Reports

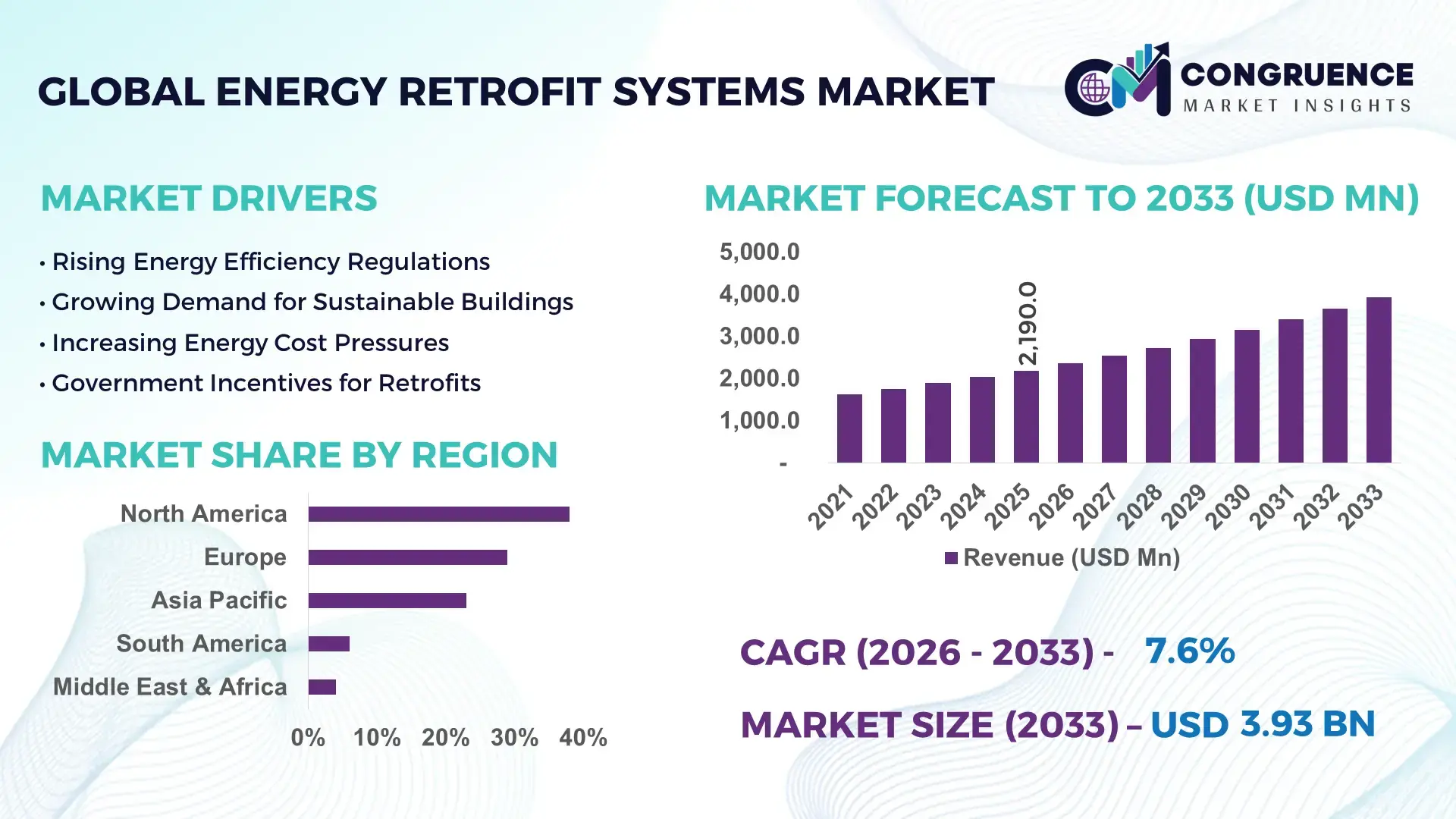

The Global Energy Retrofit Systems Market was valued at USD 2,190.0 Million in 2025 and is anticipated to reach a value of USD 3,935.0 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerating building decarbonization mandates, rising electricity tariffs, and the modernization of aging commercial and residential infrastructure.

The United States remains the dominant country in the Energy Retrofit Systems Market, supported by large-scale production capacity in HVAC upgrades, smart building controls, and high-efficiency insulation materials. Over 130 million buildings in the country are more than 30 years old, creating significant retrofit demand. Federal and state-level programs have mobilized over USD 60 billion in energy efficiency investments between 2021 and 2025. Commercial buildings account for nearly 45% of retrofit projects, with LED lighting adoption exceeding 70% penetration in large office facilities. Advanced Building Management Systems (BMS) integration has grown by over 35% in industrial facilities since 2022, reflecting rapid technological deployment. Heat pump installations surpassed 4 million units annually, strengthening electrification initiatives across residential and institutional segments.

Market Size & Growth: USD 2,190.0 Million (2025) projected to reach USD 3,935.0 Million by 2033 at 7.6% CAGR, driven by stricter energy performance standards and infrastructure upgrades.

Top Growth Drivers: 40% increase in green building certifications, 30% energy cost savings from LED retrofits, 25% rise in smart HVAC installations.

Short-Term Forecast: By 2028, integrated retrofit solutions are expected to reduce building energy consumption by 18% across commercial facilities.

Emerging Technologies: AI-enabled energy analytics, IoT-based smart meters, high-efficiency heat pumps, and digital twin modeling for retrofit planning.

Regional Leaders: North America projected at USD 1,420.0 Million by 2033 (high commercial retrofit adoption); Europe at USD 1,050.0 Million (strong regulatory compliance); Asia-Pacific at USD 890.0 Million (urban infrastructure modernization).

Consumer/End-User Trends: Commercial offices and healthcare facilities represent over 50% of retrofit deployments; residential heat pump adoption rising 28% annually.

Pilot or Case Example: In 2024, a U.S. municipal retrofit initiative achieved 22% energy savings and 15% maintenance cost reduction within 12 months.

Competitive Landscape: Johnson Controls holds approximately 18% share, followed by Siemens AG, Schneider Electric, Honeywell International Inc., and Trane Technologies.

Regulatory & ESG Impact: Net-zero mandates and building performance standards target 30–50% emission reductions by 2030 across major economies.

Investment & Funding Patterns: Over USD 75 billion invested globally (2021–2025) in building efficiency upgrades through green bonds and performance contracting models.

Innovation & Future Outlook: Integration of AI-driven predictive maintenance and electrified HVAC systems is expected to improve lifecycle efficiency by 20–25%.

Commercial buildings contribute nearly 45% of total retrofit demand, followed by residential at 35% and industrial at 20%. LED lighting and smart HVAC upgrades represent over 50% of installations. Regulatory mandates targeting 30–40% emission reductions are accelerating adoption across North America and Europe, while Asia-Pacific records double-digit growth in public infrastructure retrofits. Electrification, AI-enabled analytics, and performance-based contracting models are shaping future expansion and operational efficiency improvements.

Energy retrofit systems have emerged as a strategic instrument for governments and enterprises aiming to balance cost efficiency, regulatory compliance, and carbon reduction targets. Buildings account for nearly 37% of global energy-related emissions, making retrofit initiatives central to decarbonization strategies. Advanced AI-enabled Building Energy Management Systems deliver 25% improvement in operational efficiency compared to conventional programmable thermostats. Electrified heat pump retrofits reduce direct fossil fuel consumption by up to 40% compared to traditional gas boilers.

North America dominates in volume of retrofit deployments due to extensive aging infrastructure, while Europe leads in adoption intensity, with nearly 60% of large enterprises implementing structured building efficiency programs. By 2028, AI-driven predictive maintenance is expected to cut unexpected equipment downtime by 30% in commercial facilities. Firms are committing to ESG targets including 35% carbon intensity reduction by 2030 through structured retrofit investments.

In 2024, Germany achieved a 20% reduction in public building energy consumption through integrated digital control retrofits and high-performance insulation upgrades. These measurable outcomes reinforce the strategic importance of lifecycle asset management and electrification. Moving forward, the Energy Retrofit Systems Market will remain a pillar of infrastructure resilience, regulatory alignment, and sustainable economic growth, supporting measurable efficiency gains and long-term cost optimization.

The Energy Retrofit Systems Market is influenced by rising urbanization, stringent building efficiency regulations, and modernization of aging infrastructure assets. Governments across major economies are enforcing performance-based building codes requiring measurable emission reductions between 30% and 50% over the next decade. Commercial real estate portfolios are prioritizing operational cost reductions, where energy expenditures account for 25–35% of facility operating costs. Technological integration such as IoT sensors, automated HVAC controls, and smart lighting systems is transforming retrofit project execution. Increasing electrification trends, particularly heat pump deployment and rooftop solar integration, are further strengthening demand. Additionally, energy performance contracting (EPC) models are enabling financing flexibility, supporting adoption across municipalities, healthcare institutions, and educational campuses.

Governments across North America and Europe have implemented building performance standards targeting 30–50% emission reductions by 2030. Over 75 major cities have introduced mandatory benchmarking policies requiring annual energy disclosure. Commercial properties failing compliance face penalties exceeding 2–5% of annual asset value. Electrification incentives covering up to 30% of retrofit costs are accelerating project approvals. Institutional investors managing over USD 10 trillion in assets are integrating carbon metrics into property valuation frameworks, pushing landlords toward measurable efficiency improvements. These regulatory and financial drivers are intensifying retrofit project pipelines globally.

Comprehensive building retrofits often require capital expenditures ranging between USD 25 and USD 70 per square foot depending on system complexity. Small and medium enterprises frequently lack access to structured financing, limiting adoption. Payback periods may extend from 4 to 8 years for deep retrofits, creating budget allocation hesitations. Skilled labor shortages, particularly in HVAC modernization and digital control installation, have increased project timelines by 10–15%. Additionally, retrofitting occupied buildings can disrupt operations, leading to temporary productivity losses of 5–8% during installation phases.

IoT-enabled sensors now reduce real-time energy wastage by up to 20% in commercial facilities. Integration of AI-based analytics platforms enables predictive maintenance, lowering repair costs by 15–25%. Over 60% of newly renovated office buildings are incorporating smart meters and automated lighting systems. Data-driven optimization allows building managers to reduce peak load demand by 10–18%, supporting grid stability programs. Expanding green bond issuance, surpassing USD 500 billion annually, offers structured financing channels for large-scale retrofit portfolios, unlocking new growth avenues.

Building codes vary significantly across jurisdictions, requiring tailored engineering designs and compliance documentation. In multinational property portfolios, regulatory misalignment increases administrative costs by 12–18%. Legacy infrastructure often lacks compatibility with modern digital control systems, necessitating additional upgrades. Cybersecurity risks associated with connected building systems require advanced protection measures, increasing project budgets by 5–10%. Limited standardization in performance verification frameworks also complicates measurement of energy savings outcomes.

32% Growth in AI-Based Energy Optimization Platforms: Adoption of AI-powered building analytics increased by 32% between 2022 and 2025, enabling 18–25% reduction in real-time energy consumption across large commercial complexes. Over 48% of newly retrofitted Grade A office spaces now deploy predictive fault detection systems, reducing equipment failure rates by 20% and extending asset life by 15%.

28% Surge in Heat Pump Electrification Projects: Heat pump retrofits recorded 28% year-on-year growth, with installations exceeding 4 million units annually in developed markets. Electrified systems reduce carbon emissions by 35–45% compared to gas-based heating. Institutional facilities report 22% lower heating costs after large-scale electrification upgrades.

40% Expansion in Performance Contracting Models: Energy performance contracting adoption expanded by 40% globally, particularly in municipal and healthcare sectors. EPC-based projects deliver average verified energy savings of 18–30%, while reducing upfront capital burden by up to 80% through third-party financing structures.

35% Increase in Smart Lighting Retrofits: LED and smart lighting retrofits now account for 35% of total retrofit projects, delivering 50–60% electricity savings compared to legacy fluorescent systems. Automated daylight harvesting systems improve lighting efficiency by 20% and enhance occupant productivity metrics by 8–10% in corporate offices.

The Energy Retrofit Systems Market is segmented by type, application, and end-user, reflecting the diversity of technical upgrades implemented across aging infrastructure. By type, core systems include HVAC retrofits, lighting upgrades, building envelope improvements, energy management and control systems, and renewable integration solutions. HVAC and lighting together account for more than 55% of installed retrofit measures globally due to their immediate energy-saving impact. Application-wise, commercial buildings dominate deployment volumes, followed by residential and industrial facilities, with energy cost reduction and compliance-driven upgrades shaping adoption patterns. End-user segmentation highlights commercial real estate operators, public sector institutions, industrial manufacturers, and residential homeowners as primary stakeholders. Increasing electrification policies, smart building penetration exceeding 45% in developed markets, and digital monitoring adoption across 50% of large enterprises further reinforce differentiated demand patterns across segments.

HVAC retrofits represent the leading type in the Energy Retrofit Systems Market, accounting for approximately 34% share of total installations. Their dominance is supported by the fact that heating and cooling systems contribute 40–60% of building energy consumption in commercial facilities. Lighting retrofits hold nearly 26% share, primarily driven by LED adoption delivering 50–60% electricity savings compared to fluorescent systems. Energy management and control systems account for 18%, reflecting increasing integration of IoT-based monitoring and automated optimization platforms. Building envelope upgrades, including insulation and high-performance windows, contribute 14%, while renewable integration such as rooftop solar and battery storage represents 8%, forming a combined 22% share for niche and emerging segments. While HVAC leads in installed base, energy management and control systems are the fastest-growing type, expanding at an estimated 9.4% CAGR, fueled by AI-driven analytics adoption and predictive maintenance capabilities that reduce operational downtime by 20–30%. Renewable-integrated retrofits are also accelerating, supported by electrification mandates and distributed generation incentives.

In 2025, a U.S. Department of Energy-backed initiative upgraded over 1,200 federal buildings with high-efficiency HVAC systems, reporting average energy consumption reductions of 18% within the first operational year.

Commercial buildings constitute the leading application segment, capturing nearly 45% share of the Energy Retrofit Systems Market. Office complexes, hospitals, retail centers, and educational institutions prioritize retrofits due to high energy intensity and regulatory compliance requirements. Residential applications account for approximately 35%, driven by rising heat pump adoption and rooftop solar integration. Industrial facilities represent 20%, focusing on process optimization and facility-level energy efficiency. Commercial applications dominate due to structured ESG commitments and higher capital allocation capacity. However, residential retrofits are the fastest-growing application, expanding at an estimated 8.7% CAGR, supported by government subsidies covering up to 30% of installation costs in several economies and increasing consumer interest in reducing utility bills by 15–25%. Industrial retrofits remain stable, particularly in manufacturing hubs where energy costs account for 20–30% of operating expenses. In 2025, over 42% of large enterprises globally reported piloting smart energy monitoring platforms within commercial buildings to enhance ESG reporting transparency. Additionally, nearly 38% of homeowners in developed economies adopted at least one energy-efficient retrofit solution between 2022 and 2025.

In 2024, the European Commission’s public building renovation program upgraded more than 5,000 municipal buildings with smart metering and LED systems, achieving verified electricity savings exceeding 20% annually.

Commercial real estate operators represent the leading end-user segment with approximately 41% share, supported by portfolio-wide decarbonization strategies and regulatory reporting requirements. Public sector institutions, including government and educational facilities, account for 24%, driven by mandatory efficiency upgrades. Industrial enterprises contribute 19%, while residential homeowners and housing associations collectively represent 16%, forming a combined 35% share for non-commercial segments. While commercial operators lead in volume, residential end-users are the fastest-growing segment, expanding at an estimated 8.9% CAGR, supported by electrification incentives and consumer-driven sustainability initiatives. Public institutions are increasing digital control adoption, with over 50% of newly renovated government buildings incorporating smart energy management platforms. In 2025, nearly 46% of global corporations integrated energy efficiency metrics into annual ESG disclosures, strengthening retrofit demand. Additionally, more than 40% of urban homeowners reported prioritizing energy-efficient upgrades to mitigate rising electricity tariffs.

In 2025, a national infrastructure modernization program in Germany retrofitted over 3,000 public schools with automated energy management systems, reducing heating energy usage by 22% within two years of deployment.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of8.9% between 2026 and 2033.

North America’s dominance is supported by more than 5.6 billion square feet of commercial space undergoing phased efficiency upgrades, with LED retrofits covering over 72% of office buildings and smart HVAC penetration exceeding 48% in institutional facilities. Europe held approximately 29% share in 2025, driven by energy performance certificate mandates impacting nearly 65% of commercial properties across the EU. Asia-Pacific captured 23% share, with over 40 major metropolitan infrastructure modernization programs launched between 2022 and 2025. South America represented 6%, while Middle East & Africa accounted for 4%, supported by public infrastructure electrification and oil & gas facility efficiency upgrades. Across all regions, performance-based contracts deliver verified savings ranging between 18% and 30%, strengthening cross-regional adoption patterns.

North America holds approximately 38% market share in the Energy Retrofit Systems Market, with the United States contributing over 80% of regional installations. Key industries include commercial real estate, healthcare, higher education, and federal infrastructure projects. More than 130 million buildings are over 30 years old, creating large retrofit demand cycles. Federal incentives and state-level building performance standards mandate 30–50% emissions reductions by 2030 in several major cities. Digital transformation is evident with 52% of large enterprises integrating IoT-based building management systems. Johnson Controls has expanded AI-enabled HVAC optimization platforms across 10,000+ facilities, improving energy performance by 20%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, where uptime reliability and ESG reporting compliance influence procurement decisions.

Europe commands nearly 29% share of the Energy Retrofit Systems Market, with Germany, the UK, and France leading deployment volumes. Over 60% of commercial properties in these countries are subject to strict energy performance certification requirements. The European Green Deal mandates carbon neutrality targets, influencing retrofit investments across 27 EU member states. More than 45% of office renovations now include smart metering and digital energy analytics integration. Siemens AG is deploying intelligent building automation across municipal facilities, achieving verified 18–25% energy reductions. Consumer behavior in this region reflects strong regulatory pressure, leading to demand for transparent energy data reporting and explainable efficiency metrics. Public building renovations increased by 12% annually between 2022 and 2025, reinforcing compliance-driven market expansion.

Asia-Pacific ranks third in total market volume but leads in growth acceleration, accounting for 23% share in 2025. China, India, and Japan are the top consuming countries, together representing over 70% of regional retrofit installations. Urban infrastructure expansion includes more than 100 smart city initiatives integrating energy optimization platforms. Industrial retrofits contribute nearly 35% of regional installations, reflecting manufacturing modernization trends. Japan’s building automation adoption exceeds 40% in commercial facilities, while India’s public sector retrofits expanded by 22% between 2022 and 2025. Mitsubishi Electric has deployed high-efficiency HVAC systems across industrial parks, achieving 15–20% operational energy savings. Regional consumer behavior reflects rapid digital adoption and mobile-enabled facility management systems, accelerating smart retrofit acceptance.

South America accounts for approximately 6% market share, with Brazil and Argentina leading demand. Brazil represents over 55% of regional retrofit activity, particularly within commercial and public-sector buildings. National energy efficiency programs incentivize LED conversions delivering 40–55% lighting savings. Infrastructure modernization efforts include grid upgrades impacting over 30 major cities. Industrial facilities account for 28% of retrofit demand due to rising electricity tariffs. Local energy service companies are expanding performance-based contracting models, reducing upfront investment burdens by up to 70%. Consumer adoption patterns indicate demand tied to commercial real estate redevelopment and municipal building efficiency improvements, with sustainability certification requests increasing by 18% annually.

Middle East & Africa represents about 4% market share, driven by large-scale construction and oil & gas facility modernization. The UAE and South Africa are primary growth countries, together accounting for nearly 60% of regional retrofit deployments. Cooling systems constitute over 45% of retrofit investments due to extreme climate conditions. Government diversification initiatives emphasize 25–30% building efficiency improvements by 2030. Smart metering penetration increased by 20% between 2022 and 2025. Local utilities are promoting demand-side management programs encouraging commercial retrofits. Regional consumer behavior reflects strong interest in high-efficiency HVAC and solar-integrated building systems to reduce peak load demand by up to 15%.

United States – 31% Market Share: It leads due to extensive aging infrastructure, large-scale federal incentives, and high enterprise adoption of digital building management systems.

Germany – 11% Market Share: It is driven by stringent building efficiency regulations, strong industrial retrofit demand, and widespread integration of automated energy optimization technologies.

The Energy Retrofit Systems Market is moderately fragmented, with more than 120 active global and regional competitors operating across HVAC upgrades, smart building controls, lighting systems, insulation solutions, and renewable integration. The top five companies collectively account for approximately 46% of total market share, indicating a competitive yet innovation-driven landscape. Market leaders differentiate through vertically integrated offerings combining equipment manufacturing, digital analytics, and performance-based contracting.

Strategic initiatives intensified between 2023 and 2025, with over 35 recorded partnerships and joint ventures focused on AI-enabled building management, electrification, and grid-responsive retrofit systems. More than 25 product launches introduced advanced heat pumps, low-GWP refrigerant systems, and AI-powered energy optimization platforms. Mergers and acquisitions activity increased by nearly 18%, particularly targeting niche IoT sensor developers and digital twin solution providers.

Competitive positioning increasingly hinges on lifecycle service models, where energy performance contracts guarantee 18–30% verified energy savings. Over 52% of large retrofit projects now include bundled digital monitoring solutions, reflecting technology-driven differentiation. Innovation trends include predictive fault detection reducing downtime by 20%, modular retrofit kits shortening installation timelines by 15%, and integrated ESG reporting dashboards adopted by 48% of multinational building operators. The competitive environment is characterized by cross-sector integration, financing innovation, and sustainability-aligned product development.

Honeywell International Inc.

Trane Technologies

Daikin Industries Ltd.

Mitsubishi Electric Corporation

Carrier Global Corporation

ABB Ltd.

Eaton Corporation

Legrand SA

Emerson Electric Co.

Rockwell Automation, Inc.

Signify N.V.

Bosch Building Technologies

Technological innovation remains central to the Energy Retrofit Systems Market, particularly in digitalization, electrification, and automation. AI-driven Building Energy Management Systems (BEMS) now enable 15–25% real-time energy optimization across large commercial complexes. IoT-enabled sensors are installed in over 50% of newly retrofitted office buildings, supporting predictive maintenance strategies that reduce unexpected equipment failures by 20–30%.

Electrification technologies, especially high-efficiency heat pumps, are reshaping retrofit priorities. Modern air-to-water heat pumps deliver 300–400% coefficient of performance, significantly outperforming legacy gas boilers. Variable refrigerant flow (VRF) systems improve zone-level temperature control by up to 25%, enhancing occupant comfort while lowering energy intensity.

Digital twin modeling is gaining traction, allowing building operators to simulate retrofit scenarios before implementation. Facilities deploying digital twins report 12–18% reduction in project planning errors and improved return-on-investment predictability. Smart lighting systems integrated with occupancy sensors achieve 50–60% electricity savings compared to traditional fluorescent fixtures.

Battery storage and distributed energy resource integration are expanding within commercial retrofits, with storage capacity installations increasing by over 22% between 2023 and 2025. Cloud-based energy dashboards now support ESG data reporting, adopted by nearly 48% of multinational enterprises. Cybersecurity enhancements in connected systems are also prioritized, with 35% of retrofit budgets in critical infrastructure projects allocated to network security upgrades. These technological advancements collectively strengthen performance assurance, operational transparency, and long-term asset resilience.

• In April 2025, Johnson Controls released a commissioned study showing its OpenBlue Smart Building platform delivered up to 10% energy savings and up to 67% reduction in chiller maintenance costs over three years, with an 8-month payback period on investments, demonstrating measurable operational efficiency and sustainability gains for customers deploying the platform. Source: www.prnewswire.com

• In June 2025, Johnson Controls launched OpenBlue Workplace in the Middle East—an integrated workplace management system that enhances real estate performance through analytics, sensor-driven insights, and smart building technologies, enabling up to 10% energy savings and bolstering operational agility for businesses in the UAE. Source: www.me.johnsoncontrols.com

• In May 2025, Schneider Electric announced a multi-year initiative to build an AI-native ecosystem for sustainability and energy management, positioning agentic AI at the core of its digital energy solutions to improve automation, real-time adaptability, and collaborative intelligence across energy and building management systems. Source: www.prnewswire.com

• In March 2025, Siemens announced plans to showcase innovative and sustainable building technologies at ISH 2025, including IoT-enabled wireless automation bundles, Connect Box solutions, and the Desigo building management system focused on enhancing energy efficiency and cybersecurity across diverse building types. Source: www.press.siemens.com

The Energy Retrofit Systems Market Report provides comprehensive coverage across technology types, applications, end-user industries, and geographic regions. The scope encompasses HVAC modernization, lighting upgrades, energy management and control systems, building envelope improvements, and renewable energy integration solutions. These segments collectively address more than 70% of building-level energy consumption reduction opportunities in commercial and institutional infrastructure.

The report evaluates applications across commercial buildings, residential complexes, industrial facilities, healthcare institutions, educational campuses, and government infrastructure. Commercial properties represent the largest deployment base, while residential electrification initiatives are expanding rapidly in urban markets. Industrial retrofits focus on process efficiency and load management, accounting for nearly 20% of total installations.

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering over 40 key countries with diverse regulatory environments and infrastructure maturity levels. Technological scope includes AI-based analytics, IoT sensor networks, digital twin simulations, electrified HVAC systems, and distributed energy resources. It also assesses financing models such as performance-based contracting, green bonds, and public-private partnerships influencing adoption.

Additionally, the report highlights niche and emerging segments, including grid-interactive efficient buildings, carbon accounting software integration, and modular retrofit kits that reduce installation time by up to 15%. The analytical framework supports strategic planning, investment prioritization, regulatory compliance alignment, and long-term asset optimization for decision-makers across public and private sectors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,190.0 Million |

| Market Revenue (2033) | USD 3,935.0 Million |

| CAGR (2026–2033) | 7.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Johnson Controls; Siemens AG; Schneider Electric; Honeywell International Inc.; Trane Technologies; Daikin Industries Ltd.; Mitsubishi Electric Corporation; Carrier Global Corporation; ABB Ltd.; Eaton Corporation; Legrand SA; Emerson Electric Co.; Rockwell Automation, Inc.; Signify N.V.; Bosch Building Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |