Reports

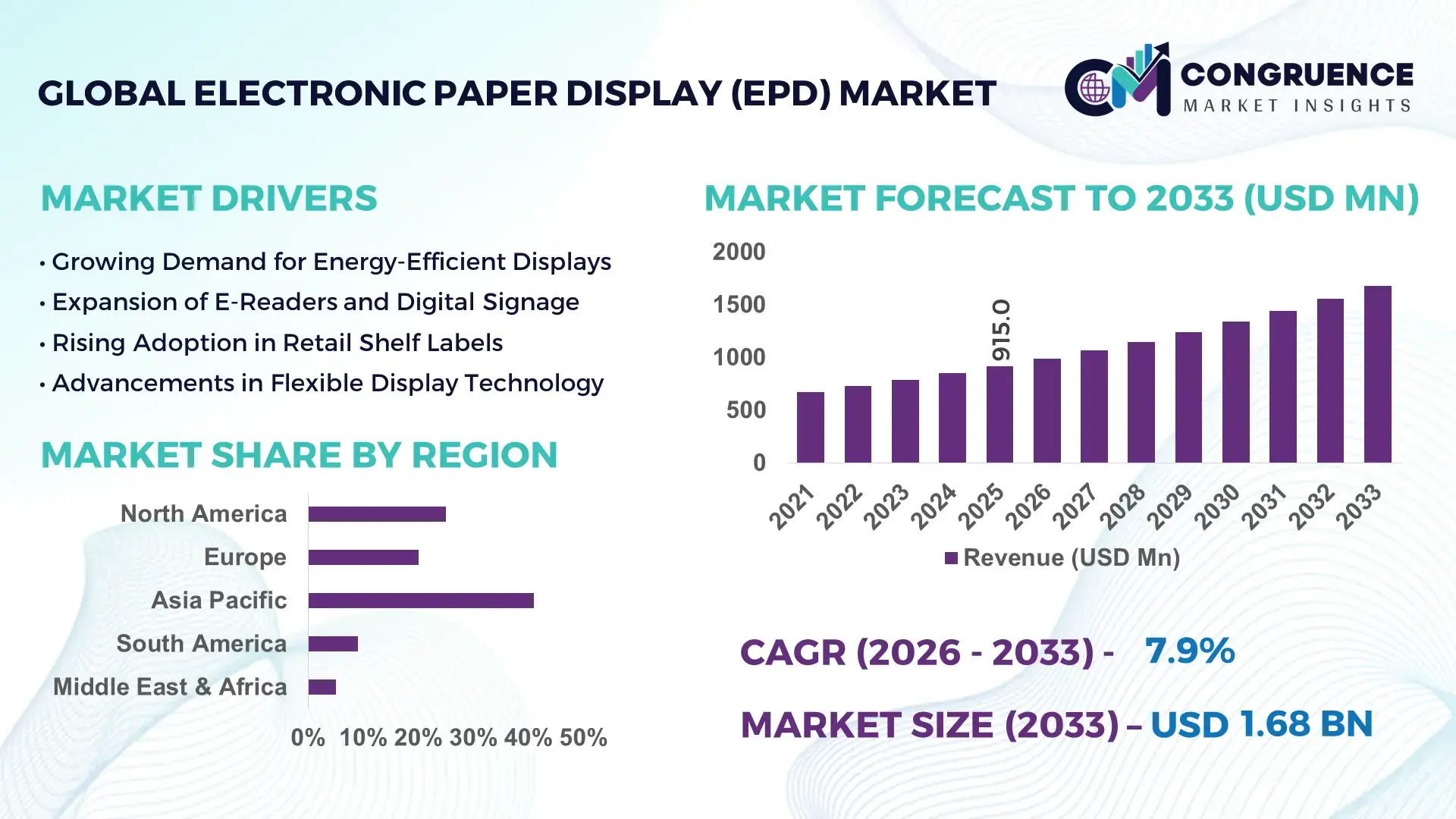

The Global Electronic Paper Display (EPD) Market was valued at USD 914.97 Million in 2025 and is anticipated to reach a value of USD 1681.05 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. The market growth is primarily driven by the rising deployment of low-power, high-visibility digital signage and e-readers across retail, education, logistics, and smart infrastructure applications.

China continues to lead global Electronic Paper Display (EPD) production with an integrated manufacturing ecosystem supporting advanced electrophoretic display modules and controller ICs. The country accounts for over 60% of global e-paper display panel production capacity, supported by large-scale fabrication facilities in Guangdong and Jiangsu provinces. In 2025, China’s domestic deployment of electronic shelf labels (ESLs) exceeded 120 million units across major retail chains, reflecting strong commercial adoption. Government-backed investments in flexible display R&D surpassed USD 450 million between 2023 and 2025, accelerating innovation in color e-paper, ultra-thin substrates, and IoT-integrated smart signage solutions.

• Market Size & Growth: Valued at USD 914.97 Million in 2025, projected to reach USD 1681.05 Million by 2033 at a CAGR of 7.9%, driven by accelerated adoption of energy-efficient digital displays and large-scale retail automation.

• Top Growth Drivers: Retail ESL adoption rising by 28%, logistics tracking digitization increasing by 22%, and e-reader device penetration expanding by 18%.

• Short-Term Forecast: By 2028, large-format EPD deployment is expected to reduce display energy consumption by 35% and lower maintenance costs by 20% across retail networks.

• Emerging Technologies: Advanced color e-paper panels, flexible and foldable EPD substrates, and IoT-enabled smart signage platforms enhancing real-time connectivity.

• Regional Leaders: Asia-Pacific projected to reach USD 720 Million by 2033 with strong retail automation; North America expected at USD 480 Million driven by smart warehousing; Europe estimated at USD 350 Million supported by sustainable digital signage initiatives.

• Consumer/End-User Trends: Major end-users include organized retail, education, healthcare, and transportation sectors, with growing preference for ultra-low power displays and glare-free readability in high-traffic environments.

• Pilot or Case Example: In 2024, a multinational retail chain implemented smart ESL systems across 1,000 stores, improving pricing accuracy by 30% and reducing manual update time by 40%.

• Competitive Landscape: The market leader holds approximately 38% share, followed by prominent players such as E Ink Holdings, BOE Technology Group, LG Display, and Samsung Display.

• Regulatory & ESG Impact: Energy-efficiency standards and carbon reduction mandates are accelerating adoption of low-power display technologies, with ESG-driven procurement policies influencing public and private sector investments.

• Investment & Funding Patterns: Over USD 600 Million invested globally between 2023 and 2025 in flexible display manufacturing expansion and advanced color EPD development.

• Innovation & Future Outlook: Integration of EPD with AI-based inventory systems, expansion of battery-free displays, and development of high-refresh color panels are shaping next-generation smart display ecosystems.

The Electronic Paper Display (EPD) market is increasingly diversified across retail (approximately 45% of demand), consumer electronics (around 30%), and industrial/logistics applications (nearly 15%), with healthcare and education contributing the remainder. Recent advancements in high-resolution color electrophoretic displays and ultra-thin flexible substrates are enhancing product versatility. Regulatory emphasis on energy-efficient digital infrastructure and reduced carbon footprints is reinforcing enterprise adoption. Asia-Pacific dominates consumption due to large retail networks and manufacturing ecosystems, while North America and Europe are witnessing accelerated uptake of sustainable digital signage. Future growth is expected to be supported by smart city initiatives, IoT integration, and next-generation low-power communication protocols.

The Electronic Paper Display (EPD) Market holds strategic relevance as enterprises accelerate digital transformation while prioritizing energy efficiency, operational agility, and ESG compliance. EPD technology has emerged as a mission-critical component in retail automation, smart logistics, healthcare labeling, and connected infrastructure due to its ultra-low power consumption and sunlight-readable display capabilities. Advanced color e-paper delivers up to 40% improvement in visual contrast and refresh optimization compared to traditional monochrome e-paper modules, enabling broader commercial signage applications.

Asia-Pacific dominates in volume owing to high-scale manufacturing capacity and retail digitization, while North America leads in adoption with nearly 55% of large retail enterprises deploying electronic shelf labels and smart display systems. The integration of AI-enabled inventory analytics with connected EPD networks is strengthening strategic value by improving pricing accuracy, stock visibility, and dynamic content management. By 2028, AI-powered smart display management platforms are expected to reduce manual update cycles by 30% and cut operational errors by 25% across multi-location retail chains.

Compliance and sustainability objectives are further shaping the market pathway. Firms are committing to measurable ESG improvements such as 35% energy reduction in in-store digital infrastructure by 2030 through battery-efficient and recyclable display materials. In 2024, a major European retail group achieved a 32% reduction in paper-based labeling waste through large-scale EPD deployment integrated with automated pricing systems. With continued advancements in flexible substrates, IoT interoperability, and AI-driven content optimization, the Electronic Paper Display (EPD) Market is positioning itself as a pillar of operational resilience, regulatory compliance, and sustainable long-term growth across digitally connected industries.

Retail automation remains a primary growth driver for the Electronic Paper Display (EPD) Market. Over 70% of organized retail chains globally are implementing digital shelf labeling systems to enhance pricing accuracy and inventory synchronization. Electronic shelf labels reduce manual labor requirements by approximately 25% while improving pricing accuracy rates above 98%. High-traffic supermarkets deploying connected EPD networks report up to 40% faster price update cycles compared to traditional paper labels. Additionally, the expansion of omnichannel retailing requires real-time stock visibility, which EPD-enabled systems support through cloud-integrated communication platforms. As large-format stores continue digital upgrades, demand for durable, low-power, glare-free displays is increasing across hypermarkets, convenience stores, and specialty retail outlets.

Despite long-term operational savings, the Electronic Paper Display (EPD) Market faces restraint from substantial upfront deployment costs. Large retail networks may require installation of tens of thousands of display units, integrated wireless gateways, and centralized management software. Infrastructure investments can exceed traditional labeling systems by 3–4 times during initial implementation phases. Additionally, integration with legacy enterprise resource planning systems can extend deployment timelines by 6–12 months. Small and medium-sized retailers often delay adoption due to capital expenditure constraints and limited technical expertise. Durability requirements in industrial environments also increase material and encapsulation costs, further affecting short-term affordability for budget-sensitive enterprises.

Smart city initiatives present significant opportunities for the Electronic Paper Display (EPD) Market. Municipalities are deploying low-power public information boards, transit timetables, and environmental monitoring displays to reduce electricity consumption by up to 50% compared to LCD alternatives. IoT-enabled EPD signage supports remote content updates and real-time alerts, enhancing urban communication networks. Flexible and weather-resistant e-paper modules are increasingly integrated into bus stops, parking systems, and utility meters. The rise of battery-free and solar-assisted EPD installations is expanding deployment in off-grid locations. As governments allocate funding toward digital infrastructure modernization, scalable and energy-efficient display technologies are gaining procurement preference.

The Electronic Paper Display (EPD) Market faces ongoing challenges related to supply chain disruptions and specialized material dependencies. Electrophoretic microcapsule materials, thin-film transistor backplanes, and controller integrated circuits require precision manufacturing processes concentrated in limited geographies. Global semiconductor shortages have previously extended component lead times by up to 20 weeks, affecting production schedules. Fluctuations in raw material prices, particularly conductive polymers and specialty substrates, increase manufacturing cost variability. Furthermore, quality control standards for durability and color consistency require rigorous testing, raising compliance expenses. These structural constraints can slow expansion plans and impact timely fulfillment of large enterprise deployment contracts.

• Rapid Expansion of Color E-Paper Deployment Across Retail Networks:

Color Electronic Paper Display (EPD) modules are witnessing accelerated adoption, particularly in organized retail and large-format supermarkets. In 2025, more than 35% of newly installed electronic shelf labels featured advanced tri-color or full-color capability, compared to less than 20% three years earlier. Retailers report up to 25% higher promotional engagement when using color-enabled displays versus monochrome alternatives. Enhanced pigment dispersion and waveform optimization technologies now deliver refresh improvements of nearly 30%, enabling dynamic pricing updates without compromising battery life. This shift is strengthening demand for scalable color EPD infrastructure across multi-location retail chains.

• Integration of IoT-Connected Smart Display Ecosystems:

The integration of IoT-enabled Electronic Paper Display (EPD) systems into centralized enterprise platforms is transforming operational efficiency. Over 60% of tier-1 retail enterprises now deploy cloud-connected EPD networks capable of real-time synchronization across more than 500 store locations. Wireless communication protocols have improved update latency by 40%, while automated inventory triggers reduce manual price adjustments by 35%. Logistics operators utilizing connected EPD tags report up to 20% improvement in warehouse picking accuracy. The convergence of low-power displays with AI-based analytics is driving measurable improvements in asset visibility and data-driven decision-making.

• Accelerated Adoption of Flexible and Ultra-Thin EPD Substrates:

Flexible Electronic Paper Display (EPD) panels are increasingly deployed in transportation signage, healthcare labeling, and wearable devices. Nearly 28% of new pilot installations in 2024 incorporated bendable substrates under 0.5 mm thickness, compared to 12% in 2022. These ultra-thin displays demonstrate up to 15% weight reduction and 18% improved durability under mechanical stress testing. Public transit authorities adopting flexible e-paper route displays report maintenance cycle reductions of approximately 22% due to enhanced resistance to vibration and temperature fluctuations. This structural innovation is expanding the addressable market beyond conventional rigid display applications.

• Energy Optimization and ESG-Driven Procurement Policies:

Sustainability-focused procurement is significantly influencing Electronic Paper Display (EPD) adoption across public and private sectors. Enterprises transitioning from LCD signage to EPD solutions report energy consumption reductions of up to 50% under static display conditions. Approximately 48% of European retail groups have committed to reducing in-store digital energy usage by at least 30% by 2030 through deployment of low-power display technologies. Battery lifecycles in modern EPD labels now extend beyond 5 years, representing a 40% improvement compared to earlier-generation devices. ESG-aligned capital allocation strategies are therefore reinforcing long-term investment in energy-efficient digital display ecosystems.

The Electronic Paper Display (EPD) Market segmentation reflects diversified demand across product types, application environments, and end-user industries. Product differentiation between monochrome, color, and flexible displays shapes deployment strategies depending on readability, durability, and energy-efficiency requirements. Application segmentation is dominated by retail electronic shelf labels, followed by e-readers, industrial signage, transportation displays, and smart cards. Retail continues to represent the most structured and scalable deployment model due to standardized pricing systems and centralized content management. End-user segmentation highlights organized retail, consumer electronics manufacturers, logistics operators, healthcare providers, and public infrastructure authorities. Adoption intensity varies by operational complexity, with enterprises managing over 500 locations demonstrating higher integration of IoT-enabled EPD networks. Regional segmentation further reflects Asia-Pacific’s strong manufacturing base, North America’s enterprise-scale adoption, and Europe’s sustainability-driven procurement policies.

Monochrome Electronic Paper Display (EPD) panels currently account for approximately 52% of total installations, primarily due to cost efficiency, extended battery life exceeding 5 years, and high contrast readability in indoor retail environments. These displays remain the preferred solution for large-scale electronic shelf labeling systems and warehouse tags where static content dominates. In comparison, color EPD modules hold nearly 33% adoption, driven by promotional labeling and marketing-oriented applications. However, flexible and advanced color EPD types represent the fastest-growing category, expanding at an estimated CAGR of 11.2%, as retailers and transportation authorities seek visually dynamic yet energy-efficient signage. Flexible EPD substrates, including ultra-thin panels under 0.5 mm thickness, are gaining traction in transportation and healthcare labeling due to their durability and lightweight construction. Other specialized types, such as segmented and large-format EPD panels, collectively contribute about 15% of installations, primarily in public information boards and industrial monitoring systems.

Retail electronic shelf labeling (ESL) remains the leading application, representing approximately 48% of total Electronic Paper Display (EPD) deployments. Retailers operating more than 1,000 outlets prioritize EPD integration to ensure pricing accuracy exceeding 98% and reduce manual labeling errors by nearly 30%. E-readers account for around 27% of application usage, driven by demand for glare-free, paper-like readability and low energy consumption. However, transportation and smart city signage applications are expanding at the fastest pace, with an estimated CAGR of 10.6%, supported by infrastructure modernization initiatives and sustainability mandates. Industrial and logistics applications collectively hold close to 15% of deployments, where EPD asset tags improve warehouse picking accuracy by up to 20%. Healthcare labeling and smart ID cards form the remaining 10%, particularly in temperature-sensitive environments requiring reliable low-power displays.

Organized retail is the leading end-user segment, accounting for approximately 46% of Electronic Paper Display (EPD) adoption. Large retail chains leverage centralized pricing systems integrated with cloud-based EPD networks to streamline inventory management and promotional updates. Consumer electronics manufacturers follow with around 24% usage, primarily through e-reader and portable device production. However, transportation and public infrastructure agencies represent the fastest-growing end-user group, expanding at an estimated CAGR of 10.9%, driven by digital signage modernization and energy-efficiency mandates. Logistics and warehousing companies contribute roughly 18% of deployments, particularly for smart tagging and real-time inventory visibility. Healthcare providers and educational institutions collectively account for nearly 12%, adopting EPD labels for patient identification, pharmaceutical tracking, and campus communication systems. Adoption rates among tier-1 logistics operators exceed 50% in automated warehouses where digital tagging enhances operational transparency.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Asia-Pacific’s leadership is supported by large-scale production capacity exceeding 65% of global Electronic Paper Display (EPD) panel output, with over 150 million ESL units deployed across organized retail networks in China, Japan, and South Korea. North America holds approximately 29% of total installations, driven by enterprise retail chains operating more than 20,000 smart-enabled stores. Europe represents nearly 21% share, reflecting sustainability-focused procurement policies and strict energy-efficiency regulations. South America and the Middle East & Africa collectively contribute 9%, with adoption concentrated in urban retail, logistics hubs, and infrastructure modernization projects. Across regions, more than 70% of tier-1 retailers have initiated partial or full EPD integration, while public transportation deployments increased by 18% in 2025 compared to the previous year, demonstrating accelerating cross-sector adoption.

How Is Large-Scale Retail Digitization Reshaping Smart Display Infrastructure?

North America accounts for approximately 29% of the global Electronic Paper Display (EPD) Market, supported by advanced retail automation, logistics optimization, and healthcare digitalization initiatives. Over 55% of organized retail chains across the United States and Canada have implemented electronic shelf labeling systems, with enterprise networks exceeding 1,000 outlets leading deployment. Healthcare and financial service institutions show higher enterprise adoption, particularly for patient labeling and secure digital signage. Regulatory focus on energy-efficient commercial infrastructure has encouraged replacement of traditional LCD signage, with energy savings reaching up to 50% in static display environments. Technological integration with AI-powered inventory systems has reduced manual pricing interventions by nearly 30%. A major regional retailer expanded EPD deployment across 1,200 stores in 2024, reducing labeling errors by 28% and improving stock visibility accuracy beyond 97%, reinforcing regional digital transformation trends.

Can Sustainability Mandates Accelerate Low-Power Display Adoption?

Europe represents nearly 21% of the Electronic Paper Display (EPD) Market, with Germany, the United Kingdom, and France accounting for over 60% of regional installations. Strong environmental directives targeting 30% reductions in commercial energy usage by 2030 are influencing procurement strategies. Retailers report up to 35% decline in paper-based labeling waste following EPD integration. Adoption of color EPD modules has increased by 22% in the past two years due to promotional labeling requirements. Regulatory pressure emphasizing transparency and sustainable digital infrastructure is driving structured investment in recyclable display components. A leading European supermarket consortium deployed more than 80 million electronic shelf labels across 7,500 stores, achieving pricing synchronization rates above 98%. Consumer behavior reflects high sensitivity to sustainability compliance, accelerating demand for low-energy, glare-free digital display ecosystems across retail and public infrastructure.

How Is Manufacturing Scale Driving Smart Display Penetration?

Asia-Pacific leads global volume with 41% market share, supported by dominant production facilities in China, Japan, and South Korea. The region manufactures over 65% of global EPD panels and exports to more than 70 countries. China alone operates fabrication lines capable of producing over 100 million display modules annually. Japan’s transportation sector has integrated more than 12,000 EPD timetable systems, reducing electricity consumption by 45% compared to legacy signage. India is witnessing rapid adoption across organized retail, with ESL penetration increasing by 26% in metropolitan centers. Innovation hubs in Shenzhen and Tokyo are advancing flexible substrates and color waveform technologies, improving refresh rates by 30%. Regional consumer behavior is influenced by strong e-commerce expansion and mobile-first digital ecosystems, driving high-volume deployment across logistics and smart retail platforms.

What Role Does Retail Modernization Play in Digital Display Adoption?

South America contributes approximately 5% of the global Electronic Paper Display (EPD) Market, with Brazil and Argentina accounting for nearly 70% of regional demand. Retail modernization initiatives across urban centers have increased ESL deployment by 18% between 2023 and 2025. Energy infrastructure constraints are encouraging businesses to adopt low-power display alternatives capable of reducing electricity consumption by up to 40% in signage applications. Government incentives promoting digital transformation in commercial sectors are supporting smart store pilots across major metropolitan areas. Logistics operators in Brazil have implemented EPD-based warehouse tags, improving picking accuracy by 16%. Consumer demand is closely tied to localized content delivery and multilingual labeling, reinforcing the need for programmable, real-time update capabilities across diverse retail environments.

How Is Infrastructure Modernization Supporting Energy-Efficient Display Systems?

The Middle East & Africa region holds nearly 4% of global Electronic Paper Display (EPD) installations, with the UAE and South Africa emerging as key growth markets. Infrastructure expansion projects, particularly in transportation and commercial real estate, are driving adoption of low-power digital signage. Oil & gas and construction sectors are incorporating durable EPD panels for field labeling and asset tracking, reducing maintenance cycles by approximately 20%. Smart city initiatives in Gulf countries prioritize energy savings exceeding 35% compared to LCD-based public displays. Trade partnerships facilitating technology imports have improved supply consistency. Consumer behavior reflects increasing demand for multilingual transit information systems and climate-resilient display materials suitable for high-temperature environments.

China – 34% market share: Dominates the Electronic Paper Display (EPD) Market due to large-scale production capacity exceeding 100 million units annually and strong domestic retail digitization programs.

United States – 24% market share: Leads in enterprise-level Electronic Paper Display (EPD) adoption, supported by widespread smart retail networks and high integration of AI-driven inventory management systems.

The Electronic Paper Display (EPD) market is moderately consolidated, with over 35 active global and regional manufacturers competing across panel production, controller IC development, and integrated electronic shelf label (ESL) systems. The top five companies collectively account for approximately 68% of total global shipments, reflecting strong technological barriers and intellectual property concentration in electrophoretic display materials and waveform optimization.

Competition is primarily driven by advancements in color rendering, refresh rate enhancement, and ultra-low power consumption. Leading players are investing heavily in flexible substrate development, with more than 25% of new product launches in 2024 focused on thin-film plastic-based displays under 0.5 mm thickness. Strategic partnerships between display manufacturers and retail automation providers have increased by nearly 30% over the past two years, accelerating deployment in large-scale retail networks exceeding 5,000 stores.

Mergers and technology licensing agreements are shaping market positioning, particularly in Asia-Pacific where production capacity exceeds 100 million display modules annually. Companies are differentiating through integrated IoT communication platforms capable of reducing update latency by 40% and extending battery life beyond 5 years. Innovation intensity remains high, with over 200 active patents filed globally in 2024 related to color e-paper waveforms, encapsulation durability, and low-temperature performance optimization.

Samsung Display

Sharp Corporation

AUO Corporation

Pervasive Displays

Plastic Logic

Visionect

Solomon Systech Limited

The Electronic Paper Display (EPD) market is being reshaped by both incremental and disruptive technology innovations that enhance readability, durability, energy efficiency, and integration with digital ecosystems. Core electrophoretic display technology remains fundamental, leveraging microcapsule particle movement within a stable particle matrix to achieve low-power, high-contrast visual output. Latest-generation EPD modules support pixel densities above 300 PPI in monochrome and color formats, improving clarity for high-resolution labeling, retail signage, and public information displays. Color EPD innovations now feature advanced pigment layering techniques that achieve refresh improvements of approximately 28% compared to earlier color e-paper iterations, enabling dynamic promotional content without pronounced ghosting. Flexible and foldable substrate technologies have matured, with ultra-thin plastic-based EPD panels under 0.5 mm thickness demonstrating a 15% reduction in display weight and 18% improved mechanical resilience under repeated bending tests. These flexible panels are gaining traction in transportation signage, healthcare wearable identifiers, and integrated IoT devices.

Power management advancements are central to EPD competitiveness. New controller ICs and waveform generation algorithms have extended battery lifespans beyond 5 years in static display environments, with some low-power modules achieving energy consumption reductions nearing 50% compared to traditional LCD alternatives in comparable use cases. Wireless communication protocols optimized for EPD networks have reduced update latency by up to 40% in multi-store retail deployments, enhancing real-time synchronization and content accuracy. Integration with cloud-based content management systems and AI-enabled analytics platforms is another evolving trend. Smart EPD ecosystems now support automated pricing updates, inventory triggers, and remote operational diagnostics, delivering measurable operational efficiency improvements in large-scale environments exceeding 1,000 display nodes. Development of industry-specific APIs and SDKs is enabling seamless interoperability with enterprise resource planning (ERP) systems and mobile device management (MDM) infrastructures.

• In January 2024, E Ink Holdings unveiled its Spectra™ 6 full-color e-paper platform, enabling enhanced color saturation and improved refresh performance for retail electronic shelf labels. The technology supports multi-color imaging with reduced power consumption, strengthening adoption in large-format digital signage. Source: www.eink.com

• In March 2024, BOE Technology Group announced mass production expansion of its ePaper display lines in China, increasing annual production capacity by over 20 million units to meet growing global demand for low-power retail and logistics display applications. Source: www.boe.com

• In September 2024, LG Display introduced a 13.3-inch color Electronic Paper Display panel optimized for outdoor digital signage, delivering up to 40% lower energy usage compared to conventional LCD signage under static display conditions. Source: www.lgdisplay.com

• In February 2025, Samsung Display showcased an ultra-thin flexible e-paper prototype at a global technology exhibition, featuring sub-0.5 mm thickness and enhanced durability for smart labeling and transportation applications. The prototype demonstrated improved refresh efficiency and extended battery life performance. Source: www.samsungdisplay.com

The Electronic Paper Display (EPD) Market Report provides comprehensive coverage of technology evolution, product segmentation, deployment models, and cross-industry adoption patterns across more than 25 key countries. The report evaluates core product types including monochrome, color, flexible, segmented, and large-format EPD panels, analyzing their technical characteristics such as pixel density exceeding 300 PPI, battery lifecycles surpassing 5 years, and energy savings reaching up to 50% compared to traditional LCD systems.

Application coverage spans retail electronic shelf labeling, e-readers, industrial asset tracking, public transportation signage, healthcare labeling systems, and smart identification cards. The report assesses enterprise-scale deployments exceeding 1,000 store networks and warehouse systems integrating over 50,000 smart tags. It further analyzes IoT-enabled display ecosystems capable of reducing manual intervention by approximately 30% through automated content management.

Geographically, the scope includes Asia-Pacific, North America, Europe, South America, and Middle East & Africa, incorporating manufacturing trends, infrastructure modernization, regulatory influences, and sustainability-driven procurement patterns. Regional production hubs with annual capacities exceeding 100 million display modules are examined alongside emerging adoption markets undergoing retail digitization.

The report also evaluates innovation pipelines, including flexible substrates under 0.5 mm thickness, color waveform optimization technologies improving refresh rates by nearly 30%, and hybrid reflective display architectures. Competitive benchmarking includes over 35 active global participants, patent activity exceeding 200 annual filings, and strategic partnerships accelerating IoT integration. By combining technology analysis, deployment metrics, regulatory insights, and end-user adoption patterns, the report delivers a structured, decision-ready framework for stakeholders evaluating long-term opportunities within the Electronic Paper Display (EPD) Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

E Ink Holdings, BOE Technology Group, LG Display, Samsung Display, Sharp Corporation, AUO Corporation, Pervasive Displays, Plastic Logic, Visionect, Solomon Systech Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |