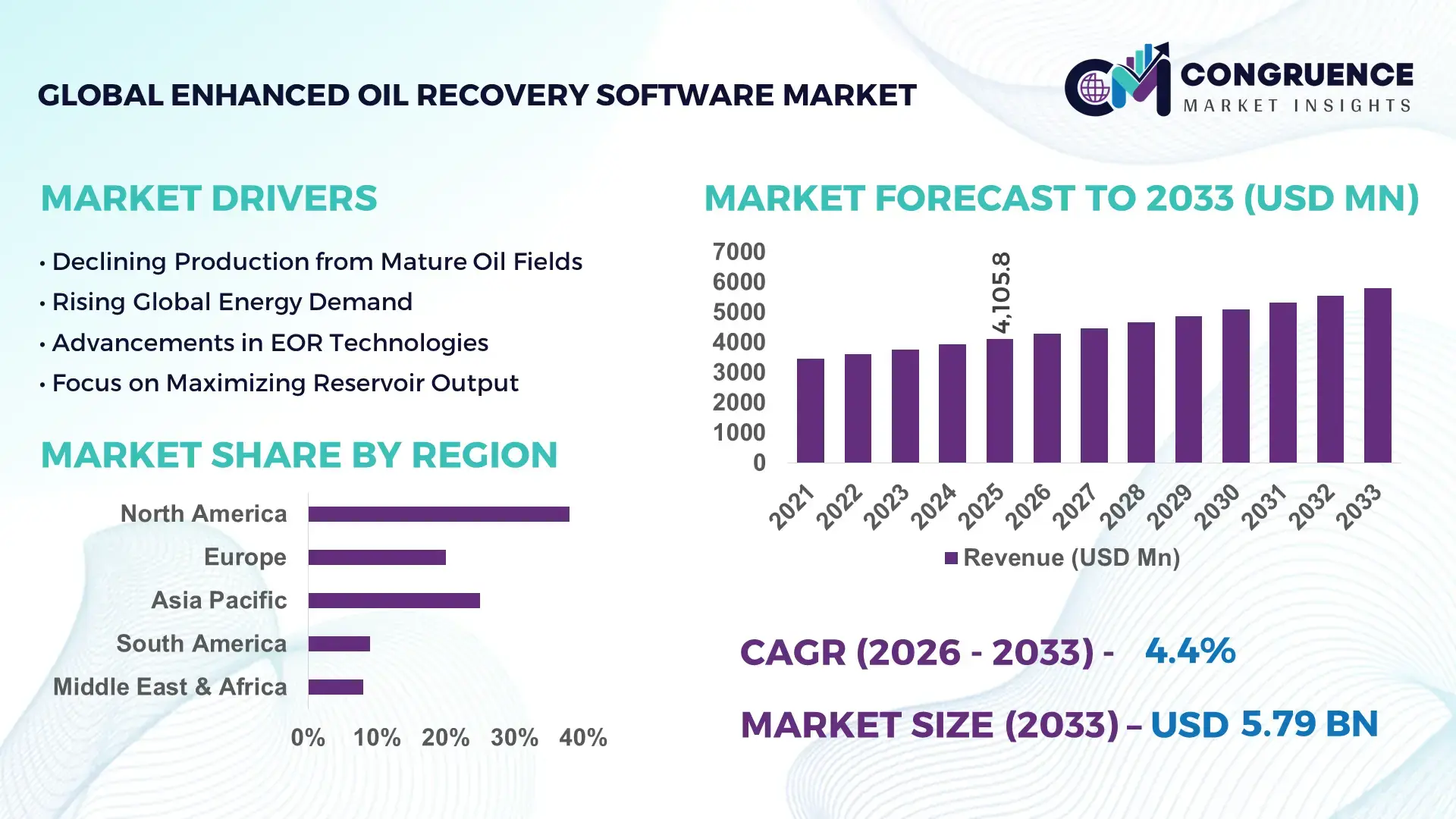

The Global Enhanced Oil Recovery Market was valued at USD 4105.78 Million in 2025 and is anticipated to reach a value of USD 5794.29 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Growth is primarily driven by rising demand for maximizing output from mature oilfields and improving recovery efficiency through advanced injection technologies.

The United States leads large-scale enhanced oil recovery deployment, supported by extensive mature reservoirs across Texas, California, and Wyoming. Over 300 active CO₂-EOR projects operate nationwide, injecting more than 70 million metric tons of CO₂ annually for tertiary recovery. Thermal EOR accounts for over 1.5 million barrels per day of incremental production, particularly in California’s heavy oil fields. Annual upstream investments exceeding USD 15 billion in advanced reservoir management, carbon capture integration, and digital oilfield technologies further strengthen production optimization capabilities. Polymer and surfactant flooding pilots in the Permian Basin have demonstrated recovery rate improvements of 10–20%, reinforcing sustained technological modernization across conventional and unconventional assets.

Market Size & Growth: Valued at USD 4105.78 Million in 2025, projected to reach USD 5794.29 Million by 2033 at a CAGR of 4.4%, supported by enhanced recovery efficiency and carbon utilization strategies.

Top Growth Drivers: Mature field redevelopment (45%), CO₂ utilization expansion (32%), improved oil recovery efficiency gains (18%).

Short-Term Forecast: By 2028, digital reservoir modeling and optimized injection processes are expected to reduce operational costs by 12% and increase recovery rates by 8%.

Emerging Technologies: Carbon capture and storage integration, AI-driven reservoir simulation, advanced polymer and surfactant flooding formulations.

Regional Leaders: North America projected at USD 2.1 Billion by 2033 with strong CO₂-EOR adoption; Middle East at USD 1.4 Billion driven by thermal EOR expansion; Asia-Pacific at USD 0.9 Billion supported by heavy oil field redevelopment.

Consumer/End-User Trends: National oil companies and independent upstream operators increasingly adopt tertiary recovery to extend field life by 10–25 years.

Pilot or Case Example: A 2024 Middle East thermal EOR pilot recorded a 17% production uplift and 14% steam-to-oil ratio improvement within 12 months.

Competitive Landscape: Schlumberger holds approximately 21% share, followed by Halliburton, Baker Hughes, Chevron Corporation, and Occidental Petroleum.

Regulatory & ESG Impact: Carbon pricing frameworks and tax incentives for CO₂ sequestration accelerate low-carbon EOR deployment across North America and Europe.

Investment & Funding Patterns: Over USD 8 Billion invested globally in CO₂ infrastructure and EOR-linked carbon capture projects between 2023–2025.

Innovation & Future Outlook: Integration of digital twin modeling, advanced chemical flooding, and low-emission steam generation systems will enhance long-term reservoir productivity.

Enhanced oil recovery technologies serve critical industry sectors including onshore conventional oilfields contributing nearly 55% of global tertiary output, offshore mature assets accounting for 20%, and heavy oil reservoirs representing approximately 25% of application demand. CO₂ injection remains the dominant method with over 60% adoption among tertiary recovery projects, while thermal techniques and chemical flooding continue expanding in high-viscosity reservoirs. Regulatory carbon reduction mandates, volatile crude pricing dynamics, and strategic energy security policies are encouraging operators to optimize asset life cycles. Rapid digitalization, advanced monitoring sensors, and sustainable injection systems are reshaping operational economics, positioning enhanced oil recovery as a long-term strategic solution for maximizing hydrocarbon recovery efficiency in aging fields worldwide.

The Enhanced Oil Recovery Market holds strategic relevance as global operators prioritize maximizing output from aging reservoirs while aligning with carbon management objectives. Nearly 60% of the world’s oil production originates from mature fields, many experiencing natural decline rates of 5–7% annually. Advanced tertiary recovery strategies, particularly carbon dioxide injection, thermal recovery, and chemical flooding, are increasingly integrated with digital reservoir optimization platforms to stabilize production and extend field life by 10–25 years. AI-driven reservoir simulation delivers 15% improvement in sweep efficiency compared to conventional static modeling methods, significantly enhancing hydrocarbon recovery outcomes.

North America dominates in production volume, while the Middle East leads in adoption with over 65% of national oil companies implementing thermal and gas injection programs across large-scale onshore fields. By 2028, AI-enabled predictive injection analytics is expected to cut operational downtime by 12% and improve reservoir monitoring accuracy by 18%. Firms are committing to ESG-driven metrics such as 20% carbon intensity reduction by 2030 through integrated CO₂ capture and utilization projects.

In 2024, Oman achieved a 17% incremental production improvement through smart steam flooding integrated with real-time digital monitoring systems. Over the next decade, integrated carbon capture, digital twins, and advanced polymer formulations are expected to reshape reservoir management economics. The Enhanced Oil Recovery Market is increasingly positioned as a pillar of resilience, regulatory compliance, and sustainable hydrocarbon development within evolving global energy frameworks.

The growing number of mature oilfields is a primary driver of Enhanced Oil Recovery deployment worldwide. Over 1,500 major oilfields have been producing for more than 25 years, with natural decline rates averaging 6% annually. Without intervention, recovery factors typically plateau at 30–35% of original oil in place. Advanced tertiary recovery techniques such as CO₂ flooding and polymer injection can increase recovery rates by an additional 10–20%, significantly improving asset utilization. In regions like the Permian Basin and Middle East carbonate reservoirs, injection optimization programs have extended field life by over 15 years. As global energy demand continues to exceed 100 million barrels per day, operators prioritize cost-effective recovery enhancement rather than new frontier exploration, strengthening long-term demand for efficient EOR technologies.

Enhanced Oil Recovery projects involve technically complex reservoir characterization, injection infrastructure development, and long implementation timelines. CO₂-EOR requires reliable access to high-purity carbon dioxide, yet global CO₂ pipeline infrastructure remains concentrated in North America, limiting broader adoption. Developing injection wells, compression facilities, and monitoring systems can increase project lead times by 3–5 years. Additionally, thermal EOR operations demand substantial energy input, with steam generation accounting for up to 40% of operating expenses in heavy oil projects. Environmental permitting requirements, water usage regulations, and subsurface monitoring compliance further add operational layers. These technical, logistical, and regulatory complexities create barriers for smaller operators and limit rapid scalability in emerging markets.

The integration of carbon capture utilization and storage presents a transformative opportunity for Enhanced Oil Recovery. Globally, more than 40 commercial CCUS facilities are operational, capturing over 45 million metric tons of CO₂ annually, a significant portion of which is used for tertiary recovery. Incentive mechanisms such as carbon credits and tax benefits are encouraging operators to deploy CO₂-EOR as a dual revenue and decarbonization strategy. In heavy oil reservoirs, solvent-assisted steam processes can reduce steam consumption by 15%, lowering emissions intensity while enhancing production. Emerging digital monitoring systems enable precise carbon accounting, supporting regulatory compliance and ESG reporting. As governments expand industrial decarbonization mandates, EOR integrated with carbon management infrastructure offers a scalable pathway to balance energy security with climate objectives.

Capital-intensive infrastructure requirements pose a significant challenge to Enhanced Oil Recovery deployment. Initial investments in injection wells, separation facilities, and compression systems can exceed hundreds of millions of dollars for large-scale projects. Reservoir heterogeneity and uncertain geological characteristics may limit sweep efficiency, reducing projected recovery improvements. Chemical flooding projects require careful formulation to prevent formation damage, and polymer degradation risks can affect long-term performance. Furthermore, fluctuating crude oil prices impact project economics, with tertiary recovery becoming less attractive during price downturns. Operators must balance technical risk assessment, long-term capital allocation, and environmental compliance obligations to ensure sustainable project returns within complex reservoir environments.

• Expansion of CO₂-EOR with Carbon Capture Integration: Carbon dioxide injection projects now represent more than 60% of active enhanced oil recovery operations globally, with over 70 million metric tons of CO₂ injected annually into mature reservoirs. Approximately 35% of newly sanctioned tertiary recovery projects are directly linked to industrial carbon capture facilities, enabling dual benefits of incremental oil production and permanent carbon storage. In North America alone, pipeline infrastructure exceeding 8,000 kilometers supports large-scale CO₂ transportation, strengthening supply chain reliability. Integrated CCUS-enabled EOR programs have demonstrated up to 18% improvement in recovery factors compared to conventional waterflooding in depleted sandstone formations.

• Digital Reservoir Optimization Improving Injection Efficiency: Advanced digital oilfield solutions are reshaping injection management strategies across the Enhanced Oil Recovery market. Over 50% of newly deployed tertiary recovery projects incorporate AI-driven reservoir modeling and real-time pressure monitoring systems. Predictive analytics platforms have reduced non-productive time by 14% and improved sweep efficiency by 12% compared to legacy reservoir simulation tools. Smart sensors installed in injection wells provide continuous subsurface data, enhancing production forecasting accuracy by nearly 20%. Operators deploying digital twin technologies have reported a 10–15% extension in effective reservoir life across complex carbonate assets.

• Growth in Chemical EOR for Complex Reservoirs: Chemical flooding techniques, including polymer and surfactant injection, account for approximately 22% of active tertiary recovery initiatives, particularly in Asia-Pacific and Latin America. Recent high-molecular-weight polymer formulations have increased oil displacement efficiency by 15% while reducing chemical degradation rates by 9% under high-temperature conditions. Field pilots in offshore environments indicate that optimized surfactant blends can enhance microscopic sweep efficiency by up to 13%. Demand for advanced chemical EOR solutions is accelerating in reservoirs with permeability challenges, where traditional waterflooding achieves less than 35% recovery efficiency.

• Thermal EOR Advancements in Heavy Oil Production: Thermal enhanced oil recovery, particularly steam-assisted gravity drainage (SAGD), contributes nearly 30% of tertiary production in heavy oil basins. In Canada and the Middle East, solvent-assisted steam processes have reduced steam-to-oil ratios by 16%, significantly lowering fuel consumption and emissions intensity. Automated steam control systems have improved thermal injection precision by 11%, enhancing bitumen recovery from viscous reservoirs. New insulated wellbore technologies have extended operational lifespan by 12% while decreasing heat loss during injection cycles, supporting more energy-efficient heavy oil extraction across large-scale onshore developments.

The Enhanced Oil Recovery market is strategically segmented by type, application, and end-user, reflecting diverse reservoir characteristics and operational priorities across global oil-producing regions. By type, CO₂ injection, thermal recovery, and chemical flooding dominate tertiary production strategies, each tailored to specific geological formations and crude characteristics. Applications primarily focus on onshore mature oilfields, offshore reservoirs, and heavy oil deposits, with deployment intensity varying by reservoir depth and viscosity profiles. End-user segmentation highlights national oil companies, independent exploration and production firms, and integrated energy majors as principal adopters. More than 70% of tertiary recovery projects are concentrated in mature onshore basins, while offshore and unconventional reservoirs are gaining traction due to technological improvements. Increasing integration of carbon capture systems, digital monitoring platforms, and advanced injection modeling tools further differentiates adoption patterns across these segments, enabling more precise recovery optimization and long-term asset management.

CO₂ injection currently represents approximately 58% of global Enhanced Oil Recovery deployment, making it the leading type due to its dual capability of improving recovery rates and enabling carbon storage. CO₂ flooding can enhance oil recovery by 10–20% beyond primary and secondary methods, particularly in light oil sandstone reservoirs. Thermal recovery methods, including steam flooding and steam-assisted gravity drainage (SAGD), account for nearly 30% of adoption, primarily in heavy oil and bitumen fields where viscosity reduction is critical for flow improvement. Chemical EOR, comprising polymer and surfactant flooding, holds about 12% share but is the fastest-growing segment, expanding at an estimated CAGR of 6.2% due to advancements in high-temperature-resistant polymers and improved chemical stability. Adoption is accelerating in Asia-Pacific and Latin America, where heterogeneous reservoirs require enhanced sweep efficiency. The combined share of emerging hybrid techniques, including microbial and low-salinity flooding, remains below 5%, yet these methods serve niche applications in complex carbonate formations.

Onshore mature oilfields account for nearly 65% of Enhanced Oil Recovery applications, driven by extensive aging reservoirs in North America and the Middle East. These fields often experience natural decline rates above 5% per year, making tertiary recovery essential to sustain output. Offshore reservoirs contribute approximately 20% of application deployment, supported by improved subsea injection systems and reservoir modeling tools that enhance production stability in deepwater environments. Heavy oil and bitumen extraction represents around 15% of total applications but is the fastest-growing segment, expanding at an estimated CAGR of 6.8% as solvent-assisted steam processes and advanced thermal techniques improve efficiency. While onshore projects dominate in volume, offshore adoption is increasing rapidly, particularly in Brazil and Southeast Asia, where more than 40% of newly developed offshore assets are evaluating tertiary recovery integration.

National oil companies (NOCs) represent the leading end-user segment, accounting for approximately 52% of Enhanced Oil Recovery project deployment due to their control over large, mature reservoirs and long-term production mandates. Independent exploration and production companies contribute around 30%, focusing on optimizing existing assets through cost-efficient tertiary recovery techniques. Integrated oil majors comprise nearly 18%, leveraging advanced digital tools and carbon management integration across diversified portfolios. While NOCs dominate in volume, independent operators represent the fastest-growing end-user group, expanding at an estimated CAGR of 5.9% as smaller producers adopt modular injection systems and digital reservoir analytics to improve field performance. Adoption rates among upstream operators in North America exceed 60% for CO₂-EOR programs in mature basins. The combined share of smaller regional operators and joint ventures accounts for nearly 12%, often targeting selective reservoir enhancement projects.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2026 and 2033.

North America’s dominance is supported by more than 300 active CO₂ injection projects and over 70 million metric tons of annual CO₂ utilization for tertiary recovery. Europe holds approximately 18% share, driven by mature North Sea reservoirs and carbon management integration programs. Asia-Pacific contributes nearly 22% of global deployment volume, with China and India accelerating polymer and thermal EOR adoption across aging onshore fields. The Middle East & Africa region represents around 15% share, supported by large carbonate reservoirs implementing miscible gas injection. South America accounts for nearly 7%, led by Brazil’s offshore pre-salt optimization initiatives. Across all regions, more than 65% of tertiary recovery investment is concentrated in onshore mature basins, while offshore EOR integration has increased by 12% over the past three years due to subsea injection advancements and digital reservoir monitoring technologies.

How Are Advanced Carbon Utilization Strategies Strengthening Tertiary Recovery Efficiency?

North America holds approximately 38% of the global Enhanced Oil Recovery market, supported by extensive mature reservoirs in the United States and Canada. The region injects more than 70 million metric tons of CO₂ annually, with Texas and Wyoming leading tertiary recovery deployment. Federal incentives encouraging carbon capture utilization have stimulated over 45 large-scale CCUS-linked oilfield projects. Digital oilfield technologies, including AI-driven reservoir modeling and real-time injection monitoring, are implemented in nearly 60% of active tertiary operations. Local players such as Occidental Petroleum operate some of the largest CO₂-EOR networks, managing thousands of kilometers of pipeline infrastructure. Regional operator behavior reflects strong adoption of carbon-integrated production models, with enterprise-level upstream companies prioritizing long-term reservoir life extension and emissions intensity reduction targets exceeding 20% by 2030.

How Is Carbon Regulation Driving Advanced Recovery Deployment in Mature Basins?

Europe represents approximately 18% of the Enhanced Oil Recovery market, with key activity concentrated in the United Kingdom, Norway, and Germany. Mature North Sea reservoirs require enhanced recovery to counter natural decline rates exceeding 6% annually. Regional sustainability frameworks encourage integration of carbon capture with tertiary recovery, particularly in offshore environments. Over 30% of active EOR feasibility projects in the region involve CO₂ injection or low-carbon gas reinjection systems. Advanced subsea compression and reservoir imaging technologies are deployed to improve sweep efficiency by nearly 12% compared to legacy waterflood systems. Companies such as Equinor are advancing carbon storage-linked EOR pilots in offshore fields. Regional adoption patterns reflect heightened regulatory pressure, prompting operators to implement transparent monitoring, reporting, and verification systems aligned with carbon reduction commitments.

How Are Expanding Onshore Developments Enhancing Reservoir Productivity?

Asia-Pacific accounts for nearly 22% of global Enhanced Oil Recovery deployment, ranking as the fastest-growing regional market. China, India, and Indonesia collectively operate more than 200 polymer flooding projects targeting mature sandstone reservoirs. Onshore heavy oil basins in China report recovery improvements of 12–18% through advanced chemical injection. Infrastructure investments exceeding 15 new injection facilities over the past three years demonstrate regional commitment to tertiary recovery. Technological innovation hubs in China are developing temperature-resistant polymers with 10% higher stability under high-salinity conditions. PetroChina has implemented large-scale polymer flooding across the Daqing oilfield, enhancing production sustainability. Regional operator behavior emphasizes cost-optimized solutions, with national oil companies integrating domestic manufacturing of injection chemicals to reduce operational expenditures by nearly 8%.

How Are Offshore Optimization Initiatives Strengthening Production Sustainability?

South America holds approximately 7% of the global Enhanced Oil Recovery market, with Brazil and Argentina leading deployment. Brazil’s offshore pre-salt reservoirs increasingly evaluate gas injection and chemical flooding to stabilize output, particularly in deepwater assets exceeding 2,000 meters depth. Around 25% of offshore mature fields in the region are assessing tertiary recovery integration to offset decline rates near 5% annually. Infrastructure modernization, including floating production storage and offloading units, supports injection-based production enhancement. Petrobras is advancing pilot CO₂ reinjection initiatives in offshore platforms to improve reservoir pressure maintenance. Regional demand patterns emphasize offshore optimization, with operators prioritizing enhanced recovery in high-value deepwater projects while balancing environmental compliance and operational efficiency.

How Are Large Carbonate Reservoirs Adopting Advanced Gas Injection Technologies?

The Middle East & Africa region represents nearly 15% of global Enhanced Oil Recovery deployment, driven by extensive carbonate reservoirs in the United Arab Emirates, Oman, and Saudi Arabia. Gas injection and thermal recovery techniques are implemented across more than 100 mature onshore fields. Regional oil producers are modernizing injection infrastructure, with automated monitoring systems improving sweep efficiency by 14%. Trade partnerships support technology transfer for solvent-assisted steam processes and miscible gas injection. ADNOC has expanded CO₂ injection capacity across multiple onshore assets, targeting carbon intensity reductions exceeding 15%. Regional operator behavior emphasizes large-scale deployment strategies, leveraging substantial reservoir volumes to achieve long-term production stability while integrating carbon management objectives.

United States – 34% share: The United States leads the Enhanced Oil Recovery market due to extensive CO₂ pipeline infrastructure exceeding 8,000 kilometers and more than 300 active tertiary recovery projects across mature basins.

China – 16% share: China maintains a strong position in the Enhanced Oil Recovery market through large-scale polymer flooding programs across over 200 mature oilfields and sustained state-backed investment in reservoir modernization.

The Enhanced Oil Recovery market exhibits a moderately consolidated competitive structure, with the top five companies accounting for approximately 54% of global project deployment. More than 120 active service providers, chemical suppliers, and integrated energy companies operate across CO₂ injection, thermal recovery, and chemical flooding segments. Leading multinational oilfield service companies dominate technology-driven segments such as advanced reservoir simulation, smart injection systems, and high-performance polymer development. Strategic positioning increasingly centers on carbon capture integration, digital oilfield transformation, and long-term reservoir management contracts.

Over the past three years, more than 25 strategic partnerships have been announced to expand CO₂ infrastructure, enhance chemical formulation capabilities, and co-develop solvent-assisted steam technologies. Mergers and joint ventures have strengthened regional presence in North America and the Middle East, where over 65% of tertiary recovery investment is concentrated. Innovation intensity is rising, with nearly 40% of large operators integrating AI-driven reservoir analytics to improve sweep efficiency by 10–15%. Competitive differentiation increasingly depends on proprietary polymer chemistry, low-emission steam generation systems, and digital twin deployment. As ESG-linked carbon utilization becomes central to upstream strategies, firms with integrated CCUS-EOR capabilities are securing long-term contracts and expanding global influence.

Schlumberger

Halliburton

Baker Hughes

Occidental Petroleum

Chevron Corporation

Royal Dutch Shell

ExxonMobil

China Petroleum & Chemical Corporation (Sinopec)

Petrobras

Linde plc

Technological innovation is fundamentally transforming the Enhanced Oil Recovery market, with operators deploying advanced injection systems, digital reservoir analytics, and carbon-integrated production models to maximize hydrocarbon extraction efficiency. CO₂ injection remains the most widely adopted technology, representing over 60% of active tertiary recovery projects worldwide. Modern miscible CO₂ flooding can increase oil recovery by 10–20% beyond secondary methods, particularly in light oil sandstone reservoirs. More than 70 million metric tons of carbon dioxide are injected annually into mature fields, supported by pipeline networks exceeding 8,000 kilometers in major producing regions.

Thermal recovery technologies, including steam-assisted gravity drainage and cyclic steam stimulation, contribute nearly 30% of tertiary production in heavy oil basins. Recent advancements in solvent-assisted steam processes have reduced steam-to-oil ratios by 15–18%, lowering fuel consumption and emissions intensity. Automated steam control systems improve injection precision by approximately 12%, enhancing reservoir contact and thermal efficiency. Insulated wellbore technologies further reduce heat loss by up to 10%, extending operational lifespan and reducing maintenance intervals.

Chemical enhanced oil recovery is gaining momentum, accounting for roughly 12% of global deployment. High-molecular-weight polymer formulations now demonstrate 9–14% higher thermal stability in reservoirs exceeding 90°C, while advanced surfactant blends enhance microscopic displacement efficiency by up to 13%. Digital transformation plays a central role, with over 50% of newly commissioned projects integrating AI-based reservoir simulation and real-time pressure monitoring systems. Predictive analytics platforms have reduced non-productive time by 14% and improved sweep efficiency by nearly 12% compared to traditional static modeling approaches.

Emerging technologies such as low-salinity water flooding, nanofluid injection, and microbial enhanced oil recovery are undergoing pilot testing across more than 25 fields globally. Digital twin platforms enable continuous reservoir modeling updates, improving forecasting accuracy by nearly 20%. The convergence of carbon capture integration, intelligent injection optimization, and advanced chemical engineering is positioning the Enhanced Oil Recovery market for sustained operational resilience and higher recovery performance across mature oilfield assets.

• In March 2024, Occidental Petroleum announced expansion of its direct air capture–linked CO₂ supply to support Permian Basin enhanced oil recovery operations, targeting injection capacity of up to 500,000 metric tons of CO₂ annually in the first phase. The project integrates carbon sequestration with tertiary recovery optimization. Source: www.oxy.com

• In February 2025, ADNOC confirmed scaling of its carbon capture capacity to 1.5 million metric tons per year, with captured CO₂ injected into onshore reservoirs for enhanced oil recovery. The initiative supports reservoir pressure maintenance while advancing a 25% reduction in upstream carbon intensity by 2030. Source: www.adnoc.ae

• In September 2024, Equinor advanced feasibility studies for CO₂ injection in the Norwegian Continental Shelf to enhance recovery from mature fields, evaluating storage potential exceeding 5 million metric tons annually linked to offshore reservoir management programs. Source: www.equinor.com

• In April 2025, PetroChina reported expansion of polymer flooding across the Daqing oilfield, increasing treated reservoir area by over 200 square kilometers and achieving incremental recovery improvements of approximately 12% compared to conventional waterflooding. Source: www.petrochina.com

The Enhanced Oil Recovery Market Report provides a comprehensive evaluation of tertiary recovery technologies, reservoir applications, and strategic investment trends across major oil-producing regions. The report covers primary EOR types including CO₂ injection, thermal recovery, chemical flooding, and emerging hybrid techniques such as low-salinity water and microbial injection. Together, CO₂ and thermal technologies account for nearly 85% of global tertiary production methods, while chemical EOR contributes approximately 12%, reflecting growing adoption in heterogeneous and high-temperature reservoirs.

Geographically, the report analyzes five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—covering more than 40 key oil-producing countries. It evaluates over 300 active CO₂ injection projects worldwide and more than 200 polymer flooding operations concentrated in Asia-Pacific. Offshore and onshore application segmentation is included, with onshore mature fields representing nearly 65% of tertiary deployment volume.

Industry focus areas include carbon capture integration, digital reservoir optimization, solvent-assisted steam technologies, and advanced polymer engineering. The report also assesses infrastructure such as CO₂ pipeline networks exceeding 8,000 kilometers globally and emerging digital twin platforms adopted in over 50% of new large-scale projects. Niche segments such as nanofluid injection and solvent-enhanced SAGD are examined for pilot-scale potential across more than 25 fields worldwide.

This report delivers strategic insight into technological modernization, carbon management alignment, regulatory compliance frameworks, and operational efficiency benchmarks shaping long-term enhanced recovery deployment across mature hydrocarbon basins.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schlumberger, Halliburton, Baker Hughes, Occidental Petroleum, Chevron Corporation, Royal Dutch Shell, ExxonMobil, China Petroleum & Chemical Corporation (Sinopec), Petrobras, Linde plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |