Reports

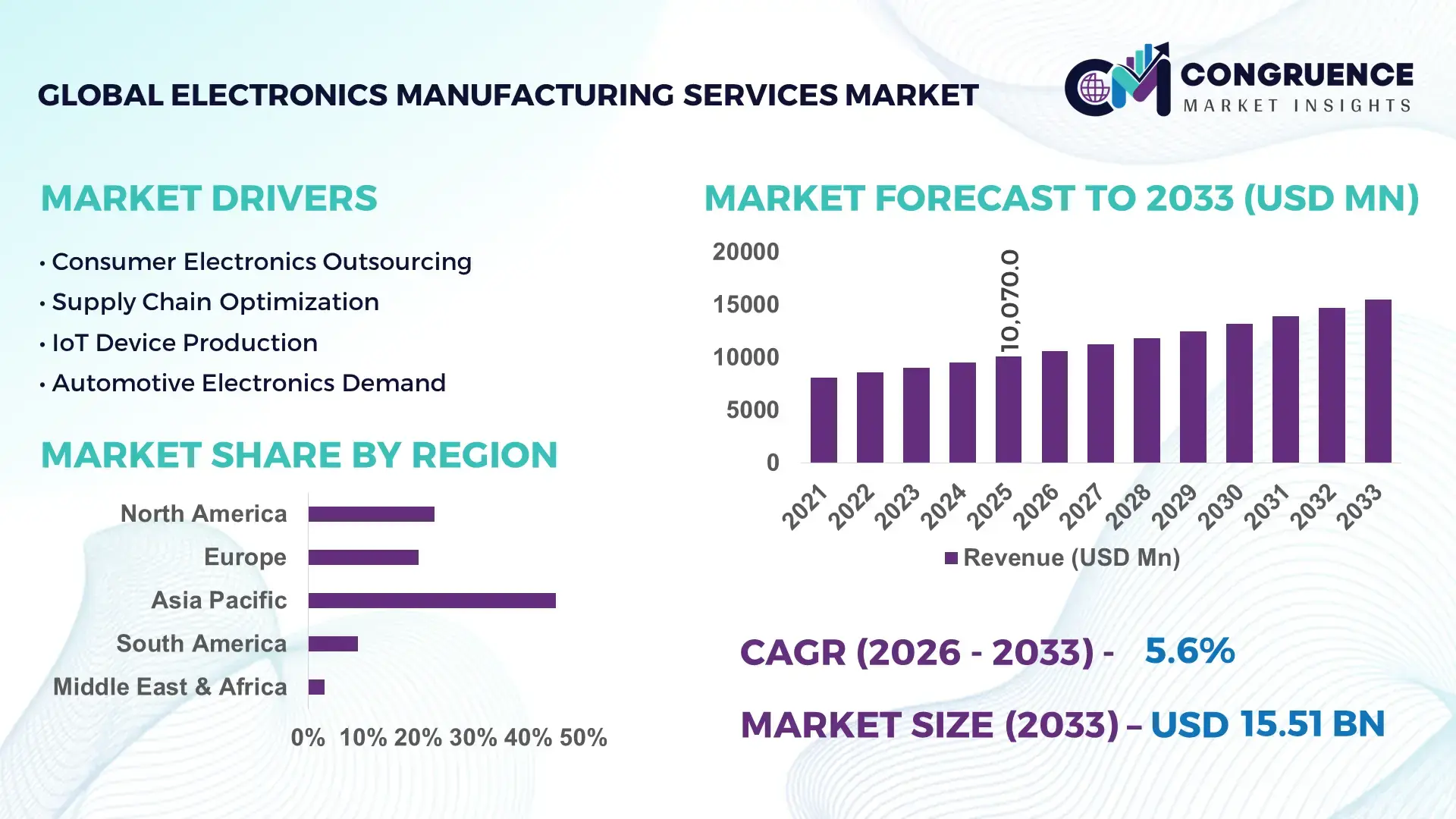

The Global Electronics Manufacturing Services Market was valued at USD 10070 Million in 2025 and is anticipated to reach a value of USD 15512.98 Million by 2033 expanding at a CAGR of 5.55% between 2026 and 2033.

The market is being actively shaped by accelerated outsourcing from OEMs seeking 18–25% cost optimization and faster product cycles through integrated design-to-delivery EMS capabilities. A critical global context between 2024 and 2026 is the ongoing supply chain realignment driven by geopolitical trade shifts and tariff recalibrations, pushing companies toward diversified manufacturing footprints across Asia and North America.

China remains the dominant hub, accounting for nearly 35% of global EMS production capacity, supported by over USD 120 billion in electronics exports and strong integration in consumer electronics and telecom equipment manufacturing. Meanwhile, countries like Vietnam and India are scaling rapidly, with India capturing approximately 7–9% of EMS capacity through government-backed production-linked incentives and expanding semiconductor ecosystems. Compared to legacy single-region dependency, multi-location sourcing has improved supply chain resilience by over 20%, reducing lead-time volatility across key verticals.

For strategic decision-makers, the shift toward geographically diversified, high-efficiency EMS partnerships is no longer optional but a critical lever for cost control, risk mitigation, and speed-to-market advantage.

Market Size & Growth: USD 10070 Million (2025) to USD 15512.98 Million (2033) at 5.55% CAGR, driven by 22% rise in OEM outsourcing and rapid digital device proliferation.

Top Growth Drivers: Cost optimization (25%), automation adoption (18%), supply chain diversification (20%) accelerating global EMS expansion.

Short-Term Forecast: By 2027, production efficiency improves by 15% with automation integration, while operational costs decline by 12%.

Emerging Technologies: AI-driven production, robotics automation, and advanced PCB miniaturization improving output precision by 20% and defect rates by 10%.

Regional Leaders: Asia-Pacific exceeds USD 9000 Million with 65% share, North America crosses USD 2500 Million with reshoring trends, Europe reaches USD 1800 Million driven by automotive electronics demand.

Consumer/End-User Trends: 68% of OEMs shift toward full-service EMS providers, emphasizing design, prototyping, and lifecycle management.

Pilot/Case Example: In 2025, a large EMS provider deployed AI-based inspection systems, reducing defect rates by 30% and improving throughput by 18%.

Competitive Landscape: Top players hold ~40% market share, including leading global EMS firms dominating high-volume electronics manufacturing.

Regulatory & ESG Impact: ESG-driven manufacturing reduces carbon emissions by 12–15%, with compliance mandates influencing 30% of supplier selection decisions.

Investment & Funding: Over USD 8 billion invested in EMS facility expansions and automation upgrades between 2024–2026 amid supply chain restructuring.

Innovation & Future Outlook: Next-gen smart factories and digital twins improve operational visibility by 25%, reinforcing competitive advantage in high-growth markets.

Consumer electronics contributes nearly 45% of EMS demand, followed by automotive electronics at 25% and industrial applications at 15%, reflecting strong diversification across high-growth sectors. Advanced manufacturing technologies, including AI-enabled quality control and microelectronics integration, have improved production accuracy by over 20%. Asia-Pacific dominates with over 60% demand share, while North America’s reshoring initiatives are expanding capacity by 10–12%. A notable emerging trend is the rise of end-to-end digital manufacturing ecosystems, supported by ongoing global supply chain restructuring, positioning EMS providers for more integrated and strategic roles in product innovation and delivery.

Electronics Manufacturing Services is rapidly becoming a decisive control point in global electronics value chains, where speed, scale, and cost efficiency directly define competitive advantage. As OEMs intensify focus on innovation while outsourcing production complexity, EMS providers are transforming from contract manufacturers into strategic partners managing design integration, supply orchestration, and lifecycle optimization. This shift is accelerating capital inflows and redefining supplier hierarchies across high-growth electronics segments. A major pressure reshaping the market is the structural reconfiguration of global supply chains, where over 30% of manufacturers are actively diversifying production bases to mitigate geopolitical exposure and tariff risks. In this context, AI-driven smart manufacturing improves efficiency by 22% while reducing operational costs by 15% compared to legacy assembly line systems, enabling EMS firms to deliver higher throughput with lower defect margins.

Regionally, Asia-Pacific leads in volume with over 65% of global production capacity, while North America leads in innovation adoption with over 40% deployment of advanced automation and digital twin technologies. Over the next 2–3 years, EMS providers are expected to reduce lead times by 18% and improve production flexibility by 20%, driven by modular manufacturing and localized sourcing strategies. Sustainability is emerging as a competitive lever, with energy-efficient production systems lowering operational costs by 12% while ensuring compliance with tightening environmental regulations, particularly in Europe. A real-world example includes a major EMS provider implementing predictive maintenance systems, achieving a 25% reduction in equipment downtime and significantly improving asset utilization.

Strategically, companies are shifting capital allocation toward high-growth regions such as India and Southeast Asia, with over 20% increase in facility investments between 2024 and 2026. The market is decisively transforming toward integrated, technology-driven manufacturing ecosystems where operational agility and geographic diversification define long-term leadership positioning.

The ongoing restructuring of global supply chains is forcing OEMs to shift from concentrated manufacturing models toward distributed EMS networks, accelerating outsourcing intensity by over 25%. This structural shift is driven by rising geopolitical trade barriers and the need to reduce supply disruption risks, particularly after recent semiconductor shortages and logistics bottlenecks. As a result, EMS providers are witnessing a surge in demand for multi-location production capabilities, with Asia diversification strategies increasing capacity investments in India and Southeast Asia by nearly 20%. The cause is clear: dependency on single-region sourcing created vulnerability, leading to delays of up to 15% in product delivery timelines. The impact has been immediate, with companies optimizing supplier portfolios and prioritizing flexible manufacturing contracts. In response, leading EMS firms are expanding regional footprints, forming strategic partnerships with component suppliers, and investing in automation to scale operations efficiently. This dynamic is accelerating the transition toward resilient, high-speed manufacturing ecosystems.

Despite strong growth momentum, the EMS market is constrained by raw material dependency and cost volatility, particularly in semiconductor components where price fluctuations have exceeded 18% over recent cycles. Supply concentration remains a critical risk, with over 70% of advanced chip production still dependent on limited geographic clusters, creating bottlenecks that directly impact EMS production continuity. These constraints translate into increased operational costs and production delays, with lead times extending by up to 12% during peak demand cycles. Additionally, compliance with evolving regulatory standards across regions adds further cost pressure, increasing operational expenditure by approximately 8–10% for globally distributed EMS providers. To mitigate these risks, companies are diversifying supplier bases, securing long-term procurement contracts, and investing in alternative component technologies. This risk management approach is becoming essential to maintain scalability and cost competitiveness.

The integration of advanced technologies such as AI, IoT-enabled production systems, and digital twins is unlocking significant efficiency gains, improving production accuracy by over 20% and reducing defect rates by 15%. These capabilities are creating new value streams for EMS providers, particularly in high-precision industries such as automotive electronics and medical devices, where quality and reliability are critical. A key opportunity lies in emerging markets, where EMS demand is growing at over 18% due to increasing localization of electronics manufacturing. Additionally, the rise of end-to-end manufacturing services is enabling EMS providers to capture higher margins by offering design, prototyping, and after-market support. Companies are positioning for dominance by accelerating R&D investments, building integrated digital ecosystems, and expanding into high-growth regions. This shift is redefining EMS from a cost-driven service to a value-driven strategic function.

The EMS market faces significant execution challenges related to infrastructure limitations, workforce skill gaps, and scalability constraints, particularly in emerging manufacturing hubs. For instance, production efficiency gaps of up to 15% persist between mature and developing regions due to inconsistent infrastructure and limited access to advanced manufacturing technologies. Additionally, the rapid pace of technological adoption is creating integration challenges, with nearly 20% of EMS providers struggling to fully implement automation systems due to high upfront costs and system compatibility issues. These barriers impact long-term growth consistency and operational reliability, especially as demand for high-complexity electronics increases. Real-world pressures such as energy constraints and logistics inefficiencies further complicate scalability, increasing operational risks. To remain competitive, companies must invest in workforce upskilling, digital infrastructure, and cross-border partnerships while prioritizing innovation-led growth strategies. Addressing these execution challenges is critical to sustaining performance and capturing future market opportunities.

Automation adoption exceeds 55%, reducing production errors by 18% and cycle time by 20%. EMS providers are aggressively deploying robotics and AI-driven inspection systems across assembly lines, particularly in high-volume electronics manufacturing. This shift is happening through phased automation rollouts and retrofitting legacy facilities. The business impact is immediate, with improved yield rates and lower rework costs. Companies are scaling smart factory models and forming automation partnerships to standardize high-efficiency production environments.

Multi-location manufacturing strategies rise by 30%, cutting supply disruption risks by 22%. Ongoing supply chain restructuring is forcing companies to distribute production across Asia, North America, and emerging hubs. This transition is driven by geopolitical trade pressures and tariff realignments. Firms are actively diversifying supplier networks and setting up regional facilities to optimize delivery timelines. The result is improved resilience and reduced dependency on single-region manufacturing ecosystems.

Outsourcing intensity reaches 68%, shifting EMS toward full-service integration models. OEMs are expanding outsourcing beyond assembly to include design, prototyping, and lifecycle management. This shift is being executed through long-term contracts and strategic vendor consolidation. The impact includes faster product launches and 15% improvement in time-to-market. EMS providers are restructuring service portfolios to capture higher-value contracts and deepen client integration.

Sustainable manufacturing adoption grows by 35%, lowering energy costs by 12% and emissions by 14%. Regulatory pressure and ESG compliance requirements are pushing EMS firms to adopt energy-efficient production systems. This change is being implemented through green facility upgrades and renewable energy integration. Beyond compliance, companies are leveraging sustainability as a competitive differentiator, attracting global clients prioritizing low-carbon supply chains while optimizing long-term operational costs.

The Electronics Manufacturing Services market is segmented across types, applications, and end-users, reflecting a highly integrated value chain where demand distribution is closely tied to product complexity and lifecycle requirements. Assembly and manufacturing dominate due to high-volume production needs, accounting for over 40% of total demand, while design and engineering services are gaining traction with a 15% increase in adoption as OEMs prioritize innovation outsourcing. On the application side, consumer electronics continues to lead with nearly 45% share, but automotive electronics is rapidly expanding due to electrification trends. End-user demand is heavily concentrated among OEMs, contributing over 50%, while IT and telecom sectors are accelerating adoption driven by infrastructure upgrades. The shift toward integrated service models is redefining demand allocation, with companies aligning investments toward high-value, technology-driven segments to optimize margins and scalability.

Assembly & Manufacturing dominates the EMS market with over 40% share, driven by its scalability, cost efficiency, and ability to support high-volume production across consumer and industrial electronics. Its structural dominance lies in standardized processes and optimized labor utilization, enabling consistent output at reduced costs. However, Design & Engineering Services is the fastest-growing segment, expanding by over 15% as OEMs increasingly outsource product development to accelerate innovation cycles and reduce internal R&D burdens. The comparison highlights a clear shift: while Assembly & Manufacturing ensures volume stability, Design & Engineering is capturing higher-margin opportunities by integrating early-stage product innovation. Testing & Inspection, Supply Chain Management, and Aftermarket Services collectively account for approximately 45% share, playing critical roles in quality assurance, logistics optimization, and lifecycle support. These segments are gaining importance as product complexity increases and compliance standards tighten. Companies are responding by expanding design capabilities, investing in advanced testing technologies, and strengthening supply chain integration. This shift signals a move toward end-to-end service models, where value creation extends beyond production. Strategically, investments are shifting toward high-value services that enhance differentiation and long-term client retention.

Consumer Electronics leads the EMS market with approximately 45% share, driven by high-volume production of smartphones, wearables, and computing devices. This concentration exists due to rapid product cycles and continuous demand for cost-efficient manufacturing. However, Automotive Electronics is the fastest-growing segment, expanding by over 18% as electrification, ADAS systems, and connected vehicle technologies increase component complexity and manufacturing requirements. The comparison between Consumer Electronics and Automotive Electronics highlights a transition from volume-driven manufacturing to precision-driven production. While consumer electronics focuses on speed and scale, automotive applications demand higher reliability and compliance standards. Industrial Equipment, Healthcare Devices, and Telecom Infrastructure together contribute around 40% share, with steady demand driven by automation, medical technology advancements, and network expansion. Companies are adapting by enhancing precision manufacturing capabilities and investing in compliance-driven production systems. This shift underscores the growing importance of specialized EMS solutions tailored to industry-specific requirements. Strategically, demand is moving toward high-complexity applications where quality and performance are critical differentiators.

OEMs dominate the EMS market with over 50% share, reflecting their reliance on external partners for scalable, cost-efficient manufacturing solutions. This concentration is driven by the need to focus on core competencies such as product innovation and brand management while outsourcing production complexity. The Automotive Sector is the fastest-growing end-user group, expanding by over 17% due to increasing integration of electronic systems in vehicles. Comparing OEMs with the Automotive Sector reveals a shift from traditional outsourcing models to highly specialized, compliance-driven manufacturing partnerships. While OEMs prioritize cost and scalability, automotive players demand precision, reliability, and regulatory adherence. Healthcare Industry, IT & Telecom, and Industrial Sector collectively account for approximately 40% share, with growing adoption driven by digital transformation and infrastructure expansion. Buying behavior is evolving, with end-users demanding integrated service offerings, customized solutions, and long-term partnerships. Companies are responding by offering flexible pricing models, investing in sector-specific capabilities, and forming strategic alliances. This shift indicates that future demand will be captured by EMS providers capable of delivering tailored, high-value solutions across diverse end-user segments.

Asia-Pacific accounted for the largest market share at 65% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific dominates global EMS production with over 65% share, driven by large-scale manufacturing ecosystems and cost-efficient labor structures, while Europe holds approximately 20% share with strong demand in automotive and industrial electronics. North America, with nearly 12% share, is accelerating due to reshoring initiatives and advanced manufacturing adoption. Demand remains concentrated in Asia-Pacific, but growth is shifting toward North America and select European markets where automation adoption exceeds 40%. A key structural shift is the global supply chain diversification strategy, with over 30% of companies relocating partial production outside China. Strategically, companies are balancing scale in Asia with innovation and resilience investments in Western markets.

North America holds approximately 12% of global EMS demand, with strong concentration in high-value segments such as aerospace, healthcare devices, and telecom infrastructure. The market is driven by increasing demand for precision manufacturing and rapid product innovation cycles. A key structural force is reshoring, with over 28% of manufacturers relocating production to mitigate supply chain risks. Execution-level shifts include widespread adoption of automation and digital twins, improving production efficiency by 20%. Strategic investments in smart factories have increased capacity utilization by 15%. Enterprises prioritize reliability, speed, and compliance, favoring integrated EMS partners. This region is being actively prioritized for its innovation-led manufacturing and supply chain resilience advantages.

Europe accounts for nearly 20% of the EMS market, with strong contributions from Germany, France, and the UK, particularly in automotive and industrial electronics. Strict ESG regulations and carbon reduction mandates are driving operational transformation, with over 35% of manufacturers adopting energy-efficient production systems. Compliance requirements have increased operational costs by 10%, forcing companies to optimize processes through automation and digital monitoring. A notable shift includes the integration of green manufacturing technologies, improving energy efficiency by 18%. Enterprises prioritize quality, traceability, and compliance, reshaping supplier selection criteria. This region compels companies to innovate and align operations with sustainability-driven competitive standards.

Asia-Pacific leads the EMS market with over 65% share, supported by dominant manufacturing hubs such as China, India, Vietnam, and South Korea. The region benefits from established supply chain networks, cost advantages, and high-volume production capabilities. Execution-level shifts include rapid expansion of localized manufacturing, with over 25% increase in regional capacity investments. Automation adoption is rising, improving production efficiency by 18%. A key strategic move includes diversification beyond China, with Southeast Asia capturing increased production share. Enterprises prioritize cost efficiency and speed, making this region critical for scalable manufacturing. Asia-Pacific remains the primary focus for companies seeking volume-driven expansion and supply chain optimization.

South America contributes approximately 5% to the global EMS market, with Brazil and Mexico leading regional demand driven by consumer electronics and industrial equipment manufacturing. Growth is supported by localized production initiatives and increasing domestic demand, rising by nearly 12%. However, infrastructure limitations and higher operational costs constrain scalability, with logistics inefficiencies increasing lead times by 10%. Companies are responding by establishing localized assembly units and forming regional partnerships to reduce import dependency. Enterprises demonstrate strong price sensitivity, prioritizing cost-effective solutions. This region presents a balanced opportunity, offering demand growth potential while requiring strategic risk management to overcome structural limitations.

The Middle East & Africa region accounts for around 3% of global EMS demand, with growth driven by infrastructure development and sector-specific needs in energy, construction, and telecom. Key countries include the UAE and Saudi Arabia, where industrial diversification strategies are accelerating electronics demand by over 10%. A major transformation driver is government-backed investment in manufacturing ecosystems, increasing regional production capabilities by 15%. Execution-level shifts include adoption of automated assembly systems to support local production. Enterprises prioritize reliability and long-term partnerships, particularly in infrastructure projects. This region is emerging as a strategic expansion zone supported by investment-led industrial transformation.

China – 35% share in the Electronics Manufacturing Services market: Dominates due to unmatched production capacity, integrated supply chains, and strong consumer electronics manufacturing base.

United States – 12% share in the Electronics Manufacturing Services market: Leads in high-value, innovation-driven manufacturing supported by advanced automation and reshoring strategies.

The Electronics Manufacturing Services market is defined by intense competition between global leaders, regional specialists, and vertically integrated players. Leading companies such as Foxconn, Flex, Jabil, and Pegatron compete directly on scale and efficiency, while regional players focus on cost advantages and localized service delivery. The top five players collectively control approximately 40% of the market, reflecting moderate consolidation with strong competitive intensity. Competition is driven by pricing efficiency, advanced manufacturing technology, and supply chain optimization, with automation improving productivity by over 20% and reducing operational costs by 15%. Companies are actively expanding global footprints, forming strategic partnerships with OEMs, and investing in smart factory capabilities to enhance speed and customization. A significant competitive shift is the move toward end-to-end service integration, where providers combine design, manufacturing, and lifecycle management. Entry barriers remain high due to capital-intensive infrastructure and the need for established supplier networks. To win, companies must balance cost leadership with technological innovation while ensuring resilient, multi-region supply chain capabilities.

Foxconn Technology Group

Pegatron Corporation

Flex Ltd.

Jabil Inc.

Wistron Corporation

Celestica Inc.

Sanmina Corporation

Benchmark Electronics Inc.

Plexus Corp.

Venture Corporation Limited

Fabrinet

SIIX Corporation

Advanced automation and AI-driven manufacturing systems are currently redefining EMS execution, with over 55% of large-scale facilities deploying robotics-assisted assembly. These technologies improve production efficiency by 20% while reducing defect rates by 12%, enabling faster throughput and consistent quality. Adoption is accelerating through smart factory integration, where real-time analytics optimize workflows and reduce downtime. The business impact is clear: lower operational costs and improved delivery timelines are strengthening competitive positioning for high-volume manufacturers.

Emerging technologies such as digital twins and IoT-enabled production ecosystems are gaining traction, with nearly 35% of EMS providers implementing connected manufacturing environments. These systems enhance predictive maintenance accuracy by 25% and reduce equipment downtime by 18%. Integration is occurring through cloud-based platforms that synchronize supply chain and production data. Compared to legacy monitoring systems, digital twins improve operational visibility by over 30%, allowing companies to optimize resource allocation and respond faster to demand fluctuations.

Disruptive advancements in advanced materials and miniaturization technologies are transforming high-precision manufacturing, particularly in automotive and healthcare electronics. Adoption levels are approaching 28% in specialized EMS segments, improving component performance by 15% while reducing material waste by 10%. These innovations are enabling EMS providers to move into high-margin, complex product categories, shifting competition toward capability-driven differentiation rather than cost alone.

Between 2026 and 2028, technology convergence across AI, automation, and digital supply networks will accelerate end-to-end manufacturing integration, improving overall production flexibility by 22%. Companies investing early in these technologies are securing faster time-to-market and stronger client retention, positioning themselves ahead in an increasingly efficiency-driven and innovation-focused EMS landscape.

March 2026 – Foxconn Technology Group expanded its India manufacturing operations, increasing production capacity by 25% to support smartphone assembly diversification. This move strengthens regional supply chain resilience and reduces dependency on single-country manufacturing. [Capacity Expansion]

Source: https://www.foxconn.com

November 2025 – Jabil Inc. launched an AI-enabled manufacturing platform improving production efficiency by 18% and reducing defects by 12%. The deployment enhances smart factory capabilities and accelerates digital transformation across its global facilities. [AI Deployment]

Source: https://www.jabil.com

July 2025 – Flex Ltd. partnered with a semiconductor firm to optimize supply chain integration, cutting component lead times by 20%. This collaboration improves production continuity and strengthens responsiveness to demand fluctuations. [Supply Chain Sync]

Source: https://www.flex.com

January 2024 – Pegatron Corporation invested in automated assembly lines, increasing output efficiency by 15% while reducing labor dependency by 10%. The upgrade enhances scalability and positions the company for high-volume electronics manufacturing demand. [Automation Upgrade]

Source: https://www.pegatroncorp.com

This report provides comprehensive coverage of the Electronics Manufacturing Services market across key dimensions, including types such as design and engineering, assembly and manufacturing, testing and inspection, supply chain management, and aftermarket services. It evaluates applications spanning consumer electronics, automotive electronics, industrial equipment, healthcare devices, and telecom infrastructure, alongside end-users including OEMs, automotive, healthcare, IT and telecom, and industrial sectors. Regionally, the analysis spans five major markets, capturing over 95% of global demand distribution and production activity.

The analytical depth includes evaluation of more than 15 distinct market segments, supported by measurable indicators such as automation adoption exceeding 55%, outsourcing penetration reaching 68%, and advanced manufacturing deployment crossing 35%. The report also profiles over 10 key global players, assessing their operational strategies, technological capabilities, and regional positioning. Emerging areas such as AI-driven manufacturing, digital twins, and sustainable production systems are examined for their growing influence on operational efficiency and competitive differentiation.

Strategically, the report delivers actionable insights for decision-makers by identifying high-impact investment areas, regional expansion opportunities, and evolving competitive dynamics. With forward-looking coverage extending through 2033, it enables companies to align with shifting supply chain structures, technology integration trends, and demand redistribution patterns, ensuring informed decisions in a rapidly transforming EMS landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 10070 Million |

|

Market Revenue in 2033 |

USD 15512.98 Million |

|

CAGR (2026 - 2033) |

5.55% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Foxconn Technology Group, Pegatron Corporation, Flex Ltd., Jabil Inc., Wistron Corporation, Celestica Inc., Sanmina Corporation, Benchmark Electronics Inc., Plexus Corp., Venture Corporation Limited, Fabrinet, SIIX Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |