Reports

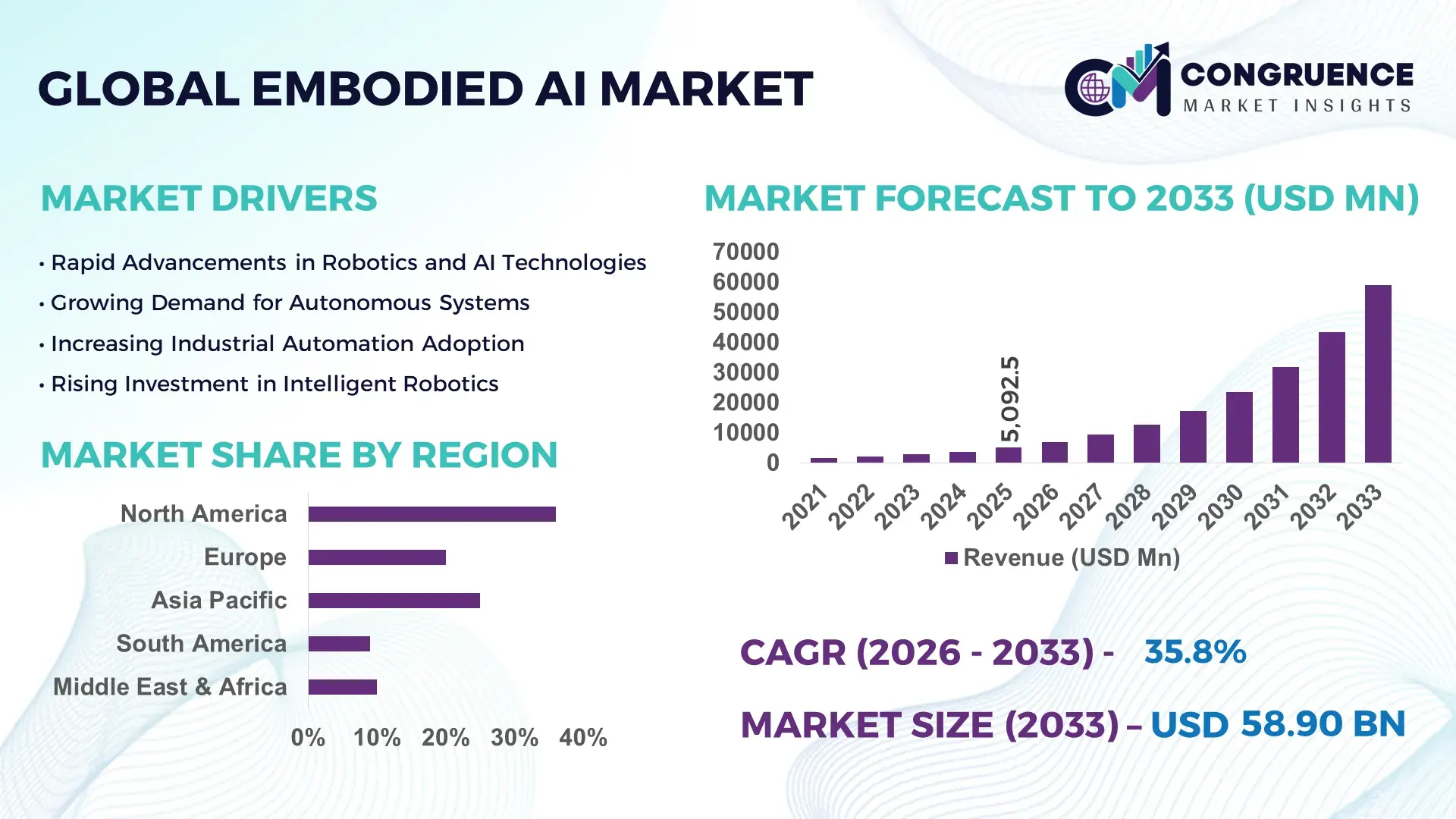

The Global Embodied AI Market was valued at USD 5092.5 Million in 2025 and is anticipated to reach a value of USD 58901.8 Million by 2033 expanding at a CAGR of 35.8% between 2026 and 2033. Rapid integration of intelligent robotics across manufacturing, logistics, healthcare, and consumer automation is accelerating market expansion worldwide.

The United States remains a central hub for embodied artificial intelligence development with more than 45% of advanced robotics research labs operating in collaboration with AI startups and major technology firms. Over 320 robotics-focused AI companies in the country are actively developing autonomous service robots, warehouse robots, and humanoid platforms. Industrial robotics deployment surpassed 420,000 installed units across U.S. manufacturing facilities in 2025, while venture funding for AI-driven robotics exceeded USD 9 billion during the same year. Embodied AI applications are widely adopted in logistics automation, with nearly 38% of large distribution centers integrating autonomous mobile robots and AI-enabled robotic manipulators to improve order fulfillment accuracy and operational efficiency.

• Market Size & Growth: The embodied AI market reached USD 5092.5 million in 2025 and is projected to grow to USD 58901.8 million by 2033, expanding at 35.8% CAGR, driven by large-scale adoption of autonomous robotics across manufacturing, logistics automation, and intelligent service systems.

• Top Growth Drivers: Autonomous robotics adoption increased by 42%, warehouse automation efficiency improved by 35%, and industrial AI-driven productivity gains exceeded 28% in global manufacturing facilities.

• Short-Term Forecast: By 2028, embodied AI–enabled robotics systems are expected to reduce operational costs in automated warehouses by nearly 30% while improving real-time task execution efficiency by approximately 40%.

• Emerging Technologies: Key innovations include reinforcement learning robotics, AI vision-guided manipulation systems, digital twin robotics simulations, and multimodal sensor fusion technologies.

• Regional Leaders: North America is projected to exceed USD 21 billion by 2033 due to advanced robotics R&D; Asia-Pacific is expected to surpass USD 24 billion driven by manufacturing automation; Europe could reach USD 13 billion supported by smart factory initiatives.

• Consumer/End-User Trends: Manufacturing, healthcare robotics, logistics automation, and smart home robotics account for over 65% of embodied AI deployments globally, with enterprise automation adoption rising rapidly.

• Pilot or Case Example: In 2024, a major logistics automation project deployed autonomous embodied AI robots in a European distribution hub, reducing manual picking errors by 32% and improving warehouse throughput by 27%.

• Competitive Landscape: Leading market participants collectively hold approximately 30% of industry influence, with major technology firms and robotics innovators competing through advanced humanoid robotics and AI automation systems.

• Regulatory & ESG Impact: Governments are introducing AI governance frameworks and robotics safety standards, while robotics manufacturers are committing to energy-efficient hardware designs reducing power consumption by up to 20%.

• Investment & Funding Patterns: Global investment in embodied AI startups and robotics platforms surpassed USD 15 billion between 2023 and 2025, with venture capital strongly supporting humanoid robotics and autonomous machine development.

• Innovation & Future Outlook: Continuous innovation in edge AI computing, collaborative robotics platforms, and embodied AI training models is expected to drive next-generation autonomous machines capable of complex physical interaction in industrial and consumer environments.

Embodied AI adoption is accelerating across key sectors including industrial robotics, healthcare assistance robots, service automation, and autonomous logistics platforms. Manufacturing currently represents nearly 40% of embodied AI deployments, followed by logistics and warehousing at approximately 25%. Recent innovations include multimodal perception systems and generative AI-based robotic learning frameworks that allow machines to adapt to real-world environments. Governments in Asia and Europe are also introducing AI robotics development programs supporting advanced automation ecosystems and intelligent infrastructure development.

The embodied AI market is emerging as a strategic pillar for next-generation automation, combining artificial intelligence with physical robotic systems capable of interacting with real-world environments. AI-driven robotics platforms are transforming industrial productivity, logistics efficiency, and intelligent service delivery across multiple sectors. Reinforcement learning robotics delivers nearly 40% improvement in task adaptability compared to traditional rule-based automation systems, enabling machines to perform complex manipulation and navigation tasks. Asia-Pacific dominates in robotics production volume due to strong manufacturing ecosystems, while North America leads in enterprise adoption with over 46% of large technology firms deploying AI-enabled robotics for warehouse automation and smart manufacturing operations. By 2027, embodied AI-powered automation platforms are expected to improve industrial productivity by nearly 35% while reducing operational downtime by up to 25%.

Compliance and sustainability considerations are also influencing market strategies. Robotics manufacturers are committing to ESG-aligned manufacturing practices, including energy-efficient robotic components capable of reducing industrial power consumption by approximately 18% by 2030. A micro-scenario demonstrating the technology’s impact occurred in 2024 when a major robotics deployment in Japan’s automotive sector integrated embodied AI robots into assembly lines, achieving a 29% improvement in operational efficiency and a 22% reduction in manual inspection time. With rapid innovation in multimodal robotics intelligence, the Embodied AI Market is expected to evolve as a core driver of resilient automation ecosystems, regulatory compliance, and sustainable industrial transformation.

Global manufacturing industries are increasingly adopting AI-enabled robotics to improve operational efficiency and reduce manual labor dependency. More than 3.9 million industrial robots were operational worldwide by 2024, with a significant share incorporating embodied AI technologies for adaptive movement, object recognition, and autonomous decision-making. Advanced robotic manipulators integrated with AI vision systems can improve production accuracy by nearly 35% while reducing operational errors by 20%. The expansion of smart factories, particularly in Asia and North America, has significantly increased the deployment of collaborative robots and intelligent autonomous machines capable of handling complex industrial tasks.

Developing embodied AI systems requires advanced robotics hardware, sophisticated sensor arrays, and high-performance AI computing infrastructure, resulting in substantial development costs. A single humanoid robotics prototype can exceed development costs of USD 100,000 due to complex actuator systems, AI training models, and real-time computing capabilities. Additionally, training AI models for real-world physical interaction requires extensive datasets and simulation environments, which significantly increases research investment. Small and mid-sized enterprises often face financial barriers when adopting embodied AI robotics platforms due to infrastructure requirements and integration complexities.

The rapid expansion of autonomous robotics across logistics, healthcare, agriculture, and service industries is creating significant opportunities for embodied AI technologies. Autonomous mobile robots in warehouses have demonstrated productivity improvements of nearly 40% by optimizing inventory movement and order fulfillment operations. Healthcare institutions are also adopting embodied AI-enabled surgical assistants and patient care robots, improving operational precision and reducing procedure times by approximately 15%. Additionally, agricultural robotics equipped with AI perception systems are capable of identifying crop conditions and performing precision farming tasks, opening new avenues for large-scale embodied AI deployment globally.

The deployment of embodied AI systems in real-world environments raises complex safety, ethical, and regulatory considerations. Governments and industry bodies are developing new robotics safety standards, requiring manufacturers to ensure fail-safe mechanisms, human-robot interaction protocols, and compliance with AI governance regulations. Testing and certification procedures for advanced robotics platforms can extend development timelines by several months. Additionally, concerns related to workforce displacement and data privacy are prompting stricter regulatory oversight, which may slow the commercialization of embodied AI systems in sensitive sectors such as healthcare, defense, and public infrastructure.

• Rapid Expansion of Autonomous Robotics in Logistics and Warehousing:

Embodied AI-powered autonomous mobile robots are transforming logistics operations across global supply chains. More than 38% of large distribution centers worldwide integrated AI-enabled robotic systems by 2025 to automate inventory handling and order fulfillment. Advanced robotic picking systems have improved warehouse throughput by nearly 35% while reducing operational errors by approximately 28%. In Asia-Pacific logistics hubs, over 120,000 autonomous warehouse robots were deployed across e-commerce facilities, significantly accelerating fulfillment speed and reducing manual labor dependency in high-volume logistics environments.

• Growing Deployment of Humanoid Robots in Industrial and Service Sectors:

Humanoid robotics platforms integrated with embodied AI capabilities are gaining strong adoption in manufacturing and service automation. Over 65% of robotics research programs globally are now focused on developing humanoid robots capable of performing complex manipulation and mobility tasks. Industrial trials conducted in 2024 demonstrated that humanoid robots improved repetitive task efficiency by nearly 30% in automotive assembly lines. Additionally, more than 150 pilot projects across Europe and North America are testing humanoid service robots in hospitality, healthcare support, and retail assistance environments.

• Integration of Multimodal AI Perception and Sensor Fusion Technologies:

Embodied AI systems increasingly rely on multimodal perception combining computer vision, tactile sensors, and real-time environmental mapping. Robotics platforms equipped with advanced sensor fusion technologies have demonstrated a 40% improvement in object recognition accuracy compared to traditional machine vision systems. In smart manufacturing facilities, nearly 45% of newly installed collaborative robots utilize AI-driven perception systems capable of identifying over 500 object variations in dynamic production environments, significantly improving automation flexibility and machine decision-making capabilities.

• Rise of Edge AI and Real-Time Robotic Decision Systems:

Edge computing is becoming a critical technology enabling embodied AI robots to process data locally with minimal latency. Over 52% of advanced robotics platforms deployed in 2025 incorporated edge AI processors to support real-time decision-making and autonomous navigation. Industrial tests show that edge-enabled embodied AI robots can reduce response latency by nearly 60% compared to cloud-dependent robotics systems. This capability is particularly valuable in autonomous vehicles, warehouse robotics, and industrial inspection robots where rapid environmental adaptation is essential for operational safety and efficiency.

The embodied AI market is segmented based on type, application, and end-user industries, reflecting the diverse adoption of intelligent robotics across global sectors. Hardware components, AI software platforms, and integrated robotic systems represent the core type categories driving innovation. Applications span manufacturing automation, logistics robotics, healthcare assistance, and service robotics, where intelligent machines perform physical tasks with adaptive learning capabilities. End-user adoption is strongest among manufacturing enterprises, e-commerce logistics operators, and healthcare institutions deploying robotics for operational efficiency and workforce support. Increasing integration of AI-driven robotics across smart factories and autonomous service environments continues to reshape global market segmentation patterns.

Embodied AI solutions are primarily categorized into robotics hardware platforms, AI software frameworks, and integrated robotic systems combining sensors, computing modules, and machine learning algorithms. Robotics hardware platforms currently account for approximately 48% of overall adoption, driven by rising deployment of autonomous mobile robots, robotic manipulators, and humanoid robotics systems across manufacturing and logistics sectors. These platforms provide the physical structure enabling AI-driven machines to interact with real-world environments. Integrated robotic systems represent the fastest-growing segment, expanding at nearly 37% CAGR as enterprises demand complete automation solutions combining robotics hardware, perception sensors, and advanced AI control software. The rapid growth is supported by the need for scalable industrial automation and intelligent robotics ecosystems. AI software frameworks and simulation environments collectively contribute around 24% of the segment, supporting robot learning models, motion planning algorithms, and reinforcement learning simulations.

Manufacturing automation remains the leading application for embodied AI technologies, accounting for nearly 41% of global adoption. Smart factories are increasingly integrating AI-enabled robotic systems capable of adaptive assembly, quality inspection, and material handling. Robotics systems equipped with advanced perception algorithms can identify product defects with more than 95% accuracy, improving manufacturing efficiency and reducing production downtime. Healthcare robotics is currently the fastest-growing application segment, expanding at approximately 36% CAGR as hospitals deploy embodied AI systems for surgical assistance, patient mobility support, and automated medication handling. These intelligent machines are designed to improve procedural precision and reduce clinical workload. Other important applications include logistics automation, agricultural robotics, and service robots used in hospitality and retail environments, collectively accounting for nearly 34% of the application landscape.

Manufacturing enterprises represent the largest end-user segment in the embodied AI market, accounting for nearly 44% of industry adoption due to the increasing deployment of intelligent robotic systems in production lines and smart factory environments. These robots enhance productivity, reduce workplace injuries, and support continuous manufacturing operations through autonomous decision-making capabilities. Healthcare institutions are emerging as the fastest-growing end-user segment with an estimated growth rate of around 34% CAGR. Hospitals are increasingly adopting embodied AI robots for surgical assistance, patient monitoring, and hospital logistics automation, improving treatment efficiency and clinical workflow management. Other significant end-users include logistics and e-commerce companies, retail businesses, and agricultural enterprises, collectively contributing around 37% of the overall market adoption as intelligent robotics systems improve operational efficiency across these industries.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 38% between 2026 and 2033.

North America leads global embodied AI adoption with more than 520 robotics research labs and over 45,000 AI engineers working on robotics intelligence systems. Asia-Pacific continues expanding through large-scale automation, where China alone operates more than 1.7 million industrial robots and Japan produces over 45,000 robots annually. Europe contributes nearly 24% of global deployments through more than 300 smart factory projects and robotics innovation programs. South America accounts for around 6% of installations led by Brazil’s industrial automation sector, while the Middle East & Africa represent approximately 5% of global deployments supported by more than 80 smart infrastructure and robotics-enabled logistics projects.

How Are Advanced Robotics and Intelligent Automation Transforming Enterprise Operations?

North America holds approximately 36% of the global embodied AI market adoption driven by advanced robotics research, enterprise digital transformation, and large-scale automation programs. The United States contributes nearly 78% of regional deployments while Canada represents around 12%, supported by more than 300 robotics innovation startups and advanced AI research centers. Manufacturing, logistics, and healthcare sectors collectively account for over 60% of embodied AI implementations across the region. Government initiatives supporting AI innovation allocate more than USD 2 billion annually toward robotics research and automation infrastructure. Boston Dynamics has deployed autonomous robotic inspection systems across more than 1,000 industrial facilities improving operational monitoring efficiency by nearly 25%. Enterprise behavior across the region demonstrates strong adoption in healthcare diagnostics, warehouse automation, and financial technology operations where AI-driven robotics improves operational productivity and reduces manual process dependency.

What Factors Are Accelerating Intelligent Robotics Integration Across Industrial Economies?

Europe represents nearly 24% of the global embodied AI deployment landscape supported by advanced manufacturing ecosystems and strong regulatory oversight. Germany leads regional adoption with approximately 40% of industrial robotics installations followed by the United Kingdom at about 18% and France at roughly 15%. Automotive manufacturing, electronics production, and smart factory automation collectively drive nearly 50% of embodied AI demand across the region. Regulatory frameworks encouraging explainable artificial intelligence and robotics safety compliance have accelerated enterprise adoption of responsible AI technologies. Sustainability programs across the European Union have also promoted energy-efficient robotics systems in more than 200 industrial modernization projects. ABB Robotics continues expanding intelligent robotic automation solutions across European manufacturing facilities while enterprise consumers increasingly prioritize transparent and explainable embodied AI systems due to regulatory and compliance requirements influencing technology purchasing behavior.

Why Is Intelligent Robotics Deployment Accelerating Across Industrial Powerhouses?

Asia-Pacific accounts for nearly 29% of global embodied AI installations and represents one of the largest robotics manufacturing hubs worldwide. China, Japan, and South Korea collectively contribute more than 70% of regional robotics production capacity while China alone operates over 1.7 million industrial robots across electronics, automotive, and consumer goods factories. Japan remains a global leader in humanoid robotics innovation with more than 30 major robotics development companies operating in Tokyo and Osaka. Technology clusters in Shenzhen, Seoul, and Tokyo host more than 900 robotics startups focusing on AI-driven automation solutions. SoftBank Robotics has deployed humanoid robots across more than 2,500 retail and hospitality locations across the region, demonstrating strong commercial adoption. Consumer and enterprise technology behavior across the region is strongly influenced by rapid e-commerce growth, mobile technology ecosystems, and high acceptance of robotics-based service automation.

How Are Emerging Automation Technologies Supporting Industrial Transformation?

South America contributes approximately 6% of global embodied AI deployments with Brazil representing nearly 52% of regional installations and Argentina contributing about 18%. Industrial sectors such as automotive production, mining operations, and energy infrastructure are the primary drivers of embodied AI adoption across the region. Government technology modernization programs have supported automation adoption through industrial productivity initiatives and robotics training programs. Brazil has introduced national digital transformation incentives encouraging companies to integrate intelligent robotics into manufacturing facilities. Several industrial automation providers have introduced AI-powered robotic inspection systems used in mining and energy operations to improve safety monitoring and reduce manual inspections by nearly 30%. Enterprise adoption patterns across the region show increasing reliance on robotics for industrial monitoring, infrastructure management, and language-based service automation in Portuguese and Spanish-speaking markets.

What Role Is Intelligent Automation Playing in Infrastructure and Energy Transformation?

The Middle East & Africa region represents approximately 5% of global embodied AI adoption driven by large-scale infrastructure modernization and smart city initiatives. The United Arab Emirates and Saudi Arabia account for more than 60% of regional robotics deployments, particularly in logistics automation, energy infrastructure inspection, and public service robotics. Autonomous inspection robots used in oil and gas facilities have reduced maintenance inspection times by nearly 35% while improving operational safety monitoring. Construction automation systems using embodied AI robots are increasingly used in major infrastructure projects across the Gulf region. Robotics innovation initiatives within the United Arab Emirates have introduced service robots in airports, shopping malls, and public transport hubs. Regional consumer behavior increasingly favors intelligent automation technologies that improve infrastructure efficiency, urban mobility services, and energy sector operations across rapidly modernizing cities.

• United States – 34% market share: The country dominates the embodied AI market through strong robotics research infrastructure, high enterprise automation adoption, and significant venture capital investment supporting robotics innovation.

• China – 28% market share: China leads embodied AI manufacturing capacity and industrial robotics deployment with more than 1.7 million robots operating across large-scale smart manufacturing ecosystems.

The embodied AI market is moderately fragmented with more than 180 active technology companies developing robotics platforms, AI software frameworks, and autonomous machine systems. The top five companies collectively account for approximately 32% of the overall competitive landscape, while numerous emerging robotics startups continue to introduce innovative technologies. Competition is driven by rapid advancements in humanoid robotics, autonomous navigation platforms, and AI-powered perception systems capable of improving machine interaction with real-world environments. Strategic collaborations between robotics manufacturers and artificial intelligence developers increased by nearly 40% between 2023 and 2025 as companies accelerated commercialization of intelligent robotics systems. More than 70 robotics prototypes and AI-powered automation platforms were introduced globally during the same period, highlighting strong innovation momentum as companies compete to develop scalable embodied AI technologies for industrial automation, logistics robotics, healthcare assistance, and service automation applications.

NVIDIA

Boston Dynamics

ABB Robotics

SoftBank Robotics

Tesla

Agility Robotics

Sanctuary AI

Unitree Robotics

Hanson Robotics

UBTECH Robotics

KUKA Robotics

FANUC Corporation

Embodied AI technologies combine artificial intelligence with physical robotic systems capable of perceiving, learning, and interacting with real-world environments. Recent advancements in multimodal perception systems have significantly enhanced robotic awareness by integrating computer vision, tactile sensing, LiDAR, and environmental mapping technologies. Modern embodied AI robots can process more than 30 sensor inputs simultaneously, allowing machines to detect obstacles, identify objects, and adapt to changing environments in real time. Vision-based AI models used in robotics have achieved object recognition accuracy exceeding 96%, enabling reliable performance in manufacturing inspection and logistics automation tasks.

Edge AI computing has also become a critical technology for embodied robotics. Over 50% of newly deployed industrial robots now integrate edge processors capable of performing local AI inference with latency below 20 milliseconds, allowing robots to respond to dynamic environments without cloud dependency. Reinforcement learning algorithms are increasingly used to train robotic systems in simulation environments where robots can complete over 10 million virtual training cycles before real-world deployment.

Digital twin technology is another major innovation supporting embodied AI development. Industrial robotics manufacturers are deploying digital twin simulation platforms capable of modeling entire production lines, allowing engineers to test robotic operations and optimize automation workflows before installation. Collaborative robotics platforms are also evolving rapidly, with advanced cobots capable of safely working alongside humans while maintaining interaction response times below 0.1 seconds. These technological advancements are enabling embodied AI systems to expand into complex applications including autonomous logistics, precision manufacturing, healthcare robotics, and intelligent service automation.

• In March 2024, NVIDIA introduced the GR00T foundation model for humanoid robots alongside its Isaac robotics platform, enabling robots to understand natural language commands and perform complex tasks such as grasping and object manipulation using multimodal generative AI. Source: www.nvidia.com

• In February 2024, Figure AI announced a strategic partnership with OpenAI to develop advanced AI models for humanoid robots, integrating natural language reasoning and real-world task execution. The collaboration aims to enhance robot intelligence for industrial and logistics applications. Source: www.figure.ai

• In September 2024, Agility Robotics expanded production of its Digit humanoid robot at a new manufacturing facility in Oregon designed to produce more than 10,000 robots annually, targeting large-scale deployment in warehouse automation and logistics operations.

• In April 2025, Boston Dynamics introduced enhanced AI-enabled capabilities for its Atlas humanoid robot, demonstrating advanced mobility, object manipulation, and autonomous task execution designed for industrial automation and complex manufacturing environments.

The Embodied AI Market Report provides a comprehensive analysis of technologies that integrate artificial intelligence with physical robotic systems capable of interacting with real-world environments. The report evaluates key segments including robotics hardware platforms, AI software frameworks, perception systems, and integrated embodied AI solutions used across industrial and service applications. It covers major technology categories such as reinforcement learning robotics, multimodal perception systems, edge AI computing, digital twin simulation platforms, and collaborative robotic systems designed for human-machine interaction.

The report analyzes multiple application domains including manufacturing automation, logistics and warehouse robotics, healthcare assistance robots, agricultural automation, and service robotics used in retail and hospitality environments. Manufacturing accounts for nearly 40% of global embodied AI adoption, followed by logistics automation representing approximately 25% of deployments across large-scale distribution facilities.

Geographically, the report examines market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 30 key countries contributing to robotics development and deployment. The analysis also highlights emerging niche areas such as humanoid robotics, AI-powered industrial inspection robots, autonomous mobile robots, and intelligent service robots capable of performing complex physical tasks. The report further evaluates industry investment patterns, enterprise adoption trends, technological innovations, and strategic initiatives shaping the evolving embodied AI ecosystem across global industrial sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

35.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA, Boston Dynamics, ABB Robotics, SoftBank Robotics, Tesla, Agility Robotics, Sanctuary AI, Unitree Robotics, Hanson Robotics, UBTECH Robotics, KUKA Robotics, FANUC Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |