Reports

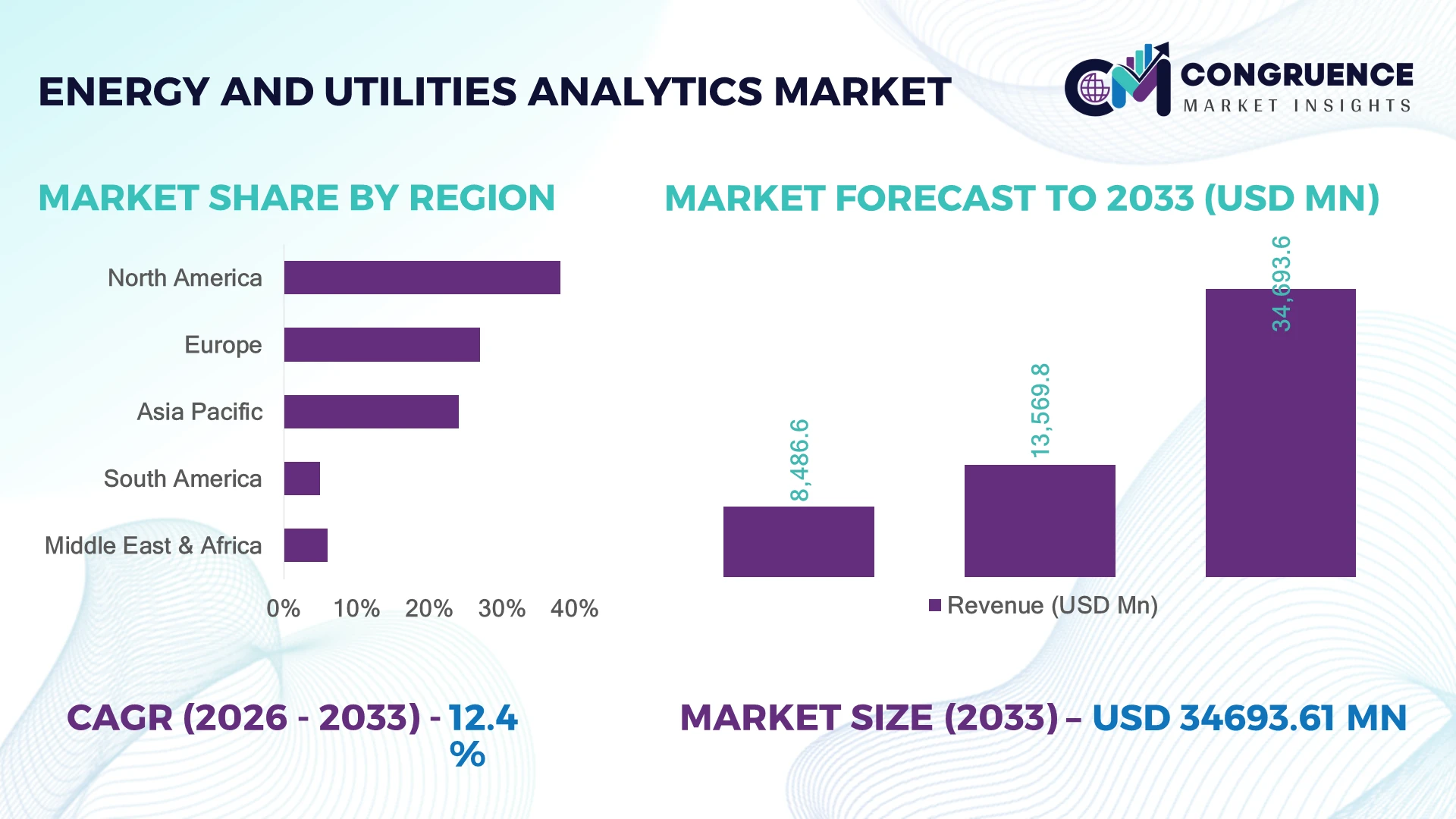

The Global Energy and Utilities Analytics Market was valued at USD 13569.81 Million in 2025 and is anticipated to reach a value of USD 34693.61 Million by 2033 expanding at a CAGR of 12.45% between 2026 and 2033. Grid modernization programs, AI-based demand forecasting, renewable energy integration, and cybersecurity-focused utility operations are accelerating advanced analytics deployment across transmission, distribution, and energy trading networks.

The United States dominates the global Energy and Utilities Analytics Market with nearly 34% share, supported by over USD 75 billion in smart grid and transmission investments under ongoing federal energy transition programs. More than 72% of large U.S. utilities deployed AI-enabled outage prediction and load-balancing systems in 2026, compared to 49% adoption across Germany’s utility sector, where renewable grid stabilization remains the core priority amid Europe’s post-energy-crisis infrastructure restructuring. Industrial utilities, LNG operations, and distributed energy management continue driving higher analytics penetration across North America than Asia-Pacific utilities.

Utilities prioritizing predictive analytics platforms, decentralized energy optimization, and real-time operational intelligence are securing stronger grid resilience, lower outage costs, and faster renewable integration scalability.

Market Size & Growth: USD 13569.81 Million in 2025 to USD 34693.61 Million by 2033 at 12.45% growth, driven by AI-powered grid optimization and renewable energy analytics deployment.

Top Growth Drivers: Smart meter penetration rose 28%, renewable integration projects increased 31%, and predictive maintenance adoption expanded 24% globally during 2026.

Short-Term Forecast: By 2028, utilities using advanced analytics platforms are projected to reduce outage response time by 36% and improve grid efficiency by 21%.

Emerging Technologies: AI-based load forecasting, digital twins, and edge analytics improved asset utilization rates by over 27% across high-growth utility infrastructure networks.

Regional Leaders: North America exceeds USD 11 billion through smart-grid analytics expansion, Europe surpasses USD 8 billion via decarbonization mandates, and Asia-Pacific crosses USD 9 billion through industrial electrification projects.

Consumer/End-User Trends: Over 63% of utility providers integrated real-time customer consumption analytics to support dynamic pricing and distributed energy management.

Pilot/Case Example: In 2026, a large-scale utility digitization project reduced transformer failure incidents by 32% using AI-driven predictive maintenance systems.

Competitive Landscape: Leading providers collectively control nearly 41% market share, with competition centered on cloud analytics, grid intelligence, and cybersecurity integration capabilities.

Regulatory & ESG Impact: Carbon reduction mandates accelerated renewable analytics deployment by 29%, especially across European and North American energy transition programs.

Investment & Funding: Global investments surpassed USD 18 billion in 2026, led by utility-cloud partnerships, transmission modernization, and advanced energy data platforms.

Innovation & Future Outlook: Autonomous grid analytics, decentralized energy orchestration, and AI-assisted demand balancing are reshaping utility operating models and energy trading strategies.

Advanced Energy and Utilities Analytics platforms are expanding rapidly across smart grids, renewable forecasting, and industrial energy optimization environments. Utilities integrating AI-enabled asset monitoring reported nearly 26% lower unplanned downtime in 2026, while cloud-native analytics platforms improved real-time energy balancing accuracy. Rising cross-border energy security concerns and stricter emissions monitoring frameworks are accelerating investments in predictive grid intelligence, creating a stronger foundation for strategic infrastructure modernization and operational resilience planning.

Energy and Utilities Analytics has become a strategic control layer for utilities managing renewable intermittency, grid decentralization, and industrial electrification. Utility operators are prioritizing predictive analytics and AI-driven grid intelligence to stabilize power distribution while lowering operational losses. The market is gaining competitive relevance as countries including the United States, India, and Germany accelerate transmission modernization and digital substation deployment following energy security disruptions and stricter emissions compliance frameworks introduced after the European energy supply restructuring cycle.

Cloud-native analytics platforms now process grid events nearly 43% faster than conventional on-premise monitoring systems while reducing maintenance planning costs by approximately 26%. In Japan, utilities are emphasizing distributed energy orchestration and battery analytics for urban resilience, whereas U.S. operators are deploying large-scale AI-based outage management across aging transmission infrastructure. Over 61% of large utility enterprises integrated real-time consumption analytics into operations during 2026, with smart meter-linked predictive platforms becoming standard in high-density industrial corridors.

A leading utility deployment in Texas integrated digital twin analytics with renewable forecasting systems, reducing transformer overload incidents by 31% within one operational cycle. Energy technology providers are responding through cloud partnerships, cybersecurity integration, and grid-edge analytics expansion. Over the next three years, utilities prioritizing interoperable analytics ecosystems and automated grid intelligence will secure stronger operational resilience, faster renewable integration, and superior long-term infrastructure efficiency.

Utility operators are accelerating analytics adoption to manage renewable intermittency, distributed energy resources, and aging transmission infrastructure. In 2026, more than 68% of large-scale utilities in the United States deployed AI-enabled outage prediction systems, while smart meter penetration exceeded 74% across advanced electricity networks. India expanded digital grid investments through transmission automation programs supporting industrial electrification and real-time energy balancing. This structural modernization shift is reducing unplanned downtime by nearly 29% and improving load forecasting precision by over 33%. Utilities are responding through cloud partnerships, grid-edge analytics investments, and acquisitions focused on predictive maintenance platforms. A major operational insight shaping procurement strategies is the growing preference for interoperable analytics ecosystems capable of integrating renewable forecasting, cybersecurity monitoring, and energy trading intelligence within a unified operational environment.

Fragmented utility infrastructure and incompatible operational technologies continue limiting analytics scalability across transmission and distribution networks. Nearly 41% of utility operators globally still rely on legacy SCADA environments with limited real-time integration capability, while modernization costs for aging substations increased by approximately 18% during 2026 due to semiconductor and industrial equipment supply volatility. Germany and parts of Eastern Europe experienced deployment delays linked to grid synchronization complexity and cybersecurity compliance upgrades. These constraints are increasing implementation timelines, raising operational expenditure, and reducing analytics standardization across multi-vendor utility systems. Companies are mitigating risk through phased modernization programs, localized equipment sourcing, and hybrid deployment architectures combining cloud analytics with existing infrastructure. Utilities with fragmented data environments are also facing slower renewable integration efficiency and weaker predictive maintenance performance compared to digitally standardized operators.

The expansion of decentralized energy systems is creating high-value opportunities for advanced analytics providers focused on grid-edge intelligence and autonomous energy optimization. More than 37% of newly deployed renewable assets in 2026 incorporated embedded analytics capabilities for real-time forecasting and storage management. China accelerated virtual power plant deployment across industrial provinces, while the United Kingdom expanded dynamic pricing infrastructure supporting decentralized energy participation. Edge analytics platforms are improving distributed asset response speed by nearly 34% compared to centralized monitoring environments. Companies are increasing investments in battery analytics, AI-driven demand response, and digital twin simulation platforms to strengthen grid flexibility. A notable strategic opportunity is emerging in industrial microgrid orchestration, where utilities and manufacturing operators are building integrated energy ecosystems that combine predictive analytics, carbon monitoring, and automated consumption balancing for operational efficiency gains.

The increasing integration of cloud platforms, connected substations, and distributed energy networks is intensifying cybersecurity and operational execution risks. In 2026, utility-sector cyber incidents targeting operational technology environments increased by approximately 27%, while nearly 46% of energy operators reported shortages in advanced analytics and grid-cybersecurity specialists. The United States and Japan are facing growing pressure to secure AI-enabled utility infrastructure against grid disruption and ransomware attacks linked to expanding digital energy ecosystems. These challenges are affecting deployment consistency, operational trust, and long-term infrastructure scalability. Companies must strengthen zero-trust architecture, operational technology segmentation, and AI-based threat monitoring while expanding workforce development partnerships with industrial technology firms and engineering institutions. Utilities unable to secure interoperable and cyber-resilient analytics environments risk higher outage exposure, regulatory penalties, and weaker competitiveness in decentralized energy markets.

• AI-Integrated Grid Operations Utilities are embedding AI analytics directly into transmission control workflows to improve grid stability and outage response precision. In 2026, automated fault detection deployment increased by 38% across U.S. utility operators, while AI-assisted load balancing reduced peak distribution losses by nearly 24%. Following grid instability events and renewable intermittency pressures, utilities are restructuring operational command centers and expanding cloud-grid partnerships to support continuous real-time analytics processing.

• Edge Analytics Expansion Accelerates Energy providers are shifting toward edge analytics architectures to process distributed energy data closer to operational assets. Smart substation deployments using edge intelligence expanded by 31% in China during 2026, while industrial microgrid response times improved by approximately 29% compared to centralized systems. Utilities are prioritizing localized processing to reduce bandwidth strain and improve battery storage coordination, especially across manufacturing-intensive industrial corridors facing energy reliability pressure.

• Cyber-Resilient Utility Platforms Rise Rising operational technology attacks are accelerating adoption of cybersecurity-integrated analytics environments. More than 44% of large utilities integrated AI-driven threat monitoring into energy analytics platforms in 2026, while ransomware-related grid interruption risks increased by 21%. Japanese utility operators are consolidating fragmented monitoring systems into unified operational intelligence platforms, enabling faster anomaly detection and reducing incident response cycles through automated infrastructure monitoring and cross-network analytics orchestration.

• Dynamic Pricing Analytics Advance Utilities are scaling consumption analytics platforms to support dynamic pricing and decentralized energy participation. Smart meter-linked tariff optimization programs improved demand response efficiency by nearly 33% across parts of Germany and the United Kingdom in 2026. Companies are integrating behavioral analytics, distributed energy forecasting, and customer consumption intelligence into unified billing ecosystems, creating stronger load management precision while reducing energy procurement volatility during high-demand industrial operating periods.

Cloud Analytics leads the Energy and Utilities Analytics Market due to its scalability, lower infrastructure dependency, and ability to integrate high-volume operational data across distributed utility networks. In 2026, over 64% of large utility enterprises shifted core analytics workloads toward cloud-native environments to improve outage management and renewable forecasting efficiency. Utilities are prioritizing cloud deployment to reduce operational latency, strengthen cybersecurity integration, and support multi-site energy orchestration. Real-Time Analytics is emerging as the fastest-growing segment as grid operators require sub-second operational visibility for battery management, decentralized energy balancing, and predictive fault detection. Real-time monitoring platforms improved response accuracy by approximately 32% compared to legacy reporting systems during large-scale transmission events.

Predictive Analytics remains strategically important for asset reliability and maintenance optimization, especially across aging utility infrastructure in the United States and Japan. Prescriptive Analytics adoption is increasing through AI-assisted energy trading and automated dispatch optimization, while Descriptive Analytics maintains relevance in regulatory reporting and consumption benchmarking. Companies are expanding investments in hybrid analytics platforms combining predictive, real-time, and prescriptive capabilities to strengthen operational resilience and energy efficiency performance.

Grid Management remains the dominant application segment due to rising transmission complexity, renewable integration requirements, and utility modernization programs. In 2026, nearly 69% of large utility operators implemented advanced analytics within transmission and distribution control systems to reduce outage frequency and improve load balancing precision. Utilities are integrating AI-driven grid intelligence platforms to strengthen operational continuity and support decentralized energy participation. Demand Response is the fastest-growing application as dynamic pricing infrastructure, distributed generation, and industrial electrification increase pressure on energy balancing systems. Smart demand-response analytics reduced peak-load stress by approximately 27% across digitally upgraded utility networks in Germany and the United Kingdom.

Energy Forecasting continues gaining strategic importance through renewable generation planning and battery-storage optimization, particularly in countries with high solar and wind penetration. Asset Management analytics adoption remains strong among utilities managing aging substations and transformer fleets, while Smart Meter Analytics is expanding rapidly through customer consumption monitoring and dynamic billing integration. Companies are scaling AI-enabled forecasting engines, automated grid orchestration, and smart metering ecosystems to improve infrastructure utilization and operational flexibility across industrial and municipal energy environments.

Power Utilities dominate the Energy and Utilities Analytics Market due to extensive transmission infrastructure, high operational data volumes, and continuous grid modernization requirements. In 2026, more than 71% of advanced utility analytics deployments were concentrated within electricity generation, transmission, and distribution operations. Utilities are prioritizing predictive maintenance, real-time balancing, and renewable integration analytics to stabilize increasingly decentralized power networks. Renewable Energy Providers represent the fastest-growing end-user segment as solar, wind, and battery operators expand forecasting and storage optimization investments. Renewable asset analytics improved generation scheduling efficiency by approximately 28% across large-scale hybrid energy projects deployed in China and India.

Oil and Gas Companies continue investing in analytics for pipeline monitoring, energy trading optimization, and refinery efficiency management, while Industrial Facilities are increasing adoption to control power consumption volatility and improve energy productivity. Government Utilities are scaling digital utility infrastructure through national smart-grid programs, and Energy Service Companies are integrating analytics into energy-efficiency contracting models. Vendors are responding through customized deployment architectures, sector-specific AI modules, and long-term utility partnerships designed to improve infrastructure visibility and operational intelligence.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

AI-Driven Grid Intelligence Dominates Utility Modernization

North America maintains the highest deployment concentration in the Energy and Utilities Analytics Market due to advanced grid infrastructure, large-scale smart meter penetration, and aggressive utility digitization programs. More than 76% of major electricity providers across the United States and Canada integrated predictive analytics into transmission and outage management operations during 2026. Utilities are prioritizing cloud-based operational intelligence platforms to improve renewable integration, grid resilience, and cybersecurity readiness. The region also leads in utility-AI partnerships, particularly for decentralized energy orchestration and battery optimization. Transmission modernization programs and industrial electrification initiatives continue accelerating analytics deployment across high-demand energy corridors, while AI-enabled maintenance systems reduced transformer failure incidents by approximately 29% in large utility networks.

United States Market Outlook: The United States remains the strategic center of utility analytics deployment due to extensive smart-grid infrastructure, high renewable integration targets, and large-scale industrial electricity demand. In 2026, over 72% of investor-owned utilities expanded AI-enabled grid monitoring systems to improve outage prediction and load-balancing precision. Federal transmission modernization initiatives and grid cybersecurity mandates are accelerating cloud analytics integration across utilities, while energy-intensive manufacturing hubs continue increasing demand for predictive operational intelligence platforms.

Decarbonization Policies Accelerate Digital Utility Transformation

Europe is strengthening its position through renewable energy integration, cross-border electricity balancing, and carbon monitoring modernization. Utilities across Germany, France, and the Nordic energy corridor are deploying advanced analytics platforms to stabilize renewable-heavy electricity networks and improve grid flexibility. More than 61% of utility operators in Western Europe integrated AI-assisted forecasting tools during 2026 to manage wind and solar intermittency. Energy security restructuring following regional supply disruptions accelerated investment in real-time grid visibility and distributed energy management systems. Utilities are also prioritizing ESG-linked analytics capabilities to improve emissions tracking and operational transparency. Digital substation deployment and smart-grid synchronization projects continue driving enterprise-scale adoption of predictive and prescriptive analytics technologies across transmission networks.

Germany Market Outlook: Germany leads the European Energy and Utilities Analytics Market through renewable infrastructure scale, industrial electrification intensity, and advanced grid modernization initiatives. In 2026, utility operators expanded digital substation deployment across manufacturing-intensive regions to support decentralized energy balancing and carbon optimization targets. More than 58% of major German utilities integrated predictive analytics into renewable forecasting workflows, while industrial operators increased investments in energy intelligence systems to improve operational efficiency and reduce exposure to electricity price volatility.

Massive Smart Grid Deployment Reshapes Operations

Asia-Pacific is emerging as the fastest-scaling market due to rapid urbanization, industrial electrification, and large-scale smart-grid infrastructure expansion. China, India, Japan, and South Korea are increasing analytics deployment to support renewable integration, transmission modernization, and industrial energy optimization. In 2026, smart meter deployment across major Asia-Pacific utility networks exceeded 68%, while grid-edge analytics integration increased by approximately 34% in industrial energy systems. Utilities are adopting AI-enabled forecasting and decentralized energy orchestration to manage rising electricity demand and grid congestion. Government-backed utility digitization programs and large-scale renewable infrastructure investments are accelerating deployment across manufacturing clusters and urban energy corridors, particularly where industrial productivity and energy reliability are operational priorities.

China Market Outlook: China dominates Asia-Pacific through extensive utility infrastructure, renewable energy deployment scale, and state-supported grid modernization initiatives. In 2026, large utility enterprises expanded AI-powered transmission analytics and virtual power plant integration across industrial provinces to improve grid balancing efficiency. The country also accelerated deployment of battery-storage analytics and edge intelligence platforms supporting renewable-heavy electricity systems, while manufacturing-intensive regions increased adoption of predictive maintenance technologies to strengthen operational continuity and energy optimization performance.

Grid Reliability and Industrial Efficiency Gain Priority

South America is advancing through utility modernization initiatives focused on grid reliability, hydropower optimization, and industrial energy efficiency. Brazil, Chile, and Colombia are increasing deployment of analytics platforms to strengthen electricity distribution performance and improve renewable integration capabilities. In 2026, utility digitization programs expanded smart-grid monitoring coverage by nearly 26% across selected urban transmission networks. Energy providers are integrating predictive maintenance analytics into hydropower and industrial electricity systems to reduce operational disruption and improve infrastructure utilization. However, fragmented grid infrastructure and uneven digital readiness continue limiting large-scale deployment consistency in some markets. Utilities are responding through phased modernization strategies, localized partnerships, and cloud-based operational intelligence integration to improve scalability and reduce infrastructure strain.

Brazil Market Outlook: Brazil leads the South American market due to its extensive electricity distribution infrastructure, hydropower dependence, and industrial energy consumption scale. In 2026, utilities increased investments in predictive grid monitoring and renewable balancing analytics to improve transmission reliability during seasonal demand fluctuations. Smart-grid deployment expanded across high-density industrial corridors, while electricity providers accelerated digital asset management integration to reduce downtime and improve operational visibility within aging infrastructure environments.

Energy Diversification Drives Digital Utility Investment

The Middle East & Africa market is expanding through utility diversification programs, smart-city infrastructure investment, and large-scale energy transition initiatives. Gulf countries are prioritizing analytics deployment to improve electricity distribution efficiency, renewable integration, and water-energy management optimization. In 2026, advanced metering and grid analytics implementation increased by approximately 32% across digitally upgraded utility projects in the Gulf Cooperation Council economies. Utilities are integrating AI-enabled monitoring systems to strengthen operational continuity within high-temperature transmission environments and rapidly expanding urban energy networks. African utility operators are also adopting cloud-based analytics platforms to improve outage visibility and infrastructure planning despite ongoing grid modernization challenges and connectivity gaps across selected national networks.

Saudi Arabia Market Outlook: Saudi Arabia remains the most strategically significant market within the region due to large-scale infrastructure investment, smart-city development programs, and utility digitization priorities linked to national economic diversification plans. In 2026, state-backed utility operators accelerated deployment of AI-based grid management systems and predictive maintenance analytics across expanding renewable and transmission projects. Large industrial and urban infrastructure developments are further increasing demand for integrated energy intelligence platforms capable of supporting operational optimization and long-term electricity network resilience.

The Energy and Utilities Analytics Market is led by technology-driven competitors including IBM, Oracle, SAP, Siemens, Schneider Electric, and SAS Institute, competing directly against specialized grid analytics providers and cloud-native industrial intelligence firms. The top five players collectively control nearly 48% of the market through integrated utility platforms, AI-enabled forecasting, and enterprise-scale grid optimization capabilities. Competition centers on deployment speed, predictive accuracy, cybersecurity integration, and interoperability, with AI-assisted outage management improving operational response efficiency by over 30% compared to legacy utility systems. Global leaders are expanding through utility-cloud partnerships, digital twin integration, and acquisition-led portfolio consolidation, while regional providers compete aggressively through lower implementation costs and localized infrastructure customization. The competitive shift is moving toward autonomous grid orchestration and decentralized energy intelligence. High integration complexity, utility compliance requirements, and operational cybersecurity expectations remain major entry barriers. Winning requires scalable analytics ecosystems, sector-specific AI models, and strong long-term utility partnerships.

IBM Corporation

Oracle Corporation

SAP SE

Siemens AG

Schneider Electric SE

SAS Institute Inc.

General Electric Company

ABB Ltd.

Honeywell International Inc.

Microsoft Corporation

Cisco Systems Inc.

Eaton Corporation plc

Hitachi Energy Ltd.

Infosys Limited

AI-powered predictive analytics platforms are becoming the operational core of modern utility networks, particularly across transmission monitoring, outage prediction, and renewable forecasting systems. In 2026, nearly 67% of large utilities integrated machine learning models into grid operations, improving fault-detection accuracy by approximately 34% and reducing maintenance scheduling costs by 22%. Cloud-native analytics platforms process high-volume smart meter and substation data nearly 41% faster than legacy on-premise utility systems, enabling faster load balancing and distributed energy coordination. Utilities deploying integrated AI-grid orchestration platforms are securing stronger operational resilience and lower outage recovery time across industrial electricity corridors.

Edge analytics and digital twin technologies are emerging rapidly as utilities manage decentralized energy systems and battery-storage integration. Real-time edge processing improved distributed grid response speed by nearly 29% during high-demand operational cycles, while digital twin-based simulation reduced infrastructure planning inefficiencies by 24%. Utilities in Japan and Germany are scaling virtual substation models and decentralized forecasting engines to stabilize renewable-heavy networks and improve energy dispatch precision.

Between 2026 and 2028, autonomous grid intelligence, AI-assisted cybersecurity analytics, and interoperable energy orchestration platforms will reshape utility competition. Companies investing early in integrated analytics ecosystems, GPU-accelerated forecasting, and grid-edge automation will gain measurable advantages in renewable scalability, transmission reliability, and operational decision speed.

March 2026 – IBM expanded its collaboration with NVIDIA to accelerate GPU-native enterprise analytics and regulated AI infrastructure deployment. The integration improved structured data analytics throughput significantly across enterprise environments, strengthening utility-scale AI deployment efficiency and operational scalability. Source: newsroom.ibm.com

March 2025 – Schneider Electric launched its One Digital Grid Platform integrating AI-driven utility analytics, DERMS, and resiliency management into a unified architecture. The platform targeted lower total infrastructure ownership costs while improving grid operational flexibility and renewable integration performance across utility networks. Source: se.com

February 2026 – Siemens Energy announced a USD 1 billion U.S. expansion focused on grid equipment and turbine production, increasing global turbine manufacturing capacity by approximately 20%. The investment strengthens analytics-enabled power infrastructure deployment supporting AI-driven electricity demand growth.

June 2026 – Schneider Electric and Foxconn partnered to develop AI-ready energy and cooling infrastructure for next-generation data centers, with production scheduled for later in 2026. The collaboration strengthens integrated energy intelligence deployment supporting rapidly expanding AI-intensive electricity environments. Source: reuters.com

The Energy and Utilities Analytics Market report delivers comprehensive analysis across predictive analytics, descriptive analytics, prescriptive analytics, real-time analytics, and cloud analytics technologies supporting utility modernization and industrial energy optimization. The study evaluates deployment patterns across grid management, energy forecasting, asset management, demand response, and smart meter analytics applications, covering more than 70% of current utility digitization priorities. The report also examines operational adoption trends across power utilities, renewable energy providers, oil and gas companies, industrial facilities, and government utilities.

Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting infrastructure modernization, renewable integration, smart-grid deployment, and decentralized energy orchestration trends between 2026 and 2033. The report provides strategic insights into AI-enabled grid intelligence, digital twin integration, cybersecurity analytics, and edge computing adoption while analyzing competitive positioning, enterprise deployment priorities, partnership activity, and utility investment direction shaping long-term operational transformation across global energy infrastructure ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 13569.81 Million |

Market Revenue in 2033 | USD 34693.61 Million |

CAGR (2026 - 2033) | 12.45% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | IBM Corporation, Oracle Corporation, SAP SE, Siemens AG, Schneider Electric SE, SAS Institute Inc., General Electric Company, ABB Ltd., Honeywell International Inc., Microsoft Corporation, Cisco Systems Inc., Eaton Corporation plc, Hitachi Energy Ltd., Infosys Limited |

Customization & Pricing | Available on Request (10% Customization is Free) |