Reports

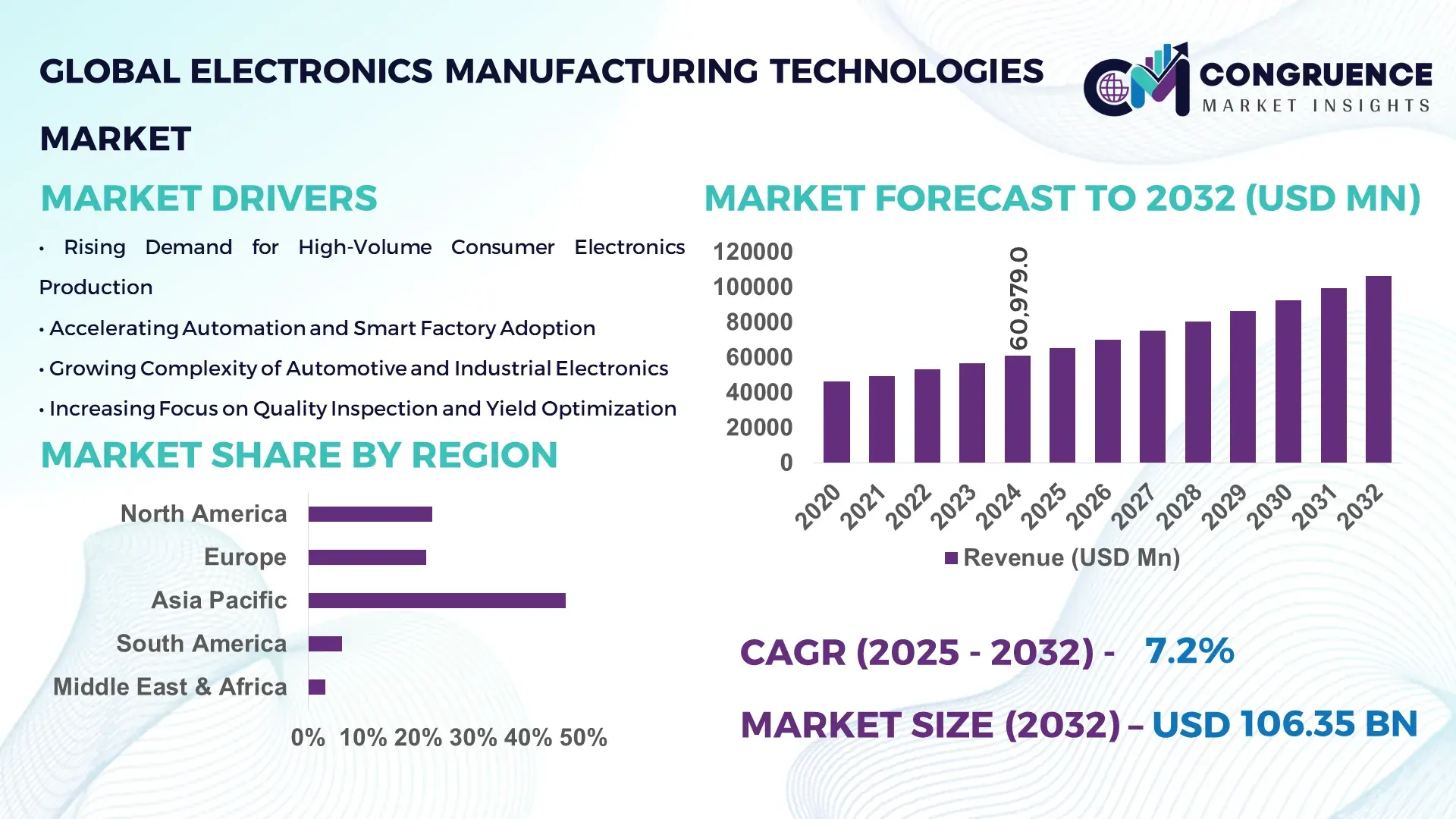

The Global Electronics Manufacturing Technologies Market was valued at USD 60,979.0 Million in 2024 and is anticipated to reach a value of USD 106,350.3 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising automation intensity, increasing semiconductor complexity, and the rapid scaling of smart, high-volume electronics production worldwide.

China remains the dominant country in the Electronics Manufacturing Technologies Market, supported by unmatched production scale, capital investment, and rapid technology deployment. The country hosts over 40% of the world’s electronics manufacturing facilities, with annual electronics output exceeding USD 2.1 trillion. Government-backed investment in advanced manufacturing surpassed USD 120 billion between 2020 and 2024, accelerating adoption of surface-mount technology (SMT), advanced PCB fabrication, and AI-enabled inspection systems. China accounts for more than 55% of global consumer electronics assembly capacity and produces over 70% of smartphones and networking equipment globally. Additionally, over 65% of large electronics plants in China deploy industrial robotics and automated optical inspection systems, reflecting strong integration of precision manufacturing technologies across automotive electronics, telecommunications, and industrial control applications.

Market Size & Growth: Valued at USD 60,979.0 Million in 2024, projected to reach USD 106,350.3 Million by 2032 at a CAGR of 7.2%, driven by rising automation and semiconductor miniaturization.

Top Growth Drivers: Automation adoption (+48%), defect reduction through AI inspection (+32%), manufacturing cycle-time improvement (+27%).

Short-Term Forecast: By 2028, smart manufacturing systems are expected to cut production downtime by 22%.

Emerging Technologies: AI-driven optical inspection, advanced SMT placement systems, digital twins for factory optimization.

Regional Leaders: Asia Pacific USD 48,900 Million (2032) with high-volume manufacturing adoption; North America USD 28,400 Million driven by high-mix electronics; Europe USD 21,600 Million focused on Industry 4.0 integration.

Consumer/End-User Trends: Automotive electronics and industrial automation account for over 46% of technology deployment.

Pilot or Case Example: In 2023, a South Korean electronics plant achieved 35% defect reduction using AI-based inspection.

Competitive Landscape: ASMPT (~14%) leads, followed by Panasonic, Fuji Corporation, Mycronic, and Koh Young.

Regulatory & ESG Impact: Energy-efficient manufacturing mandates are reducing factory emissions by up to 18%.

Investment & Funding Patterns: Over USD 18 billion invested globally in electronics manufacturing automation since 2022.

Innovation & Future Outlook: Integration of AI, robotics, and real-time analytics is reshaping next-generation electronics factories.

Electronics manufacturing technologies support key sectors including consumer electronics (34%), automotive electronics (21%), industrial automation (18%), telecommunications (15%), and medical electronics (12%). Recent innovations in AI-based defect detection and ultra-fine pitch SMT placement have improved yield rates by over 25%. Regulatory pressure on energy efficiency, coupled with Asia Pacific’s strong consumption growth and North America’s high-value production focus, continues to shape future market expansion.

The Electronics Manufacturing Technologies Market plays a critical strategic role in enabling global digital infrastructure, smart mobility, and industrial automation. Advanced manufacturing technologies are now central to competitiveness as electronics become smaller, faster, and more complex. For example, AI-powered automated optical inspection delivers up to 30% improvement in defect detection accuracy compared to traditional rule-based inspection systems. Asia Pacific dominates in production volume, while North America leads in advanced adoption, with over 62% of large manufacturers deploying AI-enabled manufacturing platforms.

In the short term, manufacturers are prioritizing flexible, data-driven factories. By 2027, predictive maintenance powered by machine learning is expected to reduce unplanned equipment downtime by 28%. ESG commitments are also shaping strategy, with firms targeting a 20% reduction in energy consumption per unit produced by 2030 through energy-efficient equipment and smart factory controls.

A micro-scenario illustrates this shift: in 2024, Japan-based electronics manufacturers achieved a 26% improvement in line efficiency after implementing digital twin simulations for SMT production lines. Looking ahead, the Electronics Manufacturing Technologies Market will serve as a foundation for resilient supply chains, regulatory compliance, and sustainable industrial growth as global demand for high-reliability electronics accelerates.

The Electronics Manufacturing Technologies Market is shaped by rapid innovation, evolving product complexity, and shifting global supply chains. Increasing demand for high-density electronics, electric vehicles, and connected devices is accelerating the adoption of advanced manufacturing solutions. Automation, precision assembly, and intelligent inspection systems are becoming essential to maintain quality and throughput. At the same time, manufacturers are balancing cost pressures, regulatory compliance, and sustainability targets. Regional dynamics also play a role, with Asia Pacific emphasizing scale efficiency, while North America and Europe focus on high-mix, high-reliability production environments.

The increasing complexity of electronics is a major driver for manufacturing technology adoption. Modern PCBs now integrate over 30% more components per square centimeter compared to five years ago, requiring ultra-precise placement and inspection systems. Automotive electronics content per vehicle has grown by over 40%, driving demand for reliable, high-accuracy manufacturing solutions. AI-enabled inspection systems are improving first-pass yield by up to 25%, while high-speed SMT machines are increasing placement accuracy below 20 microns. These performance requirements are pushing manufacturers to upgrade production lines with advanced electronics manufacturing technologies.

Advanced electronics manufacturing equipment requires substantial upfront investment, limiting adoption among small and mid-sized manufacturers. A fully automated SMT production line can cost over USD 8 million, excluding software integration and workforce training. Additionally, implementation timelines often exceed 12–18 months, delaying return on investment. Skilled labor shortages further compound this issue, with over 35% of manufacturers reporting difficulties in hiring automation and AI specialists. These factors slow technology penetration despite long-term operational benefits.

Smart factory integration offers significant growth opportunities as manufacturers seek data-driven efficiency. Connected production systems enable real-time monitoring, reducing scrap rates by up to 20%. Integration of digital twins allows manufacturers to simulate production changes before deployment, cutting process optimization time by 30%. Emerging markets are increasingly adopting these technologies to leapfrog traditional manufacturing models, creating strong demand for scalable and modular electronics manufacturing solutions.

Global supply chain volatility remains a key challenge, impacting equipment availability and deployment schedules. Lead times for advanced electronics manufacturing equipment increased by nearly 40% during recent disruptions. Dependence on specialized components and software platforms heightens vulnerability to geopolitical and trade-related risks. Additionally, compliance with varying regional standards increases system customization costs, complicating cross-border deployment of electronics manufacturing technologies.

Expansion of AI-Driven Inspection Systems: Adoption of AI-based inspection technologies has increased by over 45% across large electronics factories. These systems reduce false defect rates by nearly 30% and improve overall yield by 22%, enabling consistent quality in high-density electronics production.

Rapid Growth of Advanced SMT Platforms: Next-generation SMT machines now achieve placement speeds exceeding 120,000 components per hour with accuracy improvements of 18%. Over 60% of new production lines installed in 2024 incorporated advanced SMT platforms to support miniaturized electronics.

Increased Focus on Energy-Efficient Manufacturing: Energy-efficient electronics manufacturing equipment is reducing power consumption per unit by 15–20%. Approximately 52% of manufacturers have upgraded equipment to meet stricter energy efficiency targets and lower operational emissions.

Adoption of Modular and Prefabricated Manufacturing Lines: Modular production line adoption has grown by 38%, enabling faster capacity expansion and 25% shorter setup times. Prefabricated machine modules allow manufacturers to scale output rapidly while reducing labor dependency and improving consistency.

The Electronics Manufacturing Technologies Market is segmented based on type, application, and end-user, reflecting the diverse technology requirements across the electronics value chain. By type, the market spans assembly and placement systems, inspection and testing technologies, fabrication equipment, and supporting automation solutions, each addressing specific precision, speed, and quality demands. Application-wise, electronics manufacturing technologies are deployed across consumer electronics, automotive electronics, industrial equipment, telecommunications, and medical devices, with adoption patterns closely tied to product complexity and regulatory requirements. From an end-user perspective, large-scale contract manufacturers, original equipment manufacturers (OEMs), and specialized component producers represent distinct demand clusters, differentiated by production volume, customization needs, and technology maturity. Increasing product miniaturization, rising defect sensitivity, and growing automation penetration are reshaping segmentation dynamics, with advanced and intelligent manufacturing solutions gaining preference across all segments.

Electronics manufacturing technologies include surface-mount technology (SMT) equipment, inspection and testing systems, fabrication and processing machinery, and auxiliary automation solutions such as material handling and software platforms. SMT equipment represents the leading type, accounting for approximately 38% of total adoption, due to its critical role in high-speed, high-precision component placement for compact electronic devices. Inspection and testing systems hold around 27% adoption, driven by quality assurance requirements as defect tolerance declines. However, adoption of AI-enabled inspection technologies is rising fastest, expanding at an estimated 9.1% CAGR, as manufacturers prioritize yield improvement and predictive quality control. Fabrication and processing equipment, including PCB drilling and etching systems, contribute a combined share of nearly 22%, serving specialized and upstream manufacturing stages. Remaining segments such as material handling automation and manufacturing execution software collectively account for about 13%, supporting efficiency and traceability across production lines.

By application, consumer electronics manufacturing dominates, accounting for nearly 34% of technology adoption, supported by high production volumes, rapid product refresh cycles, and increasing device miniaturization. Automotive electronics manufacturing follows with approximately 26% adoption, reflecting growing electronic content per vehicle and stringent reliability standards. Industrial electronics applications hold around 18%, driven by automation, control systems, and power electronics demand. Telecommunications and medical electronics together contribute a combined share of roughly 22%. While consumer electronics leads in absolute adoption, automotive electronics is the fastest-growing application, expanding at an estimated 8.7% CAGR, fueled by electric vehicle production, advanced driver-assistance systems, and in-vehicle connectivity. In 2024, over 41% of global electronics manufacturers reported expanding technology deployment specifically for automotive-grade production lines. Additionally, more than 36% of enterprises piloted advanced manufacturing systems to support high-reliability electronics applications.

From an end-user perspective, large contract electronics manufacturers represent the leading segment, accounting for approximately 44% of total technology adoption. Their dominance is supported by large-scale production requirements, multi-client manufacturing, and strong emphasis on automation to manage cost and quality across high volumes. Original equipment manufacturers (OEMs) follow with about 31% adoption, focusing on proprietary product lines and differentiated manufacturing capabilities. Specialized component and subsystem manufacturers account for the remaining 25%, serving niche, high-precision markets. Among end-users, OEMs represent the fastest-growing segment, expanding at an estimated 8.9% CAGR, driven by reshoring initiatives, customization needs, and tighter integration between product design and manufacturing. In 2024, nearly 39% of OEMs globally reported increased investment in smart manufacturing technologies. Additionally, surveys indicate that over 58% of industrial buyers prefer suppliers with advanced, automated production capabilities due to consistency and traceability benefits.

Asia-Pacific accounted for the largest market share at 46.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

Asia-Pacific’s leadership is supported by over 65% of global electronics production volume, more than 70 million units/day of PCB assembly capacity, and the presence of over 55% of global electronics manufacturing facilities. North America’s accelerated growth is driven by reshoring initiatives, with over USD 52 billion allocated to electronics and semiconductor manufacturing incentives, alongside strong adoption of AI-driven manufacturing platforms. Europe holds approximately 21.4% market share, supported by regulatory-driven digital manufacturing adoption, while South America and the Middle East & Africa together account for nearly 9.3%, reflecting emerging industrialization and infrastructure-led electronics demand. Regional disparities are shaped by automation intensity, policy frameworks, labor economics, and end-use industry maturity.

North America accounts for approximately 22.6% of the global Electronics Manufacturing Technologies Market, with demand concentrated in the United States and Canada. Key industries driving adoption include automotive electronics, aerospace & defense, medical devices, and data center infrastructure. Over 48% of electronics plants in the region have integrated AI-enabled inspection or predictive maintenance systems. Government-backed programs supporting domestic manufacturing have accelerated capital equipment upgrades, while stricter quality and traceability regulations are increasing demand for advanced testing and digital manufacturing execution systems. Local players such as advanced automation solution providers are deploying smart SMT and inspection platforms to reduce defect rates by over 25%. Regionally, consumer behavior shows higher enterprise adoption in healthcare and financial electronics, where reliability and compliance are critical.

Europe represents roughly 21.4% of global market share, led by Germany, the United Kingdom, and France. Germany alone contributes over 32% of regional electronics manufacturing output, particularly in industrial automation and automotive electronics. Regulatory initiatives focused on energy efficiency and carbon reduction are pushing manufacturers toward low-power, high-efficiency production equipment. More than 57% of large European electronics manufacturers have implemented Industry 4.0 frameworks, including digital twins and smart factory analytics. Regional players are investing in precision manufacturing and advanced inspection to comply with strict product safety norms. Consumer behavior reflects strong regulatory influence, with buyers and enterprises demanding transparent, compliant, and energy-efficient electronics production systems.

Asia-Pacific leads the market with approximately 46.8% share, making it the largest regional contributor by both volume and installed manufacturing capacity. China, Japan, South Korea, and India are the top consuming and producing countries. China alone accounts for over 40% of global electronics assembly volume, while Japan and South Korea lead in precision manufacturing and advanced robotics integration. India has recorded a 2.3× increase in electronics manufacturing capacity since 2019, supported by industrial corridors and incentive programs. The region hosts multiple innovation hubs focused on SMT, semiconductor back-end manufacturing, and AI-driven quality control. Consumer behavior is heavily influenced by e-commerce expansion and mobile device proliferation, driving high-volume, cost-efficient manufacturing adoption.

South America holds close to 6.1% of global market share, with Brazil and Argentina serving as key manufacturing and consumption hubs. Brazil accounts for nearly 58% of regional electronics production, supported by local assembly requirements and import substitution policies. Infrastructure upgrades and growing demand for consumer electronics, industrial equipment, and energy-related electronics are driving technology adoption. Government incentives for local manufacturing and favorable trade agreements are encouraging investment in assembly and testing equipment. Regional players focus on flexible, mid-scale manufacturing solutions. Consumer behavior shows demand closely tied to media consumption, language localization, and affordability-driven electronics production.

The Middle East & Africa region contributes approximately 3.2% of the global market, with the UAE, Saudi Arabia, and South Africa leading adoption. Demand is primarily driven by oil & gas electronics, construction automation, telecommunications infrastructure, and defense applications. Over 41% of new electronics facilities in the Gulf Cooperation Council countries incorporate smart manufacturing systems. National diversification strategies are accelerating technology transfer and industrial automation investments. Local players and industrial zones are focusing on assembly, testing, and regional distribution capabilities. Consumer behavior varies widely, with enterprise-led adoption dominating over consumer-driven electronics manufacturing.

China – 38.9% Market Share: Dominance driven by massive production capacity, integrated supply chains, and high-volume electronics assembly infrastructure.

United States – 16.4% Market Share: Leadership supported by high-value electronics manufacturing, strong OEM demand, and rapid adoption of AI-enabled manufacturing technologies.

The Electronics Manufacturing Technologies Market is characterized by moderate fragmentation, with a mix of global equipment leaders and specialized niche technology providers competing across assembly, inspection, testing, and automation segments. The market hosts over 120 active global and regional competitors, ranging from large-scale platform vendors to precision equipment specialists. The top five companies collectively account for approximately 48–52% of total market presence, reflecting strong brand positioning but leaving room for innovation-led entrants.

Competition is driven by technology differentiation, production accuracy, automation depth, and software integration capabilities. Strategic initiatives are increasingly centered on AI-enabled inspection systems, high-speed SMT platforms, and smart factory software ecosystems. Between 2023 and 2024, more than 35% of leading players announced new product launches focused on miniaturization and yield optimization, while over 20% engaged in strategic partnerships to integrate robotics, machine vision, and analytics. Mergers and acquisitions remain selective, targeting software, AI, and niche precision capabilities rather than large-scale consolidation. Innovation intensity is high, with leading firms allocating significant engineering resources toward ultra-fine pitch placement, predictive maintenance, and closed-loop quality control, shaping a competition landscape defined by performance, reliability, and digital readiness.

JUKI Corporation

Yamaha Motor Robotics

Nordson Corporation

Universal Instruments

Foxconn

Fuji Corporation

Jabil Inc.

Mycronic AB

Koh Young Technology

Hon Hai Technology Group

Technology evolution in the Electronics Manufacturing Technologies Market is centered on precision, intelligence, and scalability. Advanced surface-mount technology (SMT) systems now achieve placement accuracies below 15 microns, supporting ultra-compact device designs. AI-powered automated optical inspection (AOI) and 3D solder paste inspection systems are reducing false call rates by 25–35%, significantly improving first-pass yield.

Smart factory integration is accelerating, with over 60% of large manufacturers deploying manufacturing execution systems (MES) connected to real-time machine data. Digital twin technology is increasingly used to simulate line balancing and process changes, cutting optimization cycles by nearly 30%. Robotics adoption continues to rise, with collaborative robots handling material transfer and repetitive tasks, improving labor productivity by 20–28%.

Emerging technologies include edge AI for in-line defect detection, closed-loop process control, and energy-efficient equipment designs that lower per-unit power consumption by up to 18%. Software-driven interoperability between machines from different vendors is also gaining traction, enabling modular line configurations and faster scalability. Collectively, these technologies are redefining electronics manufacturing toward higher reliability, lower waste, and greater operational agility.

In November 2025, Hon Hai Technology Group (Foxconn) announced a strategic commercial collaboration with OpenAI to co-develop and produce AI-hardware infrastructure components, including data center racks and custom modules, at U.S. facilities — positioning its electronics manufacturing footprint toward supporting next-generation artificial intelligence compute demand. Source: www.reuters.com

In October 2025, Foxconn revealed plans to integrate humanoid robots powered by Nvidia’s Isaac GR00T platform at its new AI server production facility in Houston, Texas, a move expected to significantly elevate automation and productivity in smart manufacturing lines. Source: www.timesofindia.indiatimes.com

In November 2025, Hon Hai Technology Group and Intrinsic launched a joint venture focused on “AI-factory of the future” solutions, advancing intelligent robotics deployment across electronics assembly, inspection, machine tending, and logistics operations worldwide. Source: www.intrinsic.ai

In December 2025, Jabil Inc. reported exceptional stock performance and financial results, with shares up ~4.9% after strong earnings and an 18.7% year-over-year revenue increase, reflecting robust demand for its electronics manufacturing and intelligent infrastructure solutions across cloud, networking, and AI sectors. Source: www.barrons.com

The Electronics Manufacturing Technologies Market Report provides a comprehensive evaluation of technologies enabling modern electronics production across global industries. The scope covers equipment types such as SMT placement systems, inspection and testing technologies, fabrication machinery, robotics, and manufacturing software platforms. It examines applications spanning consumer electronics, automotive systems, industrial automation, telecommunications, medical devices, and aerospace electronics, reflecting varied precision and compliance requirements.

Geographically, the report analyzes Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, capturing regional manufacturing capacities, technology adoption intensity, and industrial focus areas. The scope includes production-scale variations, from high-volume contract manufacturing to high-mix, low-volume specialty electronics. Emerging segments such as AI-driven inspection, digital twins, energy-efficient manufacturing equipment, and modular production lines are incorporated to reflect evolving industry priorities.

The report also evaluates end-user categories, including OEMs, contract manufacturers, and component suppliers, highlighting adoption patterns and operational requirements. By integrating technology trends, application diversity, and regional dynamics, the scope delivers a structured, decision-oriented view of the Electronics Manufacturing Technologies Market, supporting strategic planning, investment assessment, and competitive positioning without duplicating granular analyses from other sections.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 60,979.0 Million |

| Market Revenue (2032) | USD 106,350.3 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ASMPT, Panasonic Corporation, Siemens AG, JUKI Corporation, Yamaha Motor Robotics, Nordson Corporation, Universal Instruments, Foxconn, Fuji Corporation, Jabil Inc., Mycronic AB, Koh Young Technology, Hon Hai Technology Group |

| Customization & Pricing | Available on Request (10% Customization Free) |