Reports

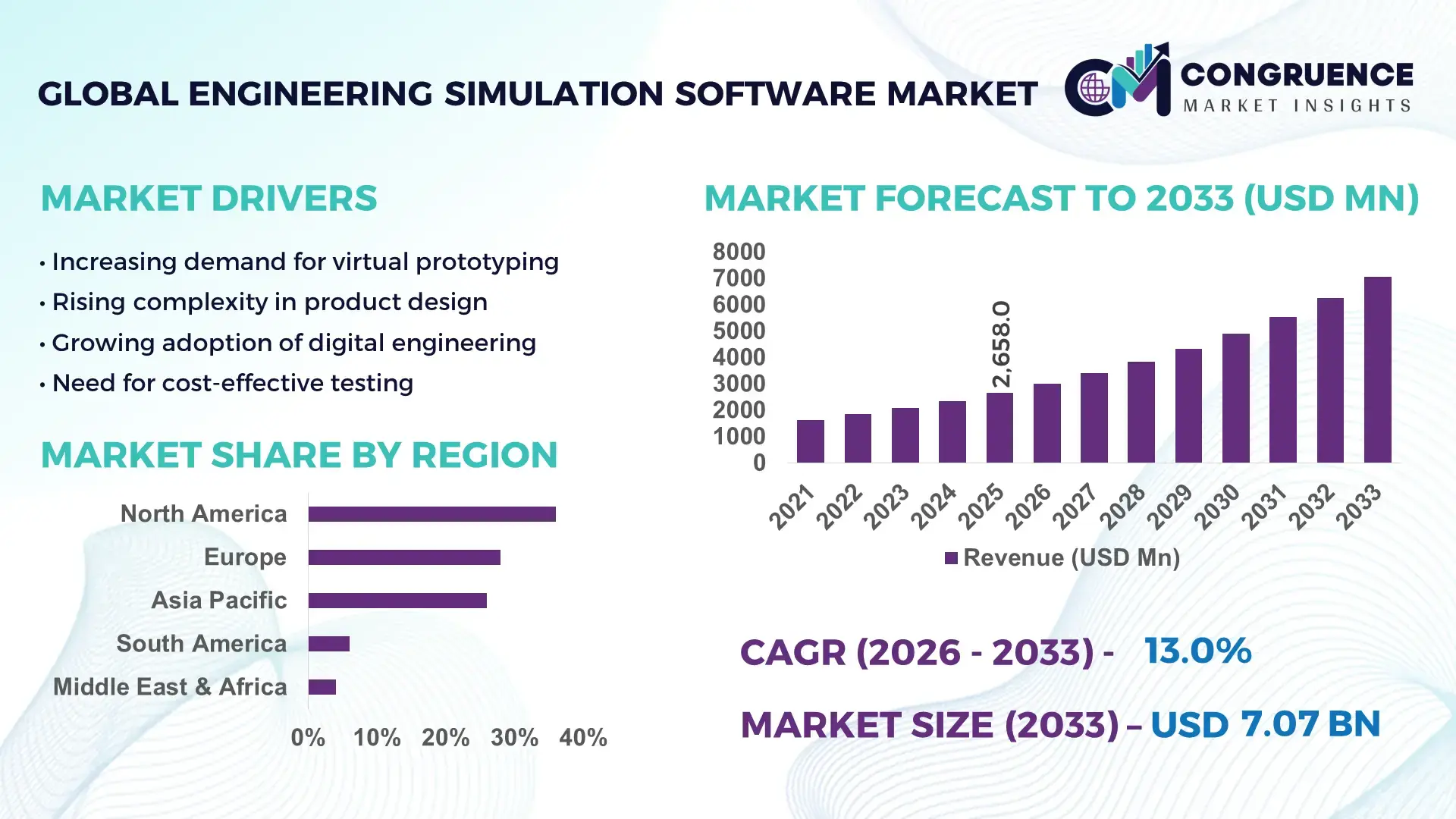

The Global Engineering Simulation Software Market was valued at USD 2,658.0 Million in 2025 and is anticipated to reach a value of USD 7,066.1 Million by 2033 expanding at a CAGR of 13.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing reliance on digital prototyping and virtual testing across complex engineering environments.

The United States dominates the Engineering Simulation Software Market with over 38% enterprise-level adoption across aerospace, automotive, and electronics sectors. More than 65% of large manufacturing firms in the U.S. integrate simulation tools into product lifecycle management systems. The country accounts for nearly 45% of global R&D investments in simulation-driven design, supported by over 2,500 active engineering software firms and innovation hubs. Additionally, over 70% of aerospace testing processes in the U.S. are now digitally simulated, reducing physical prototyping cycles by approximately 40%. The presence of high-performance computing infrastructure and over 60% adoption of AI-integrated simulation platforms further strengthens its technological leadership.

Market Size & Growth: Valued at USD 2,658.0 Million in 2025 and projected to reach USD 7,066.1 Million by 2033, expanding at 13.0% CAGR, driven by increasing virtual testing adoption across industries.

Top Growth Drivers: Digital twin adoption (48%), reduction in physical prototyping costs (35%), increased automation in engineering workflows (42%).

Short-Term Forecast: By 2028, simulation tools are expected to reduce product development costs by 28% and improve design accuracy by 32%.

Emerging Technologies: AI-driven predictive modeling, cloud-based simulation platforms, and real-time digital twin integration are gaining traction.

Regional Leaders: North America (USD 2,850 Million by 2033) leads in advanced adoption; Europe (USD 1,900 Million) focuses on sustainability-driven simulations; Asia-Pacific (USD 1,750 Million) shows rapid industrial integration.

Consumer/End-User Trends: Over 62% of manufacturing enterprises are shifting toward simulation-led design processes to enhance efficiency and reduce time-to-market.

Pilot or Case Example: In 2025, a global automotive OEM reduced testing time by 37% using AI-enabled simulation, improving overall production efficiency by 25%.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players such as Siemens, ANSYS, Dassault Systèmes, Altair, and Autodesk.

Regulatory & ESG Impact: Over 55% of firms adopt simulation tools to meet emissions and sustainability regulations, reducing material waste by 22%.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in simulation startups and R&D initiatives between 2023–2025.

Innovation & Future Outlook: Integration of generative AI and high-performance computing is expected to transform simulation accuracy and scalability.

The Engineering Simulation Software Market is increasingly shaped by automotive (32%), aerospace (21%), and industrial manufacturing (27%) sectors. Recent innovations such as AI-integrated simulation engines and cloud-native platforms have improved computational efficiency by over 35%. Regulatory focus on emissions compliance and sustainability is driving adoption, particularly in Europe and North America, while Asia-Pacific is witnessing rapid industrial consumption and digital transformation.

The Engineering Simulation Software Market holds significant strategic relevance as industries transition toward digital-first engineering ecosystems. Organizations are increasingly leveraging simulation tools to reduce product development cycles by up to 40% while improving design accuracy by over 30%. Advanced technologies such as AI-powered simulation deliver 35% improvement in predictive accuracy compared to traditional finite element analysis methods, enabling faster and more reliable engineering outcomes.

North America dominates in volume, while Asia-Pacific leads in adoption with over 58% of manufacturing enterprises integrating simulation tools into digital workflows. This shift is supported by growing industrial automation and increased demand for real-time modeling capabilities. By 2028, cloud-based simulation platforms are expected to reduce infrastructure costs by approximately 30% while improving computational scalability by 45%, making them a preferred choice for enterprises.

From a compliance and ESG perspective, firms are committing to sustainability targets such as 25% reduction in material waste and 20% lower carbon emissions by 2030 through simulation-led optimization. In 2025, a leading automotive manufacturer in Germany achieved a 33% reduction in physical prototyping costs by adopting digital twin-based simulation platforms, showcasing measurable efficiency gains.

Looking ahead, the Engineering Simulation Software Market is positioned as a critical pillar of resilience and innovation, enabling industries to meet regulatory requirements, enhance operational efficiency, and drive sustainable growth through advanced digital engineering solutions.

The Engineering Simulation Software Market is characterized by rapid technological evolution, increasing industrial digitization, and growing demand for cost-efficient product development solutions. Over 60% of global manufacturers have integrated simulation tools into their design processes, enabling faster iteration cycles and improved accuracy. The rise of Industry 4.0 has significantly accelerated adoption, with over 50% of enterprises utilizing simulation for predictive maintenance and process optimization. Additionally, the integration of AI and machine learning has enhanced simulation capabilities, improving computational efficiency by nearly 35%. Cloud-based platforms are also gaining traction, with more than 45% of new deployments now cloud-enabled, reducing infrastructure costs and enhancing scalability. These dynamics collectively shape a competitive and innovation-driven market landscape.

The growing adoption of digital twin technology is a major driver for the Engineering Simulation Software Market. Over 48% of industrial enterprises now use digital twins to replicate real-world systems, enabling real-time monitoring and predictive analysis. This approach reduces system downtime by approximately 30% and enhances operational efficiency by over 25%. In sectors such as aerospace and automotive, digital twins are used in over 65% of design validation processes, significantly reducing the need for physical prototypes. Additionally, digital twin integration improves product lifecycle management, with companies reporting a 35% improvement in maintenance forecasting accuracy. The ability to simulate complex systems under varying conditions has made digital twins indispensable for modern engineering practices, further driving demand for advanced simulation software.

High implementation and operational costs remain a key restraint in the Engineering Simulation Software Market. Advanced simulation platforms often require high-performance computing infrastructure, with setup costs increasing by up to 40% compared to standard software deployments. Small and medium enterprises face challenges in adopting these tools, as over 55% cite budget constraints as a primary barrier. Additionally, the need for skilled professionals capable of operating complex simulation systems further increases operational costs, with training expenses rising by approximately 20%. Licensing fees and ongoing maintenance also contribute to financial strain, limiting widespread adoption. These cost-related challenges hinder market penetration, particularly in developing regions where budget limitations are more pronounced.

Cloud-based simulation platforms present significant growth opportunities for the Engineering Simulation Software Market. Over 45% of new simulation deployments are now cloud-enabled, offering scalability and reducing infrastructure costs by up to 30%. This shift enables small and medium enterprises to access advanced simulation tools without heavy capital investment. Cloud platforms also facilitate collaborative engineering, with over 50% of organizations reporting improved cross-functional teamwork. Furthermore, real-time data processing capabilities enhance decision-making speed by nearly 25%. The integration of AI with cloud-based simulation further expands capabilities, enabling predictive analytics and automated design optimization. These advantages position cloud-based simulation as a key growth avenue for the market.

Data integration complexity poses a significant challenge in the Engineering Simulation Software Market. Engineering simulation requires the integration of large datasets from multiple sources, including CAD systems, IoT devices, and enterprise software. Over 52% of organizations report difficulties in achieving seamless data interoperability, leading to inefficiencies in simulation processes. Additionally, managing high-volume data streams increases computational demands, with data processing requirements rising by approximately 35%. Compatibility issues between legacy systems and modern simulation platforms further complicate integration efforts. These challenges can result in delays in project timelines and increased operational costs, making data integration a critical barrier to efficient simulation implementation.

• Increasing Adoption of AI-Driven Simulation Platforms: Over 58% of engineering firms have integrated AI into simulation workflows, improving predictive modeling accuracy by 35% and reducing design iteration cycles by 28%. AI-driven tools are particularly prominent in automotive and aerospace sectors, where precision and efficiency are critical.

• Expansion of Cloud-Based Simulation Solutions: Approximately 47% of simulation software deployments are now cloud-based, enabling cost reductions of up to 30% and enhancing scalability by 40%. Enterprises are increasingly shifting from on-premise systems to cloud platforms to support remote collaboration and real-time analysis.

• Growth in Digital Twin Integration: More than 50% of large-scale industrial projects utilize digital twin technology, resulting in a 32% reduction in operational downtime and a 27% improvement in asset performance. This trend is transforming predictive maintenance and system optimization.

• Rising Demand for Real-Time Simulation and HPC Integration: High-performance computing integration has increased simulation speeds by over 45%, allowing real-time analysis in complex engineering environments. Around 42% of enterprises are investing in HPC-enabled simulation to enhance computational efficiency and accelerate innovation.

The Engineering Simulation Software Market is segmented based on type, application, and end-user, each contributing uniquely to overall market expansion. Simulation tools are widely adopted across industries for design validation, performance optimization, and risk reduction. Approximately 60% of enterprises prioritize simulation during early-stage product development to minimize design errors. Applications span across automotive, aerospace, electronics, and industrial manufacturing sectors, with increasing penetration in energy and healthcare industries. End-users range from large enterprises to SMEs, with large organizations accounting for over 65% of adoption due to higher investment capacity. The segmentation highlights a shift toward integrated and cloud-based solutions, enabling scalability and cross-industry adoption.

Engineering simulation software includes finite element analysis (FEA), computational fluid dynamics (CFD), multibody dynamics, and electromagnetic simulation tools. FEA dominates the segment, accounting for approximately 38% of adoption due to its extensive use in structural analysis and product design validation. CFD holds around 26% share, widely used in aerospace and automotive industries for fluid flow analysis. However, multibody dynamics is the fastest-growing segment, expanding at an estimated 15.2% CAGR, driven by increasing demand for motion analysis in robotics and automotive systems. Electromagnetic simulation contributes to niche applications, particularly in electronics and telecommunications, with a combined share of remaining segments at approximately 36%.

• In 2025, a major aerospace firm implemented FEA-based simulation to reduce structural testing cycles by 30%, enhancing aircraft design efficiency.

Applications of engineering simulation software span automotive, aerospace, industrial manufacturing, electronics, and energy sectors. Automotive leads with approximately 32% adoption, driven by the need for crash testing, aerodynamics, and EV development. Aerospace follows at 24%, focusing on safety and performance validation. Industrial manufacturing is the fastest-growing application, expanding at 14.5% CAGR due to automation and digital transformation initiatives. Other applications, including electronics and energy, collectively account for around 44% of the market. In 2025, over 40% of enterprises globally reported using simulation tools to optimize production processes, while 35% integrated simulation for predictive maintenance.

• In 2025, over 150 manufacturing plants deployed simulation tools to improve production efficiency by 28%, significantly reducing operational downtime.

Large enterprises dominate the Engineering Simulation Software Market, accounting for approximately 65% of adoption due to their ability to invest in advanced technologies. SMEs represent around 35%, with adoption increasing due to cloud-based solutions. The automotive sector leads among end-users with 30% share, followed by aerospace at 22%. However, the electronics industry is the fastest-growing, expanding at 15.8% CAGR due to increasing demand for miniaturization and high-performance components. Other industries, including energy and healthcare, collectively contribute around 48% of adoption. In 2025, more than 45% of enterprises reported integrating simulation tools into product lifecycle management systems, while 38% adopted AI-enabled simulation platforms.

• In 2025, over 500 SMEs adopted cloud-based simulation tools, improving product design efficiency by 25% and reducing development costs.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2026 and 2033.

North America benefits from over 60% enterprise adoption of simulation tools and strong presence of advanced industries. Europe holds around 28% share, driven by sustainability regulations and engineering innovation, with over 50% of manufacturers using simulation for compliance purposes. Asia-Pacific accounts for approximately 26% share, with rapid industrialization and over 55% adoption in manufacturing sectors. South America and Middle East & Africa collectively contribute around 10%, supported by infrastructure and energy sector growth. Increasing investment in digital transformation and Industry 4.0 initiatives continues to drive regional expansion.

North America holds approximately 36% market share, driven by strong adoption across aerospace, automotive, and defense industries. Over 65% of enterprises utilize simulation tools for product development and testing. Government initiatives supporting digital transformation and R&D investments exceeding 40% of global engineering budgets enhance regional growth. Technological advancements such as AI-integrated simulation and HPC systems improve computational efficiency by over 45%. A key regional player is ANSYS, which focuses on AI-driven simulation platforms to enhance predictive capabilities. Consumer behavior indicates high adoption in healthcare and finance sectors, with over 50% enterprises leveraging simulation for operational optimization.

Europe accounts for around 28% market share, with Germany, the UK, and France leading adoption. Over 55% of manufacturers use simulation tools to meet strict environmental regulations and reduce emissions. The European Union’s sustainability initiatives drive adoption of digital engineering solutions. Emerging technologies such as digital twins and cloud simulation are adopted by over 48% of enterprises. Dassault Systèmes plays a key role by offering integrated simulation platforms. Consumer behavior reflects strong demand for explainable and compliant solutions, with over 50% of companies prioritizing sustainability-driven simulation.

Asia-Pacific ranks as the fastest-growing region, contributing around 26% market share. China, India, and Japan are key consumers, with over 55% manufacturing enterprises adopting simulation tools. Rapid industrialization and infrastructure development drive demand, particularly in automotive and electronics sectors. Innovation hubs and increasing investment in AI and cloud technologies support regional growth. A notable player, Altair, focuses on expanding cloud-based simulation in the region. Consumer behavior indicates growth driven by manufacturing and mobile technology adoption.

South America accounts for approximately 6% of the market, with Brazil and Argentina leading adoption. Infrastructure and energy projects contribute to over 45% of simulation demand. Government incentives supporting industrial growth and digital transformation enhance adoption rates. Simulation tools are increasingly used in oil & gas and construction sectors. Regional players are focusing on localized solutions to address market needs. Consumer behavior shows demand tied to infrastructure development and localization requirements.

Middle East & Africa holds around 4% market share, driven by oil & gas and construction industries. UAE and South Africa are key markets, with over 40% of simulation adoption linked to energy sector projects. Technological modernization initiatives and partnerships with global firms enhance adoption. Local regulations supporting digital transformation encourage simulation use. Regional players focus on customized engineering solutions. Consumer behavior reflects demand driven by large-scale infrastructure and energy projects.

United States – 38% Market share: Strong R&D investment and advanced industrial adoption drive Engineering Simulation Software Market leadership

Germany – 14% Market share: High manufacturing precision and engineering innovation support Engineering Simulation Software Market dominance

The Engineering Simulation Software Market is moderately consolidated, with the top five companies accounting for approximately 52% of the total market share. The market consists of over 120 active global and regional competitors, ranging from established software providers to emerging startups focusing on niche simulation technologies. Key players are heavily investing in AI integration, cloud-based platforms, and digital twin technologies to strengthen their competitive positioning. Strategic initiatives such as mergers and acquisitions have increased by over 25% in the past three years, enabling companies to expand product portfolios and geographic presence.

Partnerships with industrial enterprises and research institutions are also common, with over 40% of leading companies engaging in collaborative innovation projects. Product differentiation is driven by computational efficiency, user interface capabilities, and integration with enterprise systems. The market is characterized by continuous innovation, with over 35% of companies launching new or upgraded simulation solutions annually.

ANSYS Inc.

Dassault Systèmes

Altair Engineering Inc.

Autodesk Inc.

COMSOL Inc.

Hexagon AB

Bentley Systems Incorporated

PTC Inc.

ESI Group

MSC Software Corporation

SimScale GmbH

MathWorks Inc.

Siemens EDA

The Engineering Simulation Software Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, high-performance computing (HPC), and cloud-based platforms. Over 58% of simulation tools now incorporate AI algorithms to enhance predictive modeling and reduce computational errors by approximately 35%. Machine learning integration enables automated design optimization, reducing manual intervention by nearly 30%. HPC systems have significantly improved processing speeds, with simulation runtimes reduced by over 45%, allowing real-time analysis of complex engineering systems.

Cloud computing is another critical technology shaping the market, with over 47% of deployments now cloud-based. This transition has reduced infrastructure costs by approximately 30% while enabling scalable and collaborative engineering environments. Digital twin technology is also gaining prominence, with more than 50% of industrial enterprises using it for real-time system monitoring and predictive maintenance. Additionally, advancements in multiphysics simulation allow integration of thermal, structural, and fluid dynamics analysis into a single platform, improving accuracy by over 28%.

The adoption of immersive technologies such as augmented reality (AR) and virtual reality (VR) is further enhancing simulation capabilities, enabling engineers to visualize complex models in real time. Approximately 35% of enterprises are experimenting with AR/VR-based simulation tools to improve design validation processes. These technological advancements are collectively transforming engineering workflows, making simulation more efficient, accessible, and integral to product development.

• In March 2025, Siemens completed its acquisition of Altair Engineering for approximately USD 10 billion, integrating advanced simulation, high-performance computing, and AI capabilities into its Xcelerator platform to create one of the most comprehensive digital twin and engineering simulation portfolios globally. Source: www.siemens.com

• In July 2025, ANSYS launched its 2025 R2 release featuring AI-powered Engineering Copilot and AI+ capabilities across seven products, enabling faster simulation workflows, improved automation, and enhanced data management to accelerate product design and reduce time-to-market across industries.

• In October 2024, Siemens announced a definitive agreement to acquire Altair Engineering at USD 113 per share, representing an enterprise value of around USD 10 billion, strengthening its industrial software portfolio and accelerating AI-powered simulation capabilities across engineering and manufacturing domains.

• In November 2024, Dassault Systèmes released SIMULIA Manatee 2025X R1, enhancing electromagnetic simulation performance by reducing magnetic calculation time by up to 50% while improving data integration and simulation accuracy for advanced engineering applications.

The Engineering Simulation Software Market Report provides a comprehensive analysis of key market segments, including type, application, end-user, and regional insights. The report covers simulation technologies such as finite element analysis, computational fluid dynamics, and multiphysics simulation, offering detailed insights into their adoption across industries. Applications analyzed include automotive, aerospace, industrial manufacturing, electronics, and energy sectors, which collectively account for over 80% of simulation usage globally.

Geographically, the report examines major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional adoption patterns and industrial trends. The scope includes evaluation of enterprise adoption rates, with over 60% of large organizations integrating simulation tools into their workflows. Additionally, the report explores emerging technologies such as AI-driven simulation, cloud-based platforms, and digital twins, which are transforming engineering processes.

The report also provides insights into competitive dynamics, profiling key market players and their strategic initiatives. It includes analysis of technological advancements, regulatory influences, and industry-specific requirements. Furthermore, the scope extends to niche segments such as real-time simulation and AR/VR integration, offering a holistic view of the market landscape. This comprehensive coverage enables decision-makers to understand market trends, identify growth opportunities, and develop strategic initiatives effectively.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,658.0 Million |

| Market Revenue (2033) | USD 7,066.1 Million |

| CAGR (2026–2033) | 13.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens Digital Industries Software; ANSYS Inc.; Dassault Systèmes; Altair Engineering Inc.; Autodesk Inc.; COMSOL Inc.; Hexagon AB; Bentley Systems Incorporated; PTC Inc.; ESI Group; MSC Software Corporation; SimScale GmbH; MathWorks Inc.; Siemens EDA |

| Customization & Pricing | Available on Request (10% Customization Free) |