Reports

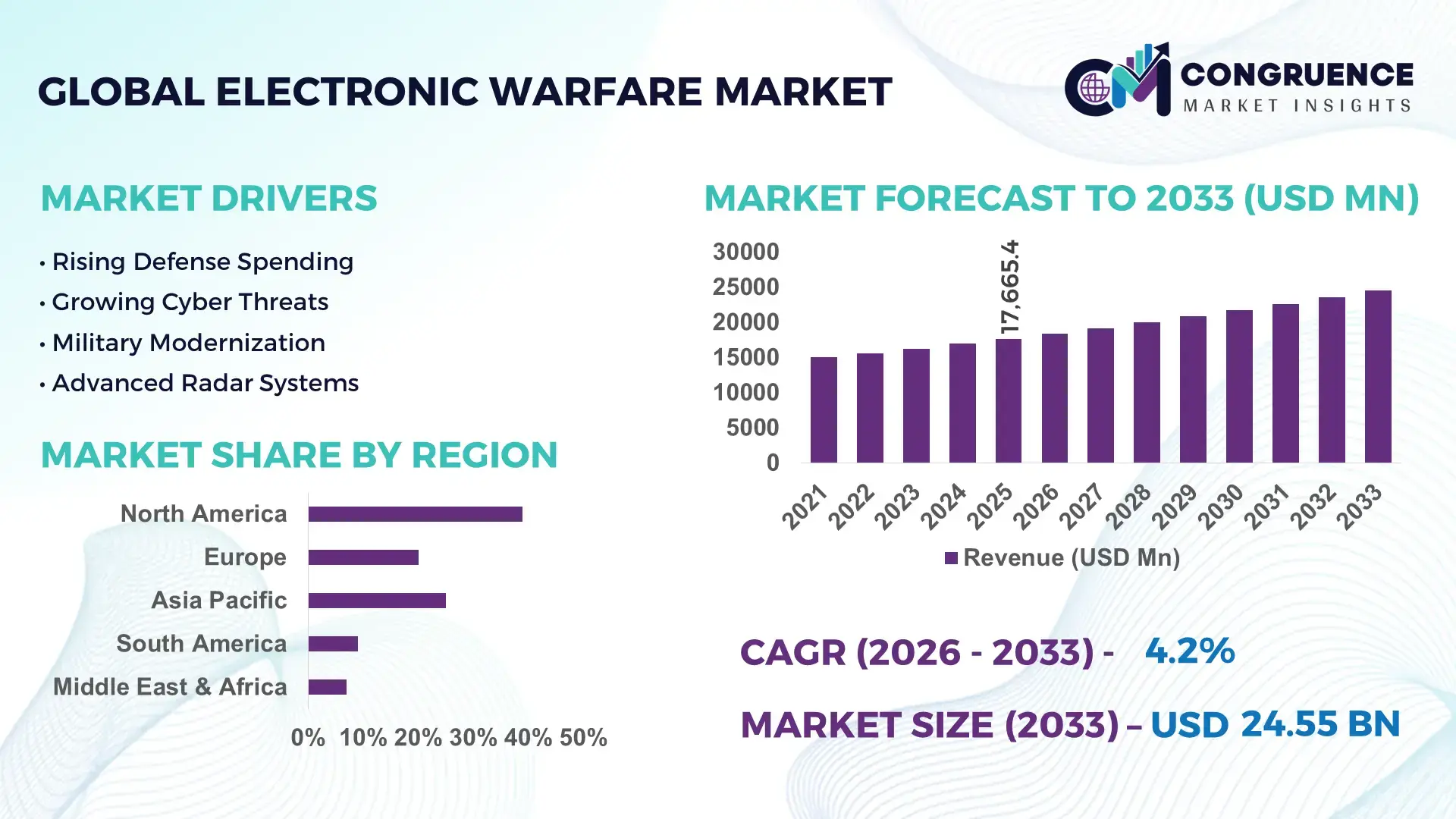

The Global Electronic Warfare Market was valued at USD 17665.38 Million in 2025 and is anticipated to reach a value of USD 24550.74 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. Growth is being driven by accelerated deployment of spectrum-dominance systems, counter-drone capabilities, cognitive electronic warfare platforms, and modernization programs linked to evolving geopolitical tensions across Europe, the Indo-Pacific, and the Middle East.

The United States remains the dominant country, accounting for approximately 38% of global electronic warfare procurement activity, supported by multi-billion-dollar defense modernization investments and extensive integration across airborne, naval, and land-based platforms. China follows with an estimated 22% share, driven by rapid military-electronics expansion and indigenous radar-jamming development programs. Advanced electronic attack and electronic support technologies are now deployed across more than 65% of newly commissioned high-end defense platforms in these leading markets, reflecting the strategic priority placed on electromagnetic spectrum superiority following ongoing regional security challenges and lessons derived from recent conflict environments.

Organizations and defense agencies that prioritize next-generation electronic protection architectures, AI-enabled threat detection, and multi-domain interoperability are positioned to secure stronger operational resilience and long-term strategic advantage.

Market Size & Growth: USD 17,665.38 million in 2025 rising to USD 24,550.74 million by 2033 at 4.2% CAGR, supported by advanced spectrum-dominance and counter-drone deployments.

Top Growth Drivers: Electronic modernization programs (+31%), unmanned threat proliferation (+27%), and AI-enabled defense integration (+24%) drive procurement activity.

Short-Term Forecast: By 2028, mission-response efficiency is projected to improve by 18% through automated threat identification and signal-processing upgrades.

Emerging Technologies: AI-assisted electronic attack, cognitive EW systems, and software-defined architectures are reducing response times by 20–30%.

Regional Leaders: North America exceeds USD 8.8 billion, Asia-Pacific approaches USD 6.4 billion, and Europe surpasses USD 5.2 billion, supported by defense digitalization.

Consumer/End-User Trends: Over 60% of advanced defense platforms now integrate electronic support and protection capabilities as standard mission systems.

Pilot/Case Example: In 2026, advanced counter-UAS electronic warfare trials demonstrated threat-neutralization effectiveness improvements exceeding 25%.

Competitive Landscape: Leading suppliers collectively control about 45% market share, with competition centered on integrated multi-domain warfare capabilities.

Regulatory & ESG Impact: Defense-electronics localization initiatives increased domestic procurement participation by nearly 15% across several strategic markets.

Investment & Funding: More than USD 10 billion in modernization and capability-expansion investments support resilient supply chains and regional manufacturing.

Innovation & Future Outlook: Next-generation cognitive jamming, autonomous spectrum management, and AI-driven electromagnetic operations are reshaping global defense strategies.

The Electronic Warfare Market is witnessing strong demand across airborne surveillance, naval defense, counter-drone operations, and integrated battlefield management systems. Recent innovations include AI-enabled signal classification, cognitive jamming platforms, and software-defined electronic attack architectures that improve threat response accuracy by more than 20%. Growing emphasis on domestic defense-electronics production and secure component sourcing is influencing procurement strategies, while multi-domain operational requirements continue to drive the market toward more adaptive and networked electronic warfare capabilities.

Electronic warfare has become a strategic capability underpinning modern defense competitiveness, operational resilience, and technology investment decisions. As military platforms become increasingly networked, control of the electromagnetic spectrum is emerging as a decisive operational advantage. Defense agencies are restructuring procurement strategies around software-defined architectures, while supply-chain localization initiatives in the United States, India, and Japan are reducing dependency on foreign electronic components. More than 60% of newly deployed advanced defense platforms now integrate electronic support, attack, or protection functions as core mission systems rather than optional capabilities.

Technology modernization is accelerating performance gains across the sector. AI-enabled signal processing systems can improve threat identification speed by approximately 30% compared with legacy rule-based electronic warfare suites while reducing operator workload by nearly 20%. The United States leads in deployment scale and platform integration, whereas China is advancing rapidly through indigenous component development and high-volume defense-electronics manufacturing. A practical example is the deployment of cognitive counter-drone systems that automatically classify and neutralize spectrum threats in contested environments, improving mission effectiveness and reducing response latency.

Over the next two to three years, adoption of software-upgradable electronic warfare platforms is expected to exceed 70% among newly commissioned high-end defense assets. Companies are expanding partnerships with semiconductor, AI, and radar-specialist firms to accelerate capability development. Organizations that establish interoperable, upgradeable, and spectrum-dominant solutions will secure stronger competitive positioning as electromagnetic superiority becomes a core defense procurement priority.

Defense modernization programs are increasingly centered on electromagnetic spectrum superiority, creating sustained demand for advanced electronic warfare capabilities. More than 65% of next-generation combat platforms now incorporate integrated electronic attack and protection systems, while AI-enabled signal processing improves threat detection efficiency by approximately 25–30%. Recent conflict environments have demonstrated the operational importance of counter-drone and anti-jamming technologies, prompting procurement acceleration across the United States, India, and Poland. The result is a direct increase in investment across radar, communications intelligence, and electronic countermeasure systems. Companies are responding through joint development programs, indigenous manufacturing expansion, and software-defined architecture innovation. A notable strategic insight is that upgradeable electronic warfare software is becoming as important as hardware performance, shifting competition toward lifecycle capability management rather than platform acquisition alone.

Electronic warfare deployment remains constrained by high system integration costs and dependence on specialized semiconductor, RF, and microwave components. Approximately 40% of critical electronic warfare subsystems rely on complex supply chains with limited qualified suppliers, while advanced gallium nitride component costs remain 15–20% higher than conventional alternatives. Export-control frameworks affecting sensitive defense electronics create procurement delays and certification challenges, particularly for countries seeking rapid capability expansion. These constraints increase deployment timelines, pressure operating budgets, and complicate fleet-wide modernization programs. Companies are mitigating risks through supplier diversification, domestic production investments, and long-term procurement agreements. A key operational insight is that supply-chain resilience has become a procurement differentiator, influencing contract awards alongside technical performance and mission effectiveness.

The transition toward cognitive electronic warfare creates significant opportunities for technology providers and defense integrators. AI-assisted threat recognition can improve spectrum analysis efficiency by nearly 35%, while automated mission adaptation reduces operator intervention requirements by approximately 25%. India, South Korea, and Australia are expanding investment in indigenous defense-electronics ecosystems, creating new partnership and localization opportunities. Emerging software-defined architectures allow capability upgrades without major hardware replacement, lowering lifecycle costs and accelerating deployment cycles. Companies are increasing R&D spending, forming semiconductor partnerships, and developing open-system ecosystems to capture this shift. A particularly valuable opportunity lies in counter-unmanned systems, where rapidly evolving threat profiles require continuously adaptive electronic countermeasure solutions rather than fixed-function hardware deployments.

The most significant long-term challenge is integrating electronic warfare systems across air, land, sea, space, and cyber domains while maintaining operational consistency. More than 50% of defense organizations report interoperability limitations between legacy and next-generation mission systems, while cyber-related vulnerabilities account for nearly 20% of identified modernization concerns. As electronic warfare platforms become increasingly software-driven, maintaining secure updates, data integrity, and real-time interoperability becomes more complex. The United Kingdom and United States are investing heavily in digital mission-network architectures to address these requirements. Companies must strengthen cybersecurity frameworks, workforce expertise, and systems-engineering capabilities through partnerships and infrastructure investments. The critical strategic insight is that future competitiveness will depend not only on electronic attack effectiveness but also on seamless integration across connected defense ecosystems.

• AI-Native Spectrum Operations Electronic warfare platforms are shifting from rule-based processing to AI-assisted spectrum management, with automated signal classification adoption exceeding 45% across newly deployed systems. Threat identification speeds have improved by nearly 30%, while operator workload has declined by around 20%. Defense contractors are expanding software partnerships and integrating machine-learning algorithms directly into mission architectures to accelerate response cycles and reduce dependence on manual electronic intelligence workflows.

• Counter-Drone Capability Expansion Unmanned aerial system proliferation has increased demand for dedicated electronic countermeasure deployments, with procurement activity rising by approximately 35% across key defense programs. More than 50% of recent electronic warfare upgrades now include counter-UAS functionality. Companies are restructuring product portfolios around modular jamming systems and scalable electronic attack capabilities as military organizations prioritize low-cost threat neutralization over kinetic interception in contested operational environments.

• Software-Defined Platform Migration Software-defined electronic warfare architectures now account for nearly 60% of next-generation system development programs, reducing upgrade timelines by about 25% compared with hardware-centric designs. Supply-chain pressures and component availability concerns are encouraging greater reliance on software-driven capability enhancements. Manufacturers are increasing investment in open-system frameworks and digital engineering approaches to improve interoperability and extend platform service life without extensive hardware replacement.

• Domestic Supply Chain Localization Strategic procurement policies in the United States, India, and Japan are accelerating domestic defense-electronics sourcing, with localized component procurement increasing by roughly 15–20% in recent modernization initiatives. Companies are forming semiconductor alliances, expanding regional manufacturing footprints, and securing long-term supplier agreements. A less visible outcome is improved program predictability, as localized sourcing reduces certification delays and strengthens operational readiness across critical electronic warfare deployments.

Electronic Attack remains the leading segment, accounting for the largest share of deployment activity due to its direct role in disrupting adversary communications, radar networks, and command systems. Its dominance is supported by broad integration across airborne, naval, and land-based platforms, with more than 55% of advanced electronic warfare modernization programs prioritizing offensive spectrum-control capabilities. The segment benefits from scalability, mission flexibility, and increasing adoption of software-defined jamming technologies. Companies are investing in adaptive electronic attack systems and AI-enhanced waveform generation to improve mission effectiveness while reducing response latency.

Electronic Support is emerging as the fastest-growing segment as defense organizations prioritize real-time spectrum awareness and threat intelligence. Adoption of advanced signal analysis platforms has increased by approximately 28% in recent procurement cycles. Meanwhile, Electronic Protection continues gaining relevance through anti-jamming and resilient communications requirements. Radar Jamming remains strategically important for suppression missions, while Signal Intelligence is expanding through growing demand for persistent surveillance and battlefield awareness. Companies are increasingly pursuing integrated solutions that combine attack, protection, and intelligence functions within unified mission architectures, reflecting a broader shift toward multi-domain operational effectiveness.

Surveillance remains the dominant application segment, supported by persistent demand for electromagnetic spectrum monitoring, situational awareness, and threat tracking across modern defense operations. Approximately 50% of newly deployed electronic warfare capabilities include dedicated surveillance functions as a core operational requirement. The segment benefits from increasing sensor integration, data fusion technologies, and real-time battlefield visibility needs. Defense technology providers are scaling advanced monitoring platforms and expanding analytics capabilities to strengthen mission intelligence and operational decision-making.

Threat Detection is the fastest-growing application as armed forces prioritize rapid identification of evolving spectrum threats, drone activity, and electronic attacks. Advanced detection systems have improved response accuracy by nearly 25% compared with earlier-generation platforms. Intelligence Gathering continues to expand through increased deployment of signals intelligence and electronic support assets. Communication Jamming remains critical for denying adversary coordination capabilities, while Battlefield Management is becoming more integrated with network-centric operational frameworks. Companies are responding through automation, AI-enabled analytics, and deeper platform integration, positioning electronic warfare systems as central components of command-and-control ecosystems.

Defense Forces represent the dominant end-user segment due to extensive deployment requirements across ground, air, maritime, and joint-force operations. More than 45% of electronic warfare procurement programs are directly linked to force modernization initiatives and operational readiness objectives. Large-scale infrastructure dependency, continuous mission requirements, and expanding spectrum-contested environments reinforce demand concentration within this segment. Suppliers are tailoring integrated electronic warfare suites, long-term support contracts, and modular upgrade pathways to address evolving operational requirements.

Intelligence Agencies are emerging as the fastest-growing end-user segment as governments increase investments in electronic intelligence collection, threat monitoring, and strategic surveillance capabilities. Adoption of advanced signals intelligence platforms has risen by approximately 30% in recent acquisition cycles. Air Force and Naval Forces continue investing heavily in platform-specific electronic protection and electronic attack systems, while Homeland Security Agencies are expanding counter-drone and border-monitoring capabilities. Defense Contractors remain influential buyers through testing, integration, and technology development programs. Companies are strengthening ecosystem partnerships and mission-specific customization strategies to capture demand from increasingly specialized end-user requirements.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

Advanced Spectrum Dominance Modernization

North America remains the largest electronic warfare market, supported by extensive defense modernization programs, advanced defense-electronics manufacturing capabilities, and strong integration of AI-enabled mission systems. The region accounts for approximately 39% of global deployment activity, with electronic warfare capabilities embedded across next-generation aircraft, naval platforms, and integrated command networks. Increased focus on counter-drone operations, electromagnetic spectrum management, and software-defined architectures is accelerating procurement activity. More than 65% of newly specified high-end defense platforms in the region now incorporate advanced electronic support and protection functions. Companies are expanding digital engineering capabilities and strengthening partnerships with semiconductor and software providers to improve operational adaptability and mission readiness.

United States Market Outlook: The United States represents the largest national market due to its unmatched defense-electronics ecosystem, extensive research infrastructure, and large-scale platform modernization programs. AI-enabled electronic warfare integration has become a procurement priority across multiple military branches, while domestic semiconductor investments support supply-chain resilience. More than 70% of advanced combat-system upgrades include spectrum-management enhancements, positioning the country as a technology leader in cognitive electronic warfare, electronic attack, and integrated mission-system development.

Defense Modernization and Interoperability Focus

Europe is strengthening its position through accelerated military modernization, interoperability initiatives, and indigenous defense technology development. The region contributes approximately 26% of global market activity, supported by growing investments in electronic intelligence, radar countermeasures, and secure communications systems. Ongoing security concerns have increased procurement of electronic protection and electronic support capabilities across several European defense programs. Cross-border industrial partnerships are becoming more common, improving technology sharing and manufacturing efficiency. Deployment of digital mission systems and software-upgradable electronic warfare architectures has increased by nearly 20% across major modernization projects, reinforcing long-term operational readiness objectives.

Germany Market Outlook: Germany serves as a key electronic warfare hub due to its advanced defense manufacturing base, engineering expertise, and focus on integrated military-electronics modernization. National investments in secure communications, electronic intelligence, and battlefield digitization continue to expand. The country has increased procurement of electronically protected mission systems and supports extensive collaboration between defense contractors and research institutions, strengthening its role in next-generation electronic warfare innovation and operational integration.

Rapid Deployment and Indigenous Expansion

Asia-Pacific is the fastest-expanding market, driven by defense-industrial expansion, indigenous technology development, and rising deployment of advanced military platforms. The region accounts for approximately 24% of global electronic warfare activity and is experiencing significant investment in radar-jamming systems, signal intelligence infrastructure, and AI-assisted spectrum management capabilities. Governments are prioritizing local manufacturing and technology transfer programs to reduce external dependence. More than 30% of recent electronic warfare procurement programs in key Asia-Pacific countries include domestic production requirements. Companies are responding through regional partnerships, localized production facilities, and expanded R&D operations to support evolving operational requirements.

China Market Outlook: China maintains a strong position through large-scale defense-electronics manufacturing, substantial military modernization efforts, and extensive investment in indigenous component development. The country continues expanding deployment of advanced electronic attack, electronic support, and integrated intelligence systems across multiple operational domains. Domestic suppliers play a central role in technology development, while sustained investment in AI-enabled defense applications strengthens national capabilities and accelerates electronic warfare system deployment.

Targeted Security Capability Enhancement

South America represents a developing electronic warfare market characterized by selective modernization programs and increasing focus on surveillance, border security, and communications protection. The region contributes a smaller share of global demand but continues investing in mission-critical electronic intelligence and monitoring systems. Defense agencies are prioritizing operational efficiency and affordability, leading to greater interest in modular and upgradeable electronic warfare solutions. Infrastructure limitations and budget constraints remain important considerations; however, deployment activity has increased by approximately 15% across selected modernization initiatives. Companies are focusing on partnerships, technology transfer agreements, and localized support services to strengthen regional presence.

Brazil Market Outlook: Brazil leads the regional market through its established aerospace sector, defense-industrial capabilities, and ongoing modernization of military communications and surveillance infrastructure. The country continues investing in electronic intelligence, border-monitoring technologies, and integrated mission systems. Domestic defense programs encourage local participation and technology development, while expanding operational requirements are supporting adoption of advanced electronic support and protection capabilities across strategic security applications.

Strategic Defense Technology Investment

The Middle East & Africa market is shaped by defense modernization programs, security infrastructure expansion, and increasing investment in advanced military technologies. Countries across the region are deploying sophisticated electronic warfare systems to strengthen surveillance, communications security, and counter-drone operations. The region accounts for approximately 11% of global market activity and continues to prioritize rapid capability acquisition. Modernization programs have increased procurement of integrated electronic warfare solutions by nearly 18% over recent years. Companies are expanding regional partnerships, local maintenance capabilities, and technology collaboration initiatives to support long-term operational requirements.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant market in the region due to extensive defense modernization initiatives, industrial localization policies, and investment in advanced security technologies. The country is expanding domestic defense manufacturing capabilities while strengthening partnerships with international technology providers. Electronic warfare deployment is increasingly aligned with broader military transformation objectives, with growing emphasis on integrated command systems, counter-drone technologies, and advanced spectrum-management capabilities.

The electronic warfare market is led by competition between global defense technology leaders such as Lockheed Martin, RTX Corporation, Northrop Grumman, BAE Systems, and L3Harris Technologies, while specialized electronic warfare providers and regional defense manufacturers compete through niche capabilities and localization strategies. The top five players collectively control approximately 55–60% of market activity, reflecting high concentration in advanced platform integration and mission-critical systems. Competition centers on technology performance, spectrum-processing speed, and software adaptability, with AI-enabled systems improving threat identification efficiency by nearly 30% and software-defined architectures reducing upgrade timelines by about 25%. Companies are competing through strategic acquisitions, semiconductor partnerships, indigenous manufacturing expansion, and vertically integrated supply chains. The current competitive shift favors cognitive electronic warfare, open-system architectures, and lifecycle upgrade capability over hardware-centric differentiation. Entry barriers remain high due to certification requirements, classified technology access, and extensive R&D commitments. Winning requires superior interoperability, rapid software innovation, secure supply networks, and continuous mission-system modernization.

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

BAE Systems plc

L3Harris Technologies, Inc.

Saab AB

Thales Group

Leonardo S.p.A.

Elbit Systems Ltd.

Israel Aerospace Industries Ltd.

HENSOLDT AG

Rheinmetall AG

Bharat Electronics Limited

ASELSAN A.S.

Electronic warfare technology is rapidly shifting toward AI-enabled spectrum management, software-defined architectures, and advanced digital receivers. AI-assisted signal classification improves threat identification accuracy by approximately 25%, while software-defined electronic warfare systems reduce upgrade cycles by nearly 20% compared with hardware-dependent platforms. More than 60% of newly specified electronic warfare programs now incorporate open-system architectures to enable faster mission updates and interoperability. This transition provides operational flexibility, lowers lifecycle support requirements, and allows defense organizations to respond more quickly to evolving electromagnetic threats.

Emerging technologies include cognitive electronic warfare, gallium nitride (GaN)-based transmitters, and cloud-connected spectrum operations. GaN-powered systems deliver roughly 15% higher power efficiency and stronger signal performance than conventional technologies. Cognitive electronic warfare platforms automatically adapt to threat environments, reducing response times by around 30%. Adoption levels for AI-assisted mission software have surpassed 40% in advanced defense modernization programs. Companies investing in adaptive jamming, autonomous threat recognition, and integrated intelligence capabilities are gaining a competitive advantage through faster deployment and superior operational effectiveness.

Disruptive innovation is increasingly focused on multi-domain electronic warfare ecosystems, photonic processing, and autonomous counter-drone technologies. Compared with legacy rule-based systems, next-generation cognitive platforms improve operational decision speed by nearly 35%. Between 2026 and 2028, deployment of software-upgradable electronic warfare capabilities is expected to exceed 70% among advanced defense platforms. Organizations that accelerate integration of AI, advanced semiconductors, and adaptive spectrum-control technologies will secure stronger mission resilience, lower modernization costs, and greater long-term strategic relevance.

September 2024 – L3Harris Technologies initiated production of its Viper Shield all-digital electronic warfare suite for F-16 fleets across six countries. The compact 3U architecture supports advanced threat detection and electronic protection, accelerating international deployment schedules and strengthening spectrum-dominance capabilities.

November 2024 – L3Harris Technologies completed Safety of Flight qualification for the Viper Shield electronic warfare system supporting six international F-16 partners. Successful completion of extensive environmental and electrical testing reduced program risk and enabled progression toward operational flight testing and deliveries. Source: l3harris.com

May 2026 – Northrop Grumman advanced production plans for its Integrated Viper Electronic Warfare Suite after U.S. Air Force interest in 206 upgrade packages for F-16 aircraft. The initiative strengthens survivability capabilities while supporting broader electronic warfare modernization and manufacturing scale expansion. Source: axios.com

June 2026 – HENSOLDT was selected by the Netherlands as the primary contractor for a national electronic warfare system upgrade program. The modernization effort enhances electronic threat response capabilities and reinforces the company’s position within European defense-electronics modernization initiatives. Source: reuters.com

This report provides comprehensive coverage of the global electronic warfare market across key technology domains, deployment models, operational applications, and end-user segments. The analysis evaluates Electronic Attack, Electronic Protection, Electronic Support, Radar Jamming, and Signal Intelligence capabilities while assessing demand patterns across Surveillance, Threat Detection, Communication Jamming, Battlefield Management, and Intelligence Gathering functions. The study also examines procurement behavior among Defense Forces, Air Force, Naval Forces, Homeland Security Agencies, Defense Contractors, and Intelligence Agencies. More than 60% of current modernization programs emphasize software-defined and AI-enabled electronic warfare capabilities, highlighting the sector’s evolving technology landscape.

The report delivers detailed regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying deployment concentration, industrial capabilities, and investment priorities. It evaluates adoption trends, platform integration strategies, competitive positioning, supply-chain developments, and emerging technologies expected to influence operational requirements between 2026 and 2033. The findings support expansion planning, technology investment decisions, partnership development, risk assessment, and long-term competitive strategy formulation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 17665.38 Million |

|

Market Revenue in 2033 |

USD 24550.74 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |