Reports

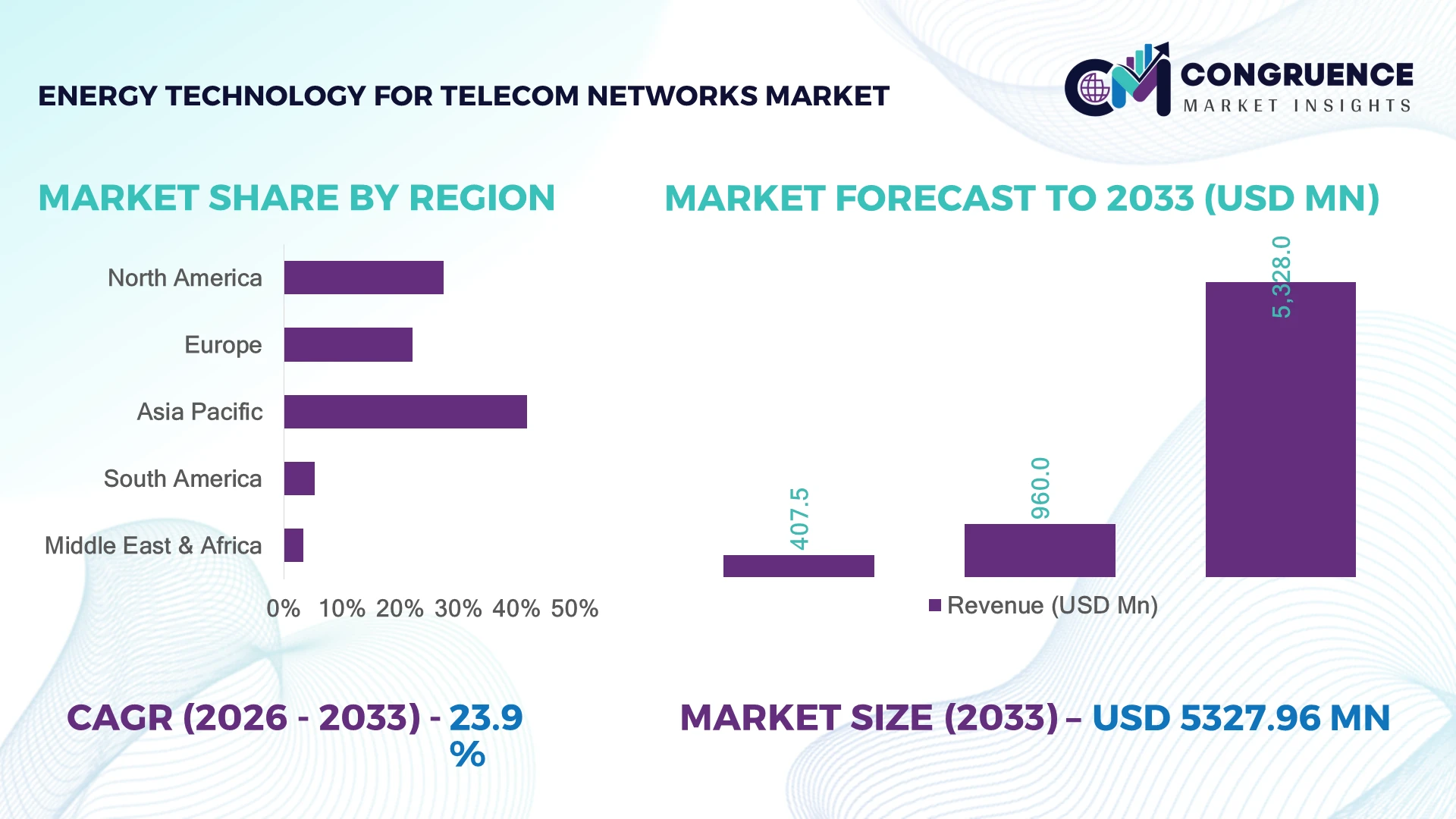

The Global Energy Technology for Telecom Networks Market was valued at USD 960.0 Million in 2025 and is anticipated to reach a value of USD 5,328.0 Million by 2033 expanding at a CAGR of 23.89% between 2026 and 2033. Rapid deployment of 5G infrastructure, expansion of hybrid renewable-powered telecom sites, and rising adoption of intelligent energy management platforms are accelerating investments in advanced telecom network energy technologies.

China leads the global market with an estimated 34% share, supported by deployment across more than 4.4 million 5G base stations, large-scale renewable-powered telecom infrastructure, and sustained grid modernization investments. Compared with India, where rural telecom expansion is advancing rapidly, China demonstrates greater integration of AI-enabled energy optimization and battery storage technologies. Geopolitical emphasis on energy security and resilient communications infrastructure further strengthens nationwide deployment.

Organizations prioritizing scalable, energy-efficient telecom infrastructure and intelligent power management solutions will secure stronger operational resilience and long-term network competitiveness.

Market Size & Growth: USD 960.0 Million (2025) to USD 5,328.0 Million (2033) at 23.89% CAGR, driven by advanced 5G energy infrastructure and renewable integration.

Top Growth Drivers: 5G rollout 42%, renewable-powered telecom sites 35%, AI-enabled energy optimization 28%.

Short-Term Forecast: By 2028, telecom energy costs decline by nearly 18% through intelligent power management and hybrid energy systems.

Emerging Technologies: AI-powered energy analytics, lithium-ion and sodium-ion storage, and digital remote monitoring accelerate high-growth deployments.

Regional Leaders: Asia-Pacific USD 2.1 Billion, North America USD 1.4 Billion, Europe USD 1.0 Billion, each advancing infrastructure modernization and network resilience.

Consumer/End-User Trends: Over 61% of telecom operators prioritize renewable-backed power systems for remote and edge network sites.

Pilot/Case Example: 2025 hybrid solar-battery telecom deployments reduced diesel consumption by approximately 40% at remote base stations.

Competitive Landscape: Top providers hold nearly 48% combined share, led by Huawei, Schneider Electric, Vertiv, Eaton, and Delta Electronics.

Regulatory & ESG Impact: Energy-efficiency initiatives improve telecom power utilization by nearly 20%, supporting lower operational emissions amid infrastructure expansion.

Investment & Funding: More than USD 3.5 Billion supports partnerships, battery storage expansion, and resilient telecom energy infrastructure amid global supply-chain diversification.

Innovation & Future Outlook: AI-driven predictive energy control, modular microgrids, and advanced battery platforms strengthen next-generation telecom network reliability.

The Energy Technology for Telecom Networks Market is expanding as telecom operators modernize power infrastructure for dense 5G deployments, edge computing facilities, and remote communication sites. AI-based energy optimization, hybrid solar-storage systems, and advanced battery technologies are improving network uptime while lowering operational costs. Nearly 30% of newly deployed remote telecom sites now incorporate renewable energy solutions, supported by resilient supply-chain strategies and stricter energy-efficiency requirements, setting the foundation for broader strategic transformation.

The Energy Technology for Telecom Networks Market has become strategically important as telecom operators prioritize resilient, intelligent, and energy-efficient infrastructure to support expanding digital connectivity. Infrastructure modernization, decentralized power systems, and supply-chain diversification are reshaping procurement strategies while reducing dependence on conventional diesel-powered backup solutions. Growing deployment of edge computing and high-density 5G networks is further increasing demand for advanced power management technologies capable of maintaining uninterrupted operations.

Modern hybrid renewable energy systems combined with AI-enabled energy management platforms improve overall power efficiency by approximately 25% compared with conventional diesel-based configurations while reducing maintenance requirements. Asia-Pacific continues to lead large-scale deployment through aggressive telecom infrastructure expansion, whereas North America emphasizes intelligent automation, predictive maintenance, and resilient microgrid integration across mission-critical communication networks. This regional contrast reflects differences in deployment scale and technology maturity.

Telecom providers are increasingly deploying solar-powered base stations integrated with battery energy storage and cloud-based monitoring platforms to improve uptime in remote areas. Companies are expanding strategic partnerships with battery manufacturers, power electronics suppliers, and software providers while accelerating localized production capabilities. Over the next two to three years, wider adoption of intelligent energy orchestration platforms and modular power architectures will strengthen operational resilience, improve network availability, and establish sustainable competitive positioning across the global telecom ecosystem.

Expansion of dense 5G infrastructure and increasing adoption of intelligent power management platforms are fundamentally reshaping telecom energy ecosystems. More than 65% of newly commissioned macro base stations are designed with hybrid energy architectures, while AI-enabled energy optimization lowers power consumption by nearly 20% and predictive maintenance reduces unplanned outages by around 30%. China continues to accelerate renewable-powered telecom deployments as national digital infrastructure programs prioritize resilient communications. This transition is driving demand for modular battery storage, advanced rectifiers, and remote energy monitoring platforms. In response, leading technology providers are expanding manufacturing capacity, forming strategic battery partnerships, and integrating cloud-based energy analytics into telecom power portfolios. The strategic advantage increasingly lies in combining operational efficiency with energy resilience rather than simply expanding network coverage.

Dependence on imported battery materials, semiconductor components, and advanced power electronics continues to constrain deployment timelines and investment efficiency. Lithium battery costs still account for approximately 35% of total remote-site modernization expenditure, while nearly 45% of telecom operators report procurement delays linked to component availability. India and several developing telecom markets remain exposed to imported energy storage technologies despite growing domestic manufacturing initiatives. Rising logistics costs and evolving technical certification requirements further complicate large-scale deployments. Companies are mitigating these pressures through localized manufacturing, long-term procurement agreements, supplier diversification, and standardized modular power platforms. Organizations capable of reducing supply dependency while improving procurement flexibility will achieve stronger cost control and deployment consistency across expanding telecom infrastructure.

Next-generation telecom energy ecosystems are creating opportunities beyond conventional backup power by integrating AI-driven microgrids, digital twins, and distributed renewable generation. Intelligent energy orchestration can improve power utilization by nearly 25%, while hybrid solar-storage installations reduce diesel dependence by approximately 40% at remote telecom locations. India is accelerating rural digital connectivity through renewable-powered telecom infrastructure supported by national clean-energy initiatives and localized manufacturing incentives. Technology vendors are strengthening competitive positioning through software partnerships, battery innovation programs, and integrated energy-as-a-service offerings. A significant strategic opportunity lies in monetizing predictive energy optimization platforms, enabling telecom operators to transform power infrastructure into digitally managed operational assets rather than fixed utility costs.

Long-term scalability depends on seamless integration between legacy telecom equipment, renewable power assets, battery storage systems, and intelligent energy management software. Nearly 38% of operators identify interoperability as a primary deployment challenge, while cybersecurity incidents targeting critical infrastructure have increased by over 20% in recent years, requiring stronger protection for remotely managed energy assets. The United States is strengthening critical infrastructure security requirements, increasing compliance expectations for telecom energy systems. Companies must invest in standardized communication protocols, secure edge computing architectures, workforce development, and interoperable software platforms. Sustainable competitive advantage will depend on delivering unified, cyber-resilient energy ecosystems capable of supporting expanding digital infrastructure without compromising operational reliability.

AI-Powered Energy Optimization Intelligent energy management platforms are becoming standard across telecom networks, with more than 48% of newly deployed telecom power systems incorporating AI-based monitoring and predictive analytics. Automated load balancing has reduced power wastage by nearly 20%, while predictive maintenance lowers emergency site visits by around 30%. Rising electricity costs and stricter energy-efficiency targets are encouraging operators in China and the United States to digitize energy workflows. Companies are expanding software partnerships and integrating cloud-based analytics to improve network availability while reducing operational expenditure.

Hybrid Renewable Power Expansion Telecom operators are accelerating deployment of hybrid solar, wind, and battery-powered sites, particularly in remote locations where grid reliability remains limited. Approximately 36% of newly commissioned off-grid telecom sites now utilize renewable-hybrid energy systems, reducing diesel consumption by nearly 40%. India’s rural connectivity initiatives and continued fuel price volatility are accelerating this transition. Equipment suppliers are scaling modular energy solutions and localized battery production to improve deployment speed and long-term operational resilience.

Advanced Battery Technology Adoption Lithium-ion batteries remain the dominant storage technology, while sodium-ion and solid-state battery development is gaining momentum for telecom applications. Battery replacement cycles have improved by approximately 25%, and energy density has increased by nearly 18% compared with earlier systems. Growing concerns over critical mineral supply are encouraging manufacturers to diversify sourcing strategies and invest in next-generation storage platforms. Companies are strengthening long-term supply agreements and expanding domestic manufacturing to enhance supply security.

Modular Power Infrastructure Deployment Operators are replacing conventional centralized power architectures with modular, scalable energy systems capable of supporting 5G expansion and edge computing facilities. Standardized modular designs have shortened deployment timelines by nearly 22% while reducing maintenance complexity by approximately 17%. Enterprise demand for faster network expansion and evolving infrastructure standards are driving adoption across developed telecom markets. Vendors are restructuring product portfolios toward integrated power cabinets, digital monitoring platforms, and remote diagnostics to improve lifecycle efficiency and service responsiveness.

Renewable Energy represents the largest segment, accounting for an estimated 38.6% of market demand as telecom operators increasingly deploy solar and hybrid renewable systems to reduce operating costs and strengthen network resilience. The segment benefits from lower lifecycle costs, improved energy independence, and compatibility with remote telecom infrastructure. Energy Storage remains a critical complementary technology, ensuring uninterrupted power during grid failures and supporting high-density 5G deployments. Together, these mature technologies form the foundation of modern telecom energy infrastructure. Energy Management Systems are emerging as the fastest-growing segment as operators prioritize AI-driven monitoring, predictive maintenance, and intelligent load optimization. Nearly 45% of newly modernized telecom sites now integrate digital energy management capabilities, while intelligent power optimization improves energy utilization by approximately 20%. The Others segment, including advanced rectifiers and power conversion technologies, continues supporting specialized deployment requirements. Technology providers are expanding software capabilities, investing in integrated hardware platforms, and strengthening partnerships with telecom equipment manufacturers as investment priorities shift toward intelligent, software-defined energy ecosystems.

Base Stations remain the dominant application, representing approximately 60.1% of total deployment as dense 5G rollouts significantly increase power consumption across macro and small-cell networks. Continuous operation requirements, remote location deployments, and higher equipment density are driving investment in resilient power systems incorporating renewable generation, battery storage, and intelligent monitoring. Telecom operators are standardizing modular energy architectures to improve scalability while minimizing operational interruptions. Data Centers are the fastest-growing application as edge computing, cloud-native telecom architecture, and AI-enabled network functions require highly efficient power infrastructure. Around 32% of new telecom edge facilities incorporate advanced energy optimization technologies, while automated power management improves infrastructure utilization by nearly 18%. The Others category includes transmission infrastructure and distributed communication facilities where specialized energy solutions continue expanding. Vendors are increasing deployment automation, integrating remote diagnostics, and developing unified energy platforms that support both centralized and distributed telecom operations.

Telecom Operators account for approximately 54.8% of total market demand due to their direct responsibility for nationwide network deployment, infrastructure modernization, and uninterrupted service delivery. Growing investments in 5G, rural connectivity, and energy-efficient network operations continue strengthening purchasing activity. Tower Companies remain an important customer segment as infrastructure-sharing models expand, encouraging deployment of centralized renewable energy systems and intelligent power management across multiple operator networks. Data Center Operators represent the fastest-growing end-user segment as edge computing infrastructure, network virtualization, and AI-enabled applications increase demand for resilient telecom energy ecosystems. Nearly 35% of newly developed edge facilities now incorporate integrated renewable energy and battery storage solutions to improve uptime and operational efficiency. Companies are responding with customized power architectures, flexible financing models, and ecosystem partnerships that combine hardware, software, and managed services. Competitive differentiation increasingly depends on delivering scalable, intelligent energy platforms capable of supporting next-generation digital infrastructure.

Asia-Pacific accounted for the largest market share at 41.8%in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 25.6%between 2026 and 2033.

North America accounted for approximately 27.4% of the global market in 2025, supported by extensive 5G deployment, edge computing expansion, and modernization of telecom energy infrastructure. Operators are replacing legacy diesel-based backup systems with intelligent battery storage, renewable hybrid solutions, and cloud-connected energy management platforms to improve operational efficiency and network resilience. The United States and Canada continue investing in resilient digital infrastructure while expanding AI-driven predictive maintenance across telecom assets. More than 55% of newly upgraded telecom sites now incorporate intelligent energy monitoring systems, enabling faster fault detection, lower maintenance costs, and improved network availability. Technology vendors are strengthening software integration capabilities and expanding strategic partnerships with telecom infrastructure providers.

United States Market Outlook: The United States remains the largest national market due to its advanced telecom infrastructure, nationwide 5G expansion, and strong presence of leading power technology companies. More than 450,000 cellular sites require continuous power optimization, encouraging rapid deployment of lithium-ion battery systems, remote energy analytics, and hybrid renewable solutions. Federal infrastructure investments and increasing adoption of edge computing continue accelerating modernization projects, while telecom operators collaborate with energy technology providers to improve network resilience and operational sustainability.

Europe represented nearly 22.1% of the global market in 2025 as operators accelerated decarbonization initiatives and energy-efficiency upgrades across telecom infrastructure. Rising electricity prices and stringent sustainability policies have encouraged widespread deployment of renewable-powered base stations, modular battery storage, and intelligent energy management platforms. Telecom companies are increasingly integrating solar energy and remote monitoring technologies to improve operational continuity while reducing carbon emissions. More than 48% of telecom infrastructure modernization projects now include renewable energy integration, reflecting the region's strong commitment to sustainable network operations and digital infrastructure resilience.

Germany Market Outlook: Germany leads the European market through advanced industrial capabilities, strong renewable energy integration, and widespread deployment of intelligent telecom infrastructure. National digital transformation initiatives continue supporting energy-efficient network modernization, while domestic engineering expertise strengthens innovation across battery storage and power electronics. Approximately 60% of newly upgraded telecom sites utilize advanced energy monitoring systems, enabling operators to optimize electricity consumption and enhance long-term operational reliability through intelligent infrastructure management.

Asia-Pacific dominated the global market with approximately 41.8% share in 2025, supported by large-scale telecom infrastructure expansion, extensive manufacturing capabilities, and continuous investment in digital connectivity. China, India, Japan, and South Korea continue deploying renewable-powered telecom sites, intelligent battery systems, and AI-enabled power management technologies to support expanding 5G networks. Regional manufacturers maintain significant production capacity for batteries, power electronics, and telecom energy equipment, strengthening supply-chain competitiveness. More than 65% of newly deployed telecom base stations incorporate high-efficiency energy systems, reflecting strong emphasis on operational performance and infrastructure scalability.

China Market Outlook: China remains the largest individual market owing to its extensive telecom infrastructure, domestic manufacturing ecosystem, and continued investment in digital infrastructure modernization. With more than 4.4 million operational 5G base stations, demand for intelligent power management, advanced battery storage, and renewable energy integration continues expanding rapidly. Local manufacturers benefit from strong supply-chain integration, enabling faster deployment of next-generation telecom energy technologies while supporting national energy security and infrastructure resilience objectives.

South America accounted for approximately 5.3% of the global market in 2025, with telecom operators prioritizing network expansion into underserved and remote communities. Hybrid renewable energy systems are increasingly replacing conventional diesel-powered telecom sites where grid connectivity remains inconsistent. Infrastructure modernization initiatives and growing mobile broadband adoption continue strengthening demand for efficient telecom energy technologies despite logistical and investment constraints. Around 34% of newly deployed remote telecom sites now incorporate solar-powered energy systems, improving network uptime while reducing long-term operating costs. Equipment providers are expanding regional partnerships and localized technical support to strengthen deployment efficiency.

Brazil Market Outlook: Brazil represents the region's largest market due to extensive telecom coverage requirements, expanding rural connectivity programs, and increasing investment in digital infrastructure. Large geographic coverage creates strong demand for autonomous power systems capable of supporting remote communication networks. Telecom operators continue deploying hybrid solar-battery solutions across isolated locations while strengthening infrastructure partnerships to improve operational resilience and reduce dependence on conventional fuel-powered backup systems.

The Middle East & Africa represented approximately 3.4% of the global market in 2025, supported by expanding telecom coverage, increasing renewable energy investments, and infrastructure modernization initiatives. Countries across the Gulf region and Africa are accelerating deployment of off-grid telecom energy systems to improve network reliability in challenging operating environments. Hybrid solar-battery installations are becoming increasingly common as operators reduce diesel dependency and improve energy efficiency. Nearly 40% of newly deployed remote telecom sites utilize renewable-supported energy systems, reflecting growing emphasis on operational resilience and sustainable infrastructure expansion.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through significant digital transformation investments, nationwide 5G deployment, and large-scale renewable energy development. Government-backed infrastructure programs continue encouraging modernization of telecom energy systems using intelligent power management and advanced battery storage technologies. Strategic partnerships between telecom operators and energy technology providers are strengthening localized deployment capabilities while supporting long-term national digital infrastructure and sustainability objectives.

The market is led by global technology providers including Huawei Technologies, Schneider Electric, Eaton, Vertiv, and Delta Electronics, competing against regional power-system specialists and telecom infrastructure suppliers on integrated energy platforms rather than standalone hardware. The top five players collectively account for approximately 53% of the market, reflecting moderate consolidation and strong technology differentiation. Competition centers on energy efficiency, digital power management, and lifecycle operating costs, with advanced rectifier efficiency exceeding 97% and intelligent monitoring reducing maintenance visits by nearly 30%. Global leaders leverage vertically integrated portfolios, while regional suppliers compete through customization, faster deployment, and localized service networks. Companies are expanding manufacturing, strengthening battery partnerships, integrating AI-enabled energy management, and securing long-term telecom operator contracts. The competitive landscape is shifting toward software-defined energy ecosystems and supply-chain localization, increasing pressure on suppliers lacking digital capabilities. High certification requirements, telecom-grade reliability standards, and extensive service networks remain significant entry barriers. Sustainable competitive advantage depends on delivering integrated, intelligent, scalable solutions with proven operational performance.

Schneider Electric SE

Eaton Corporation plc

Vertiv Holdings Co.

Delta Electronics, Inc.

ZTE Corporation

ABB Ltd.

Cummins Inc.

EnerSys

Eltek AS

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

Alpha Technologies Ltd.

NEC Corporation

Artificial intelligence, lithium-ion energy storage, digital power electronics, and cloud-connected energy management platforms are transforming telecom energy infrastructure. AI-enabled predictive maintenance reduces unplanned outages by nearly 30%, while intelligent load optimization improves power utilization by approximately 20%. Around 48% of newly modernized telecom sites now deploy intelligent monitoring systems, allowing operators to automate energy optimization and improve network resilience. Vendors increasingly integrate analytics, battery diagnostics, and remote asset management into unified software platforms that simplify distributed infrastructure management.

Hybrid renewable energy systems are replacing conventional diesel-dependent architectures across remote telecom sites. Compared with legacy power configurations, hybrid solar-battery systems lower fuel consumption by almost 40% while reducing maintenance frequency by nearly 25%. Lithium-ion batteries continue replacing lead-acid technologies because they deliver higher energy density, longer service life, and faster charging performance. Global technology leaders including Huawei, Schneider Electric, Eaton, and Vertiv benefit from integrated hardware-software portfolios, enabling stronger differentiation through intelligent energy orchestration rather than standalone equipment. Advanced modular DC power systems further accelerate deployment across dense 5G networks and edge computing facilities.

Between 2026 and 2028, intelligent microgrids, sodium-ion batteries, digital twins, and edge-based energy orchestration are expected to reshape telecom infrastructure management. Operators adopting these technologies will strengthen operational resilience, reduce lifecycle costs, and improve deployment flexibility. Companies investing early in software-defined energy ecosystems, cybersecurity, and interoperable power platforms will establish stronger competitive positioning as telecom networks become increasingly autonomous and energy intensive.

March 2026 – Huawei Technologies introduced its New-Gen AI-Powered Green Site solution and received Frost & Sullivan's 2025 Global Technology Innovation Leadership Recognition. The platform manages up to 10,000 telecom sites simultaneously, delivers over 95% control precision, and responds in less than 7.5 seconds, enabling operators to improve energy storage utilization while reducing site energy operating costs. Source: www.prnewswire.com

March 2026 – Huawei Technologies was recognized by Frost & Sullivan for innovation in telecom DC power systems, highlighting its cloud-based intelligent energy architecture and grid-supportive distributed power technologies. The solution integrates AI-driven site management and intelligent power coordination, helping telecom operators improve infrastructure resilience and optimize energy efficiency across large-scale communication networks.

January 2025 – Vertiv introduced a new modular power solution designed for telecom operators and edge data centers. The scalable architecture supports rapid capacity expansion while enabling integration with renewable energy sources, allowing operators to improve energy efficiency and reduce operating costs through flexible deployment across distributed telecom infrastructure.

2025 – Schneider Electric continued expanding its electrification and digital energy portfolio, accelerating deployment of AI-enabled energy management, EcoStruxure-based monitoring, and sustainable telecom power infrastructure. The company strengthened its market position through increased investment in digital energy technologies and sustainability-focused innovation, supporting telecom operators pursuing lower-emission, highly resilient network power systems.

This report provides comprehensive coverage of the global Energy Technology for Telecom Networks Market across Renewable Energy, Energy Storage, Energy Management Systems, and Others, evaluating technology adoption, operational performance, and evolving investment priorities. The analysis assesses demand across Base Stations, Data Centers, and Other telecom infrastructure, together with detailed evaluation of Telecom Operators, Tower Companies, and Data Center Operators. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment intensity, infrastructure modernization, and competitive positioning. More than 50% of current deployments are concentrated among telecom operators implementing intelligent power management and renewable-backed network infrastructure.

The report further examines competitive benchmarking, technology innovation, supply-chain developments, regulatory influences, and enterprise investment strategies shaping industry evolution between 2026 and 2033. It evaluates adoption of AI-enabled energy management, advanced battery storage, hybrid renewable systems, modular power architectures, and digital monitoring platforms while identifying emerging opportunities across rural connectivity, edge computing, and resilient communications infrastructure. Strategic insights support market entry, expansion planning, product development, partnership evaluation, competitive positioning, procurement decisions, and long-term infrastructure investment through detailed analysis of deployment trends, technology maturity, operational efficiency, and evolving customer requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 960.0 Million |

| Market Revenue (2033) | USD 5,328.0 Million |

| CAGR (2026–2033) | 23.89% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Huawei Technologies Co., Ltd.; Schneider Electric SE; Eaton Corporation plc; Vertiv Holdings Co.; Delta Electronics, Inc.; ZTE Corporation; ABB Ltd.; Cummins Inc.; EnerSys; Eltek AS; Mitsubishi Electric Corporation; Fuji Electric Co., Ltd.; Alpha Technologies Ltd.; NEC Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |