Reports

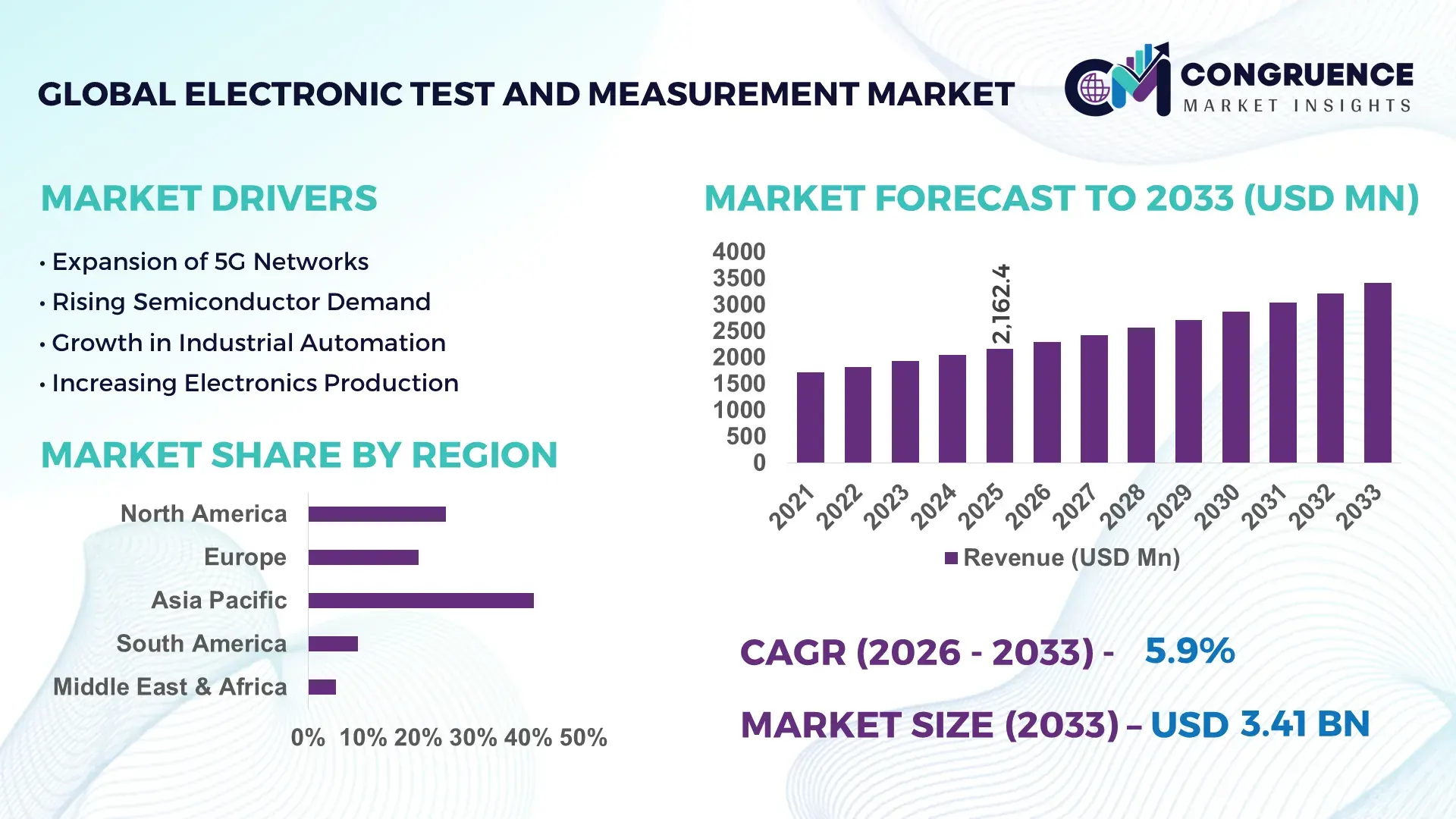

The Global Electronic Test and Measurement Market was valued at USD 11501.81 Million in 2025 and is anticipated to reach a value of USD 16672.41 Million by 2033 expanding at a CAGR of 4.75% between 2026 and 2033.

Rising deployment of 5G infrastructure, EV power electronics, semiconductor validation platforms, and AI-driven automated testing systems is accelerating demand for high-precision oscilloscopes, spectrum analyzers, signal generators, and modular test equipment across industrial and telecom applications. Between 2024 and 2026, semiconductor localization programs in the U.S., China, India, and the European Union intensified procurement of advanced testing platforms as geopolitical chip restrictions and supply chain diversification increased validation requirements for high-frequency and mixed-signal components by over 18%.

The United States continues to dominate the global electronic test and measurement market with approximately 34% share, supported by over USD 52 billion in semiconductor and electronics manufacturing investments, strong aerospace and defense procurement, and rapid adoption of automated RF testing technologies. More than 68% of large-scale telecom equipment manufacturers in the country integrated AI-assisted testing workflows by 2026, improving fault detection efficiency by nearly 27% compared to conventional manual inspection systems. In comparison, China leads in production-scale electronics testing capacity, particularly in consumer electronics and EV battery validation, while Japan maintains leadership in precision calibration systems and industrial automation testing accuracy.

Companies prioritizing automated, software-defined, and high-frequency testing ecosystems are positioned to secure stronger operational efficiency, faster product validation cycles, and long-term competitive resilience in the advanced electronics manufacturing landscape.

Market Size & Growth: USD 11501.81 Million in 2025 reaching USD 16672.41 Million by 2033, supported by rapid 5G rollout, EV electronics production, and semiconductor testing modernization.

Top Growth Drivers: 31% rise in EV electronics testing demand, 24% increase in RF validation requirements, and 19% expansion in automated semiconductor inspection adoption during 2024–2026.

Short-Term Forecast: By 2027, AI-enabled testing platforms are projected to reduce diagnostic downtime by 22% while improving manufacturing efficiency by nearly 18%.

Emerging Technologies: AI-driven analytics, software-defined instrumentation, and mmWave testing systems are increasing precision rates by over 25% across advanced electronics facilities.

Regional Leaders: North America exceeds USD 5.4 Billion through aerospace integration, Asia-Pacific surpasses USD 6.8 Billion with semiconductor expansion, and Europe crosses USD 3.7 Billion through industrial automation upgrades.

Consumer/End-User Trends: More than 61% of telecom and semiconductor manufacturers adopted automated testing workflows to accelerate validation cycles and improve production consistency.

Pilot/Case Example: In 2025, a major semiconductor fabrication project reduced chip validation time by 29% after deploying AI-powered automated testing infrastructure.

Competitive Landscape: The top five companies collectively control nearly 42% market share, driven by advanced RF testing portfolios, software integration, and industrial automation expertise.

Regulatory & ESG Impact: Energy-efficient testing platforms lowered operational power consumption by approximately 16% as manufacturers aligned with stricter industrial sustainability regulations.

Investment & Funding: Global investments exceeded USD 9 billion between 2024 and 2026, led by semiconductor expansion projects, strategic partnerships, and regional electronics manufacturing diversification.

Innovation & Future Outlook: Next-generation quantum testing tools, cloud-connected instrumentation, and AI-assisted predictive diagnostics are reshaping high-frequency electronic validation strategies.

Automotive electronics, telecommunications, and semiconductor manufacturing collectively account for more than 64% of total electronic test and measurement equipment utilization, driven by increasing complexity in EV architectures, 5G infrastructure, and advanced chip fabrication. AI-enabled predictive diagnostics and cloud-based remote calibration platforms improved testing throughput by nearly 21% in 2026, while modular software-defined instruments gained stronger adoption across multi-device production environments. Asia-Pacific remains the strongest demand center due to accelerated electronics manufacturing relocation and supply chain diversification, while North America continues expanding aerospace and defense testing investments. Growing emphasis on high-frequency validation, energy-efficient testing systems, and real-time analytics is expected to redefine competitive positioning across the advanced electronic measurement ecosystem.

Electronic test and measurement systems are becoming a strategic control layer for semiconductor manufacturing, EV electronics validation, aerospace diagnostics, and high-frequency telecom infrastructure, transforming the market into a critical investment battleground for industrial competitiveness. As device architectures become more compact and software-defined, manufacturers are accelerating adoption of automated RF analyzers, modular instrumentation, and AI-assisted predictive testing platforms to optimize validation cycles and reduce production failures. Between 2024 and 2026, growing semiconductor localization programs and export-control restrictions forced companies to redesign testing ecosystems closer to manufacturing hubs, increasing demand for high-speed validation equipment by nearly 26%.

AI-enabled automated testing platforms improve inspection efficiency by 32% while reducing operational costs by 21% compared to legacy manual calibration systems. Asia-Pacific leads in production volume through large-scale semiconductor and electronics manufacturing capacity, while North America leads in advanced testing innovation with nearly 67% adoption of AI-assisted validation technologies across aerospace and telecom applications. Over the next three years, advanced software-defined instrumentation is projected to reduce product verification time by 24%, strengthening throughput across high-volume electronics production lines. ESG-linked energy optimization has also become a competitive advantage, with low-power digital testing systems lowering facility-level energy consumption by approximately 14%.

In 2025, a leading EV battery manufacturer improved power module defect detection accuracy by 29% after integrating automated thermal and signal integrity testing systems into its production facilities. Companies are now shifting capital allocation toward cloud-connected instrumentation, localized calibration centers, and AI-driven diagnostics to secure supply chain resilience and faster product commercialization. Organizations capable of integrating intelligent, scalable, and energy-efficient testing ecosystems will define the next phase of competitive leadership across the advanced electronics value chain.

Rapid semiconductor expansion, EV electronics integration, and 5G infrastructure deployment are accelerating demand for high-precision electronic test and measurement systems across manufacturing ecosystems. Advanced RF testing requirements increased by 24% between 2024 and 2026 as telecom operators expanded mmWave deployments and automotive manufacturers integrated complex power electronics into EV platforms. Simultaneously, semiconductor validation workloads rose nearly 28% due to chiplet architectures and higher mixed-signal complexity. Global supply chain restructuring and regional semiconductor localization programs in the U.S., India, and Europe are forcing manufacturers to establish localized testing capacity and faster calibration cycles. In response, companies are accelerating capital investments, expanding automated testing facilities, and forming strategic partnerships focused on AI-enabled diagnostics and high-frequency validation systems.

Electronic test and measurement manufacturers are facing rising constraints from component dependency, calibration complexity, and escalating production costs tied to advanced semiconductor nodes and precision instrumentation. Prices for high-frequency signal processing components increased by nearly 17% during recent semiconductor shortages, while lead times for specialized testing modules extended beyond 22 weeks in several industrial regions. Dependence on concentrated chip fabrication ecosystems in East Asia continues exposing testing equipment suppliers to geopolitical trade disruptions and logistics instability. These pressures are directly increasing procurement costs, delaying industrial deployments, and constraining scalability for mid-sized manufacturers. To reduce operational exposure, companies are diversifying supplier networks, securing long-term semiconductor agreements, and accelerating development of software-defined testing architectures requiring lower hardware dependency and improved lifecycle flexibility.

AI-driven testing automation, edge-device validation, and localized electronics manufacturing are creating high-impact expansion opportunities across the electronic test and measurement ecosystem. Automated predictive diagnostics improved fault detection efficiency by nearly 31% in advanced semiconductor facilities, while software-defined instrumentation reduced manual configuration time by approximately 26%. Emerging manufacturing hubs in India, Vietnam, and Mexico are rapidly increasing investment in electronics assembly and validation infrastructure as global supply chains continue diversifying beyond traditional production centers. A major future shift involves cloud-connected remote calibration ecosystems, enabling real-time performance monitoring and lower operational downtime across distributed facilities. Companies are responding by increasing R&D spending, building integrated testing ecosystems, and expanding regional calibration centers to secure long-term dominance in high-growth industrial and telecom applications.

Scaling advanced electronic testing ecosystems is becoming increasingly difficult due to infrastructure intensity, interoperability limitations, and rapidly evolving validation standards across semiconductor and telecom industries. Testing complexity for high-frequency and mixed-signal devices increased by over 33% as manufacturers adopted smaller chip geometries and integrated AI-enabled electronics into industrial systems. At the same time, nearly 21% of manufacturers report delays in automated testing deployment due to workforce shortages in calibration engineering and software integration. Rising energy consumption from large-scale validation facilities is also creating operational pressure as industrial sustainability regulations tighten globally. To remain competitive, companies must accelerate workforce training, invest in interoperable software-defined architectures, and strengthen partnerships across semiconductor, telecom, and industrial automation ecosystems to ensure scalable long-term deployment efficiency.

AI-driven automation cuts testing downtime by 22% across semiconductor facilities. Electronics manufacturers are rapidly deploying AI-assisted fault detection and predictive calibration systems to optimize validation workflows and reduce manual inspection dependency. More than 61% of large semiconductor production facilities integrated automated analytics platforms during 2025–2026, while real-time defect identification improved inspection accuracy by nearly 28%. Companies are restructuring testing operations around centralized software platforms to accelerate throughput and stabilize production quality amid rising labor shortages in precision engineering environments.

Software-defined instrumentation adoption rises 27% as manufacturers optimize multi-device validation. Enterprises are replacing fixed-function hardware systems with modular software-controlled testing architectures capable of handling multiple communication standards and signal frequencies simultaneously. Deployment flexibility improved by approximately 31%, while calibration cycles shortened by 18% across telecom and industrial automation facilities. The shift is redefining procurement strategies, with companies prioritizing scalable ecosystems instead of isolated instruments to reduce lifecycle costs and improve operational adaptability during evolving product transitions.

Asia-Pacific electronics testing capacity expands 24% as supply chains continue shifting regionally. Semiconductor packaging and electronics assembly relocation into India, Vietnam, and Southeast Asia is forcing rapid deployment of localized calibration centers and high-frequency validation infrastructure. China maintains manufacturing scale dominance, while Japan and South Korea continue leading in precision testing innovation and automation integration. Global manufacturers are expanding regional partnerships and localized support networks to reduce logistics delays and strengthen production continuity amid geopolitical trade restructuring.

Cloud-connected remote calibration systems improve operational efficiency by 19% in distributed facilities. Industrial manufacturers and telecom operators are increasingly adopting remote diagnostic and calibration platforms to manage geographically dispersed production environments. More than 46% of advanced manufacturing sites integrated cloud-based monitoring tools by 2026, reducing unplanned maintenance intervals by nearly 17%. A non-obvious shift is emerging as testing providers transition from equipment-centric sales models toward recurring software and service ecosystems, reshaping long-term customer retention strategies and operational profitability.

The electronic test and measurement market is segmented by type, application, and end-user, with demand increasingly concentrated around high-frequency electronics validation and automated industrial testing. Oscilloscopes and semiconductor testing collectively account for over 48% of deployment demand due to rising complexity in EV electronics, RF communication systems, and chip validation processes. Telecommunications and electronics manufacturing remain dominant end-user segments, while automotive testing adoption increased by nearly 21% following accelerated EV production expansion. Demand is steadily shifting toward AI-enabled, software-defined, and modular testing platforms as companies prioritize faster calibration, lower downtime, and scalable multi-device validation capabilities across geographically diversified manufacturing ecosystems.

Oscilloscopes lead the market with nearly 36% share due to strong demand in semiconductor, telecom, and EV electronics testing. Spectrum analyzers are the fastest-growing segment, expanding by around 23% as 5G and RF validation requirements increase. Compared with multimeters, oscilloscopes deliver stronger real-time signal analysis and higher integration flexibility for advanced electronics environments. Signal generators and multimeters together account for nearly 41% share, mainly supporting industrial maintenance, calibration, and automation applications. Companies are shifting investments toward AI-enabled oscilloscopes, portable analyzers, and software-defined testing systems to improve operational flexibility and high-frequency performance. Demand is increasingly moving toward integrated multi-function testing platforms capable of reducing validation time and improving production efficiency across complex electronics manufacturing ecosystems.

“According to a 2025 report by International Electrotechnical Commission (IEC), advanced oscilloscope platforms were adopted by over 69% of semiconductor and telecom equipment manufacturers, resulting in nearly 26% improvement in high-frequency signal validation efficiency, reinforcing their growing strategic importance.”

Semiconductor testing dominates the market with approximately 33% share due to increasing chip complexity and advanced packaging validation requirements. Wireless communication is the fastest-growing application, rising by nearly 25% as 5G infrastructure and satellite communication deployments accelerate globally. Compared with traditional product testing, wireless communication testing requires higher-frequency bandwidth analysis and faster RF diagnostics, redefining equipment procurement priorities. Network testing, industrial automation, and product testing collectively account for over 52% of total operational deployments supporting connected devices and factory automation. Companies are expanding AI-enabled validation systems and cloud-connected calibration tools to improve throughput and reduce downtime. Demand is shifting toward automated high-frequency testing environments capable of supporting faster production cycles and geographically diversified electronics manufacturing operations.

“According to a 2025 report by International Telecommunication Union (ITU), wireless communication testing systems were deployed across more than 4,800 telecom infrastructure projects, improving network signal optimization efficiency by 24%, highlighting its rapid operational adoption.”

Electronics manufacturing leads the market with nearly 38% share due to continuous demand for semiconductor, consumer electronics, and industrial device validation. Automotive is the fastest-growing end-user segment, expanding by approximately 27% as EV production and battery management systems increase testing requirements. Telecommunications maintains strong demand for network reliability and RF infrastructure validation, while aerospace and manufacturing together contribute nearly 49% of specialized testing deployments. Companies are increasingly targeting automotive and telecom sectors through customized software-defined testing systems, automated diagnostics, and regional calibration partnerships. Buying behavior is shifting toward scalable and energy-efficient testing ecosystems capable of supporting high-frequency electronics and multi-device validation across distributed production environments.

“According to a 2025 report by International Organization for Standardization (ISO), adoption among automotive electronics manufacturers increased by 29%, with over 3,200 production facilities implementing advanced automated testing systems, leading to nearly 23% improvement in defect detection efficiency, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

Asia-Pacific leads in production scale and electronics manufacturing demand, supported by semiconductor expansion across China, Japan, South Korea, and India, where over 58% of global electronics assembly capacity is concentrated. North America is accelerating through AI-driven testing innovation, aerospace electronics validation, and telecom infrastructure modernization, with automated testing adoption exceeding 67% across advanced manufacturing facilities. Europe maintains nearly 24% market share through industrial automation and compliance-focused testing deployment. Supply chain diversification and semiconductor localization programs are reshaping regional investment priorities, forcing companies to expand localized calibration centers, automation partnerships, and high-frequency validation infrastructure across strategically important manufacturing hubs.

North America holds nearly 29% of the electronic test and measurement market due to strong concentration of semiconductor manufacturing, aerospace electronics, telecom infrastructure, and defense-related testing requirements. Demand is accelerating for AI-enabled RF analyzers, software-defined instrumentation, and automated validation systems as manufacturers prioritize faster product verification and lower operational downtime. Semiconductor localization policies and stricter supply chain resilience strategies are forcing companies to expand regional testing capabilities and reduce overseas dependency. More than 67% of advanced electronics facilities integrated automated diagnostics platforms by 2026, improving fault detection efficiency by approximately 27%. Enterprises increasingly prefer scalable cloud-connected testing ecosystems capable of supporting multi-device validation and predictive maintenance. Companies continue prioritizing this region because it combines innovation leadership, high-value industrial demand, and strong infrastructure for advanced electronics commercialization.

Europe accounts for approximately 24% of the electronic test and measurement market, driven by industrial automation, automotive electronics, aerospace systems, and energy-efficient manufacturing initiatives across Germany, France, and the Nordic region. Strict environmental compliance frameworks and energy-efficiency regulations are accelerating adoption of low-power digital testing systems and automated calibration technologies. More than 52% of industrial manufacturers upgraded testing infrastructure between 2024 and 2026 to align with operational sustainability targets and precision manufacturing standards. Enterprises are increasingly adopting software-defined instrumentation to improve efficiency while reducing calibration-related energy consumption by nearly 16%. Companies operating in this region prioritize compliance-focused innovation, precision reliability, and long-term lifecycle performance. Europe continues forcing manufacturers to optimize testing ecosystems around regulatory adaptation, operational efficiency, and advanced industrial quality assurance requirements.

Asia-Pacific dominates the electronic test and measurement market with nearly 41% demand concentration due to large-scale semiconductor production, electronics assembly, telecom infrastructure deployment, and EV manufacturing growth across China, Japan, South Korea, and India. Regional manufacturing expansion and supply chain diversification are accelerating deployment of localized calibration facilities and high-frequency testing infrastructure. More than 58% of global electronics assembly operations are concentrated in the region, while semiconductor testing deployments increased by approximately 26% between 2024 and 2026. Enterprises are rapidly adopting automated testing systems to optimize throughput, reduce operational delays, and support mass-scale device production. Companies increasingly prioritize this region because it combines manufacturing scale, cost efficiency, and accelerating domestic electronics demand, making it critical for production expansion and long-term industrial competitiveness.

South America represents nearly 7% of the electronic test and measurement market, with Brazil and Argentina leading regional demand through automotive electronics, industrial automation, and telecom infrastructure modernization projects. Manufacturing digitalization and expansion of connected industrial systems are increasing deployment of automated testing equipment across production facilities. However, import dependency and currency volatility continue constraining rapid infrastructure scaling and advanced instrumentation accessibility. More than 34% of industrial manufacturers increased investment in digital testing systems between 2024 and 2026 to improve operational efficiency and reduce maintenance downtime. Enterprises remain highly price-sensitive, prioritizing modular and scalable testing platforms capable of balancing cost with operational flexibility. Companies view the region as a selective growth opportunity where localized partnerships and affordable automation solutions are essential for long-term market penetration.

Middle East & Africa account for approximately 6% of the electronic test and measurement market, supported by growing infrastructure modernization, telecom expansion, industrial automation, and energy-sector digitization across the UAE, Saudi Arabia, and South Africa. Oil and gas facilities, smart city initiatives, and renewable energy projects are accelerating deployment of high-precision monitoring and calibration systems. More than 29% of industrial infrastructure projects integrated automated testing technologies during 2025–2026 to improve equipment reliability and operational continuity. Governments and enterprises are increasing partnerships with global testing equipment providers to strengthen local technical capabilities and reduce maintenance inefficiencies. Enterprises prioritize durable, scalable, and remotely manageable testing systems capable of operating across complex industrial environments. Companies increasingly view this region as a strategic infrastructure-driven expansion market with rising long-term industrial modernization potential.

United States – Holds approximately 34% share of the Electronic Test and Measurement market due to strong semiconductor manufacturing, aerospace electronics demand, and rapid adoption of AI-enabled automated testing systems.

China – Accounts for nearly 27% share of the Electronic Test and Measurement market through large-scale electronics production capacity, telecom infrastructure expansion, and dominant semiconductor assembly operations.

The electronic test and measurement market is dominated by global technology leaders including Keysight Technologies, Rohde & Schwarz, Tektronix, Anritsu, and National Instruments competing against regional automation specialists and cost-focused instrumentation providers. The top five players collectively control nearly 42% market share through advanced RF testing, semiconductor validation, and software-defined instrumentation portfolios. Competition is increasingly centered on automation capability, high-frequency precision, cloud integration, and deployment speed, with AI-enabled testing systems improving operational efficiency by over 28% while reducing calibration time by approximately 19%. Companies are aggressively expanding regional calibration centers, strengthening semiconductor partnerships, and accelerating software-based diagnostics to secure recurring enterprise demand. Market dynamics are shifting from standalone hardware competition toward integrated testing ecosystems combining analytics, remote monitoring, and predictive maintenance capabilities. High R&D intensity, precision engineering requirements, and semiconductor dependency remain major entry barriers. Winning increasingly depends on scalable automation, ecosystem integration, and localized technical support infrastructure.

Keysight Technologies

Rohde & Schwarz

Tektronix

Anritsu Corporation

National Instruments

Advantest Corporation

Yokogawa Electric Corporation

Teledyne LeCroy

Viavi Solutions

Fortive Corporation

Chroma ATE Inc.

EXFO Inc.

GW Instek

B&K Precision

AI-enabled automated testing platforms are reshaping electronic validation workflows by reducing manual calibration time by nearly 28% and improving defect detection accuracy by approximately 31% across semiconductor and telecom environments. More than 63% of advanced electronics manufacturers integrated predictive diagnostics and real-time analytics into testing operations by 2026 to optimize throughput and minimize production delays. Compared with legacy manual inspection systems, AI-assisted testing improves operational efficiency by 34% while lowering maintenance costs by 22%, creating a strong competitive advantage for semiconductor fabs, aerospace electronics suppliers, and EV component manufacturers operating under tighter production timelines.

Software-defined instrumentation and cloud-connected calibration systems are accelerating deployment flexibility across multi-device production ecosystems. Automated remote calibration platforms improved testing uptime by approximately 19%, while modular RF testing systems reduced configuration complexity by nearly 24% in high-frequency telecom and industrial automation applications. Companies are increasingly integrating cloud analytics, edge-device monitoring, and centralized diagnostics to support geographically distributed manufacturing operations. Organizations capable of deploying scalable software-centric testing ecosystems are securing faster product validation cycles and stronger operational resilience amid continuing supply chain restructuring.

Disruptive technologies including quantum validation systems, mmWave signal analysis, and digital twin-enabled simulation platforms are redefining high-frequency testing performance between 2026 and 2028. Adoption of advanced mmWave testing tools increased by over 21% as 5G infrastructure, satellite communication, and autonomous electronics systems expanded globally. Digital twin-based testing environments are reducing prototype validation cycles by nearly 18%, allowing manufacturers to optimize product development before physical deployment. Technology leaders are aggressively investing in AI-driven RF diagnostics, interoperable testing ecosystems, and ultra-high-speed automation platforms to capture leadership in next-generation electronics validation markets.

July 2024 – Anritsu Corporation partnered with LITEON Technology to strengthen 5G Open RAN performance testing using MT8000A and MX773000PC platforms, reducing testing time and operational costs while accelerating O-RU verification efficiency across Sub-6 GHz infrastructure deployments. The collaboration strengthened scalable multi-vendor telecom validation capabilities. [Open RAN Validation] Source: Anritsu

November 2024 – Nokia secured deployment across more than 3,000 Open RAN sites in Germany using energy-efficient ReefShark-based infrastructure, expanding commercial-scale O-RAN integration and strengthening high-capacity network testing requirements for telecom interoperability and multi-vendor validation systems. The rollout accelerated large-scale RF testing demand in Europe. [Telecom Scale-Up] Source: Reddit Telecom Update

January 2026 – Keysight Technologies intensified focus on AI system validation and behavioral drift testing for safety-critical applications, addressing long-term reliability issues in regulated AI environments. The initiative highlighted growing enterprise demand for continuous validation systems as AI deployment complexity and operational monitoring requirements accelerated globally. [AI Reliability Shift] Source: The Component Club

June 2024 – Samsung and MediaTek completed advanced 5G RedCap testing over virtualized RAN infrastructure, demonstrating energy-saving features capable of extending IoT device sleep cycles up to 3 hours. The deployment improved battery efficiency and reinforced growing demand for power-optimized wireless testing ecosystems supporting large-scale IoT connectivity. [Energy-Efficient Testing] Source: TechPop Discussion

The Electronic Test and Measurement Market Report delivers detailed coverage across core product categories including oscilloscopes, signal generators, spectrum analyzers, and multimeters, alongside strategic application areas such as semiconductor testing, wireless communication, network testing, industrial automation, and product validation. The report evaluates demand patterns across electronics, telecommunications, automotive, aerospace, and manufacturing sectors while analyzing regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Advanced technologies including AI-driven diagnostics, software-defined instrumentation, cloud-connected calibration systems, and mmWave validation platforms are extensively assessed within the 2026–2033 outlook framework.

The report provides deep analytical benchmarking across more than 15 strategic market indicators, including deployment intensity, automation adoption, RF testing integration, and high-frequency electronics validation trends. Over 63% of advanced semiconductor facilities adopting AI-assisted testing ecosystems and nearly 21% growth in automated wireless communication validation deployments are evaluated to identify operational transformation patterns and competitive shifts.

The study supports strategic decision-making by identifying demand concentration, emerging technology priorities, regional expansion opportunities, and competitive positioning strategies. It delivers actionable insights for manufacturers, investors, telecom operators, and industrial automation providers seeking to optimize capital allocation, strengthen supply chain resilience, and capture long-term advantages in next-generation electronics testing ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 11501.81 Million |

|

Market Revenue in 2033 |

USD 16672.41 Million |

|

CAGR (2026 - 2033) |

4.75% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Keysight Technologies, Rohde & Schwarz, Tektronix, Anritsu Corporation, National Instruments, Advantest Corporation, Yokogawa Electric Corporation, Teledyne LeCroy, Viavi Solutions, Fortive Corporation, Chroma ATE Inc., EXFO Inc., GW Instek, B&K Precision |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |