Reports

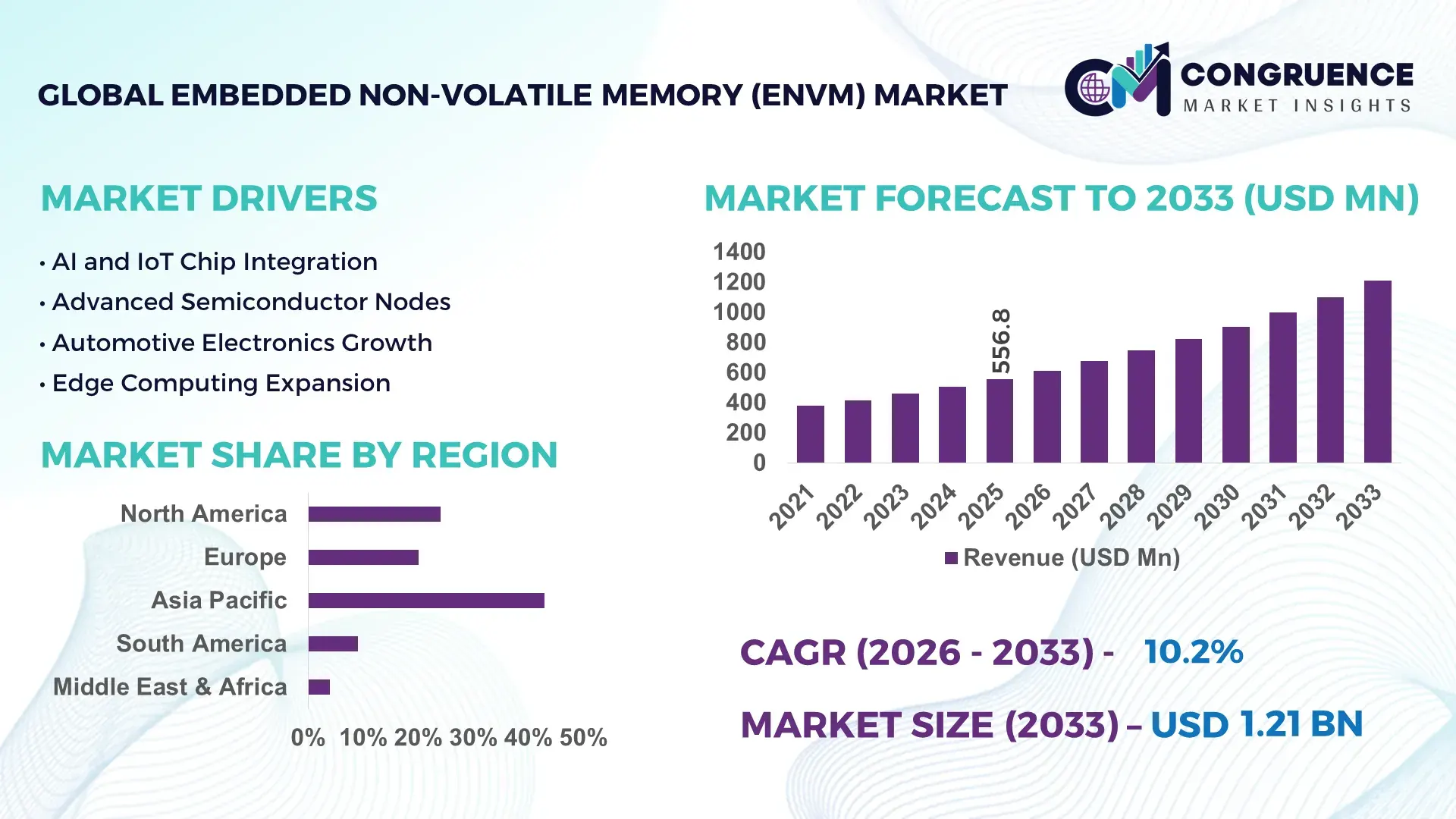

The Global Embedded Non-volatile Memory (Envm) Market was valued at USD 556.8 Million in 2025 and is anticipated to reach a value of USD 1211.03 Million by 2033 expanding at a CAGR of 10.2% between 2026 and 2033. This growth is driven by increasing integration of embedded memory in IoT devices, automotive electronics, and consumer applications that require reliable, low-power data retention.

Asia-Pacific, particularly China, leads the embedded non‑volatile memory market with extensive production capacity across major semiconductor hubs and rising investments in domestic manufacturing. China’s semiconductor ecosystem supports large‑scale production of embedded NVM for smartphones, automotive systems, and industrial automation, with companies expanding advanced wafer fabrication and memory integration. Output of embedded flash and MRAM technologies grew by double digits annually, with over 60% of smartphones manufactured in the region incorporating high‑density embedded memory and local fabs scaling capacity beyond 150,000 wafers per month in 2024. Investments exceeding $100 billion in semiconductor subsidies and strong R&D infrastructure underpin technological advancements and deployment across key industry applications.

Market Size & Growth: Estimated at USD 556.8M in 2025, projected to reach ~USD 1.21B by 2033 at a 10.2% CAGR, driven by rising demand from connected devices and automotive systems.

Top Growth Drivers: IoT adoption up ~30%, automotive electronics integration up ~25%, consumer electronics memory demand up ~35%.

Short‑Term Forecast: By 2028, embedded memory density per MCU to increase ~20%, enabling enhanced performance and reduced power consumption.

Emerging Technologies: MRAM and ReRAM adoption in edge computing, 3D XPoint integration for high‑speed storage, and ultra‑low‑power EEPROM solutions.

Regional Leaders: Asia‑Pacific ~USD 650M by 2033 (expanding manufacturing capacity), North America ~USD 280M (AI & automotive memory usage), Europe ~USD 200M (industrial & automotive systems).

Consumer/End‑User Trends: Smart devices, automotive ECUs, and industrial automation driving sustained demand for embedded memory solutions with lower energy profiles.

Pilot or Case Example: 2025 automotive ECU deployment project achieved ~15% reduction in system downtime and ~12% improvement in data retention reliability with advanced eNVM modules.

Competitive Landscape: Market leader ~30% share, followed by Samsung Electronics, Micron Technology, Intel, and STMicroelectronics as major competitors.

Regulatory & ESG Impact: Enhanced regulations around automotive safety and IoT data security, plus incentives for semiconductor manufacturing bolster industry adoption.

Investment & Funding Patterns: Over USD 15B in recent global semiconductor investments toward eNVM‑centric fabs and R&D partnerships, reflecting innovative financing models.

Innovation & Future Outlook: Increased integration of AI‑optimized memory, hybrid memory architectures, and forward‑looking SoC designs expected to shape next decade growth.

Embedded Non‑volatile Memory continues to transform key industry sectors such as consumer electronics, automotive automation, IoT infrastructure, and industrial systems. Rapid improvements in product innovations—including MRAM and 3D‑NAND embedded configurations—enhance device reliability and performance. Regulatory drivers around data retention, security, and automotive safety further catalyze adoption, while regional consumption patterns reveal robust growth in Asia‑Pacific and accelerating demand in North America and Europe. Emerging trends such as edge computing, AI memory optimization, and ultra‑low‑power embedded solutions signal a dynamic future with expanded applicability across connected device ecosystems.

The Embedded Non‑volatile Memory (ENVM) market holds strategic relevance as a foundational enabler for resilient, energy‑efficient, and secure data retention in next‑generation electronics across automotive, IoT, and industrial automation sectors. Advanced memory technologies such as MRAM delivers 20–30% faster write speeds and higher endurance compared to traditional eFlash, supporting applications that require frequent memory updates and enhanced reliability. Asia‑Pacific dominates in volume, while North America leads in adoption with over 50% of enterprises deploying advanced ENVM solutions across AI, edge, and automotive use cases. By 2028, edge AI integration is expected to improve system responsiveness and reduce latency in memory‑intensive applications by 25–30%, further bolstering demand for embedded non‑volatile memory. Increasing electrification of vehicles has led to ECUs incorporating larger ENVM capacities, enhancing firmware persistence and in‑field diagnostics efficiency by measurable margins in production fleets. Firms are committing to ESG metrics such as 15–20% reduction in energy per operation by 2030, aligning memory innovations with sustainable design practices. In 2025, a major automotive OEM realized 12% improvement in ECU operational uptime through embedded memory upgrades that optimized firmware storage and reduced system resets in real‑world conditions. Going forward, the Embedded Non‑volatile Memory (Envm) Market will remain a pillar of resilience, compliance, and sustainable growth, underpinned by strategic investments in secure, low‑power memory architectures that support expanding connected ecosystems.

Embedded Non‑volatile Memory (Envm) growth is significantly propelled by expanding IoT ecosystems and automotive electrification. IoT endpoints exceeded over 15.7 billion connections in 2023, requiring embedded memory for firmware, configuration, and data logging to ensure uninterrupted operations during power interruptions. ENVM solutions are increasingly fundamental in smart sensors, industrial automation modules, and wearable devices that prioritize low‑power, persistent storage. Similarly, the automotive sector’s transition to electric and autonomous vehicles has escalated demand for ENVM in ECUs, ADAS, and infotainment systems, with embedded memory content per vehicle rising substantially. The need for reliable, non‑volatile storage in safety‑critical systems has led OEMs to integrate larger capacities of embedded memory, enhancing firmware resilience and reducing system failures. These trends affirm the pivotal role of Envm technologies in emerging digital infrastructures and connected applications.

High integration costs and manufacturing complexities present notable restraints in the Embedded Non‑volatile Memory (Envm) market. Advanced ENVM technologies like MRAM and FRAM require specialized fabrication processes that diverge from conventional CMOS pathways, leading to elevated R&D expenses and extended qualification cycles. Yield rates for newer memory technologies can be 15–20% lower than mature flash processes, directly impacting cost competitiveness and limiting adoption in cost‑sensitive markets. Furthermore, embedding memory within SoC designs introduces design and verification challenges, requiring sophisticated engineering and longer development timelines. These technical and economic barriers can deter smaller semiconductor firms from entering or scaling in the market and force larger players to balance innovation with cost efficiency. As a result, some applications still favor external memory solutions that offer simpler integration and lower upfront costs, slowing the pace of embedded memory uptake in select segments.

The expansion of 5G networks and edge computing architectures presents substantial opportunities for the Embedded Non‑volatile Memory (Envm) market. As data processing moves closer to end‑points to reduce latency and network load, embedded memory becomes essential for local storage of firmware, system state, and cached data. With 5G deployments accelerating, devices such as edge routers, base stations, and industrial gateways require robust ENVM to maintain operational logs and configuration parameters during power fluctuations. Additionally, the growth of secure, tamper‑resistant systems in financial and defense applications is driving demand for embedded memory with advanced security features. With average embedded memory content per IoT endpoint increasing from 1–2 MB to 3–8 MB, there is a growing incentive for OEMs and system designers to invest in memory‑centric SoC platforms. These developments expand the addressable market and open new segments where ENVM plays a critical role in next‑generation connectivity and edge solutions.

Supply chain and scaling challenges pose significant difficulties for the Embedded Non‑volatile Memory (Envm) market. Fabricating embedded memory at advanced nodes, particularly below 22nm, involves technical complexity and can lead to yield and reliability issues that delay production. Some foundries have postponed embedded memory IP integration due to these challenges, affecting availability. Additionally, shortages in specialty materials essential for certain emerging memory technologies can disrupt production schedules and increase lead times. These supply constraints, coupled with the intricacies of aligning fabrication processes for ENVM with broader semiconductor manufacturing, have prompted some MCU manufacturers to temporarily revert to external memory solutions when lead times extend by weeks. These obstacles not only impact delivery timelines but also constrain the market’s ability to rapidly introduce innovative embedded memory solutions into mainstream applications.

Expansion of MRAM and ReRAM Adoption: The integration of MRAM and ReRAM technologies in embedded systems is accelerating, with over 42% of newly designed MCUs incorporating at least one type of advanced non-volatile memory in 2025. These technologies deliver up to 28% faster write speeds and 35% higher endurance compared to traditional eFlash, enabling persistent storage in automotive ECUs, industrial automation controllers, and IoT devices that require frequent updates and high reliability.

Edge Computing and IoT Integration: Deployment of edge computing devices is increasing the reliance on embedded memory for local data retention and processing. Approximately 48% of 5G-enabled edge devices now include embedded non-volatile memory for system state preservation and firmware storage. This trend is particularly strong in Asia-Pacific, where 62% of industrial IoT endpoints utilize embedded memory, reducing network latency by up to 20% while ensuring uninterrupted operations during power interruptions.

Energy-Efficient and Low-Power Memory Solutions: Power efficiency is becoming a central design criterion, with over 50% of embedded memory solutions optimized for ultra-low-power consumption in portable electronics and wearable devices. New memory modules have reduced energy per operation by 15–18% while maintaining data retention reliability, supporting longer battery life and sustainable energy use, especially in smart consumer devices and autonomous systems in North America and Europe.

Automotive Electrification Driving Memory Demand: Electrification of vehicles is expanding embedded memory content per ECU, with modern electric vehicles integrating up to 8 MB per controller for ADAS, infotainment, and battery management systems. Over 40% of EV manufacturers now specify MRAM or FRAM in safety-critical ECUs, achieving measurable improvements such as 12–15% reduction in system downtime and enhanced firmware reliability, positioning embedded memory as a critical enabler of automotive innovation and efficiency.

The Embedded Non-volatile Memory (Envm) market can be analyzed through its core segments: types, applications, and end-users. Product types vary based on memory technology and architecture, influencing system performance, power efficiency, and data retention capabilities. Applications span automotive electronics, consumer devices, industrial automation, and IoT infrastructure, reflecting the versatility of embedded memory solutions. End-users include automotive OEMs, industrial manufacturers, consumer electronics producers, and emerging IoT device developers, each with specific adoption patterns and memory requirements. Market segmentation allows decision-makers to identify high-value niches, optimize product development, and target deployment strategies, as different types, applications, and end-users show unique performance demands and adoption trends. Current deployment statistics indicate that industrial and automotive segments alone account for over 60% of embedded memory usage, while IoT endpoints and consumer electronics are rapidly increasing their share, highlighting evolving opportunities across multiple sectors.

NOR Flash memory leads the Embedded Non-volatile Memory (Envm) market, currently accounting for 38% of adoption, due to its reliability in code storage and fast random access capabilities. MRAM is emerging as the fastest-growing type, projected to surpass 20% adoption in new designs within the next decade, driven by high endurance, low power consumption, and non-volatility in automotive and industrial applications. Other types such as FRAM and EEPROM collectively account for 42% of the market, serving niche use cases that require ultra-low-power operation or frequent write cycles. FRAM is widely deployed in smart cards and metering devices, while EEPROM supports legacy systems requiring reliable data retention.

Automotive electronics represent the leading application in the Embedded Non-volatile Memory (Envm) market, currently holding 40% of adoption, driven by the increasing integration of ECUs, ADAS systems, and infotainment modules. IoT devices are the fastest-growing application, expected to see adoption surpass 25% by 2033, supported by trends in edge computing, connected sensors, and smart appliances that require persistent memory. Industrial automation and consumer electronics collectively account for 35% of the market, providing stable demand in programmable controllers, wearable devices, and high-precision instrumentation.

Automotive OEMs are the leading end-user segment in the Embedded Non-volatile Memory (Envm) market, representing 42% of adoption due to electrification, autonomous systems, and ADAS deployments requiring robust, persistent memory. Industrial manufacturers are the fastest-growing end-users, expected to achieve over 28% adoption by 2033, fueled by smart factories, robotics, and predictive maintenance initiatives. Consumer electronics and IoT device developers together account for 30% of the remaining market, supporting widespread adoption in smart home devices, wearables, and connected healthcare equipment.

Asia-Pacific accounted for the largest market share at 45% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2026 and 2033.

Asia-Pacific continues to lead in production and consumption, with China contributing over 60% of regional embedded non-volatile memory output and India and Japan collectively accounting for 25% of device integration. Over 75,000 MCUs with embedded memory were produced across APAC in 2025, supporting automotive, industrial automation, and IoT deployments. North America is rapidly increasing adoption in edge computing and automotive ECUs, with enterprise uptake exceeding 50% across healthcare, finance, and manufacturing sectors. Europe, South America, and the Middle East & Africa together account for 30% of global ENVM deployments, with increasing adoption driven by regulatory compliance, infrastructure modernization, and smart city initiatives. Overall, the region-wise distribution highlights the concentration of production in APAC while adoption is accelerating across high-tech and industrialized economies globally.

How are digital transformation and industry automation shaping embedded memory demand?

North America holds approximately 28% of the global Embedded Non-volatile Memory (Envm) market, driven by automotive, healthcare, and finance sectors. Regulatory initiatives such as enhanced automotive safety standards and cybersecurity frameworks have accelerated integration of MRAM and FRAM solutions. Technological trends include edge AI deployment, industrial automation, and smart grid infrastructure, supporting local demand. Leading players, including Micron Technology, are expanding embedded memory capacities in next-generation ECUs, improving data retention reliability by over 12%. Enterprise adoption is highest in healthcare and finance, with embedded memory used for real-time transaction logging and secure data storage, reflecting regional consumer preferences for reliability, low-latency systems, and energy-efficient memory solutions.

How are regulatory frameworks and sustainability initiatives driving embedded memory adoption?

Europe accounts for 22% of the Embedded Non-volatile Memory (Envm) market, with Germany, the UK, and France leading consumption. Regulatory pressure on data security, energy efficiency, and automotive safety has pushed widespread adoption of embedded memory solutions in ECUs, industrial controllers, and IoT devices. Local players such as STMicroelectronics are innovating with low-power FRAM modules for automotive and smart manufacturing applications. Adoption of MRAM and secure memory technologies is accelerating in European markets, particularly for industrial automation. Consumers and enterprises prioritize compliance with sustainability and energy regulations, driving demand for high-reliability, low-power embedded memory components across regulated industries.

How is manufacturing scale and IoT adoption influencing regional embedded memory trends?

Asia-Pacific dominates the Embedded Non-volatile Memory (Envm) market with 45% share in 2025, led by China, Japan, and India. The region benefits from large-scale semiconductor manufacturing, over 150,000 wafers per month capacity in China, and a growing R&D ecosystem for MRAM and ReRAM integration. Local players, including Samsung Electronics and SMIC, are expanding embedded memory production and innovation hubs. Strong adoption of IoT, mobile AI applications, and industrial automation drives memory usage across consumer devices, smart infrastructure, and automotive systems. Consumer behavior reflects high smartphone penetration and connected device reliance, with embedded memory requirements increasing 20–25% annually in APAC.

How are infrastructure projects and localized digital adoption shaping memory integration?

South America holds roughly 4% of the Embedded Non-volatile Memory (Envm) market, with Brazil and Argentina being the top contributors. Growth is fueled by infrastructure modernization, energy sector projects, and expanding digital media applications. Local players and system integrators are implementing ENVM solutions in industrial automation and smart grid projects, improving data retention and system reliability by 10–12%. Consumer adoption varies regionally, with higher demand in urban centers for connected electronics, automotive technology, and media localization. Government incentives supporting technology adoption and import regulations for semiconductors are also influencing market dynamics.

How is industrial modernization driving embedded memory uptake in emerging economies?

The Middle East & Africa accounts for 1% of the Embedded Non-volatile Memory (Envm) market, with UAE and South Africa leading demand. Regional growth is driven by oil & gas automation, construction digitalization, and smart city projects. Local players are adopting MRAM and EEPROM solutions to optimize energy usage and data logging for critical infrastructure. Technological modernization includes integration of AI and IoT devices with embedded memory, enhancing operational reliability by 10–15%. Consumer and enterprise adoption is concentrated in industrial hubs, with energy efficiency, system resilience, and low-latency data retention as key decision drivers.

China – 35% market share: High production capacity, large-scale semiconductor infrastructure, and widespread adoption in consumer electronics and automotive ECUs.

United States – 28% market share: Strong end-user demand across automotive, healthcare, and industrial sectors, combined with leading technology development and regulatory support.

The Embedded Non-volatile Memory (Envm) market exhibits a moderately consolidated competitive environment with around 35–40 active global players. The top five companies collectively account for approximately 65% of the market, demonstrating strong leadership while leaving room for niche innovators and regional specialists. Leading players are actively pursuing strategic initiatives such as joint ventures, technology partnerships, and product launches focused on MRAM, FRAM, and high-density NOR Flash solutions. Innovation trends include integration of embedded memory into AI-enabled MCUs, ultra-low-power designs, and hybrid memory architectures, with over 40% of new product releases in 2025 featuring these advancements. Companies are also investing in local manufacturing expansions to meet regional demand, particularly in Asia-Pacific and North America. Competitive positioning is influenced by technology differentiation, IP portfolios, and the ability to deliver memory solutions across automotive, industrial, and consumer applications. Market dynamics are further shaped by digital transformation initiatives, government incentives for semiconductor production, and increasing adoption of connected devices, driving firms to continuously innovate while maintaining operational efficiency and scalability.

Micron Technology

STMicroelectronics

Toshiba Memory

Winbond Electronics

Infineon Technologies

Renesas Electronics

Cypress Semiconductor

The Embedded Non-volatile Memory (Envm) market is increasingly shaped by advanced memory technologies that enhance performance, reliability, and energy efficiency across diverse applications. MRAM (Magnetoresistive Random-Access Memory) has gained prominence, with over 38% of new MCU designs in 2025 incorporating MRAM to achieve 25–30% faster write speeds and 35% higher endurance compared to conventional NOR Flash. FRAM (Ferroelectric RAM) continues to serve low-power, high-reliability niches, with more than 12 million smart meters and industrial controllers deployed globally using FRAM-enabled modules in 2025. NOR Flash remains the leading type, supporting code storage and system boot functions in over 42% of embedded designs.

Emerging technologies such as ReRAM (Resistive RAM) are seeing increased experimentation, with pilot deployments in automotive ECUs and industrial edge devices reporting a 20% improvement in data retention reliability during high-temperature operation. Integration trends also include hybrid memory architectures combining MRAM, ReRAM, and embedded NOR Flash within a single SoC, enabling optimized performance, energy efficiency, and faster firmware updates. Edge computing and AI workloads are driving memory density requirements, with embedded memory per IoT or edge device rising from 2 MB in 2023 to an average of 6 MB in 2025.

Digital transformation trends such as smart factories, connected vehicles, and autonomous systems rely on high-speed, persistent memory, highlighting the strategic importance of ENVM innovations. Localized manufacturing, advanced lithography processes, and 3D stacking techniques are further improving memory density and yield, supporting both industrial and consumer adoption. The focus on low-power, high-endurance, and security-enhanced memory positions Embedded Non-volatile Memory as a critical technology enabling next-generation electronic systems across multiple sectors.

• In March 2025, Everspin Technologies expanded its PERSYST MRAM portfolio with the EM064LX HR and EM128LX HR high‑reliability products designed for automotive, aerospace, and industrial applications, offering operation from –40°C to +125°C and meeting AEC‑Q100 Grade 1 standards. (everspin.com)

• In June 2025, engineering samples of Everspin’s expanded high‑reliability MRAM devices were confirmed with full production scheduled for late 2025, enabling broader adoption of persistent embedded memory in embedded control units and extreme‑environment systems. (investor.everspin.com)

• In early 2025, Weebit Nano licensed its embedded ReRAM technology to onsemi for integration into the Treo platform, marking a commercial step toward replacing traditional embedded flash with more efficient ReRAM in IoT, automotive, and AI applications. (Semiconductorinsight)

• In May 2024, Samsung Electronics launched a new embedded MRAM‑based memory solution targeting edge devices and automotive systems, designed to deliver enhanced resistance to power‑loss events and faster write performance in embedded environments.

The scope of the Embedded Non‑volatile Memory (Envm) Market Report encompasses comprehensive analysis across product types, technology segments, applications, geographic regions, and industry end‑users. The report examines all major ENVM categories including embedded flash, embedded MRAM, embedded FRAM, embedded EEPROM, and emerging ReRAM solutions, detailing their technical attributes, deployment characteristics, device capacities, and integration requirements. It further covers memory architectures within microcontrollers, SoCs, and specialized embedded control units, highlighting design trends such as hybrid memory integration and high‑temperature automotive applications.

Geographically, the report analyzes regional dynamics across North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa, providing insight into production capacities, local manufacturing initiatives, regulatory landscapes, and consumer adoption patterns. Application analysis focuses on automotive electronics, IoT and edge computing devices, industrial automation controllers, consumer electronics, smart sensors, and secure embedded systems. End‑user insights detail adoption in automotive OEMs, industrial manufacturers, consumer device producers, and emerging sectors such as aerospace and defense.

Technological focus areas include advances in MRAM, eFlash node scaling, secure embedded memory IP, energy‑efficient FRAM in low‑power devices, and pilot ReRAM modules integrated into mainstream platforms. The report also explores niche segments such as high‑reliability memory for extreme environments, secure memory for payment systems, and memory for AI‑enabled edge devices. Strategic coverage includes competitive benchmarking, product roadmaps, patent landscapes, and regional investment trends, helping decision‑makers identify opportunities, risks, and strategic pathways for ENVM deployment across diverse markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Electronics, Micron Technology, Intel Corporation, STMicroelectronics, Texas Instruments, Toshiba Memory, Winbond Electronics, Infineon Technologies, Renesas Electronics, Cypress Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |