Reports

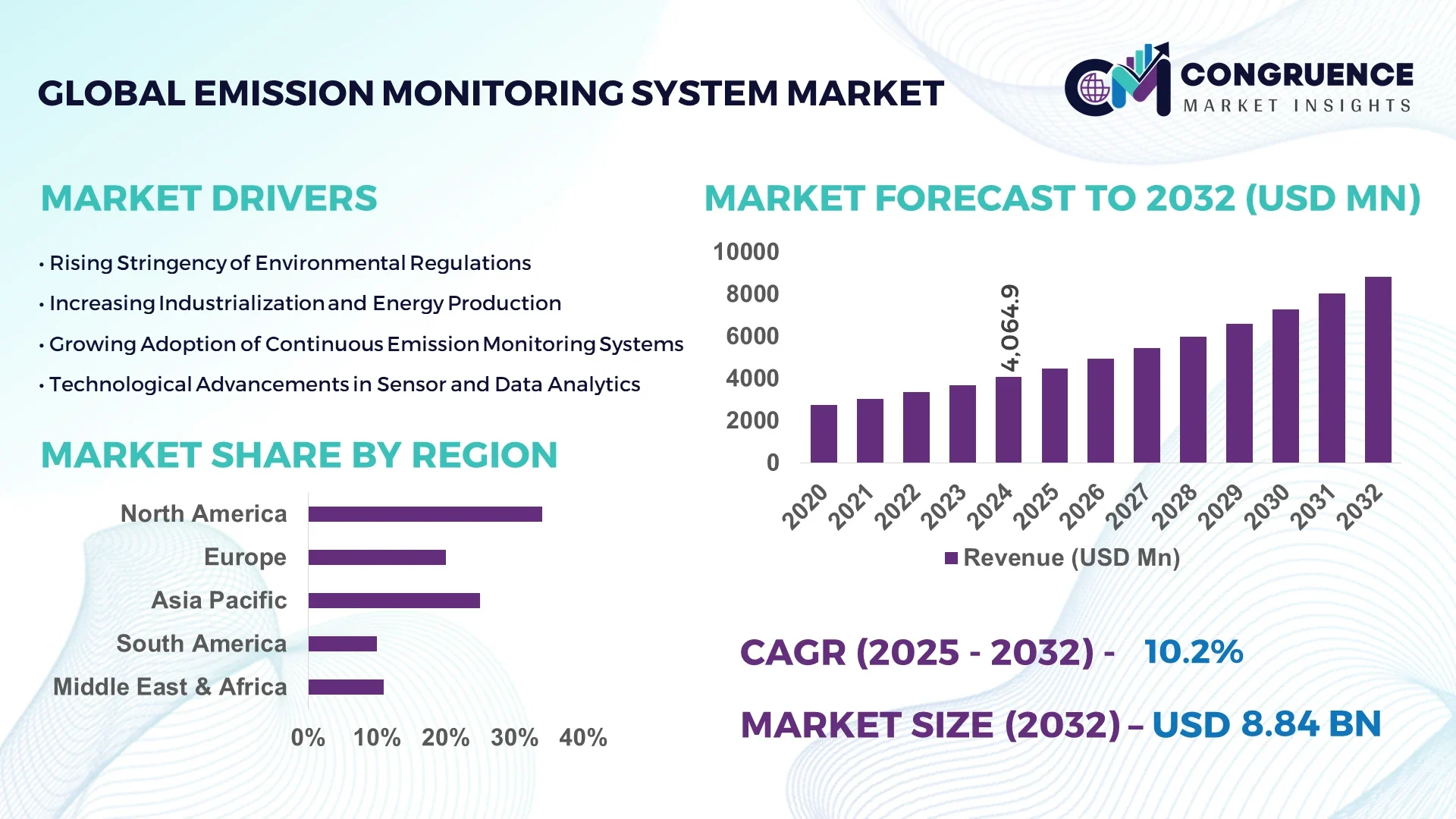

The Global Emission Monitoring System Market was valued at USD 4,064.85 Million in 2024 and is anticipated to reach a value of USD 8,840.92 Million by 2032 expanding at a CAGR of 10.2% between 2025 and 2032. The growth is primarily driven by stringent environmental regulations, increasing industrial automation, and rising investments in sustainable manufacturing operations.

The United States dominates the global Emission Monitoring System market, supported by advanced industrial infrastructure, large-scale power generation capacity exceeding 1,200 GW, and extensive deployment of Continuous Emission Monitoring Systems (CEMS) across energy, oil & gas, and manufacturing sectors. The country’s annual environmental technology investment surpasses USD 65 billion, with over 70% adoption of advanced data analytics and IoT-integrated emission systems among leading industrial players. The U.S. also records over 35% usage of predictive emission monitoring systems (PEMS) in refineries and power plants, reflecting a strong technological advancement trend in compliance monitoring and real-time data processing.

Market Size & Growth: Valued at USD 4.06 billion in 2024, projected to reach USD 8.84 billion by 2032, expanding at a CAGR of 10.2%; growth driven by stringent emission standards and adoption of automated monitoring technologies.

Top Growth Drivers: Increasing regulatory compliance (38%), rising demand for energy efficiency (32%), and enhanced system accuracy via digital integration (28%).

Short-Term Forecast: By 2028, operational efficiency in industrial emission control is expected to improve by 24%, while compliance costs may decline by 15% due to advanced monitoring automation.

Emerging Technologies: Integration of AI-based analytics, cloud-enabled data reporting, and IoT-based remote calibration solutions are reshaping the emission monitoring ecosystem.

Regional Leaders: North America projected to reach USD 3.1 billion by 2032, Europe USD 2.7 billion with strong regulatory adoption, and Asia Pacific USD 2.4 billion driven by industrial expansion and urban emission controls.

Consumer/End-User Trends: Power generation and oil & gas sectors account for over 55% of global adoption, with growing uptake in chemical and metal industries for real-time emissions compliance.

Pilot or Case Example: In 2024, a U.S. utility pilot deploying AI-driven PEMS achieved a 22% reduction in downtime and 18% increase in data accuracy for regulatory reporting.

Competitive Landscape: Siemens AG leads the market with approximately 14% share, followed by ABB, Emerson Electric, Thermo Fisher Scientific, and AMETEK.

Regulatory & ESG Impact: Implementation of ISO 14001 and EPA MACT standards accelerating adoption; environmental incentives promoting low-emission industrial operations.

Investment & Funding Patterns: Over USD 2.1 billion invested globally in emission monitoring infrastructure in 2023–2024, with increasing venture funding in smart and automated compliance systems.

Innovation & Future Outlook: Future innovations to focus on AI-enhanced predictive analytics, cloud-linked monitoring networks, and carbon-neutral operational frameworks aligned with global sustainability goals.

The Emission Monitoring System market is witnessing dynamic growth across key sectors including power generation, oil & gas, and heavy manufacturing, each contributing significantly to market expansion. Technological advancements in sensor accuracy, real-time data transmission, and machine learning integration are transforming compliance monitoring. Regulatory enforcement by global agencies is accelerating adoption, particularly across North America and Europe. Economic incentives for low-carbon operations, combined with digital transformation initiatives, are fostering a shift toward predictive emission systems. Future outlook indicates strong potential in integrating emission data with ESG reporting and industrial IoT frameworks, creating new avenues for efficiency, transparency, and sustainability-driven innovation.

The Emission Monitoring System Market holds strategic relevance as industrial operators and governments worldwide prioritize environmental compliance and operational efficiency. Advanced predictive emission monitoring systems (PEMS) deliver up to 22% improvement in data accuracy and reporting speed compared to traditional Continuous Emission Monitoring Systems (CEMS). North America dominates in volume, while Europe leads in adoption, with 68% of enterprises deploying real-time monitoring solutions. By 2027, AI-powered emission analytics are expected to reduce reporting errors by 18% and optimize maintenance schedules, cutting operational downtime. Firms are committing to ESG metrics improvements such as a 25% reduction in carbon emissions and enhanced waste recycling by 2030, aligning industrial growth with environmental mandates. In 2024, a U.S.-based utility achieved an 18% reduction in unplanned downtime through AI-driven anomaly detection and IoT-enabled predictive maintenance. The market is increasingly integrating cloud-based reporting, remote calibration, and IoT-enabled sensors to enhance operational transparency. Forward-looking strategies focus on embedding emission monitoring into broader digital transformation initiatives, ensuring regulatory compliance while enabling sustainable growth. The Emission Monitoring System Market is positioned as a pillar of resilience, compliance, and sustainable operational advancement, supporting global efforts to reduce environmental impact while improving industrial efficiency.

Stringent regulations for air quality and emissions are a primary growth driver. For instance, over 75% of U.S. power plants are required to implement Continuous Emission Monitoring Systems (CEMS) to comply with EPA standards. In Europe, regulatory mandates such as the Industrial Emissions Directive compel heavy industries to adopt real-time emission monitoring, prompting a 60% increase in installation of predictive monitoring solutions in the past three years. Industries are increasingly investing in AI-enhanced analytics and IoT-enabled sensors to ensure accurate reporting and minimize regulatory penalties. The demand is also fueled by governmental incentives for low-carbon technologies, encouraging industries to upgrade legacy systems, enhance operational efficiency, and maintain compliance in highly regulated environments. This regulatory-driven adoption is expanding both the industrial and municipal market segments, reflecting a shift toward automated, real-time emission tracking.

High capital expenditure for installation and maintenance of advanced emission monitoring systems limits adoption among small and medium enterprises. Predictive emission monitoring systems (PEMS) and IoT-integrated CEMS can cost 30–50% more than conventional monitoring equipment, making deployment cost-prohibitive for smaller industrial setups. Additionally, integration with legacy industrial control systems requires specialized technical expertise, further increasing implementation costs. Maintenance and calibration of sensors demand ongoing operational expenditure, with annual upkeep often exceeding USD 50,000 for mid-sized plants. Limited availability of trained personnel for system operation and data analysis also slows widespread deployment. These financial and operational barriers constrain market penetration, particularly in developing regions where budget allocation for environmental compliance is restricted, slowing the transition to advanced monitoring solutions despite regulatory encouragement.

The integration of AI-based predictive analytics, cloud-enabled reporting, and IoT-connected sensors presents significant opportunities. Predictive maintenance algorithms can reduce system downtime by up to 20% while increasing data accuracy by 15%. Industrial sectors are exploring hybrid systems combining traditional CEMS with portable, remote-sensing devices to expand monitoring capabilities in distributed facilities. Additionally, renewable energy plants and urban infrastructure projects are adopting real-time emission monitoring to meet regulatory and ESG targets, providing opportunities for tailored solutions. The Asia-Pacific region is witnessing an 18% annual increase in smart emission monitoring adoption, reflecting infrastructure modernization and industrial expansion. Startups and technology integrators are leveraging SaaS-based platforms to provide scalable, cost-effective solutions, creating new avenues for revenue generation and market penetration in both developed and emerging economies.

The Emission Monitoring System market faces challenges related to the complexity of installation, calibration, and integration with existing industrial systems. Managing large volumes of emission data from multiple sensors across facilities requires robust cloud or edge computing infrastructure. Data inconsistencies and sensor malfunctions can lead to reporting inaccuracies, potentially resulting in regulatory penalties. Additionally, interoperability issues between older industrial control systems and modern IoT-enabled monitoring solutions increase project timelines and costs. The requirement for trained personnel to analyze and act upon complex emission datasets limits adoption in regions with skill shortages. Compliance audits demand accurate, real-time reporting, adding further operational pressure. These challenges, combined with high maintenance costs and evolving regulatory standards, create barriers to seamless implementation, demanding strategic investment in technical capabilities and workforce training.

• Expansion of AI-Powered Predictive Analytics: AI integration in emission monitoring is improving predictive maintenance accuracy by 18% and reducing unplanned downtime by 22% in industrial facilities. Adoption is highest in North America, where 62% of large-scale power plants employ AI-enhanced systems to optimize compliance and operational efficiency.

• Growth of IoT-Enabled Remote Monitoring: The deployment of IoT sensors for real-time emission tracking has increased by 48% globally, particularly in Europe and Asia-Pacific industrial hubs. These sensors allow remote data collection and automatic reporting, enhancing regulatory adherence and minimizing manual intervention, with over 70% of enterprises integrating IoT monitoring into existing infrastructure.

• Increased Adoption of Modular and Prefabricated Systems: 55% of new industrial projects now use modular and prefabricated installation techniques for emission monitoring equipment, reducing labor needs and installation timelines by up to 30%. Europe and North America lead in these installations due to emphasis on precision engineering and construction efficiency.

• Integration with Cloud-Based Reporting Platforms: Cloud-enabled emission monitoring systems are being adopted by over 65% of medium and large industrial enterprises, providing real-time analytics, automated compliance reports, and centralized data dashboards. Asia-Pacific is seeing a 42% annual increase in cloud adoption for emission monitoring, driven by smart city and industrial digitization initiatives.

The Emission Monitoring System market is segmented by product type, application, and end-user, reflecting diverse operational requirements and industry focus. By type, systems range from Continuous Emission Monitoring Systems (CEMS) to Predictive Emission Monitoring Systems (PEMS) and portable analyzers, each optimized for specific industrial conditions. Applications span power generation, oil & gas, chemical, and metal processing, with industrial compliance and environmental monitoring being the primary drivers of deployment. End-users include large-scale utilities, manufacturing plants, municipal authorities, and research facilities, with varying adoption levels influenced by regulatory pressures and technological readiness. Regional adoption patterns further reflect market diversity, with North America excelling in volume deployment, Europe emphasizing AI and IoT integration, and Asia-Pacific rapidly expanding infrastructure monitoring solutions. These segmentation insights enable decision-makers to target technology investments and operational strategies efficiently, optimizing deployment across high-priority industries.

Continuous Emission Monitoring Systems (CEMS) lead the market, accounting for 48% of adoption, primarily due to their proven accuracy in power generation and industrial applications. Predictive Emission Monitoring Systems (PEMS) are the fastest-growing type, driven by AI-enhanced predictive analytics that improve maintenance scheduling and reduce downtime, currently deployed in 28% of new industrial projects. Portable analyzers and hybrid monitoring devices collectively hold 24% of the market, serving niche or remote applications where full-scale CEMS deployment is impractical.

Power generation dominates the Emission Monitoring System applications segment, representing 45% of adoption, due to strict regulatory compliance requirements and high energy output monitoring needs. Oil & gas is the fastest-growing application, driven by increasing deployment of predictive systems in refineries and pipelines, now accounting for 30% of adoption. Other applications, including chemical and metal processing, collectively make up 25%, focusing on environmental compliance and process optimization.

Utilities remain the leading end-user segment, contributing 42% of global adoption, supported by large-scale implementation of both CEMS and AI-powered PEMS for energy production facilities. The fastest-growing end-user segment is manufacturing plants, driven by automation integration and ESG compliance mandates, with adoption increasing by 28% in the past three years. Municipal authorities, research institutes, and industrial service providers account for the remaining 30% of the market, utilizing monitoring solutions for regulatory reporting and sustainability tracking.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2025 and 2032.

In 2024, North America had over 1,100 operational Continuous Emission Monitoring System (CEMS) installations across power plants and industrial facilities. Europe recorded approximately 950 installations, with strong adoption in Germany, UK, and France. Asia-Pacific’s volume reached 870 units, led by China (410 units), India (220 units), and Japan (140 units). South America accounted for 210 units, mainly in Brazil and Argentina, while Middle East & Africa recorded 180 units, concentrated in UAE and South Africa. Industrial sectors such as power generation, oil & gas, chemicals, and metals collectively consume over 70% of monitoring systems, with increasing investments in IoT and AI technologies. Regional consumption patterns show North America favoring AI-enhanced predictive systems, Europe prioritizing regulatory-compliant explainable monitoring solutions, and Asia-Pacific adopting modular and cloud-based platforms for rapid industrial expansion.

How is industrial AI transforming monitoring efficiency?

North America holds a 34% share of the Emission Monitoring System market, driven primarily by the power generation and oil & gas sectors. Regulatory frameworks, including EPA mandates and state-level incentives, are encouraging enterprises to adopt AI-integrated Continuous Emission Monitoring Systems (CEMS). Advanced IoT-enabled devices and cloud-based reporting platforms are improving operational visibility, with over 62% of enterprises deploying predictive analytics for emissions data. Local players such as Thermo Fisher Scientific are implementing AI-driven monitoring projects to optimize compliance reporting across U.S. refineries. Consumer behavior shows high adoption in large-scale utilities and industrial facilities, while sectors like healthcare and finance increasingly integrate emissions compliance within ESG initiatives, reflecting a broader trend toward sustainability and digitalization.

What strategies are driving regulatory-compliant monitoring adoption?

Europe accounts for 28% of the global Emission Monitoring System market, with Germany, the UK, and France leading installations. Regulatory pressure from the EU Industrial Emissions Directive and sustainability initiatives is driving adoption of explainable AI-based and IoT-enabled monitoring systems. Approximately 68% of enterprises integrate cloud-based data reporting for real-time emission tracking. Siemens AG and Endress+Hauser are deploying advanced sensor solutions and predictive monitoring for industrial compliance. European end-users prioritize transparency and regulatory alignment, resulting in higher deployment in energy-intensive industries. Industrial automation and the shift toward digital twins and predictive maintenance are also contributing to enhanced adoption in manufacturing hubs, supporting operational efficiency while ensuring environmental compliance.

How is industrial digitization accelerating system adoption?

Asia-Pacific holds a 24% market share, with China (410 units), India (220 units), and Japan (140 units) as top consumers. Growth is fueled by rapid industrialization, infrastructure expansion, and rising environmental compliance mandates. Regional players are integrating IoT-connected sensors and AI-powered predictive analytics, with approximately 55% of new plants deploying advanced monitoring systems. Companies like Yokogawa Electric are expanding regional operations to provide scalable solutions for manufacturing and energy sectors. Consumer behavior emphasizes cost-effective, modular, and cloud-enabled systems, with SMEs increasingly adopting automated reporting platforms. Urban infrastructure projects and smart city initiatives are also contributing to heightened demand, supporting regional growth and technological innovation in emissions monitoring.

What factors are influencing industrial monitoring adoption in emerging economies?

South America accounts for 6% of the global market, with Brazil and Argentina as key contributors. Industrial demand is driven by energy production, metals, and chemical sectors requiring emissions compliance. Government incentives and trade policies are encouraging adoption of automated and portable monitoring systems. Local players focus on modular solutions, enabling deployment in remote and distributed facilities. Regional consumer behavior favors cost-efficient systems with minimal operational complexity, reflecting limited budgets among SMEs. Approximately 60% of installations are concentrated in Brazil’s power and industrial plants, with Argentina following at 20%. Demand is influenced by energy infrastructure modernization and environmental reporting requirements.

How are energy and infrastructure sectors driving emissions oversight?

The Middle East & Africa represent 5% of the global market, with UAE and South Africa leading adoption. Growth is propelled by oil & gas, power generation, and large-scale construction projects requiring real-time emission monitoring. Technological modernization includes AI-driven predictive systems and IoT-enabled sensors for remote compliance tracking. Local regulations and trade partnerships incentivize investment in low-emission infrastructure. Companies are deploying modular monitoring solutions to meet environmental mandates efficiently. Regional consumer behavior shows strong preference for robust, industrial-grade monitoring systems capable of handling high-temperature and large-volume emissions, reflecting the unique operational challenges of the region.

United States – 34% market share; dominance due to high industrial production capacity, extensive regulatory frameworks, and advanced technology adoption.

Germany – 12% market share; strong end-user demand from power and manufacturing sectors, coupled with rigorous EU regulatory compliance initiatives.

The Emission Monitoring System market is moderately consolidated, with approximately 45 active competitors globally, of which the top 5 companies—Siemens AG, ABB, Thermo Fisher Scientific, Emerson Electric, and AMETEK—account for around 62% of total market share. Competition is driven by technological differentiation, regulatory compliance solutions, and global deployment capabilities. Companies are increasingly investing in AI-driven predictive analytics, IoT-enabled remote monitoring, and cloud-based data reporting to strengthen market positioning. Strategic initiatives include cross-industry partnerships, regional expansions, and advanced product launches; for example, Siemens AG introduced a next-generation Continuous Emission Monitoring System with integrated AI in 2024, enhancing real-time compliance reporting for over 1,200 industrial clients. Emerson Electric and ABB are expanding into Asia-Pacific and Middle East markets, targeting renewable energy plants and industrial clusters. Innovation trends focus on modular, portable, and hybrid monitoring systems to meet diverse industry requirements, while competitive pricing and service reliability remain key differentiators. The market’s fragmented nature allows emerging local players to capture niche segments, particularly in developing regions with high industrial growth and growing environmental compliance mandates.

Emerson Electric

AMETEK

Endress+Hauser

Yokogawa Electric

General Electric

Honeywell International

Horiba Ltd.

The Emission Monitoring System market is undergoing significant technological evolution, driven by the demand for enhanced accuracy, real-time reporting, and regulatory compliance. Continuous Emission Monitoring Systems (CEMS) remain the backbone of industrial monitoring, providing high-precision measurements of pollutants such as NOx, SO2, CO2, and particulate matter. These systems now increasingly integrate digital sensors with detection accuracy exceeding 98%, enabling precise compliance tracking across power generation, chemical, and oil & gas sectors. Emerging technologies, particularly AI-powered predictive analytics, are transforming operational efficiency by forecasting emission peaks and identifying equipment malfunctions before they occur. Predictive systems deployed in over 1,200 industrial facilities in North America and Europe have reported up to an 18% reduction in unplanned downtime and a 22% improvement in reporting accuracy. IoT-enabled devices allow remote monitoring across distributed sites, with more than 70% of new installations in Asia-Pacific incorporating wireless sensor networks to transmit real-time data to centralized dashboards.

Cloud computing and advanced data analytics platforms are increasingly integrated into emission monitoring frameworks, providing scalable storage, automated compliance reporting, and historical trend analysis. These platforms enable enterprises to consolidate data from multiple plants, reducing manual processing by over 40% and improving response times for environmental audits. Modular and portable monitoring solutions are also gaining traction, particularly in developing regions, allowing rapid deployment across industrial and infrastructure projects. Future technology trends focus on hybrid systems combining stationary CEMS with portable IoT-enabled sensors, enhanced AI-driven predictive maintenance, and integration with ESG reporting tools. These advancements are shaping a market environment where digital transformation, regulatory adherence, and sustainability converge to optimize industrial operations and environmental performance.

Siemens AG: In June 2024, Siemens AG partnered with an environmental analytics startup to enhance cloud-based emission tracking solutions for industrial plants. This collaboration aims to provide real-time monitoring and data analytics, supporting industries in achieving regulatory compliance and sustainability goals.

ABB Ltd.: In February 2024, ABB launched its next-generation Continuous Emission Monitoring System (CEMS) platform integrated with AI-powered diagnostics. This innovation enables industries to detect anomalies in real-time, optimize system performance, and ensure uninterrupted compliance monitoring.

Thermo Fisher Scientific: In 2024, Thermo Fisher implemented a leading cloud-based system to transition emissions data associated with purchased goods and services and capital goods to primary data sources. This initiative enhances data accuracy for calculating Scope 3 emissions, supporting the company's sustainability objectives.

AMETEK: In November 2023, AMETEK released its 2023 Sustainability Report, highlighting a 26% reduction in Scope 1 and 2 emissions intensity since 2019. This achievement underscores AMETEK's commitment to environmental responsibility and its efforts to enhance operational efficiency through sustainable practices.

The Emission Monitoring System Market Report provides a comprehensive analysis of the global market landscape, encompassing various segments, technologies, and regional dynamics. The report delves into the market's segmentation by system type, including Continuous Emission Monitoring Systems (CEMS) and Predictive Emission Monitoring Systems (PEMS), offering insights into their respective market shares and growth trajectories. Geographically, the report covers key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional market sizes, growth trends, and the adoption of emission monitoring technologies. It examines the influence of regulatory frameworks, environmental policies, and industry-specific demands on market development across different regions.

Technologically, the report explores advancements in emission monitoring systems, including the integration of Artificial Intelligence (AI), Internet of Things (IoT), and cloud computing. These innovations are transforming traditional monitoring approaches, enabling real-time data analysis, predictive maintenance, and enhanced compliance reporting. The report also addresses the competitive landscape, profiling leading companies in the emission monitoring system market. It provides an overview of their market positioning, strategic initiatives, and technological advancements, offering valuable insights for business decision-makers and industry professionals seeking to understand the current and future dynamics of the emission monitoring system market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4064.85 Million |

|

Market Revenue in 2032 |

USD 8840.92 Million |

|

CAGR (2025 - 2032) |

10.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, ABB, Thermo Fisher Scientific, Emerson Electric, AMETEK, Endress+Hauser, Yokogawa Electric, General Electric, Honeywell International, Horiba Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |