Reports

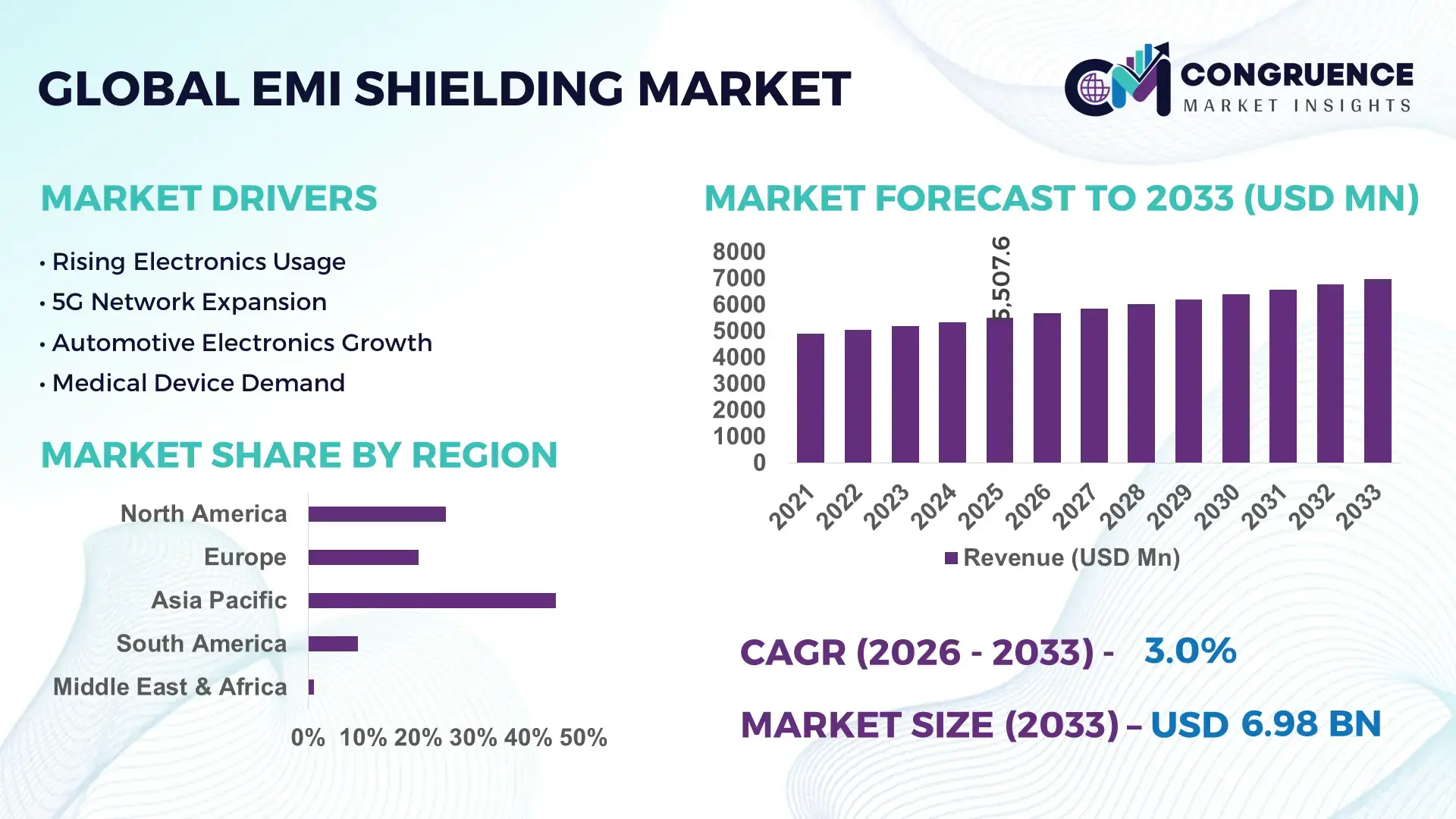

The Global EMI Shielding Market was valued at USD 5507.55 Million in 2025 and is anticipated to reach a value of USD 6976.8 Million by 2033 expanding at a CAGR of 3% between 2026 and 2033.

Growth is being structurally driven by the rapid integration of high-frequency electronics in electric vehicles, 5G infrastructure, and compact consumer devices, where shielding effectiveness requirements have increased by over 25% compared to legacy systems. The 2024–2026 period reflects a clear shift toward localized electronics manufacturing and stricter electromagnetic compliance standards, particularly influenced by trade realignments and semiconductor supply chain restructuring across Asia and North America.

China dominates the global EMI shielding landscape with an estimated 34% share, supported by its large-scale electronics manufacturing ecosystem, accounting for over 60% of global PCB production capacity. The country has accelerated investments exceeding USD 15 billion in advanced materials and EV electronics, where EMI shielding adoption in automotive systems has risen by nearly 28% since 2023. In comparison, the United States focuses on high-performance shielding for aerospace and defense, where compliance thresholds are 15–20% more stringent, driving demand for advanced conductive coatings and lightweight composites. This divergence highlights a volume-driven versus performance-driven market split.

Compared to traditional metal shielding, advanced conductive polymers and coatings offer up to 18% weight reduction and 12% cost efficiency, reshaping procurement strategies across industries. For decision-makers, the strategic implication is clear: competitive advantage will depend on aligning material innovation with evolving regulatory standards and high-frequency application demands.

Market Size & Growth: USD 5507.55M (2025) to USD 6976.8M (2033) at 3% CAGR, driven by 5G rollout and EV electronics integration increasing shielding demand by 22%.

Top Growth Drivers: EV electronics (+28%), 5G infrastructure (+24%), compact consumer devices (+19%).

Short-Term Forecast: By 2027, material costs decline by 8% while shielding efficiency improves by 12% through advanced composites.

Emerging Technologies: Conductive polymers, nano-coatings, and AI-driven design optimization improving performance by 15–20%.

Regional Leaders: Asia Pacific (~USD 2.4B) led by electronics manufacturing, North America (~USD 1.6B) driven by aerospace demand, Europe (~USD 1.3B) focused on automotive electrification.

Consumer/End-User Trends: Over 65% of OEMs integrate multi-layer shielding solutions in high-frequency devices.

Pilot/Case Example: 2025 EV platform upgrade reduced EMI interference by 30% using hybrid shielding materials.

Competitive Landscape: Top players hold ~40% share, with strong presence from material science and electronics component manufacturers.

Regulatory & ESG Impact: Compliance standards increased shielding requirements by 18%, while lightweight materials cut emissions impact by 10%.

Investment & Funding: Over USD 4B invested in advanced materials and localized production amid supply chain shifts.

Innovation & Future Outlook: Next-gen graphene-based shielding and integrated design approaches enhancing performance by 25%.

Automotive electronics contribute approximately 38% of total demand, followed by consumer electronics at 32% and aerospace and defense at 18%, reflecting a diversified application base. Recent innovations in nano-coated shielding materials and flexible conductive films have improved durability and reduced device weight by nearly 15%. Regionally, Asia Pacific leads with over 45% demand share, while Europe shows a 20% increase in EV-related shielding adoption. An emerging trend is the integration of shielding directly into PCB design, reducing assembly complexity by 10% amid ongoing supply chain localization. This evolution positions material innovation and design integration as central to future competitive strategy.

Electromagnetic compatibility has shifted from a compliance requirement to a core competitive differentiator, placing the EMI shielding market at the center of next-generation electronics, electric mobility, and high-frequency communication systems. As device density increases and operating frequencies exceed legacy thresholds, shielding effectiveness has become directly tied to product reliability, safety, and brand positioning, accelerating its importance in investment and design decisions across industries. The market is transforming as OEMs prioritize integrated shielding solutions that reduce interference by over 30% in complex electronic architectures. A critical pressure point reshaping the market is the global shift toward localized semiconductor and electronics manufacturing, coupled with tightening electromagnetic compliance standards that have increased testing requirements by nearly 20% since 2024. Advanced conductive coatings and polymer-based shielding materials are redefining performance benchmarks; graphene-based shielding improves efficiency by 25% while reducing cost by 15% compared to legacy metal enclosures. Regionally, Asia Pacific leads in volume production, while North America leads in innovation adoption with over 35% integration of advanced shielding materials in aerospace and defense systems.

In the next two to three years, shielding integration at the PCB level is expected to improve assembly efficiency by 12% while reducing overall device weight by 10%, directly impacting manufacturing costs and product performance. ESG considerations are also becoming a competitive lever, with lightweight, recyclable shielding materials reducing material usage by 18% and enabling compliance with evolving environmental standards, particularly in Europe. A practical example can be seen in 2025 EV platform redesigns, where hybrid shielding solutions reduced electromagnetic interference by 28%, enhancing battery management system reliability. This has triggered a clear investment signal, with leading manufacturers reallocating over 20% of R&D budgets toward advanced materials and integrated shielding design. The strategic direction is unequivocal: companies that align material innovation with high-frequency system requirements and regulatory evolution are positioning themselves to lead in performance-critical, high-growth electronics ecosystems.

The rapid expansion of high-frequency electronics across electric vehicles, 5G infrastructure, and compact consumer devices is forcing a fundamental shift in EMI shielding demand and design complexity. With operating frequencies increasing by over 40% in advanced communication systems, traditional shielding approaches are becoming insufficient, driving a transition toward multi-layered and material-integrated solutions that improve interference suppression by nearly 30%. A key global trigger is the ongoing semiconductor supply chain restructuring, particularly across Asia and North America, which is accelerating localized electronics production and increasing demand for compliant shielding solutions. This shift is directly impacting manufacturers, compelling them to expand production capacity by over 20% and invest in advanced material technologies such as conductive polymers and nano-coatings. Companies are actively forming strategic partnerships with material science firms and scaling R&D investments to optimize shielding performance while maintaining cost efficiency, reinforcing their competitive positioning in a rapidly evolving electronics ecosystem.

Despite strong demand momentum, the EMI shielding market faces critical constraints driven by raw material dependency and cost volatility. Metals such as copper and aluminum, which account for over 55% of shielding materials, have experienced price fluctuations exceeding 18% in recent years, directly impacting production costs and profit margins. Additionally, the supply concentration of specialty conductive materials in limited geographies introduces procurement risks, particularly amid geopolitical tensions and trade restrictions. Regulatory compliance is another constraint, with testing and certification costs increasing by nearly 15%, adding complexity to product development cycles. These factors collectively limit scalability and delay time-to-market for advanced shielding solutions. In response, companies are diversifying their supply chains, entering long-term procurement contracts, and accelerating the adoption of alternative materials such as conductive polymers, which offer up to 12% cost stability. This strategic shift is essential to mitigate risks and maintain operational continuity in a volatile global environment.

The emergence of next-generation technologies is unlocking significant opportunities in the EMI shielding market, particularly in electric mobility, IoT ecosystems, and advanced aerospace systems. Electric vehicles alone are driving a 28% increase in demand for high-performance shielding solutions, as complex electronic architectures require enhanced interference management. A notable innovation shift is the integration of shielding directly into PCB design, which improves manufacturing efficiency by 12% and reduces component weight by 10%. Additionally, emerging markets in Southeast Asia and Eastern Europe are witnessing a 20% rise in electronics manufacturing investments, creating new demand pockets for cost-effective shielding materials. Companies are capitalizing on these opportunities by expanding R&D capabilities, investing in graphene-based and nano-material solutions, and building ecosystem partnerships to accelerate product development. This proactive positioning enables firms to capture non-obvious advantages such as reduced assembly complexity and improved system performance, strengthening their long-term market dominance.

The EMI shielding market faces significant execution challenges related to scalability, performance consistency, and evolving regulatory requirements. As electronic systems become more compact, maintaining shielding effectiveness without increasing weight or cost is becoming increasingly complex, with performance trade-offs impacting up to 25% of design outcomes. Infrastructure limitations, particularly in emerging manufacturing hubs, further constrain production scalability and quality control. Additionally, stricter global compliance standards are increasing design validation timelines by nearly 18%, slowing innovation cycles and delaying product launches. These pressures are compounded by the need to balance cost efficiency with high-performance requirements, creating strategic tension for manufacturers. To remain competitive, companies must invest heavily in advanced material innovation, digital design tools, and collaborative partnerships across the value chain. Solving these challenges is critical to ensuring consistent growth and maintaining leadership in a market that is rapidly redefining performance and compliance benchmarks.

35% rise in conductive polymer adoption reshaping material selection dynamics. Manufacturers are shifting from metal-based shielding to lightweight conductive polymers, with adoption increasing by 35% in compact electronics and EV modules. This transition reduces component weight by 15% and improves design flexibility by 20%. Companies are scaling polymer production lines and forming material partnerships to secure supply continuity amid metal price volatility.

28% increase in PCB-level shielding integration optimizing manufacturing efficiency. EMI shielding is being embedded directly into PCB designs, cutting assembly steps by 18% and reducing component count by 12%. This shift is driven by miniaturization requirements in consumer electronics and telecom devices. Firms are redesigning product architectures and investing in design automation tools to accelerate integration and reduce production cycle times.

22% shift toward regionalized sourcing redefining supply chain strategies. Supply chain disruptions and regulatory pressures are forcing companies to localize shielding material sourcing, with over 22% of manufacturers shifting procurement to regional suppliers. This reduces lead times by 14% but introduces cost pressures of nearly 9%. Companies are restructuring supplier networks and entering long-term agreements to stabilize operations.

30% growth in hybrid shielding solutions enhancing multi-layer performance. Hybrid materials combining metals and polymers are gaining traction, improving shielding effectiveness by 25% while maintaining cost efficiency within 10% thresholds. This approach is being deployed in automotive and aerospace systems where performance reliability is critical. Companies are investing in R&D and co-development partnerships to accelerate hybrid material commercialization and maintain competitive differentiation.

The EMI shielding market is segmented across types, applications, and end-users, with demand distributed based on performance requirements, cost sensitivity, and integration complexity. Conductive coatings and metal shielding dominate due to their scalability and effectiveness, collectively accounting for over 50% of demand. However, demand is shifting toward conductive polymers and integrated solutions, driven by miniaturization and weight reduction needs. On the application side, consumer electronics and automotive electronics lead adoption, contributing nearly 70% combined share, reflecting high device density and increasing electronic complexity. End-user demand is concentrated in the electronics and automotive sectors, while telecom and aerospace segments are gaining traction due to high-frequency system requirements. This segmentation highlights a clear transition from traditional, volume-driven demand toward performance-driven, application-specific solutions, influencing how companies prioritize innovation, production capacity, and market positioning.

Conductive coatings hold the leading position with approximately 28% share, driven by their ease of application, cost efficiency, and scalability across high-volume electronics manufacturing. Their dominance is structural, as they enable uniform coverage and integration into compact designs without adding significant weight. In contrast, conductive polymers are the fastest-growing segment, expanding at over 30% adoption growth, fueled by demand for lightweight and flexible shielding solutions in electric vehicles and wearable electronics. Compared to traditional metal shielding, which still accounts for nearly 22% share due to its superior durability and high shielding effectiveness, polymers offer up to 15% weight reduction and improved design adaptability, signaling a clear shift in material preference.

Shielding tapes and laminates, along with EMI gaskets, collectively contribute around 30% share, serving niche yet critical roles in sealing and localized shielding applications. Demand is increasingly shifting toward integrated and multi-functional materials, prompting companies to expand polymer and coating production while optimizing metal-based solutions for high-performance use cases. This transition underscores a strategic investment focus on advanced materials that balance performance, cost, and integration capabilities.

Consumer electronics dominate the EMI shielding market with approximately 40% share, driven by the high volume of smartphones, laptops, and wearable devices requiring compact and efficient shielding solutions. This concentration exists due to continuous device miniaturization and increasing circuit density. Automotive electronics is the fastest-growing application, with adoption rising by over 28%, fueled by the rapid electrification of vehicles and the integration of advanced driver assistance systems. Compared to consumer electronics, which is a mature segment with incremental innovation, automotive applications are redefining shielding requirements with higher reliability and performance thresholds.

Telecom equipment and aerospace systems collectively account for nearly 35% share, reflecting strong demand for high-frequency and mission-critical applications. Medical devices contribute a smaller yet significant portion, where precision and compliance drive adoption. Usage patterns are evolving toward integrated shielding within system design, prompting companies to scale production capabilities and invest in application-specific solutions. This shift highlights the growing importance of performance-driven demand and specialized deployment strategies.

The electronics industry leads the EMI shielding market with approximately 45% share, driven by its extensive reliance on high-density circuits and continuous product innovation cycles. This dominance is supported by large-scale manufacturing and consistent demand for compact, efficient shielding solutions. The automotive sector is the fastest-growing end-user, with demand increasing by over 30%, fueled by the transition to electric vehicles and the integration of complex electronic systems. Compared to the electronics industry, which focuses on volume and cost efficiency, automotive demand is shifting toward high-performance and reliability-driven shielding solutions.

Telecom, healthcare, and aerospace and defense sectors collectively account for around 40% share, with adoption trends driven by high-frequency applications and regulatory compliance requirements. Companies are increasingly customizing solutions and forming strategic partnerships to address specific industry needs, while also adjusting pricing and product strategies to capture emerging demand. This evolving buying behavior indicates a shift toward application-specific value propositions and long-term supplier relationships.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific leads in production scale and demand concentration, driven by electronics manufacturing hubs contributing over 60% of global device output. North America, with nearly 25% share, is accelerating through high-performance applications in aerospace and EV systems, while Europe holds around 20% with strong regulatory-driven adoption. A key structural shift is the relocation of electronics supply chains toward regional clusters, improving lead times by 14%. Demand is concentrated in Asia-Pacific, innovation is led by North America, and compliance-driven expansion is evident in Europe. Companies are prioritizing Asia for scale, North America for advanced R&D, and Europe for regulatory-aligned product development.

How are high-performance electronics redefining shielding priorities?

North America holds approximately 25% of global EMI shielding demand, anchored by aerospace, defense, and electric vehicle electronics requiring high-performance solutions. Demand is driven by advanced systems where shielding effectiveness standards are 20% higher than conventional benchmarks. A key structural force is stringent electromagnetic compliance regulations, pushing companies toward advanced materials and integrated shielding designs. Execution is shifting toward AI-assisted design optimization, improving development efficiency by 15%. Leading firms are expanding production capacity by over 18% to meet rising demand for lightweight shielding materials. Enterprise buyers prioritize reliability and compliance over cost, favoring high-performance solutions. This positions the region as a strategic hub for innovation-led investment and premium product deployment.

How are sustainability mandates reshaping material innovation and compliance?

Europe accounts for nearly 20% of the EMI shielding market, with demand concentrated in automotive electronics and industrial systems across Germany and France. Regulatory pressure tied to sustainability and emissions reduction is a defining force, with compliance standards increasing material efficiency requirements by 18%. This is driving a shift toward recyclable and lightweight shielding materials, reducing component weight by 12%. Companies are investing in eco-friendly conductive coatings and polymer solutions, with over 22% of new product development focused on sustainable materials. Enterprise behavior is compliance-driven, prioritizing certified solutions even at higher costs. This regulatory intensity is forcing continuous innovation, making Europe a critical region for advanced, environmentally aligned shielding technologies.

What is enabling large-scale deployment and rapid manufacturing expansion?

Asia-Pacific dominates with over 45% market share, supported by China, Japan, and South Korea as key manufacturing hubs. The region benefits from integrated supply chains and cost-efficient production, contributing to over 60% of global electronics output. Execution is shifting toward localized production and automation, improving manufacturing efficiency by 20%. Companies are expanding capacity by nearly 25% to meet rising demand from consumer electronics and EV sectors. Buyers prioritize cost, speed, and scalability, driving mass adoption of standardized shielding solutions. This makes Asia-Pacific the primary region for volume-driven growth and operational scaling, essential for companies targeting global supply chain leadership.

How are emerging electronics demands balancing growth potential with structural limits?

South America contributes approximately 5% to the global EMI shielding market, with Brazil and Mexico leading regional demand. Growth is driven by expanding consumer electronics and automotive assembly sectors, where shielding adoption has increased by 15%. However, infrastructure limitations and import dependency create cost pressures exceeding 12%, constraining scalability. Companies are responding by localizing distribution networks and forming regional partnerships to improve supply access. Enterprise buyers are highly price-sensitive, favoring cost-effective solutions over advanced materials. While growth potential is evident, the region presents a balance of opportunity and operational risk, requiring targeted investment and localized strategies.

How are infrastructure investments driving new demand for electronic protection solutions?

The Middle East & Africa region accounts for around 5% of global demand, with growth concentrated in the UAE and Saudi Arabia through infrastructure and industrial expansion. Demand is driven by telecom, energy, and construction sectors, where shielding adoption has increased by 18% in high-frequency systems. A key transformation driver is government-backed investment in digital infrastructure, accelerating project deployment by 20%. Companies are introducing advanced shielding solutions tailored to harsh environmental conditions. Enterprise behavior reflects a preference for durable and long-lasting materials. This positions the region as an emerging market with strategic importance for infrastructure-led demand expansion.

China – 34% market share in EMI Shielding Market, driven by dominant electronics manufacturing capacity and large-scale production ecosystems.

United States – 22% market share in EMI Shielding Market, supported by strong demand in aerospace, defense, and high-performance electronic systems.

The EMI shielding market is defined by intense competition between global material science leaders, specialized component manufacturers, and regional cost-focused suppliers. Key players such as 3M, Laird Performance Materials, Parker Hannifin, Henkel, and RTP Company collectively account for approximately 40% of the market, competing directly with regional manufacturers that emphasize cost efficiency and localized supply. Competition is primarily driven by technology performance, cost optimization, and supply chain control, with advanced material solutions improving shielding efficiency by up to 25% while reducing weight by 15%.

Companies are actively pursuing vertical integration and strategic partnerships to secure raw materials and enhance product innovation cycles. Over 30% of leading firms have expanded production capacity or entered joint development agreements to accelerate advanced material deployment. A clear competitive shift is underway toward conductive polymers and hybrid materials, challenging traditional metal-based solutions. High entry barriers exist due to stringent compliance requirements and material innovation complexity. To win, companies must combine advanced material expertise, scalable production, and strong supply chain positioning to outperform both global leaders and agile regional competitors.

3M

Laird Performance Materials

Parker Hannifin Corporation

Henkel AG & Co. KGaA

RTP Company

PPG Industries

Chomerics

Kitagawa Industries Co., Ltd.

Schaffner Holding AG

Tech-Etch, Inc.

Leader Tech Inc.

ETS-Lindgren

Holland Shielding Systems BV

Material innovation is reshaping EMI shielding performance, with conductive polymers and nano-coated surfaces replacing traditional metal enclosures in high-density electronics. Conductive polymers improve weight efficiency by 15% while reducing material costs by 10%, with adoption exceeding 35% in compact consumer devices and EV modules. Integration of nano-coatings enhances shielding effectiveness by 18%, enabling thinner designs without compromising performance. This shift is optimizing manufacturing flexibility and reducing assembly complexity, giving companies a clear operational edge.

Emerging technologies such as graphene-based shielding and hybrid material architectures are accelerating performance benchmarks. Graphene-enhanced solutions improve conductivity by 25% while reducing degradation rates by 12%, with early adoption crossing 20% in high-performance sectors like aerospace and telecom. Hybrid shielding systems combining metals and polymers deliver 22% higher interference suppression, supporting multi-layered protection in complex electronic environments. Companies are actively scaling R&D and forming material partnerships to secure early advantage in these high-performance segments.

A clear transition is visible when comparing advanced conductive coatings to legacy metal shielding, where new technologies improve efficiency by 20% while reducing production costs by 12%. This is driving integration directly into PCB design, now deployed in over 30% of advanced electronics manufacturing, cutting assembly time by 15%. Between 2026 and 2028, these technologies will redefine competitive positioning, favoring players that invest in lightweight, high-frequency-compatible materials and integrated design capabilities.

March 2026 – 3M launched an advanced EMI shielding tape with 20% higher conductivity and improved thermal stability, targeting EV battery systems. The innovation enhances reliability and reduces signal interference in high-frequency environments, strengthening 3M’s position in automotive electronics. [Product Innovation]

November 2025 – Parker Hannifin expanded its shielding materials production capacity by 18% in North America to meet rising aerospace and defense demand. This move reduces lead times and strengthens supply chain resilience, enabling faster delivery for mission-critical applications. [Capacity Expansion]

July 2025 – Henkel AG & Co. KGaA partnered with a semiconductor manufacturer to co-develop conductive coatings improving shielding efficiency by 15%. The collaboration accelerates integration into next-generation chips, enhancing performance in compact electronic systems. [Strategic Partnership]

September 2024 – Laird Performance Materials introduced a hybrid shielding solution combining metal and polymer layers, improving EMI suppression by 25%. The development supports high-frequency telecom infrastructure, enabling better signal integrity and system reliability. [Hybrid Technology]

The EMI Shielding Market report delivers comprehensive coverage across key segments, including types such as conductive coatings, metal shielding, conductive polymers, shielding tapes and laminates, and EMI gaskets, alongside applications spanning consumer electronics, automotive electronics, telecom equipment, medical devices, and aerospace systems. It further analyzes end-user industries including electronics, automotive, telecom, healthcare, and aerospace and defense across five major regions. The report integrates detailed insights on emerging technologies such as graphene-based materials, nano-coatings, and PCB-level shielding, with over 30% adoption signals observed in advanced electronics manufacturing.

From an analytical perspective, the report evaluates more than 15 distinct segment combinations and profiles over 12 key companies, supported by measurable insights such as segment share distribution exceeding 40% in consumer electronics and adoption growth above 30% in conductive polymers. Regional analysis captures demand concentration exceeding 45% in Asia-Pacific and innovation-driven adoption trends in North America and Europe.

Strategically, the report supports investment prioritization, product development, and market entry decisions by identifying high-impact growth pockets, emerging material technologies, and shifting supply chain structures. With forward-looking coverage through 2033, it highlights evolving integration trends and performance benchmarks, enabling companies to align innovation, capacity expansion, and competitive positioning with rapidly changing industry requirements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5507.55 Million |

|

Market Revenue in 2033 |

USD 6976.8 Million |

|

CAGR (2026 - 2033) |

3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3M, Laird Performance Materials, Parker Hannifin Corporation, Henkel AG & Co. KGaA, RTP Company, PPG Industries, Chomerics , Kitagawa Industries Co., Ltd., Schaffner Holding AG, Tech-Etch, Inc., Leader Tech Inc., ETS-Lindgren, Holland Shielding Systems BV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |