Reports

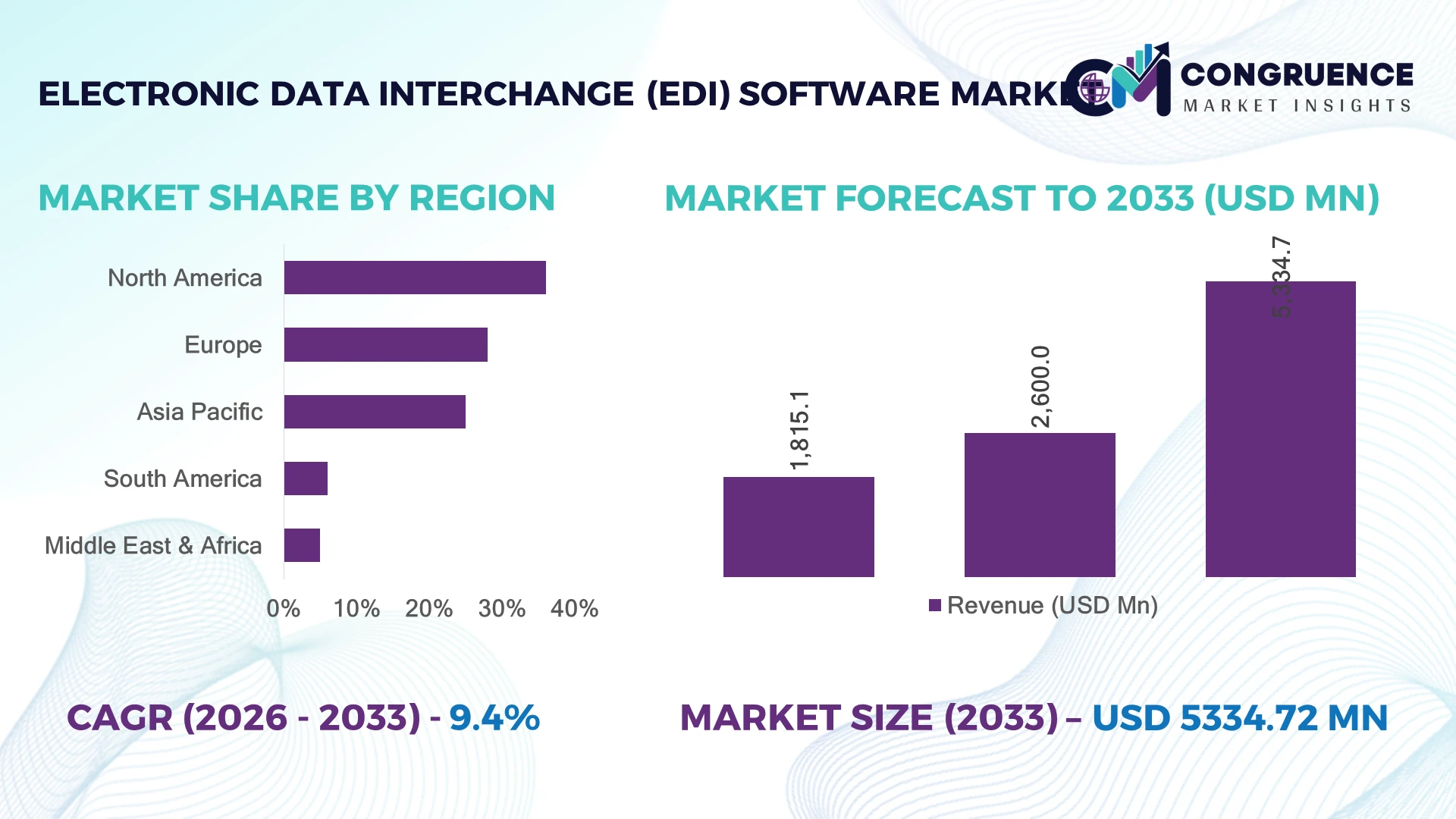

The Global Electronic Data Interchange (EDI) Software Market was valued at USD 2600 Million in 2025 and is anticipated to reach a value of USD 5334.72 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. Growth is accelerating through AI-enabled B2B transaction automation, rising multi-enterprise supply chain digitization, and mandatory e-invoicing compliance frameworks across manufacturing, retail, healthcare, and logistics sectors.

The United States dominates the global Electronic Data Interchange (EDI) Software Market with nearly 34% share, supported by advanced retail, automotive, and healthcare transaction ecosystems processing over 22 billion EDI documents annually in 2026. Germany leads European industrial integration with over 68% adoption among large manufacturers, while China records the fastest enterprise onboarding rate due to cross-border trade digitization and export compliance modernization amid ongoing Red Sea shipping disruptions and regional supply chain realignments. Cloud-based EDI deployment penetration exceeded 61% across large enterprises, outperforming legacy on-premise infrastructure in transaction speed and partner integration scalability.

Organizations prioritizing interoperable, API-connected EDI platforms with real-time analytics capabilities are securing stronger supplier visibility, lower transaction error rates, and faster procurement execution across global trade networks.

Market Size & Growth: USD 2600 Million in 2025 reaching USD 5334.72 Million by 2033, driven by cloud-native B2B integration and automated supplier onboarding across global trade ecosystems.

Top Growth Drivers: E-invoicing mandates increased 41%, AI-driven workflow automation adoption rose 38%, and digital supply chain integration expanded 35% across enterprises.

Short-Term Forecast: By 2028, automated EDI deployment reduces invoice processing costs by 32% and improves procurement cycle efficiency by 27%.

Emerging Technologies: AI-powered exception handling, API-EDI convergence, and blockchain-backed transaction validation improved data accuracy by nearly 29%.

Regional Leaders: North America exceeds USD 1.8 Billion with healthcare digitization growth; Europe surpasses USD 1.4 Billion through compliance modernization; Asia-Pacific crosses USD 1.6 Billion driven by export manufacturing automation.

Consumer/End-User Trends: Nearly 64% of enterprises prioritize cloud EDI platforms for faster partner integration and multi-channel transaction visibility.

Pilot/Case Example: In 2026, a global retail distribution project reduced order reconciliation delays by 36% through AI-enabled EDI workflow orchestration.

Competitive Landscape: Top vendors collectively control approximately 46% market share, with competition intensifying among enterprise integration and SaaS-based EDI providers.

Regulatory & ESG Impact: Digital invoicing and paperless trade initiatives lowered document processing waste by 31% across regulated logistics and manufacturing sectors.

Investment & Funding: Enterprise integration investments exceeded USD 2.1 Billion in 2026, fueled by cloud migration partnerships and cross-border trade infrastructure expansion.

Innovation & Future Outlook: Real-time predictive transaction analytics and autonomous supplier communication platforms are reshaping advanced global EDI software deployment strategies.

Electronic Data Interchange (EDI) Software Market demand is expanding rapidly across retail fulfillment, automotive procurement, healthcare claims processing, and third-party logistics operations. AI-assisted transaction validation and API-integrated cloud EDI platforms improved processing accuracy by nearly 30% in 2026, while enterprises accelerated migration from legacy VAN networks to scalable SaaS environments. Growing e-invoicing mandates and supply-chain resiliency initiatives across Asia-Pacific and Europe continue strengthening strategic enterprise integration priorities.

Electronic Data Interchange (EDI) software has become strategically critical as enterprises restructure supply chains, automate procurement ecosystems, and comply with expanding digital invoicing mandates across global trade corridors. Large manufacturers and retailers now prioritize real-time transaction orchestration to reduce order discrepancies, improve supplier visibility, and accelerate cross-border fulfillment. In 2026, over 63% of multinational enterprises integrated cloud-based EDI platforms into procurement and logistics operations, particularly following trade rerouting pressures linked to Red Sea shipping disruptions and stricter European electronic compliance frameworks.

Modern API-enabled EDI platforms process partner onboarding nearly 45% faster than legacy VAN-based systems while reducing manual invoice reconciliation costs by approximately 30%. The United States leads in healthcare and retail transaction density, whereas Germany and Japan emphasize industrial interoperability and manufacturing-grade automation standards. Over the next two to three years, AI-assisted exception management and predictive transaction monitoring are expected to reduce operational processing delays by more than 25% across high-volume enterprise environments.

Global logistics providers and automotive suppliers are expanding partnerships with cloud integration vendors to standardize supplier communication across multi-country operations. Companies investing in interoperable EDI ecosystems, cybersecurity resilience, and real-time analytics infrastructure are strengthening long-term competitive positioning through faster transaction execution, lower compliance exposure, and scalable digital trade operations.

Manufacturing, retail, and healthcare enterprises are rapidly modernizing transaction infrastructure to improve procurement speed, inventory synchronization, and supplier coordination. More than 61% of large organizations shifted toward cloud-based EDI ecosystems in 2026, while automated invoice processing reduced manual reconciliation workloads by nearly 34%. Germany’s industrial export sector and the United States healthcare claims network continue driving high-volume transaction automation due to stricter compliance requirements and rising operational complexity. Companies are responding by integrating AI-driven exception management, API-based connectivity, and multi-enterprise data orchestration into EDI environments. A notable operational shift involves retailers consolidating fragmented supplier communication systems into centralized digital trade networks, improving order accuracy and reducing fulfillment latency. Strategic partnerships between enterprise software providers and logistics operators are accelerating scalable EDI deployment across cross-border supply chains.

Fragmented enterprise infrastructure and incompatible transaction standards continue limiting scalable EDI software deployment across mid-sized enterprises and supplier networks. Nearly 42% of organizations still operate hybrid legacy systems requiring costly middleware integration, while onboarding smaller suppliers increases implementation timelines by approximately 28%. In Japan and parts of Southeast Asia, dependence on outdated proprietary communication protocols slows interoperability between manufacturers, distributors, and logistics providers. Rising cybersecurity compliance requirements are also increasing operational expenditures for encrypted transaction management and audit tracking. Companies handling multi-country operations face inconsistent electronic invoicing regulations, complicating standardized deployment models. To reduce integration risks, enterprises are investing in modular cloud architectures, localized compliance engines, and third-party managed integration services. Businesses prioritizing interoperability flexibility are achieving faster partner expansion and lower operational disruption during digital migration initiatives.

AI-powered automation and predictive transaction analytics are creating high-value opportunities across advanced Electronic Data Interchange (EDI) Software Market ecosystems. Intelligent EDI orchestration platforms improved exception resolution efficiency by nearly 37% in 2026, while API-integrated supplier onboarding reduced implementation time by over 40%. India and Mexico are emerging as important deployment hubs due to expanding export manufacturing networks and rapid digital procurement adoption among mid-sized enterprises. Governments implementing mandatory electronic invoicing frameworks are accelerating enterprise migration toward cloud-native transaction infrastructure. Companies are increasingly investing in embedded analytics, real-time shipment visibility, and autonomous procurement communication systems to strengthen supply chain responsiveness. A non-obvious strategic opportunity involves integrating EDI platforms with sustainability tracking modules, enabling enterprises to monitor paperless transaction compliance and supplier-level carbon reporting without additional operational layers.

As enterprise transaction volumes expand, cybersecurity resilience and skilled integration management are becoming critical long-term execution challenges. Nearly 48% of global organizations reported increased exposure to B2B data vulnerabilities linked to interconnected supplier ecosystems, while complex multi-format integrations increased deployment maintenance workloads by approximately 31%. The United States and South Korea face rising pressure to secure healthcare, automotive, and semiconductor transaction networks against ransomware and data interception threats. Shortages of experienced EDI integration specialists are also delaying large-scale modernization projects and increasing dependency on outsourced managed services. Companies must strengthen encryption frameworks, real-time anomaly detection, and zero-trust transaction architectures to maintain operational continuity. Businesses investing early in AI-assisted monitoring, workforce upskilling, and scalable cloud security infrastructure are expected to achieve stronger deployment consistency and competitive resilience across digitally interconnected supply chains.

AI-Led Workflow Automation Expansion Enterprise EDI environments are rapidly integrating AI-assisted exception handling and predictive transaction validation to reduce manual intervention. In 2026, automated reconciliation deployment increased by 39%, while transaction error resolution time declined nearly 33% across retail and manufacturing operations. Labor shortages in logistics and procurement functions accelerated workflow orchestration investments. Companies are scaling intelligent document processing capabilities and partnering with enterprise AI providers to improve supplier communication speed, compliance accuracy, and procurement continuity.

API And EDI Convergence Growth Enterprises are restructuring legacy B2B integration frameworks through API-enabled EDI ecosystems supporting real-time data synchronization. More than 58% of multinational companies now operate hybrid API-EDI transaction environments, improving partner onboarding speed by approximately 42%. German automotive suppliers and U.S. healthcare networks are prioritizing interoperable architectures to support multi-format transaction exchanges. Vendors are responding through modular integration platforms and cloud-native deployment models that simplify enterprise expansion and reduce infrastructure dependency across fragmented supplier networks.

Cross-Border Compliance Digitization Surge Mandatory electronic invoicing frameworks and digital trade regulations are accelerating EDI standardization across export-driven industries. In 2026, enterprise compliance automation adoption increased 36%, while paper-based transaction workflows declined by nearly 29%. Mexico and India strengthened digital tax reporting requirements, forcing suppliers to modernize procurement communication systems. Companies are investing in localized compliance engines, encrypted transaction management, and regional integration partnerships to maintain uninterrupted cross-border operations and reduce customs processing delays.

Managed Services Adoption Intensifies Rising cybersecurity complexity and integration maintenance costs are increasing demand for managed EDI services among mid-sized enterprises. Outsourced transaction monitoring deployment expanded by 31% in 2026, particularly across logistics providers and healthcare distributors handling sensitive supplier data. A non-obvious operational shift involves companies consolidating fragmented regional EDI vendors into centralized managed ecosystems to improve visibility and reduce duplicated infrastructure spending. Service providers are expanding multilingual support capabilities and industry-specific compliance modules to strengthen long-term client retention.

Cloud-Based EDI remains the dominant segment due to its scalability, faster supplier onboarding, and lower infrastructure dependency across high-volume enterprise transaction environments. In 2026, more than 61% of multinational organizations prioritized cloud deployment models because they reduced implementation timelines by nearly 35% and improved multi-partner integration flexibility. Large retailers and healthcare providers in the United States increasingly shifted away from isolated on-premises architectures toward centralized cloud orchestration systems supporting real-time procurement visibility and AI-enabled monitoring. Vendors are expanding API integration capabilities, encrypted data exchange layers, and industry-specific compliance modules to strengthen enterprise retention.

Managed EDI Services represent the fastest-growing segment as mid-sized companies outsource transaction monitoring, cybersecurity management, and compliance operations to reduce operational complexity. Meanwhile, On-Premises EDI continues serving heavily regulated sectors requiring strict data control, while Web EDI maintains relevance among smaller suppliers with limited IT infrastructure. Mobile EDI adoption is also accelerating in logistics and field-based operations where real-time shipment updates are operationally critical. Companies are increasingly restructuring product portfolios through hybrid deployment offerings combining cloud scalability with localized security controls.

Supply Chain Management remains the leading application segment due to growing enterprise dependence on synchronized procurement, supplier communication, and shipment coordination across multi-country trade networks. In 2026, automated supply-chain transaction processing improved order fulfillment visibility by approximately 32%, while digital supplier onboarding efficiency increased nearly 28%. Global manufacturers and retail distributors are integrating EDI workflows with warehouse management and transportation systems to reduce stock disruptions caused by shipping route volatility and inventory imbalances. Companies are scaling AI-assisted transaction monitoring and predictive procurement analytics to improve operational continuity and supplier responsiveness.

Invoice Management is emerging as the fastest-growing application as governments strengthen electronic invoicing mandates and tax reporting digitization frameworks. Logistics Management continues expanding through real-time freight coordination and shipment status integration, particularly in Germany and Japan. Order Processing remains strategically important for high-volume retail operations, while Inventory Management adoption is increasing among automotive and healthcare suppliers seeking tighter stock accuracy. Vendors are investing in interoperable transaction ecosystems connecting invoicing, procurement, and logistics workflows through unified digital trade platforms.

The Manufacturing Industry remains the dominant end-user segment due to high transaction intensity across procurement, production scheduling, supplier synchronization, and export operations. In 2026, more than 67% of large industrial manufacturers operated integrated EDI transaction frameworks supporting automated supplier communication and real-time inventory coordination. Germany, Japan, and the United States continue leading deployment density because automotive, electronics, and industrial equipment sectors require highly standardized transaction processing environments. EDI vendors are targeting manufacturers through customized interoperability modules, predictive transaction analytics, and vertically integrated procurement automation platforms designed for complex supplier ecosystems.

Logistics Companies represent the fastest-growing end-user group as freight operators modernize shipment coordination, customs documentation, and warehouse communication systems under rising cross-border delivery pressure. Retail Industry adoption remains strong due to omnichannel fulfillment expansion and supplier visibility requirements, while Healthcare Industry deployment is increasing for claims processing and pharmaceutical procurement accuracy. BFSI organizations continue prioritizing secure transaction authentication and regulatory reporting workflows. Automotive Industry buyers are expanding investment in multi-tier supplier connectivity and AI-assisted procurement orchestration to improve production continuity and operational resilience.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Enterprise Automation and Compliance Integration Leadership

North America maintains the highest deployment concentration in the Electronic Data Interchange (EDI) Software Market due to mature digital trade infrastructure, advanced healthcare transaction networks, and large-scale retail procurement ecosystems. The region accounted for approximately 36% of global deployment activity in 2025, supported by rapid migration toward cloud-native B2B integration frameworks. U.S.-based logistics and retail enterprises increased AI-assisted EDI workflow implementation by nearly 34% during 2026 to reduce order reconciliation delays and supplier coordination gaps. Healthcare providers and automotive manufacturers are also expanding encrypted transaction management capabilities to comply with stricter cybersecurity and electronic invoicing standards. Technology vendors continue strengthening regional partnerships with ERP providers and supply-chain software firms to improve interoperability across complex enterprise transaction environments.

United States Market Outlook: The United States leads regional deployment through extensive healthcare claims processing, omnichannel retail infrastructure, and industrial procurement digitization. More than 68% of large enterprises integrated cloud-based EDI environments into supply-chain coordination systems by 2026, particularly across manufacturing and logistics sectors. Companies are investing heavily in API-enabled interoperability, predictive transaction analytics, and AI-driven exception handling to strengthen procurement efficiency and reduce supplier communication bottlenecks across multi-state operations.

Regulatory Standardization Accelerates Industrial Modernization

Europe remains a strategically important market driven by electronic invoicing mandates, industrial automation priorities, and cross-border digital trade modernization. Manufacturing-heavy economies including Germany, France, and Italy continue expanding interoperable EDI infrastructure to improve supplier synchronization and export coordination. Nearly 59% of large industrial enterprises across the region adopted integrated procurement communication systems in 2026 to comply with evolving digital tax reporting regulations. Sustainability-focused paperless transaction initiatives are also strengthening enterprise migration toward cloud-enabled EDI platforms. Logistics operators are consolidating fragmented transaction networks through centralized compliance management systems to reduce operational complexity and customs processing delays across intra-European trade corridors.

Germany Market Outlook: Germany dominates the regional market through its advanced automotive, industrial equipment, and export manufacturing ecosystem. More than 71% of large manufacturers implemented automated supplier transaction frameworks by 2026 to improve production continuity and procurement traceability. German enterprises are prioritizing standardized API-EDI integration models and encrypted trade documentation systems to support high-volume industrial exports while complying with strict European digital invoicing and cybersecurity requirements.

Export Manufacturing Expansion Drives Deployment Scale

Asia-Pacific is emerging as the fastest-expanding regional market due to export manufacturing growth, digital procurement modernization, and rapid enterprise cloud adoption. China, India, Japan, and South Korea continue increasing deployment density across automotive, electronics, healthcare, and logistics industries. In 2026, cloud-based EDI adoption across export-oriented enterprises increased by approximately 38%, supported by government-backed digital trade initiatives and expanding cross-border e-commerce activity. Regional manufacturers are integrating EDI platforms with warehouse automation and transportation management systems to improve inventory coordination and shipment visibility. Technology vendors are accelerating localized partnerships and multilingual transaction capabilities to strengthen penetration among mid-sized industrial suppliers and logistics operators.

China Market Outlook: China leads regional scale through its extensive export manufacturing infrastructure and high-volume cross-border trade operations. Nearly 66% of large industrial exporters integrated automated procurement communication systems by 2026 to improve supplier responsiveness and customs documentation efficiency. Chinese enterprises are expanding investments in AI-enabled transaction monitoring, cloud interoperability, and smart logistics coordination to strengthen operational resilience amid evolving global supply-chain restructuring pressures.

Digital Tax Reform Reshapes Enterprise Transactions

South America is experiencing steady Electronic Data Interchange (EDI) software adoption as governments strengthen electronic invoicing frameworks and enterprises modernize fragmented procurement operations. Brazil, Argentina, and Chile are increasing digital transaction infrastructure deployment across retail, logistics, and manufacturing sectors to improve compliance efficiency and reduce paper-based workflow dependency. In 2026, enterprise invoice automation deployment across the region increased by approximately 29%, supported by expanding cloud integration accessibility among mid-sized businesses. However, inconsistent connectivity infrastructure and varying compliance frameworks continue slowing deployment standardization across cross-border trade environments. Companies are responding through localized managed EDI services, regional data hosting expansion, and modular integration offerings tailored for evolving tax reporting requirements.

Brazil Market Outlook: Brazil represents the largest regional market due to its advanced electronic invoicing ecosystem and extensive industrial distribution network. More than 62% of enterprise procurement workflows in large retail and manufacturing organizations incorporated automated digital transaction management by 2026. Brazilian companies are prioritizing localized compliance integration, logistics coordination automation, and cloud-based supplier communication systems to improve operational visibility and reduce administrative processing inefficiencies across domestic and export-oriented supply chains.

Infrastructure Modernization Supports Digital Trade Expansion

Middle East & Africa is strengthening its position through infrastructure modernization, logistics digitization, and government-led smart trade initiatives. Gulf countries are rapidly integrating EDI systems into customs processing, freight coordination, and healthcare procurement networks to improve operational transparency and trade efficiency. In 2026, digital transaction management deployment across regional logistics hubs increased by nearly 31%, supported by port modernization investments and expanding cloud infrastructure capacity. South Africa and the United Arab Emirates are emerging as key deployment centers due to advanced logistics ecosystems and enterprise digitalization strategies. Technology providers are forming partnerships with regional telecom and cloud infrastructure firms to improve integration scalability and transaction security.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional deployment activity through advanced logistics infrastructure, free-trade zone expansion, and aggressive smart government transformation programs. Nearly 57% of large logistics and trade-focused enterprises integrated automated electronic transaction systems into customs and procurement workflows by 2026. UAE-based organizations are investing in cloud interoperability, multilingual transaction management, and AI-assisted compliance monitoring to strengthen regional trade coordination and accelerate cross-border shipment processing efficiency.

The Electronic Data Interchange (EDI) Software Market is dominated by competition between global enterprise integration leaders such as IBM, OpenText, SPS Commerce, TrueCommerce, and Cleo, alongside regional managed-service specialists and cloud-native interoperability providers. The top five players collectively control approximately 48% of market activity through large-scale enterprise contracts, integrated supply-chain ecosystems, and long-term compliance infrastructure relationships. Competition increasingly centers on transaction speed, AI-assisted automation, cybersecurity resilience, and onboarding efficiency, with cloud-native platforms reducing deployment timelines by nearly 35% compared to legacy integration frameworks. Vendors are expanding through ERP partnerships, logistics software alliances, and industry-specific compliance modules targeting healthcare, automotive, and retail procurement networks. A major competitive shift involves API-EDI convergence, where technology innovators are displacing slower VAN-based environments with scalable real-time integration architectures. High switching costs, regulatory complexity, and interoperability requirements remain major entry barriers. Winning requires scalable cloud infrastructure, deep enterprise integration capability, advanced security controls, and faster multi-partner deployment execution.

IBM

OpenText

SPS Commerce

TrueCommerce

Cleo

MuleSoft

Epicor Software Corporation

Babelway

Boomi

Comarch

Data Masons

SEEBURGER

DiCentral

Jitterbit

Cloud-native EDI platforms, API-integrated transaction orchestration, and AI-assisted validation engines are redefining enterprise B2B communication infrastructure. In 2026, nearly 64% of large enterprises operated hybrid API-EDI environments to improve supplier synchronization and real-time procurement visibility. Automated transaction reconciliation reduced manual processing workloads by approximately 34%, while cloud deployment models lowered infrastructure maintenance costs by nearly 29% compared to traditional on-premises frameworks. Retail, healthcare, and automotive companies are consolidating fragmented supplier communication systems into centralized interoperability platforms to accelerate onboarding speed and improve operational continuity across multi-country trade networks.

Emerging technologies including AI-driven exception management, predictive transaction analytics, and embedded compliance automation are improving workflow responsiveness and reducing processing delays by approximately 27%. API-enabled EDI ecosystems process supplier onboarding nearly 45% faster than legacy VAN-based environments, creating measurable advantages in logistics coordination and inventory synchronization. Germany and the United States are leading enterprise-scale deployments, while India and Mexico are rapidly expanding cloud-based procurement integration among export-focused manufacturers and third-party logistics providers.

Between 2026 and 2028, competitive differentiation will increasingly depend on intelligent automation, cybersecurity resilience, and interoperability scalability. Vendors integrating AI-assisted mapping, real-time anomaly detection, and autonomous compliance validation into EDI platforms are expected to secure stronger enterprise retention, faster transaction execution, and lower operational disruption across digitally interconnected supply-chain ecosystems.

December 2024 – Cleo released an upgraded Cleo Integration Cloud platform featuring procurement automation and supplier relationship management enhancements supporting over 4,000 global enterprises. The release strengthened real-time supply-chain orchestration efficiency and accelerated enterprise transaction visibility across manufacturing and logistics environments. Source: cleo.com

May 2025 – SPS Commerce launched its Manufacturing Supply Chain Performance Suite, expanding full-service EDI capabilities for manufacturers and co-packers. The solution improved procurement coordination and operational continuity while supporting modernized supplier collaboration workflows across complex industrial production networks. Source: spscommerce.com

November 2025 – OpenText reported 19 consecutive quarters of cloud organic growth, with cloud revenue increasing 6.0% year-over-year through expanded enterprise information management and AI-enabled integration services. The development reinforced large-enterprise migration toward scalable cloud-based EDI and compliance automation infrastructure. Source: opentext.com

May 2026 – OpenText announced 29.6% growth in quarterly enterprise cloud bookings alongside expanded enterprise AI and secure data integration initiatives. The operational shift strengthened cloud interoperability adoption and accelerated modernization of enterprise-grade digital trade and transaction management ecosystems globally. Source: opentext.com

The Electronic Data Interchange (EDI) Software Market report delivers comprehensive analysis across Cloud-Based EDI, On-Premises EDI, Web EDI, Mobile EDI, and Managed EDI Services, covering enterprise deployment patterns, interoperability trends, and transaction automation strategies between 2026 and 2033. The study evaluates operational adoption across Supply Chain Management, Invoice Management, Logistics Management, Inventory Management, and Order Processing applications, with manufacturing and logistics sectors representing over 55% of enterprise deployment concentration in 2026.

The report provides region-wise assessment across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, cloud integration acceleration, and regulatory digitization trends shaping enterprise procurement ecosystems. It also analyzes AI-assisted transaction management, API-EDI convergence, cybersecurity frameworks, and predictive analytics integration influencing operational efficiency and competitive positioning. Strategic insights support vendor benchmarking, expansion planning, partnership evaluation, procurement transformation, and long-term digital trade infrastructure investment decisions across global enterprise supply-chain networks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2600 Million |

|

Market Revenue in 2033 |

USD 5334.72 Million |

|

CAGR (2026 - 2033) |

9.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, OpenText, SPS Commerce, TrueCommerce, Cleo, MuleSoft, Epicor Software Corporation, Babelway, Boomi, Comarch, Data Masons, SEEBURGER, DiCentral, Jitterbit |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |