Reports

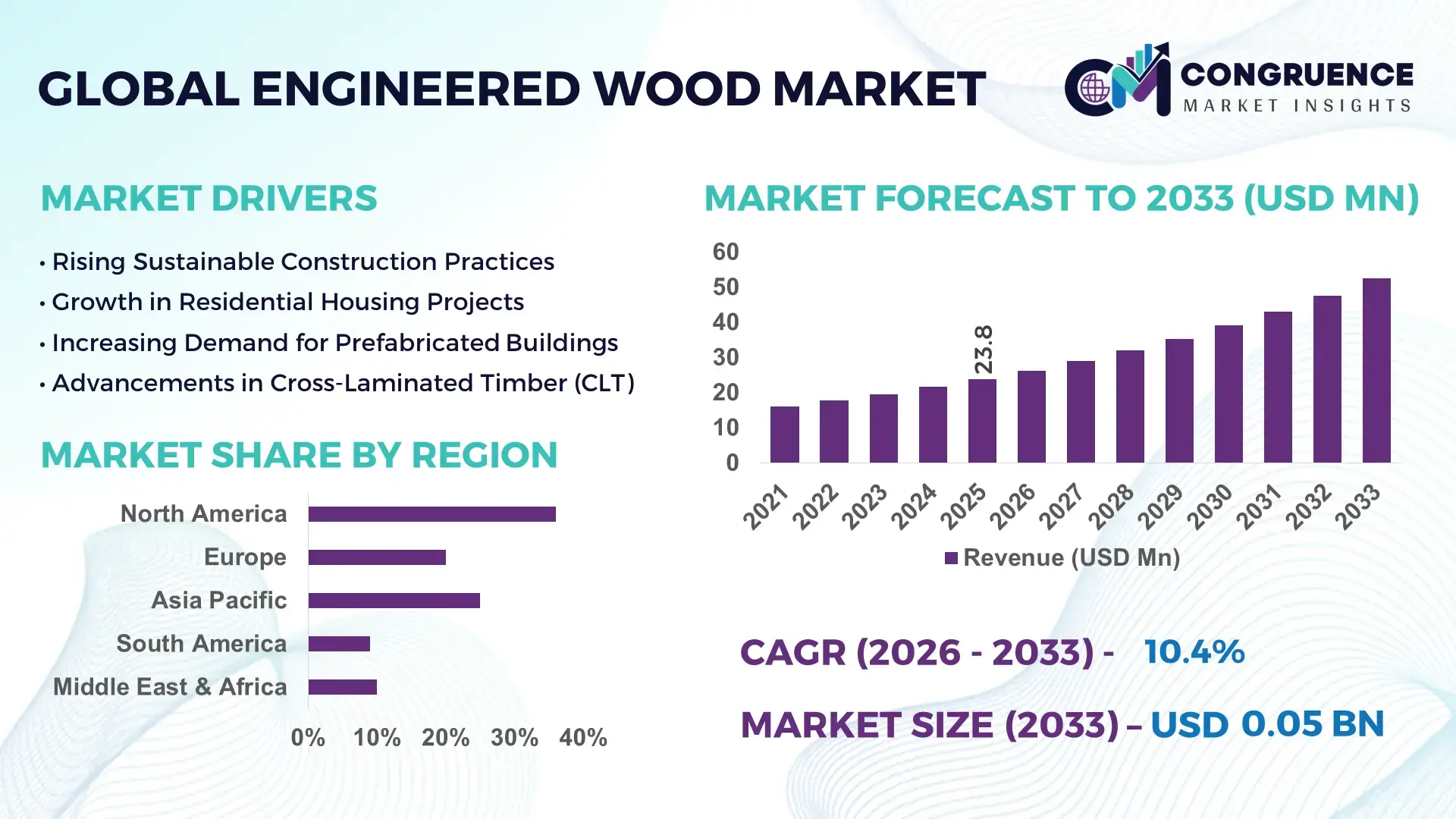

The Global Engineered Wood Market was valued at USD 23.8 Million in 2025 and is anticipated to reach a value of USD 52.52 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. Accelerating demand for sustainable construction materials and high-performance structural wood products is a primary growth catalyst.

The United States remains a dominant force in the engineered wood market, supported by advanced manufacturing infrastructure and large-scale residential and commercial construction activity. The country produces over 13 billion square feet of oriented strand board annually and more than 500 million cubic feet of laminated veneer lumber, reflecting substantial domestic capacity. More than 70% of new single-family homes in the U.S. incorporate engineered wood components such as I-joists, cross-laminated timber, and glulam beams. Investments exceeding USD 1.5 billion in automated mass timber facilities between 2022 and 2025 have strengthened precision fabrication and digital modeling integration. Engineered wood is widely applied in multi-story timber buildings, modular housing, and prefabricated construction, with building codes in over 40 states allowing timber structures up to 18 stories.

Market Size & Growth: Valued at USD 23.8 Million in 2025, projected to reach USD 52.52 Million by 2033 at 10.4% CAGR, driven by rapid urbanization and green building adoption.

Top Growth Drivers: 35% increase in mass timber construction adoption, 28% rise in modular housing demand, 22% improvement in material efficiency over traditional lumber.

Short-Term Forecast: By 2028, digital prefabrication integration is expected to reduce on-site construction waste by 18%.

Emerging Technologies: Cross-laminated timber (CLT), AI-driven structural design software, and low-emission bio-based adhesives.

Regional Leaders: North America projected at USD 18 Million by 2033 with strong residential demand; Europe at USD 15 Million driven by green building mandates; Asia-Pacific at USD 12 Million supported by urban infrastructure expansion.

Consumer/End-User Trends: Residential builders account for over 60% usage, with growing adoption in mid-rise commercial buildings and educational infrastructure.

Pilot Example: In 2024, a Scandinavian timber housing project achieved 25% faster build time using prefabricated CLT panels.

Competitive Landscape: Weyerhaeuser holds approximately 14% share, followed by Stora Enso, West Fraser, Boise Cascade, and UPM-Kymmene.

Regulatory & ESG Impact: Carbon reduction targets in 30+ countries are promoting timber-based structural systems.

Investment & Funding Patterns: Over USD 3 billion invested globally in mass timber plants and automation upgrades since 2022.

Innovation & Future Outlook: Hybrid timber-steel systems and smart moisture-monitoring sensors are shaping next-generation engineered wood applications.

Engineered wood products such as plywood, laminated veneer lumber, and cross-laminated timber collectively serve residential construction, commercial real estate, industrial packaging, and infrastructure sectors, with residential applications contributing more than half of total consumption. Product innovation focuses on fire-resistant panels, formaldehyde-free adhesives, and enhanced load-bearing composites that improve structural integrity by up to 30% compared to conventional sawn lumber. Environmental regulations promoting low-carbon materials and sustainable forestry certifications are reshaping procurement strategies across Europe and North America. Asia-Pacific is witnessing rapid growth in engineered wood flooring and modular housing systems due to expanding urban populations. Increasing preference for prefabricated construction, circular economy practices, and carbon-sequestering materials positions engineered wood as a high-performance, climate-aligned alternative for modern construction ecosystems.

The engineered wood market holds strategic relevance within the global construction and infrastructure ecosystem due to its measurable environmental advantages and structural performance capabilities. Advanced cross-laminated timber technology delivers 20% higher load-bearing efficiency compared to traditional reinforced concrete in mid-rise structures, while reducing embodied carbon emissions by nearly 40%. This performance advantage is influencing procurement decisions among large-scale developers seeking cost-effective and low-carbon building materials.

North America dominates in volume due to established forestry supply chains and widespread residential construction, while Europe leads in adoption with nearly 45% of large construction enterprises integrating mass timber systems into new commercial developments. Asia-Pacific is rapidly expanding manufacturing capacity, supported by government-backed smart city initiatives and modular housing programs.

By 2028, AI-enabled Building Information Modeling integrated with engineered wood prefabrication is expected to improve construction productivity by 15% and reduce material wastage by 12%. Firms are committing to ESG targets, including 50% recycled wood fiber utilization and 30% reduction in volatile organic compound emissions by 2030.

In 2024, Sweden achieved a 22% reduction in construction time for multi-family timber housing projects through digital fabrication and automated panel assembly. Such measurable outcomes highlight operational efficiencies and carbon mitigation benefits. As regulatory frameworks increasingly prioritize sustainable materials, the engineered wood market is positioned as a pillar of structural resilience, environmental compliance, and long-term sustainable growth within the global built environment.

Global construction accounts for nearly 37% of carbon emissions, prompting developers to adopt low-carbon alternatives such as engineered wood. Cross-laminated timber structures can store approximately 1 ton of CO₂ per cubic meter, significantly enhancing their sustainability profile. More than 30 countries have introduced green building certifications encouraging timber-based designs. In North America, over 1,700 mass timber projects were underway by 2025, reflecting rapid adoption. The ability of engineered wood to reduce foundation load by up to 25% compared to concrete further enhances cost efficiency in high-density urban projects. These structural, environmental, and operational benefits collectively accelerate market expansion.

Engineered wood manufacturing depends heavily on softwood lumber supply, which experiences price fluctuations exceeding 20% annually due to logging restrictions, climate-related disruptions, and trade policies. Rising energy and resin costs increase production expenses, impacting profit margins for manufacturers. Transportation expenses have risen by nearly 15% in certain export corridors, affecting global competitiveness. Additionally, inconsistent supply of certified sustainable timber can delay project timelines. Such cost uncertainties reduce pricing predictability for builders and developers, temporarily limiting adoption in price-sensitive markets despite long-term sustainability advantages.

Modular construction is projected to account for nearly 25% of new urban housing developments in advanced economies within the next decade. Engineered wood panels enable 30% faster assembly times compared to conventional site-built systems. Prefabricated CLT modules reduce on-site labor requirements by 20% and minimize material waste by up to 15%. Emerging economies investing in affordable housing and disaster-resilient infrastructure present untapped demand potential. Integration with smart building systems and moisture-sensing technologies also enhances lifecycle performance, opening opportunities in institutional and healthcare construction projects.

Despite code advancements, fire resistance concerns remain a barrier in certain regions. Regulatory approvals for multi-story timber structures can extend project timelines by 6 to 12 months. Compliance with evolving fire testing standards requires additional investment in product certification and performance validation. Insurance premiums for high-rise timber buildings can be 10% higher in conservative markets due to perceived risk. Addressing these regulatory and perception challenges demands continuous innovation in fire-retardant treatments, performance testing, and stakeholder education to sustain long-term engineered wood market expansion.

• 55% Cost Optimization Through Modular and Prefabricated Construction: The rapid adoption of modular construction is significantly reshaping demand patterns in the engineered wood market. Approximately 55% of newly initiated urban housing and commercial projects report measurable cost efficiencies through prefabricated building practices. Pre-cut cross-laminated timber (CLT) panels and laminated veneer lumber components are manufactured off-site using CNC-controlled automated systems, reducing on-site labor requirements by nearly 30% and compressing project timelines by 20%. In North America and Europe, over 40% of mid-rise residential projects now integrate prefabricated timber modules, increasing demand for precision-engineered structural wood panels and high-capacity pressing lines.

• 40% Carbon Reduction Targets Driving Mass Timber Adoption: Engineered wood solutions are gaining traction due to their carbon sequestration potential and low embodied emissions. A cubic meter of structural timber can store close to 1 ton of CO₂, supporting corporate decarbonization goals. Nearly 60% of large real estate developers in Europe have incorporated timber-based structural materials into sustainability roadmaps targeting 40% emission reductions by 2030. Green building certifications have increased engineered wood specifications by 25% in institutional and mixed-use projects, accelerating structural timber integration in climate-focused construction strategies.

• 30% Productivity Gains via Digital Fabrication and BIM Integration: Advanced Building Information Modeling integration with engineered wood manufacturing has improved fabrication precision by up to 30%. AI-enabled design tools optimize load distribution and material utilization, reducing raw material waste by 12% to 18%. Automated glulam beam assembly lines have enhanced output consistency, cutting defect rates below 3%. Digital twin simulations are now deployed in more than 35% of large-scale timber projects, improving coordination and reducing structural design errors.

• 22% Growth in Fire-Resistant and High-Performance Panels: Fire-resistant engineered wood panels and enhanced adhesive systems are expanding application scope in multi-story buildings. Advanced intumescent coatings and fire-rated CLT assemblies can withstand fire exposure for over 120 minutes, meeting updated building standards in more than 30 countries. Demand for high-strength laminated beams has increased by 22% as urban projects exceed 10 to 18 stories. Structural testing improvements have increased load-bearing capacity by 15% compared to earlier-generation timber composites, broadening adoption in commercial infrastructure.

The engineered wood market segmentation reflects diversified product formats, expanding construction applications, and varied end-user demand profiles. By type, cross-laminated timber, plywood, laminated veneer lumber, oriented strand board, and glulam beams form the core structural categories, each serving distinct load-bearing and design functions. Applications are primarily concentrated in residential construction, commercial infrastructure, industrial packaging, and institutional buildings. Residential use accounts for a significant portion due to strong housing demand and modular construction adoption. End-user insights indicate dominance of real estate developers and large construction contractors, followed by industrial manufacturers and infrastructure agencies. Increasing specification of fire-rated timber systems and precision-prefabricated modules is altering procurement patterns, while sustainable forestry certifications and low-emission adhesive standards influence purchasing decisions across global markets.

Cross-laminated timber (CLT), plywood, laminated veneer lumber (LVL), oriented strand board (OSB), and glued laminated timber (glulam) represent the primary engineered wood product categories. Plywood currently accounts for approximately 38% of total product adoption due to its versatility in flooring, roofing, and wall sheathing. Oriented strand board follows with nearly 27% share, driven by its cost-effective structural performance in residential construction. In comparison, cross-laminated timber represents about 18% of usage but is expanding rapidly in mid-rise and high-rise applications. Cross-laminated timber is the fastest-growing segment, advancing at an estimated 12.8% CAGR, fueled by mass timber construction and regulatory approvals for buildings up to 18 stories. CLT panels provide 20% higher dimensional stability compared to traditional framing systems. Laminated veneer lumber and glulam collectively contribute around 17% of the remaining market, primarily used in beams, headers, and heavy-load applications.

Residential construction leads engineered wood applications, accounting for nearly 52% of overall demand, supported by strong single-family housing starts and modular home integration. Commercial construction contributes approximately 28%, particularly in office buildings, retail centers, and educational facilities adopting sustainable building materials. Industrial packaging and infrastructure projects represent the remaining 20%, including pallets, bridges, and transit hubs. While residential remains dominant, commercial multi-story timber construction is the fastest-growing application, expanding at an estimated 11.6% CAGR. The rise of green-certified office developments and mixed-use complexes is accelerating specification of CLT and glulam beams. Residential sheathing applications currently account for over half of plywood and OSB consumption, whereas heavy structural beams are increasingly deployed in commercial atriums and transit terminals.

Real estate developers and large construction contractors constitute the leading end-user segment, contributing approximately 48% of total engineered wood consumption due to their role in residential and commercial building execution. Infrastructure authorities and government agencies account for around 22%, particularly in public housing, transport terminals, and educational facilities. Industrial manufacturers represent 15%, focusing on packaging and material handling applications. The remaining 15% includes architects, modular construction firms, and specialty builders. Although developers lead in total usage, modular construction firms are the fastest-growing end-user group, advancing at nearly 13.2% CAGR as off-site prefabrication scales globally. Adoption among modular builders has increased by 30% in the past three years, driven by demand for rapid, cost-efficient housing solutions. Over 45% of large architectural firms now specify mass timber in sustainable design projects.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.9% between 2026 and 2033.

North America’s dominance is supported by more than 13 billion square feet of annual oriented strand board production and over 500 million cubic feet of laminated veneer lumber output. Europe follows with approximately 30% market share, driven by strong green building regulations and over 1,500 active mass timber construction projects. Asia-Pacific holds close to 24% share, supported by rapid urbanization across China and India, where annual housing completions exceed 20 million units combined. South America represents nearly 6% of global consumption, with Brazil contributing over 60% of regional demand. The Middle East & Africa accounts for approximately 4%, with the UAE and South Africa leading engineered timber imports for commercial developments exceeding 10 million square meters annually. Regional consumption patterns show that more than 65% of engineered wood demand globally originates from residential and mid-rise commercial construction.

How Is Advanced Timber Construction Transforming Structural Building Demand?

North America holds approximately 36% of the global engineered wood market volume, driven by residential construction, commercial real estate, and infrastructure modernization. The United States accounts for nearly 85% of regional demand, with over 70% of new single-family homes incorporating plywood, OSB, or I-joists. Canada contributes significantly through mass timber exports exceeding 2 million cubic meters annually. Government support includes building code approvals permitting timber structures up to 18 stories across more than 40 jurisdictions. Digital fabrication adoption has increased by 28% in large-scale timber plants, enhancing production precision and reducing defects below 3%. Weyerhaeuser continues expanding high-performance OSB capacity by upgrading automated manufacturing lines, strengthening domestic supply chains. Consumer behavior in this region favors sustainable housing, with nearly 60% of developers prioritizing certified timber materials in procurement strategies.

Is Sustainable Construction Policy Accelerating Timber Innovation and Adoption?

Europe represents around 30% of global engineered wood consumption, with Germany, the United Kingdom, and France collectively accounting for over 55% of regional demand. Germany alone records more than 25% of Europe’s mass timber projects, while the UK has seen a 35% increase in multi-story timber approvals since 2022. Strict carbon reduction mandates require new buildings to lower embodied emissions by up to 40%, accelerating cross-laminated timber integration. Advanced robotic panel assembly and digital BIM integration are implemented in nearly 45% of large timber manufacturing facilities. Stora Enso has expanded CLT production capacity by over 100,000 cubic meters annually to meet institutional building demand. Regional consumer behavior is shaped by regulatory pressure, with over 65% of commercial developers specifying low-emission, certified engineered wood products in public infrastructure projects.

Can Rapid Urbanization and Smart Manufacturing Scale Structural Timber Adoption?

Asia-Pacific holds nearly 24% of global engineered wood market share and ranks as the fastest-growing regional market. China leads regional consumption with more than 40% share, followed by Japan at 18% and India at 15%. Urban housing completions in China exceed 15 million units annually, creating strong demand for plywood and LVL panels. Japan remains a global innovation hub for earthquake-resistant glulam beams, with over 50% of new low-rise homes incorporating engineered timber components. Smart manufacturing investments in automated pressing lines have increased regional production capacity by 20% over the past three years. West Fraser has expanded export-oriented OSB production to serve Asia-Pacific markets. Consumer behavior reflects rising preference for prefabricated housing, with modular construction adoption increasing by 30% across urban centers.

How Are Infrastructure Investments Stimulating Structural Wood Demand?

South America accounts for approximately 6% of the global engineered wood market, with Brazil contributing nearly 60% of regional consumption and Argentina around 15%. Infrastructure development programs exceeding 5,000 public housing units annually are boosting plywood and OSB usage. Brazil’s plantation forests cover more than 9 million hectares, ensuring consistent raw material supply for engineered wood production. Export-oriented policies have increased cross-border timber shipments by 18% within Latin America. Arauco has expanded laminated veneer lumber production capacity by modernizing drying kilns and automated grading systems. Consumer behavior across the region shows growing adoption of engineered wood in mid-income housing projects, where material efficiency improvements of 20% support cost-sensitive construction.

Is Rapid Urban Development Increasing Demand for High-Performance Timber Systems?

The Middle East & Africa region represents roughly 4% of the global engineered wood market, with the UAE and Saudi Arabia accounting for over 50% of regional imports. Large-scale commercial developments exceeding 8 million square meters annually are integrating laminated beams and fire-rated CLT panels. South Africa leads sub-Saharan demand, contributing nearly 30% of regional consumption. Technological modernization includes adoption of automated panel cutting systems, improving precision by 25%. Trade partnerships have reduced import tariffs on certified timber products by 10% in select Gulf markets. Regional consumer behavior is influenced by premium commercial and hospitality projects, where over 40% of new sustainable developments specify engineered wood components for aesthetic and structural performance.

United States – 32% market share: The Engineered Wood market in the United States leads due to high production capacity exceeding 13 billion square feet of OSB annually and strong residential construction demand.

Germany – 14% market share: The Engineered Wood market in Germany dominates in Europe due to advanced mass timber engineering, strict sustainability regulations, and over 25% share of regional timber building projects.

The engineered wood market exhibits a moderately consolidated structure, with the top five companies collectively controlling approximately 48% of global production capacity. More than 120 active manufacturers operate worldwide, ranging from integrated forestry conglomerates to specialized mass timber producers. Competitive positioning is shaped by vertical integration strategies, including ownership of plantation forests and in-house adhesive manufacturing. Strategic initiatives between 2022 and 2025 include over 15 production capacity expansions, 10 cross-border partnerships, and multiple automation upgrades improving output efficiency by up to 25%.

Product innovation remains central to competition, with fire-resistant CLT, high-load LVL beams, and formaldehyde-free adhesive systems gaining traction. Automation investments exceeding USD 3 billion globally have enhanced digital fabrication and robotic assembly capabilities. Market leaders emphasize sustainable forestry certification, with over 70% of top-tier production facilities holding internationally recognized environmental credentials. Competitive intensity is further driven by regional players expanding export operations, while leading firms prioritize R&D spending representing approximately 4% to 6% of operational budgets to strengthen high-performance structural wood portfolios.

Weyerhaeuser

Stora Enso

West Fraser Timber Co. Ltd.

Boise Cascade Company

UPM-Kymmene Corporation

Arauco

Norbord Inc.

Louisiana-Pacific Corporation

Binderholz GmbH

Metsä Wood

Advanced manufacturing technologies are significantly reshaping the engineered wood market, enhancing structural performance, sustainability, and production efficiency. Cross-laminated timber (CLT) and laminated veneer lumber (LVL) production now widely incorporate computer numerical control (CNC) machining systems capable of cutting panels with tolerances below 2 millimeters, improving assembly precision by nearly 30% compared to conventional sawing processes. Automated pressing lines equipped with high-frequency curing systems reduce adhesive curing time by up to 40%, increasing throughput capacity in large-scale plants.

Bio-based and ultra-low-emission adhesive technologies are gaining traction, with formaldehyde emissions reduced by over 70% in next-generation resin formulations. Polyurethane and lignin-based binders are being integrated into oriented strand board (OSB) and plywood production, aligning with tightening indoor air quality standards. Fire-performance innovation has also advanced, as intumescent coating systems and char-layer engineering allow CLT panels to achieve fire resistance ratings exceeding 120 minutes, enabling approval for timber buildings up to 18 stories in several jurisdictions.

Digital integration through Building Information Modeling (BIM) and digital twin simulations supports real-time load analysis and structural optimization, reducing material waste by 12% to 18%. Nearly 35% of large engineered wood facilities globally have adopted automated grading systems using AI-enabled visual scanners that detect defects with over 95% accuracy. Moisture-monitoring sensors embedded in glulam beams provide lifecycle data, improving maintenance planning and extending service life by up to 15%. Collectively, these technological advancements are strengthening engineered wood as a high-performance, climate-aligned structural solution for modern construction ecosystems.

• In February 2025, Stora Enso announced the start-up of its expanded cross-laminated timber production line at its Ždírec facility in the Czech Republic, increasing annual CLT capacity by approximately 100,000 cubic meters to meet growing European demand for mass timber construction. Source: www.storaenso.com

• In April 2024, West Fraser Timber Co. Ltd. completed the acquisition of Spruce Products Ltd. in Alberta, adding about 140 million board feet of annual lumber capacity and strengthening its engineered wood and value-added wood products portfolio in North America.

• In May 2024, Weyerhaeuser began operations at its new TimberStrand® laminated veneer lumber facility in Arkansas, designed to produce high-strength LVL beams and headers, increasing engineered wood production capacity in the U.S. South. Source: www.weyerhaeuser.com

• In March 2025, UPM-Kymmene Corporation advanced its wood-based materials strategy by expanding its plywood production line in Finland, improving processing efficiency and enhancing output of high-performance birch plywood panels for industrial and construction applications. Source: www.upm.com

The Engineered Wood Market Report provides a comprehensive evaluation of structural wood products including cross-laminated timber, laminated veneer lumber, oriented strand board, plywood, and glued laminated timber. The scope encompasses analysis of residential, commercial, industrial, and institutional construction applications, which collectively account for more than 65% of engineered wood utilization globally. The report assesses material performance parameters such as load-bearing strength, fire resistance ratings exceeding 120 minutes, and emission compliance aligned with low-VOC standards.

Geographically, the study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing over 95% of global production and consumption activity. It evaluates regional production capacities exceeding 20 million cubic meters annually in leading markets and examines trade flows, plantation forest availability exceeding 9 million hectares in select regions, and infrastructure investments driving timber adoption.

Technological coverage includes digital fabrication systems, AI-based defect detection with 95% accuracy rates, bio-based adhesive development, and automated panel assembly lines improving throughput by up to 25%. The report further explores emerging segments such as hybrid timber-steel construction systems, modular prefabrication integration reducing build time by 20%, and smart moisture-monitoring innovations enhancing structural longevity. This structured scope enables stakeholders to assess product positioning, competitive intensity, operational efficiency benchmarks, and long-term structural material transition trends within the engineered wood industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Weyerhaeuser, Stora Enso, West Fraser Timber Co. Ltd., Boise Cascade Company, UPM-Kymmene Corporation, Arauco, Norbord Inc., Louisiana-Pacific Corporation, Binderholz GmbH, Metsä Wood |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |