Reports

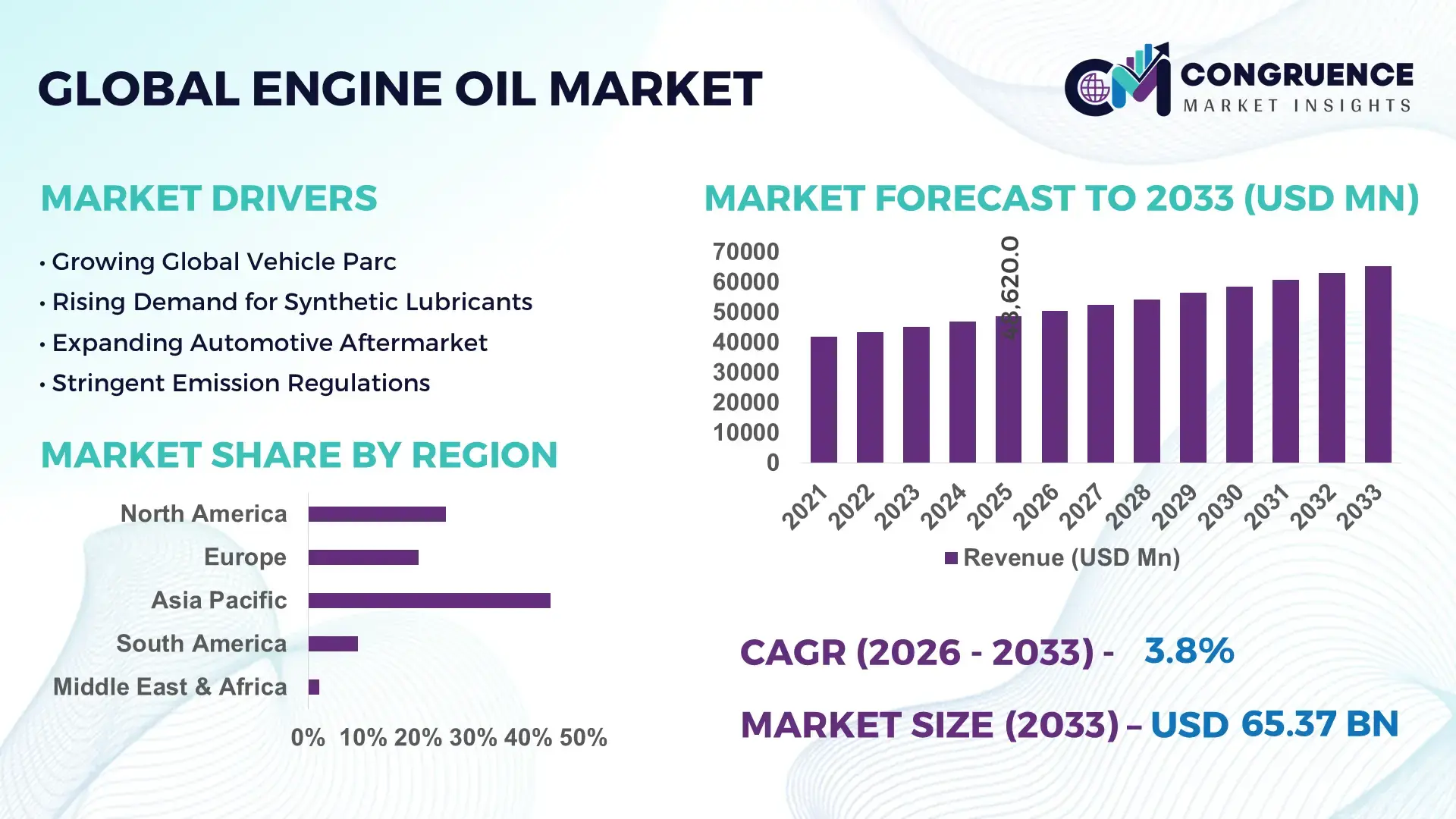

The Global Engine Oil Market was valued at USD 48620 Million in 2025 and is anticipated to reach a value of USD 65371.656254658 Million by 2033 expanding at a CAGR of 3.77% between 2026 and 2033. Rising global vehicle parc expansion, increasing industrialization, and the growing penetration of high-performance lubricants are key factors sustaining long-term demand for advanced engine oil formulations.

China stands as the dominant country in the global engine oil industry, supported by large-scale automotive production exceeding 30 million vehicles annually and extensive commercial fleet operations. The country’s installed lubricant blending capacity surpasses 12 million metric tons per year, backed by continuous investments in synthetic and semi-synthetic engine oil facilities. Heavy-duty trucking, construction machinery, marine engines, and passenger vehicles collectively drive domestic consumption above 8 million metric tons annually. Over 45% of new passenger vehicles in tier-one cities utilize fully synthetic engine oils, reflecting strong consumer adoption of premium lubricants. Furthermore, automation in blending plants and AI-enabled quality control systems have reduced batch inconsistencies by nearly 18%, enhancing supply chain efficiency and product reliability across OEM and aftermarket channels.

Market Size & Growth: USD 48,620 Million in 2025 projected to reach USD 65,371.656254658 Million by 2033 at 3.77% CAGR, driven by expanding vehicle fleet and demand for fuel-efficient lubricants.

Top Growth Drivers: 22% increase in synthetic oil adoption, 18% improvement in engine efficiency standards, 15% growth in commercial vehicle fleet utilization.

Short-Term Forecast: By 2028, advanced additive technologies are expected to improve engine cleanliness by 12% and reduce maintenance frequency by 10%.

Emerging Technologies: Nano-additive formulations, bio-based synthetic blends, and AI-powered lubricant monitoring systems.

Regional Leaders: Asia-Pacific projected to reach USD 28,000 Million by 2033 with strong two-wheeler demand; North America to exceed USD 15,000 Million driven by synthetic oil adoption; Europe to cross USD 12,000 Million with strict emission compliance trends.

Consumer/End-User Trends: Passenger vehicles contribute over 55% of demand, followed by commercial fleets and industrial engines emphasizing extended drain intervals.

Pilot Example: In 2024, a fleet digitization program in Germany reduced engine downtime by 14% through predictive oil monitoring.

Competitive Landscape: Shell holds approximately 12% share, followed by ExxonMobil, BP, TotalEnergies, and Chevron.

Regulatory & ESG Impact: Euro 7 and low-emission standards accelerating low-viscosity lubricant adoption; 20% reduction targets in lifecycle emissions by 2030.

Investment Patterns: Over USD 2.5 Billion invested globally in synthetic base oil upgrades and blending automation between 2023–2025.

Innovation & Outlook: Integration of smart sensors, extended-drain fully synthetic oils, and circular lubricant recycling initiatives shaping next-generation engine oil demand.

The engine oil market serves passenger vehicles, heavy commercial vehicles, off-highway equipment, marine engines, and power generation sectors, with passenger and light commercial vehicles accounting for over half of global lubricant consumption. Recent innovations include low-viscosity SAE 0W-16 and 0W-8 formulations improving fuel economy by up to 3%, alongside advanced detergent-dispersant additive packages enhancing sludge control by nearly 20%. Environmental regulations promoting lower sulfur and phosphorus content are reshaping product portfolios, while economic growth in Asia-Pacific continues to drive high-volume consumption. Electrification trends are encouraging the development of hybrid-compatible lubricants and thermal management fluids, reinforcing future-ready product diversification for automotive OEMs and industrial operators.

The engine oil market holds strategic relevance as a critical enabler of automotive efficiency, industrial reliability, and emission compliance. With global vehicle population surpassing 1.5 billion units, demand for high-performance engine lubricants remains structurally resilient despite electrification shifts. Synthetic engine oil technology delivers 25% longer drain intervals compared to conventional mineral oil standards, significantly reducing lifecycle maintenance costs for fleet operators. Asia-Pacific dominates in volume due to large automotive production bases, while North America leads in premium adoption with nearly 65% of passenger vehicles using synthetic or semi-synthetic oils.

By 2028, AI-powered predictive oil diagnostics integrated with telematics systems are expected to reduce unplanned engine failures by 15% across commercial fleets. ESG commitments are intensifying, with lubricant manufacturers targeting 30% recycled base oil utilization and 25% carbon intensity reduction by 2030. In 2024, a major U.S. fleet operator achieved a 13% fuel efficiency improvement through adoption of ultra-low-viscosity synthetic engine oil combined with digital oil monitoring systems.

Strategically, companies are diversifying portfolios toward hybrid engine fluids, bio-based lubricants, and circular recycling ecosystems to mitigate regulatory risk and supply volatility. As emission standards tighten and vehicle technologies evolve, the Engine Oil Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable industrial growth across global transportation and heavy equipment sectors.

Global vehicle ownership has surpassed 1.5 billion units, with annual new registrations exceeding 90 million vehicles worldwide. Each internal combustion engine vehicle requires periodic lubrication, creating recurring demand cycles. In emerging economies, two-wheeler ownership growth above 8% annually significantly increases lubricant consumption volumes. Commercial transportation activity, particularly in logistics and e-commerce, has increased heavy-duty truck utilization rates by nearly 12%, driving higher engine oil replacement frequency. Additionally, stricter fuel economy standards are promoting low-viscosity engine oils that enhance mechanical efficiency by up to 3%, encouraging rapid product upgrades across OEM and aftermarket channels.

Battery electric vehicles eliminate the need for traditional engine oil, directly impacting long-term lubricant demand. Global electric vehicle sales exceeded 14 million units recently, accounting for approximately 18% of new car sales. As EV penetration increases, especially in Europe and China, internal combustion engine vehicle growth moderates. Moreover, improved engine durability and extended oil drain intervals reduce overall replacement frequency by up to 20% compared to older engines. These structural changes constrain volume expansion in mature automotive markets and require lubricant manufacturers to diversify into EV thermal fluids and hybrid-compatible lubricants.

Synthetic engine oils provide 30% better oxidation stability and 20% improved temperature resistance compared to conventional mineral oils, creating strong premiumization opportunities. Bio-based lubricants derived from renewable feedstocks are gaining traction due to lower carbon footprints and improved biodegradability. Government mandates targeting 25% lifecycle emission reductions by 2030 are accelerating research investments in sustainable base oils. Fleet operators adopting fully synthetic lubricants report maintenance cost reductions of 10–15% annually due to extended drain intervals. Additionally, emerging markets in Southeast Asia and Africa offer high-growth potential as vehicle penetration continues to rise alongside infrastructure expansion.

Base oil prices are closely linked to crude oil fluctuations, which can vary by more than 20% annually, directly impacting production costs. Additive components such as zinc dialkyldithiophosphate (ZDDP) face tightening environmental scrutiny due to phosphorus content restrictions. Compliance with Euro 7 and similar emission standards requires costly reformulation and advanced testing procedures. Small and mid-sized blending companies often face capital constraints when upgrading facilities for automated blending and digital quality monitoring systems. Additionally, counterfeit and low-quality lubricants in developing regions undermine brand reputation and reduce formal sector sales by an estimated 5–8%, creating persistent operational and regulatory complexities.

• Synthetic Lubricants Surpass 40% of Passenger Vehicle Usage Globally: Fully synthetic and semi-synthetic engine oils now account for over 40% of global passenger vehicle lubricant consumption, compared to less than 30% a decade ago. In North America, nearly 65% of new passenger cars use SAE 0W-20 or lower viscosity grades to meet fuel efficiency standards. Extended drain intervals of up to 15,000–20,000 kilometers are increasingly common, reducing maintenance frequency by nearly 18%. This measurable shift toward premium formulations is reshaping blending operations, additive demand, and OEM service-fill strategies worldwide.

• Expansion of Low-Viscosity and Fuel-Efficient Grades Improving Engine Performance by 3–4%: Low-viscosity engine oils such as SAE 0W-16 and 0W-8 are witnessing adoption growth exceeding 20% annually in developed automotive markets. Automakers report fuel economy improvements of 3–4% when switching from traditional 10W-30 grades to advanced low-friction lubricants. Over 55% of new vehicles launched in Japan and more than 45% in the United States specify ultra-low-viscosity oils as factory fill, accelerating demand for advanced viscosity modifiers and friction-reducing additives.

• Digital Oil Monitoring Systems Reducing Fleet Downtime by 12–15%: Commercial fleet operators are integrating IoT-based lubricant sensors capable of measuring viscosity, contamination, and oxidation in real time. More than 35% of large logistics fleets in Europe have deployed predictive oil analytics platforms, resulting in maintenance cost reductions of 10% and unplanned downtime decreases of up to 15%. These data-driven maintenance strategies are transforming lubricant procurement models from time-based replacement cycles to condition-based optimization frameworks.

• Growth of Re-Refined and Bio-Based Engine Oils Supporting 25% Carbon Intensity Reduction Targets: Sustainability initiatives are accelerating the adoption of re-refined base oils, which can reduce lifecycle greenhouse gas emissions by nearly 25% compared to virgin base stocks. Over 1.2 million metric tons of used lubricants are reprocessed annually in North America and Europe combined. Bio-based engine oil formulations derived from renewable feedstocks are expanding at adoption rates above 12% yearly, particularly among government fleets and environmentally certified industrial operators seeking measurable ESG improvements.

The engine oil market is segmented by type, application, and end-user, reflecting diverse lubrication requirements across automotive and industrial ecosystems. By type, mineral, semi-synthetic, and fully synthetic oils dominate product differentiation, with premium synthetic formulations gaining structural momentum due to longer drain intervals and emission compliance compatibility. In application terms, passenger vehicles represent the largest consumption base, supported by a global vehicle parc exceeding 1.5 billion units, while commercial vehicles and off-highway equipment contribute significantly due to higher oil volume requirements per unit. End-user segmentation highlights OEMs, automotive aftermarket service providers, industrial operators, and fleet managers as key demand clusters. More than 60% of lubricant sales occur through aftermarket distribution channels, underscoring recurring maintenance cycles. Regionally, Asia-Pacific accounts for the highest consumption volumes due to large automotive production bases, while North America leads in premium synthetic adoption rates above 60%.

Mineral engine oil, semi-synthetic engine oil, and fully synthetic engine oil constitute the primary product categories. Mineral engine oil currently accounts for approximately 38% of total global consumption, particularly in cost-sensitive emerging markets and older vehicle segments. Fully synthetic engine oil leads the premium segment with nearly 42% share, driven by superior oxidation stability, up to 30% longer drain intervals, and improved thermal resistance exceeding 250°C operating thresholds. Semi-synthetic oils hold around 20%, serving as a mid-range option balancing cost and performance. While fully synthetic oils dominate advanced automotive markets, semi-synthetic formulations represent the fastest-growing segment with an estimated growth rate of 5.2%, supported by increasing consumer preference for affordable performance upgrades. Collectively, specialty and niche formulations, including racing and heavy-duty diesel oils, contribute the remaining combined 8% share of the total market landscape.

Passenger vehicles represent the leading application segment, accounting for nearly 55% of global engine oil consumption due to widespread private vehicle ownership and standardized service intervals. Commercial vehicles contribute approximately 30%, supported by higher oil sump capacities and intensive mileage cycles. Off-highway equipment, marine engines, and power generation units collectively account for the remaining 15%. Although passenger vehicles dominate overall volume, commercial vehicle applications are expanding at a faster rate of 4.8%, driven by rising logistics demand and freight movement increases above 10% in major trade corridors. Heavy-duty diesel engines require oil replacement volumes that are 2–3 times higher per service cycle compared to passenger cars, amplifying lubricant consumption intensity.

The automotive aftermarket is the leading end-user segment, accounting for approximately 60% of total engine oil demand, reflecting recurring maintenance cycles and independent service networks. OEM factory fill and authorized service networks contribute nearly 25%, while industrial operators and fleet management companies represent the remaining 15%. While the aftermarket remains dominant, fleet management companies constitute the fastest-growing end-user group with an estimated growth rate of 5.6%, fueled by predictive maintenance adoption and digital lubricant monitoring technologies. Over 40% of large fleet operators in Europe and North America have integrated oil condition monitoring systems, enhancing maintenance planning and reducing service-related downtime.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific consumed more than 18 million metric tons of engine oil in 2025, supported by annual vehicle production exceeding 50 million units across China, India, Japan, and South Korea. North America held approximately 24% share, driven by synthetic lubricant penetration above 60% in passenger vehicles and commercial fleet utilization rates exceeding 75%. Europe accounted for nearly 20% share, with over 70% of newly registered vehicles requiring low-viscosity oils compliant with Euro 6 and Euro 7 standards. South America contributed around 6%, while the Middle East & Africa represented close to 4% of total global consumption, supported by expanding construction, mining, and oilfield equipment operations. Regional consumption patterns vary significantly, with Asia-Pacific emphasizing high-volume mineral oils, while North America and Europe demonstrate strong preference for premium synthetic formulations exceeding 65% of total regional demand.

How Are Advanced Synthetic Lubricants Transforming Industrial and Automotive Efficiency?

North America accounts for approximately 24% of global engine oil consumption, with the United States representing over 80% of regional demand. Passenger vehicles and light trucks constitute nearly 58% of total lubricant usage, while commercial trucking and logistics fleets contribute around 30%. Stringent Corporate Average Fuel Economy (CAFE) standards have accelerated adoption of SAE 0W-20 and 0W-16 grades, now specified in more than 65% of new vehicle models. Digital transformation is evident, with over 35% of large fleet operators implementing oil condition monitoring systems to reduce maintenance costs by 10–12%. ExxonMobil has expanded its synthetic lubricant production capacity in the U.S., introducing advanced low-viscosity formulations that improve engine cleanliness by up to 20%. Consumers in this region prioritize extended drain intervals of 15,000 kilometers or more, reflecting higher adoption of premium engine oil solutions in automotive and industrial sectors.

Why Is Regulatory Compliance Accelerating Demand for Low-Emission Lubricants?

Europe represents nearly 20% of the global engine oil market, with Germany, the United Kingdom, and France collectively contributing over 55% of regional consumption. More than 70% of new vehicles sold across the region require low-SAPS (sulfated ash, phosphorus, sulfur) compliant lubricants to meet Euro 6 and Euro 7 emission norms. Sustainability initiatives targeting 30% carbon intensity reduction by 2030 are accelerating demand for re-refined base oils and bio-based blends. Approximately 68% of passenger vehicles in Western Europe use synthetic or semi-synthetic engine oils. TotalEnergies has introduced circular lubricant solutions incorporating up to 50% re-refined base stocks, reducing lifecycle emissions by nearly 25%. Consumers exhibit strong preference for environmentally certified and OEM-approved engine oil products, with over 60% of service centers promoting manufacturer-recommended synthetic formulations.

How Is Expanding Automotive Manufacturing Driving High-Volume Lubricant Consumption?

Asia-Pacific leads global demand with a 46% market share and annual consumption exceeding 18 million metric tons. China, India, and Japan account for more than 75% of regional engine oil usage. China alone produces over 30 million vehicles annually, while India manufactures more than 5 million vehicles per year, sustaining robust lubricant replacement cycles. Infrastructure expansion and construction equipment utilization rates above 70% in urban development zones further drive heavy-duty engine oil demand. Sinopec has invested in automated blending facilities capable of producing over 1 million metric tons annually, integrating AI-based quality control systems that reduce formulation deviations by 15%. Consumers in this region demonstrate mixed behavior: premium synthetic adoption exceeds 45% in urban centers, while mineral oil demand remains strong in rural and cost-sensitive markets.

What Factors Are Strengthening Industrial and Automotive Lubricant Demand?

South America contributes approximately 6% to global engine oil consumption, with Brazil and Argentina accounting for nearly 70% of regional demand. Brazil produces over 2.3 million vehicles annually and maintains a vehicle parc exceeding 45 million units, supporting consistent lubricant replacement cycles. Mining, agriculture, and energy sectors collectively account for 35% of industrial engine oil consumption. Government trade agreements within MERCOSUR facilitate lubricant base oil imports, stabilizing supply chains. Petrobras has expanded its lubricant blending operations, increasing domestic production capacity by 12% to meet heavy-duty diesel demand. Consumers often favor semi-synthetic oils, which account for nearly 40% of regional passenger vehicle lubricant sales, reflecting a balance between cost efficiency and performance reliability.

How Are Energy and Infrastructure Projects Boosting Lubricant Modernization?

The Middle East & Africa region represents close to 4% of global engine oil demand, driven by oil & gas operations, construction megaprojects, and mining activities. The United Arab Emirates and Saudi Arabia together account for over 50% of regional consumption, while South Africa leads demand within sub-Saharan Africa. Construction equipment utilization rates exceed 65% in major infrastructure corridors, increasing heavy-duty engine oil requirements. ADNOC Distribution has expanded its lubricant blending plant capacity by 20%, introducing high-temperature-resistant formulations suitable for desert operating conditions above 45°C. Regulatory modernization and trade partnerships are improving product standardization. Consumers in this region prioritize durability and thermal stability, with over 55% of fleet operators selecting high-viscosity synthetic diesel engine oils for extreme climate performance.

China – 28% share: Engine Oil market leadership driven by annual vehicle production exceeding 30 million units and installed lubricant blending capacity above 12 million metric tons.

United States – 19% share: Engine Oil market strength supported by high synthetic lubricant adoption above 65% and a vehicle parc surpassing 280 million units.

The Engine Oil market is moderately consolidated, with the top five companies collectively accounting for approximately 42% of global share. More than 200 active lubricant manufacturers operate worldwide, ranging from multinational energy corporations to regional blending specialists. Leading players compete through product innovation, OEM approvals, and expanded synthetic base oil capacity. Over USD 2.5 billion has been invested globally between 2023 and 2025 in upgrading Group III and Group IV base oil facilities to support premium synthetic demand. Strategic initiatives include partnerships with automotive OEMs for factory-fill contracts covering over 40% of newly manufactured vehicles. Mergers and acquisitions activity increased by 8% in 2024, particularly in Asia-Pacific, where companies seek localized production capabilities. Digitalization is reshaping competitive dynamics, with more than 30% of large manufacturers integrating AI-driven formulation testing to shorten product development cycles by 15%. Brand positioning increasingly emphasizes sustainability, extended drain intervals, and compliance with evolving emission standards, reinforcing technological differentiation and long-term competitive resilience.

Royal Dutch Shell

ExxonMobil

BP plc

TotalEnergies

Chevron Corporation

Sinopec Lubricant Company

Valvoline Inc.

Fuchs Petrolub SE

Idemitsu Kosan Co., Ltd.

PetroChina Company Limited

Technological innovation in the engine oil market is increasingly centered on advanced base oil chemistry, high-performance additive systems, and digital monitoring integration. Group III and Group IV synthetic base oils now account for more than 45% of new lubricant formulations in developed automotive markets, offering oxidation resistance improvements of up to 30% compared to conventional Group I oils. These advanced base stocks enable extended drain intervals reaching 20,000 kilometers in passenger vehicles and more than 60,000 kilometers in heavy-duty diesel engines under optimized conditions.

Additive technology remains a core differentiator, with modern detergent-dispersant packages improving sludge control by nearly 20% and friction modifiers reducing mechanical wear by up to 15%. Low-SAPS (sulfated ash, phosphorus, sulfur) formulations have become standard for over 70% of new European vehicles to ensure compatibility with diesel particulate filters and catalytic converters. Nanotechnology-based anti-wear additives are being tested in controlled fleet environments, demonstrating up to 8% reduction in friction losses during high-load operations.

Digital transformation is reshaping lubricant lifecycle management. IoT-enabled oil sensors capable of real-time viscosity and contamination monitoring are now deployed in more than 35% of large commercial fleets in North America and Europe. These systems can extend oil change intervals by 10–15% while reducing unexpected engine failures by approximately 12%. Additionally, re-refining technologies have advanced significantly, enabling recovery rates above 80% of used base oils with performance parity to virgin stocks. Automation in blending facilities, supported by AI-driven formulation optimization, has shortened product development cycles by nearly 15%, allowing faster compliance with evolving emission and fuel economy standards.

• In March 2024, Shell plc completed the expansion of its lubricant oil blending plant in Zhuhai, China, increasing annual production capacity by approximately 30% to serve growing demand for premium engine oils across Asia-Pacific. The upgrade enhances automated blending and quality control systems.

• In February 2024, ExxonMobil announced the start-up of its new lubricant manufacturing facility in Maharashtra, India, significantly boosting domestic production capacity to meet rising passenger and commercial vehicle demand. The plant integrates advanced formulation technologies and digital process controls.

• In September 2024, TotalEnergies expanded its re-refining capabilities in France, increasing production of high-quality regenerated base oils used in sustainable engine oil formulations. The initiative supports circular economy targets and reduces lifecycle carbon emissions by up to 25% compared to conventional base oils.

• In January 2025, BP launched a new range of Castrol EDGE engine oils formulated to meet updated OEM specifications for ultra-low-viscosity grades such as 0W-8, delivering improved fuel efficiency performance of up to 3% in compatible engines.

The Engine Oil Market Report provides a comprehensive analysis of product segmentation, application coverage, end-user dynamics, regional performance, and technological evolution across the global lubricant industry. The study evaluates mineral, semi-synthetic, and fully synthetic engine oils, which collectively serve a global vehicle parc exceeding 1.5 billion units. It assesses performance specifications including SAE viscosity grades ranging from 0W-8 to 20W-50, low-SAPS formulations, and heavy-duty diesel engine oils designed for extended drain intervals above 50,000 kilometers.

Geographically, the report covers five primary regions—Asia-Pacific, North America, Europe, South America, and Middle East & Africa—representing 100% of global consumption, with Asia-Pacific accounting for nearly half of total volume demand. Application analysis includes passenger vehicles (approximately 55% of usage), commercial vehicles (around 30%), and off-highway, marine, and power generation segments (about 15%).

The scope further includes evaluation of technological trends such as Group III and IV synthetic base oil adoption, which exceeds 45% in developed markets, integration of IoT-based oil monitoring systems adopted by over 35% of large fleets, and re-refining technologies achieving base oil recovery rates above 80%. Additionally, the report examines regulatory frameworks including Euro 7 compliance requirements, sustainability targets aiming for 25–30% lifecycle emission reductions, and emerging hybrid-compatible lubricant formulations. This structured coverage equips decision-makers with actionable intelligence across product innovation, supply chain optimization, competitive positioning, and long-term strategic planning within the global engine oil ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.77% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Royal Dutch Shell, ExxonMobil, BP plc, TotalEnergies, Chevron Corporation, Sinopec Lubricant Company, Valvoline Inc., Fuchs Petrolub SE, Idemitsu Kosan Co., Ltd., PetroChina Company Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |