Reports

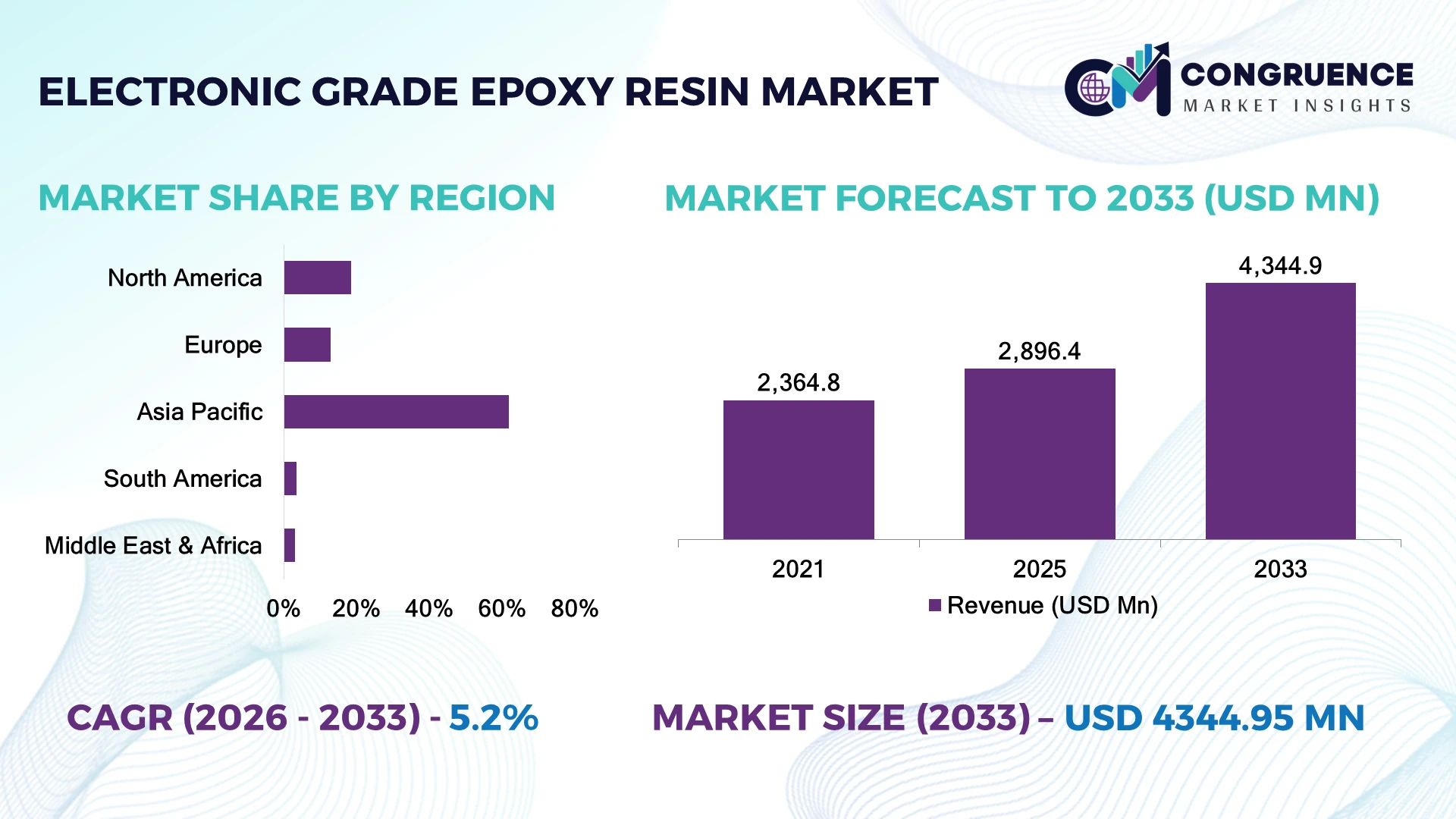

The Global Electronic Grade Epoxy Resin Market was valued at USD 2,896.4 Million in 2025 and is anticipated to reach a value of USD 4,344.9 Million by 2033 expanding at a CAGR of 5.20% between 2026 and 2033. Market expansion is driven by increasing semiconductor packaging density, advanced PCB manufacturing, and rapid deployment of high-reliability electronic components for electric vehicles, AI servers, and 5G communication infrastructure.

China dominates the global Electronic Grade Epoxy Resin Market with approximately 41% of regional production capacity, supported by multi-billion-dollar semiconductor investments and a strong electronics manufacturing ecosystem. Japan maintains technological leadership in ultra-high-purity resin formulations, while South Korea leads advanced chip packaging adoption with over 70% of memory fabrication using premium encapsulation materials. Ongoing U.S.–China semiconductor supply-chain realignment is accelerating regional production diversification and technology localization.

Companies prioritizing localized supply networks and advanced material innovation will secure stronger long-term competitive positioning.

Market Size & Growth: USD 2,896.4 Million in 2025, projected to reach USD 4,344.9 Million by 2033 at 5.20%, supported by advanced semiconductor packaging and AI electronics expansion.

Top Growth Drivers: Semiconductor packaging demand (+18%), electric vehicle electronics adoption (+16%), and high-density PCB production (+14%) continue strengthening market momentum.

Short-Term Forecast: By 2028, manufacturing defect rates decline by nearly 12% through automation and precision material processing.

Emerging Technologies: AI-assisted material formulation, automated dispensing systems, and ultra-low ionic impurity epoxy technologies enhance production performance.

Regional Leaders: Asia Pacific exceeds USD 2,450 Million, North America approaches USD 760 Million, and Europe surpasses USD 620 Million, driven by semiconductor localization and electronics manufacturing.

Consumer/End-User Trends: Nearly 68% of advanced semiconductor packaging utilizes high-purity electronic-grade epoxy materials for enhanced reliability.

Pilot/Case Example: In 2024, advanced chip packaging facilities improved production yield by approximately 15% after adopting next-generation epoxy encapsulation materials.

Competitive Landscape: Leading suppliers collectively account for approximately 48% market share, with Hexion, Olin Corporation, Huntsman Corporation, Kukdo Chemical, and Nan Ya Plastics driving innovation.

Regulatory & ESG Impact: Low-VOC processing technologies reduce manufacturing emissions by nearly 20% while supporting stricter environmental compliance across major electronics hubs.

Investment & Funding: More than USD 8 Billion in semiconductor material ecosystem investments support production expansion, strategic partnerships, and localized supply chains.

Innovation & Future Outlook: Advanced low-stress encapsulation materials, wafer-level packaging compatibility, and next-generation AI electronics accelerate long-term product innovation.

Electronic Grade Epoxy Resin Market demand continues expanding across semiconductor encapsulation, high-frequency printed circuit boards, and automotive electronics requiring exceptional thermal stability and dielectric performance. Manufacturers are introducing ultra-low impurity and halogen-free formulations, while nearly 30% of new electronic packaging projects incorporate advanced resin technologies. Semiconductor supply-chain localization and stricter material qualification standards are reinforcing innovation priorities, setting the stage for broader strategic market developments.

Electronic grade epoxy resin has become a strategic material for advanced electronics manufacturing as semiconductor miniaturization, AI computing infrastructure, and electric mobility accelerate demand for highly reliable encapsulation materials. Global supply-chain restructuring and increasing domestic semiconductor manufacturing programs are encouraging manufacturers to strengthen regional production capabilities while reducing dependence on concentrated sourcing locations.

Compared with conventional industrial epoxy systems, electronic-grade formulations deliver nearly 20% lower ionic contamination and improve component reliability by approximately 15% in advanced semiconductor packaging applications. Asia Pacific continues leading large-scale production and electronics manufacturing, while North America emphasizes domestic semiconductor capacity expansion and Europe focuses on high-value automotive and industrial electronics supported by advanced material innovation. Over the next two to three years, automated quality inspection and digital manufacturing platforms are expected to increase production consistency by more than 10%.

Leading manufacturers are expanding clean-room production facilities, establishing regional technical centers, and forming partnerships with semiconductor packaging companies to accelerate product qualification cycles. For example, advanced wafer-level packaging facilities increasingly deploy high-purity epoxy encapsulation materials to improve thermal performance and long-term device durability. Companies aligning material innovation with localized manufacturing strategies and next-generation electronics requirements will strengthen competitive positioning and secure sustainable operational advantages.

The transition toward advanced semiconductor packaging and high-density electronics is strengthening demand for electronic grade epoxy resin with superior dielectric insulation and thermal stability. More than 68% of advanced chip packages now utilize high-purity encapsulation materials, while over 55% of newly installed packaging lines support wafer-level packaging technologies. China's continued expansion of semiconductor fabrication capacity and the U.S. CHIPS manufacturing initiatives are reshaping global material sourcing and qualification standards. This shift improves component reliability, extends product life, and supports higher integration densities. In response, leading manufacturers are expanding clean-room production, investing in ultra-low ionic contamination formulations, and partnering with semiconductor packaging companies to accelerate product qualification. Companies capable of shortening qualification cycles gain a significant operational advantage in premium electronics applications.

Electronic grade epoxy resin production remains exposed to supply concentration for high-purity epichlorohydrin, bisphenol-based intermediates, and specialty curing agents. Raw material costs have experienced fluctuations exceeding 18% during recent supply disruptions, while nearly 60% of high-purity precursor production remains concentrated in a limited number of manufacturing hubs. Export controls on semiconductor-related materials and logistics disruptions continue extending procurement lead times for specialty chemical producers. These conditions increase production costs, reduce inventory flexibility, and complicate long-term customer contracts. Manufacturers are responding by diversifying supplier networks, localizing critical raw material procurement, and securing multi-year sourcing agreements. Companies establishing geographically balanced supply chains improve production resilience while reducing operational exposure to geopolitical disruptions.

Growing adoption of AI accelerators, electric vehicles, and advanced medical electronics is creating demand for next-generation electronic grade epoxy resin with enhanced thermal conductivity and reduced ionic impurities. More than 40% of new semiconductor packaging investments target advanced packaging technologies, while halogen-free electronic materials have expanded adoption by approximately 25% across premium electronics manufacturing. Japan continues advancing ultra-high-purity resin technologies through material innovation, supporting increasingly complex chip architectures. Companies are expanding R&D programs, collaborating with semiconductor equipment suppliers, and developing bio-based and recyclable epoxy chemistries that improve manufacturing efficiency while supporting evolving environmental requirements. Early investment in customized formulations positions suppliers to secure long-term design wins in high-value electronic applications.

Electronic grade epoxy resin manufacturers face increasing challenges in qualifying materials for rapidly evolving semiconductor architectures requiring exceptional purity and reliability. Product qualification frequently exceeds 12 months for advanced packaging applications, while nearly 70% of high-performance electronic materials undergo multiple validation stages before commercial deployment. Continuous reductions in semiconductor feature sizes increase sensitivity to ionic contamination and process variation, raising technical barriers for new suppliers. These complexities slow commercialization, increase development costs, and limit rapid market entry. Companies are investing in digital quality control, advanced analytical laboratories, and collaborative testing programs with semiconductor manufacturers to shorten validation cycles. Organizations capable of consistently meeting stringent qualification requirements will secure stronger long-term competitive differentiation.

Advanced Packaging Material Transition: Semiconductor manufacturers are accelerating adoption of low-stress electronic grade epoxy resin for wafer-level and heterogeneous packaging, with more than 62% of newly qualified packaging lines supporting advanced encapsulation materials. Process optimization has reduced package defects by nearly 14%, while automated dispensing systems improve production consistency. Companies are expanding dedicated clean-room manufacturing and strengthening customer qualification programs as AI processors and high-bandwidth memory increase material performance requirements.

Localized Supply Chain Expansion: Electronics material suppliers are restructuring procurement networks as localization initiatives continue across China, the United States, and Japan. Nearly 38% of new material investments are directed toward domestic production capability, while supplier qualification cycles have increased by approximately 20% to strengthen resilience. Manufacturers are establishing regional technical centers, expanding strategic inventories, and forming long-term partnerships to reduce logistics risk and improve delivery reliability for semiconductor customers.

Ultra-Low Impurity Material Development: Demand for electronic grade epoxy resin with exceptionally low ionic contamination continues rising as semiconductor nodes become increasingly complex. More than 55% of premium packaging projects specify ultra-high-purity formulations, while halogen-free product adoption has expanded by roughly 24% across advanced electronics manufacturing. Companies are increasing analytical testing capacity, automating quality inspection, and introducing customized resin systems to support next-generation chip architectures and higher production yields.

Digital Manufacturing Quality Integration: Manufacturers are integrating artificial intelligence, machine vision, and predictive quality analytics throughout electronic grade epoxy resin production. Automated inspection improves batch consistency by approximately 16%, while digital process monitoring reduces production downtime by nearly 11%. Growing pressure for defect-free semiconductor materials is encouraging companies to modernize manufacturing execution systems, standardize process control, and accelerate collaborative development with semiconductor packaging partners.

Bisphenol A (BPA) epoxy resin represents the largest product category, accounting for approximately 56% of the Electronic Grade Epoxy Resin Market due to its excellent dielectric properties, thermal stability, mechanical strength, and compatibility with semiconductor encapsulation and printed circuit board manufacturing. Its mature production ecosystem, competitive processing cost, and extensive qualification history make it the preferred choice for high-volume electronics manufacturing. Novolac epoxy resin remains another important segment where higher heat resistance and chemical durability are essential for advanced semiconductor packaging. Cycloaliphatic epoxy resin is emerging as the fastest-growing segment because of its superior UV resistance, low dielectric loss, and compatibility with miniaturized electronic devices and advanced chip packaging technologies. Glycidylamine and specialty modified epoxy systems continue expanding in high-performance aerospace electronics and AI computing applications requiring enhanced reliability. Leading manufacturers are investing in ultra-low ionic impurity formulations and customized resin platforms to strengthen competitive differentiation as electronics performance standards become increasingly demanding.

Semiconductor packaging accounts for approximately 47% of total demand and remains the dominant application due to continuous expansion of advanced chip manufacturing, AI processors, and memory devices. High reliability, moisture resistance, and electrical insulation performance make electronic grade epoxy resin indispensable for encapsulation and protection of semiconductor components. Printed circuit boards continue representing a mature application supported by growing deployment of automotive electronics, industrial automation equipment, and communication infrastructure. Semiconductor encapsulation is also the fastest-expanding application as heterogeneous integration, chiplet architecture, and wafer-level packaging become mainstream manufacturing approaches. Electrical insulation, LED packaging, and sensor modules continue strengthening their market positions through increasing deployment in electric vehicles, renewable energy systems, and medical electronics. Companies are expanding automated dispensing technologies, improving formulation precision, and collaborating with electronics manufacturers to accelerate qualification for next-generation packaging platforms.

Semiconductor manufacturers remain the largest end-user group, representing approximately 44% of total demand because of continuous investments in chip fabrication, advanced packaging, and high-performance computing devices. Strict material qualification standards, clean-room production requirements, and increasing package complexity sustain long-term consumption of electronic grade epoxy resin. Electronics component manufacturers also maintain substantial purchasing volumes for connectors, sensors, modules, and integrated electronic assemblies serving automotive, industrial, and consumer applications. Automotive electronics manufacturers are the fastest-growing end-user segment as electrification, advanced driver assistance systems, and power semiconductor deployment continue expanding. Consumer electronics, telecommunications equipment manufacturers, and industrial electronics producers are increasing purchases of specialized epoxy formulations supporting higher thermal performance and reliability. Suppliers are responding through application-specific product customization, long-term technical partnerships, and localized manufacturing strategies that improve supply continuity for strategic customers.

Asia-Pacific accounted for the largest market share at 61.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.8%between 2026 and 2033.

North America represents approximately 18.6% of the global Electronic Grade Epoxy Resin Market, supported by semiconductor manufacturing expansion, advanced electronics production, and strategic reshoring initiatives. The United States continues increasing domestic chip fabrication capacity, creating sustained demand for high-purity encapsulation materials and advanced PCB resins. More than 20 major semiconductor manufacturing and packaging expansion projects are strengthening regional material qualification activity, while AI computing infrastructure and automotive semiconductor production are increasing demand for premium epoxy systems. Companies are expanding technical support centers, strengthening long-term supply agreements, and localizing specialty material inventories to improve supply continuity. Increased automation across semiconductor packaging operations is further enhancing process consistency while reducing manufacturing variability for high-value electronic applications.

United States Market Outlook: The United States remains the region's largest market due to its expanding semiconductor fabrication ecosystem, advanced packaging investments, and strong electronics R&D capabilities. More than 80% of North America's semiconductor manufacturing investment pipeline is concentrated in the country, encouraging electronic-grade material suppliers to establish localized production, application laboratories, and customer collaboration centers. Strong government-backed manufacturing initiatives and rapid AI infrastructure deployment continue strengthening long-term demand for premium epoxy resin formulations.

Europe accounts for approximately 12.9% of the global market, supported by advanced automotive electronics, industrial automation, and high-value semiconductor research. Germany, France, and the Netherlands continue expanding production of electronic systems requiring high-reliability encapsulation materials with superior thermal stability. More than 35% of newly developed automotive electronic modules utilize advanced resin formulations for improved durability and electrical insulation. Manufacturers are emphasizing halogen-free materials, production efficiency, and localized specialty chemical supply to strengthen resilience against external procurement risks. Collaboration between electronics manufacturers and specialty material suppliers is accelerating product qualification for next-generation mobility and industrial electronics platforms.

Germany Market Outlook: Germany leads the European market through its strong automotive electronics industry, industrial automation expertise, and specialty chemical manufacturing capabilities. Advanced manufacturing facilities continue integrating premium encapsulation materials into power electronics and industrial control systems. More than 45% of regional automotive electronic production is linked to German manufacturing operations, encouraging continuous investment in material innovation, process optimization, and strategic supplier partnerships.

Asia-Pacific contributes approximately 61.8% of global demand, supported by extensive semiconductor fabrication, electronics assembly, and specialty chemical production. China, Japan, South Korea, and Taiwan collectively dominate advanced semiconductor packaging and printed circuit board manufacturing, creating sustained demand for high-purity epoxy resin formulations. Nearly 75% of global semiconductor packaging capacity operates within the region, while continued investments in advanced chip manufacturing strengthen long-term consumption of premium electronic materials. Companies are expanding clean-room production, increasing localized raw material sourcing, and investing in automated manufacturing technologies to improve quality consistency and production efficiency across high-volume electronics applications.

China Market Outlook: China remains the largest country market owing to its integrated semiconductor supply chain, electronics manufacturing scale, and expanding domestic material ecosystem. The country accounts for approximately 41% of regional electronic-grade epoxy resin production capacity, supported by extensive investments in chip fabrication and electronics assembly. Local manufacturers continue expanding specialty resin production while strengthening technical collaboration with semiconductor packaging companies to improve material performance and reduce import dependence.

South America represents approximately 3.5% of the global market, with demand primarily supported by automotive electronics, industrial equipment manufacturing, and consumer electronics assembly. Brazil and Argentina continue expanding electronics manufacturing capabilities, increasing requirements for reliable insulation and encapsulation materials. More than 30% of regional electronic component production is concentrated in organized industrial manufacturing clusters, encouraging suppliers to improve local distribution and technical support. Although specialty material imports remain significant, companies are strengthening regional warehousing, logistics partnerships, and customer service capabilities to reduce lead times and improve operational flexibility for electronics manufacturers.

Brazil Market Outlook: Brazil leads the regional market through its established electronics manufacturing base and expanding automotive component industry. Industrial production clusters continue increasing demand for high-performance electronic materials supporting consumer electronics, industrial automation, and mobility applications. Nearly 60% of South America's organized electronics manufacturing capacity is located in Brazil, creating attractive opportunities for localized inventory management, technical services, and long-term industrial partnerships.

The Middle East & Africa accounts for approximately 3.2% of global demand as governments accelerate industrial diversification, electronics assembly, and digital infrastructure investments. The United Arab Emirates, Saudi Arabia, and South Africa are strengthening industrial manufacturing ecosystems supporting electrical equipment, telecommunications hardware, and specialized electronic components. More than 25% of recent electronics-related industrial projects incorporate advanced manufacturing technologies requiring higher-performance insulation materials. Suppliers are expanding regional distribution partnerships, technical service capabilities, and customized product offerings to support emerging manufacturing operations while improving supply responsiveness across developing industrial markets.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most strategically important market through continued industrial diversification, electronics manufacturing investments, and smart infrastructure development. Large-scale industrial zones are attracting advanced manufacturing activities requiring reliable electronic materials for automation, telecommunications, and energy applications. More than 40% of new regional industrial investment announcements are associated with manufacturing diversification initiatives, encouraging suppliers to establish stronger regional commercial and technical operations.

The Electronic Grade Epoxy Resin Market is led by Hexion, Huntsman Corporation, Nan Ya Plastics, Kukdo Chemical, and DIC Corporation, with global technology leaders competing directly against cost-efficient Asian manufacturers and regional specialty suppliers. The top five companies collectively account for approximately 48% of the market, reflecting moderate consolidation with strong qualification barriers. Competition centers on material purity, thermal reliability, customized formulations, and supply-chain responsiveness rather than pricing alone. Advanced electronic-grade products improve packaging reliability by nearly 15%, while automated manufacturing reduces batch variation by approximately 12%. Suppliers are expanding localized production, strengthening semiconductor partnerships, investing in clean-room manufacturing, and vertically integrating specialty resin development with packaging technologies. Competitive intensity is shifting toward high-performance formulations for AI processors and advanced semiconductor packaging, where qualification speed increasingly determines supplier selection. Strict customer validation, capital-intensive production, and ultra-high-purity processing remain major entry barriers. Winning requires continuous innovation, localized technical support, resilient supply networks, and consistently superior material performance.

Huntsman Corporation

Olin Corporation

DIC Corporation

Nan Ya Plastics Corporation

Kukdo Chemical Co., Ltd.

Chang Chun Group

Sumitomo Bakelite Co., Ltd.

Mitsubishi Chemical Group

Aditya Birla Chemicals

Atul Ltd.

Jiangsu Sanmu Group

Electronic grade epoxy resin technology is rapidly advancing toward ultra-low ionic contamination, high thermal conductivity, and precision formulation for semiconductor packaging. Advanced encapsulation materials reduce ionic contamination by approximately 20% while improving package reliability by nearly 15% compared with conventional electronic epoxy systems. More than 60% of new advanced packaging programs now specify high-purity resin systems, particularly for AI processors, high-bandwidth memory, and automotive power semiconductors. Companies investing in customized formulations and digital material characterization achieve faster qualification and stronger customer retention.

Artificial intelligence-assisted formulation development, automated dispensing, machine vision inspection, and digital process control are transforming manufacturing operations. Automated quality inspection improves batch consistency by approximately 16%, while predictive process analytics reduce production downtime by nearly 11%. Semiconductor manufacturers benefit most because shorter qualification cycles and improved process repeatability accelerate commercialization of advanced packaging technologies. Integration of digital manufacturing platforms also strengthens traceability across increasingly complex electronics supply chains.

Between 2026 and 2028, demand will increasingly favor halogen-free, low-stress encapsulation materials compatible with chiplet architectures and heterogeneous integration. Material suppliers adopting digital R&D, automated production, and advanced analytical laboratories will strengthen competitive differentiation. Companies delaying technology modernization risk longer qualification timelines, reduced design wins, and weaker positioning in premium semiconductor applications where material performance increasingly determines manufacturing success.

February 2025 – Henkel announced a new Application Engineering Center in Chennai and expanded electronics adhesive manufacturing at Kurkumbh, India, strengthening localized electronics material support. The investment accelerates customer development cycles and expands regional manufacturing capabilities for advanced electronics. Source: www.henkel.com

August 2025 – DIC Corporation approved construction of a new semiconductor-grade epoxy resin production facility at its Chiba Plant, increasing annual production capacity by approximately 59% through advanced manufacturing processes. The expansion strengthens supply for next-generation semiconductor packaging applications.

January 2025 – Korea Institute of Science and Technology developed a next-generation one-component epoxy with improved high-temperature stability and flame resistance, delivering significantly enhanced storage stability through an advanced latent curing system. The innovation improves manufacturing consistency for electronics applications. Source: www.eurekalert.org

2025 – Hexion expanded its manufacturing digitalization strategy through AI-enabled quality and innovation initiatives, strengthening production optimization and advanced materials development for high-performance applications. The operational transformation improves manufacturing efficiency and accelerates customer-focused product innovation. Source: www.hexion.com

This report delivers comprehensive analysis across the Electronic Grade Epoxy Resin Market by resin type, application, end-user, and major geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates established and emerging product categories, semiconductor packaging technologies, printed circuit board manufacturing, electrical insulation applications, and evolving demand across semiconductor manufacturers, automotive electronics producers, consumer electronics companies, and industrial equipment manufacturers. More than 60% of market demand remains concentrated in advanced electronics manufacturing, highlighting strong deployment across high-performance semiconductor applications.

The study provides strategic evaluation of manufacturing trends, technology innovation, supply-chain developments, competitive positioning, and enterprise expansion strategies between 2026 and 2033. It also assesses advanced packaging materials, halogen-free formulations, automation adoption, localized production strategies, and next-generation electronic material development. Business intelligence throughout the report supports investment prioritization, market entry planning, partnership evaluation, product portfolio optimization, competitive benchmarking, and long-term operational decision-making across both mature and emerging electronic materials markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,896.4 Million |

| Market Revenue (2033) | USD 4,344.9 Million |

| CAGR (2026–2033) | 5.20% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Hexion; Huntsman Corporation; Olin Corporation; DIC Corporation; Nan Ya Plastics Corporation; Kukdo Chemical Co., Ltd.; Chang Chun Group; Sumitomo Bakelite Co., Ltd.; Mitsubishi Chemical Group; Aditya Birla Chemicals; Atul Ltd.; Jiangsu Sanmu Group |

| Customization & Pricing | Available on Request (10% Customization Free) |