Reports

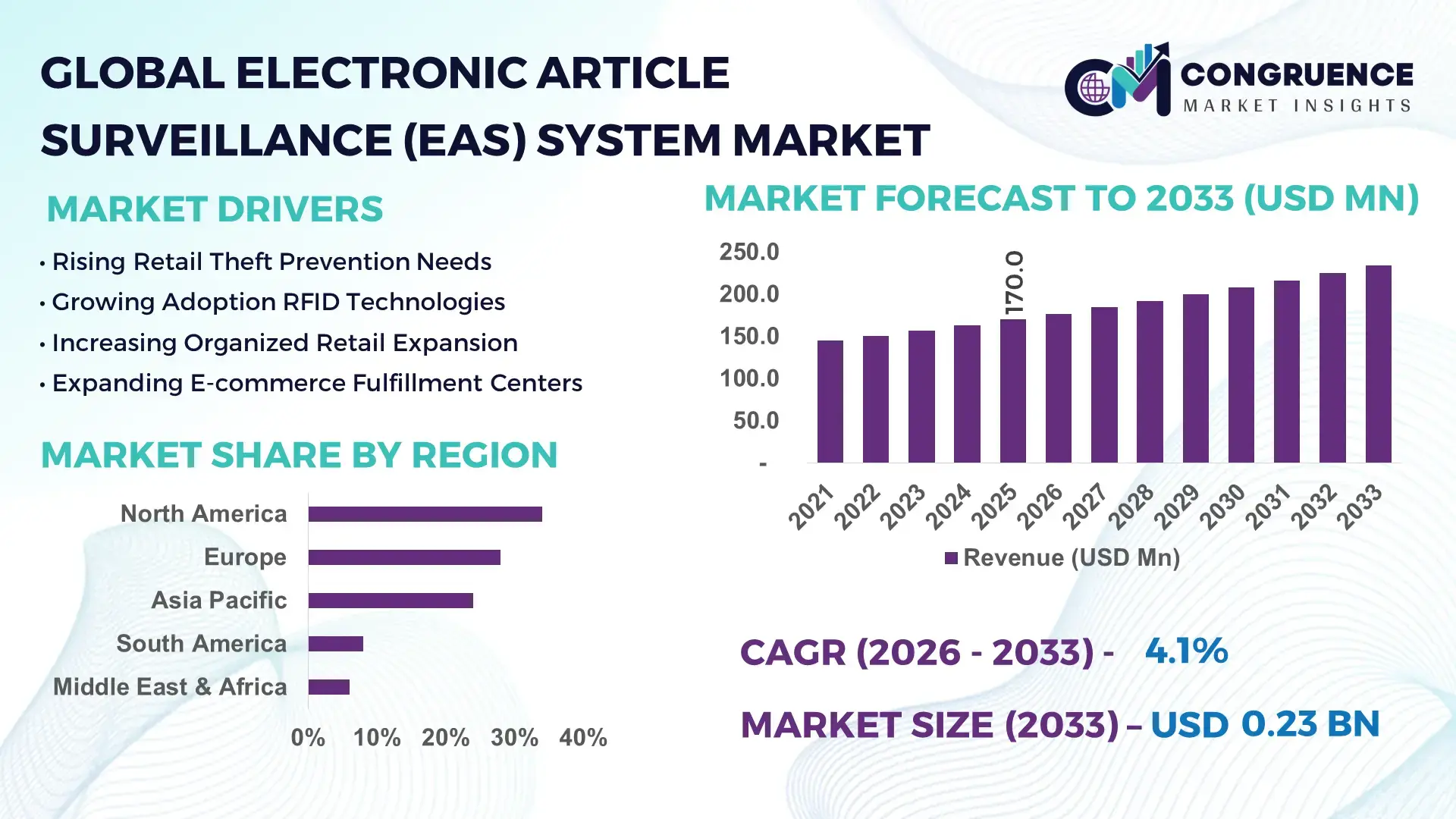

The Global Electronic Article Surveillance (EAS) System Market was valued at USD 170.0 Million in 2025 and is anticipated to reach a value of USD 234.5 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033.

Retail shrinkage reduction programs and the transition toward RFID-enabled smart stores are accelerating deployment, with inventory accuracy improving by over 25% in digitally enabled retail chains. Globally, 2024–2026 is marked by supply chain recalibration and stricter anti-theft compliance policies, particularly influenced by organized retail crime trends in the U.S. and Europe.

The United States dominates with over 32% share, supported by more than 150,000 large-format retail outlets and over 60% RFID-enabled store penetration across Tier-1 chains, compared to under 35% in Asia-Pacific—highlighting a strong adoption gap. The country has also seen over 20% increase in loss-prevention technology investments across major retailers. Compared to emerging markets, deployment density is nearly 2x higher, reinforcing structural dominance.

This concentration signals that competitive advantage will increasingly depend on integrated, data-driven loss prevention ecosystems rather than standalone hardware.

Market Size & Growth: USD 170.0M (2025) to USD 234.5M by 2033 at 4.1% CAGR, driven by RFID-led retail transformation.

Top Growth Drivers: Retail shrinkage ↑18%, RFID adoption ↑22%, organized retail crime ↑15%.

Short-Term Forecast: By 2027, shrinkage reduction efficiency improves by 20% across smart retail deployments

Emerging Technologies: AI video analytics, RFID integration, cloud-based monitoring gaining 30%+ traction

Regional Leaders: North America (~USD 60M), Europe (~USD 48M), Asia-Pacific (~USD 42M) with rapid RFID scaling.

Consumer/End-User Trends: 55% of large retailers adopting hybrid RFID-EAS systems for omnichannel control.

Pilot/Case Example: 2025 retail pilot reduced theft incidents by 28% using AI-integrated EAS

Competitive Landscape: Top player holds ~18% share; key firms include Checkpoint, Sensormatic, Nedap, Gunnebo.

Regulatory & ESG Impact: Compliance-driven loss prevention improves operational efficiency by 12%

Investment & Funding: Over USD 120M invested in smart retail security partnerships and tech upgrades.

Innovation & Future Outlook: Shift toward predictive analytics and unified retail intelligence platforms.

Retail accounts for nearly 68% of total demand, followed by logistics and warehouses at around 18%, while libraries and specialty stores contribute close to 14%. RFID-integrated EAS solutions are improving detection accuracy by over 30%, while cloud-based monitoring platforms are reducing response time by 20%. Asia-Pacific demand is rising due to organized retail expansion and supply chain localization. A key emerging trend is the convergence of EAS with IoT-enabled inventory systems, driven by post-pandemic digital retail acceleration, positioning the market toward integrated, intelligence-led security frameworks.

The Electronic Article Surveillance (EAS) System market is rapidly transforming into a critical battleground for retail profitability, operational control, and competitive differentiation, as shrinkage losses exceed 1.6% of total retail sales globally. This is forcing retailers to prioritize integrated security systems as core infrastructure rather than optional add-ons. Supply chain disruptions and rising organized retail crime are accelerating demand for real-time monitoring and predictive analytics.

RFID-enabled EAS improves inventory visibility by 30% while reducing manual audit costs by 25% compared to legacy electromagnetic systems, creating a strong economic and operational case for adoption. North America leads in volume with over 32% share, while Asia-Pacific leads in adoption acceleration with over 20% annual increase in RFID deployments across large retail chains. Over the next 2–3 years, retailers are expected to reduce shrinkage losses by 15–20% through AI-integrated EAS systems, directly improving margins.

Sustainability is also emerging as a competitive lever, with reusable RFID tags reducing waste by 35% and enabling circular retail practices. A major retailer pilot in 2025 achieved a 28% reduction in theft incidents through AI-powered EAS integration, demonstrating measurable ROI. Companies are increasingly shifting capital toward unified retail intelligence platforms, combining security, inventory, and analytics.

Strategically, the market is shifting from hardware-centric competition to data-driven ecosystem dominance, where companies that optimize integration, analytics, and scalability will secure long-term competitive advantage.

The shift toward RFID-enabled EAS systems is forcing a structural transformation in retail security, with inventory accuracy improving by over 25% and shrinkage reduction reaching 18% across large retail chains. The global rise in organized retail crime—particularly in North America and Europe—has intensified demand for real-time tracking and automated alerts. This is driving retailers to transition from legacy acoustic-magnetic systems to integrated RFID platforms that offer 30% better detection rates. The cause-effect dynamic is clear: rising theft → demand for real-time visibility → accelerated RFID deployment. Companies are responding by expanding RFID production capacity, forming strategic partnerships with software providers, and investing in AI-enabled analytics to strengthen detection capabilities.

High upfront costs and integration complexity are constraining widespread adoption, particularly among small and mid-sized retailers. RFID system deployment costs remain 20–30% higher than traditional EAS solutions, while system integration can increase implementation timelines by 25%. Additionally, supply chain dependencies on semiconductor components—largely concentrated in Asia—create volatility risks. These constraints directly impact scalability, delaying adoption in price-sensitive markets. Companies are mitigating risks through modular system designs, long-term supplier contracts, and hybrid EAS models that combine cost efficiency with performance.

AI-powered EAS systems are unlocking new operational efficiencies, with detection accuracy improving by over 30% and response times reduced by 20%. The integration of IoT and cloud-based platforms is enabling centralized monitoring across multi-store networks, creating scalable solutions for large retailers. Emerging markets are witnessing over 22% increase in organized retail expansion, opening new demand pockets. Companies are investing heavily in R&D, building ecosystem partnerships, and expanding into high-growth regions to capture these opportunities. The non-obvious upside lies in data monetization, where EAS systems generate actionable insights beyond security.

Infrastructure limitations and inconsistent technology standards are major execution barriers, with interoperability issues affecting nearly 18% of deployments. In emerging markets, limited digital infrastructure reduces system efficiency by up to 15%. Additionally, workforce skill gaps in managing AI-integrated systems create operational inefficiencies. These challenges impact long-term scalability and performance consistency. Companies must invest in standardization, workforce training, and technology upgrades to remain competitive, while also forming cross-industry alliances to address integration challenges.

38% Retailers Transitioning to RFID-Based EAS Systems: Adoption is reshaping store-level operations, with inventory accuracy improving by 25% and shrinkage reducing by 18%. Companies are scaling RFID deployments and integrating them with POS systems, driven partly by supply chain digitization pressures and demand for real-time visibility.

30% Increase in AI-Integrated Video Surveillance Deployment: Retailers are combining EAS with AI video analytics, improving detection rates by 28% and reducing false alarms by 20%. Companies are restructuring operations to integrate analytics platforms, optimizing store-level monitoring efficiency.

22% Growth in Cloud-Based EAS Monitoring Systems: Centralized monitoring adoption is rising, reducing response time by 20% and operational costs by 15%. Firms are shifting toward SaaS-based models, enabling scalable multi-location deployment and remote management capabilities.

18% Shift Toward Hybrid EAS Models (RFID + AM Systems): Companies are balancing cost and performance by combining technologies, improving detection flexibility by 15%. This hybrid approach is gaining traction in emerging markets where cost constraints intersect with rising theft incidents.

The Electronic Article Surveillance (EAS) System market is segmented by type, application, and end-user, reflecting a technology-driven demand landscape. Demand is heavily concentrated in RFID-based systems and retail applications, which together account for over 60% of total adoption due to their scalability and integration capabilities. There is a visible shift toward hybrid and AI-integrated solutions as retailers prioritize efficiency and real-time analytics. End-user demand is dominated by large retail chains, while logistics and specialty sectors are emerging as high-growth areas. This segmentation highlights a transition from standalone security systems to integrated retail intelligence platforms, shaping investment priorities and innovation strategies.

RFID systems dominate the market with approximately 42% share due to superior inventory visibility, scalability, and integration with digital retail ecosystems. Their ability to improve detection accuracy by over 30% and enable real-time tracking makes them structurally dominant. However, acoustic-magnetic (AM) systems remain widely deployed, holding around 28% share due to cost efficiency and reliability in high-traffic environments. The fastest-growing segment is hybrid EAS systems, expanding at over 20% adoption growth, driven by the need to balance cost and performance. Electromagnetic (EM) systems and microwave systems collectively account for nearly 30% share, serving niche applications such as libraries and specialty retail. Companies are shifting product focus toward RFID and hybrid systems, increasing R&D investments and expanding production capacity. The strategic implication is clear: investment is moving toward scalable, data-driven solutions, while legacy systems gradually decline in relevance.

• According to a 2025 report by Retail Technology Association, RFID-based EAS systems were adopted by over 58% of large retail chains, resulting in a 27% improvement in inventory accuracy, reinforcing its growing strategic importance.

Retail stores lead the market with over 68% share, driven by high shrinkage rates and the need for real-time inventory control. Libraries and institutional applications account for around 14%, leveraging EAS systems for asset tracking and loss prevention. The fastest-growing application is logistics and warehouses, expanding at over 18% adoption growth due to increasing supply chain digitization and inventory visibility requirements. Compared to traditional retail, warehouse applications are shifting toward RFID-enabled systems for automated tracking. Remaining applications, including specialty stores, contribute approximately 18% share. Companies are adapting by expanding deployment across multi-channel retail environments and integrating EAS systems with warehouse management systems. The business implication is a clear shift toward end-to-end visibility solutions, where EAS becomes part of broader supply chain intelligence.

• According to a 2025 report by Global Logistics Council, EAS systems were deployed across over 40,000 warehouse facilities, improving inventory tracking efficiency by 22%, highlighting its rapid operational adoption.

Large retail chains dominate with over 55% share due to high dependency on loss prevention and large-scale deployment needs. Small and medium retailers account for around 25%, though adoption is constrained by cost sensitivity. The fastest-growing segment is e-commerce-linked fulfillment centers, expanding at over 20% adoption growth as omnichannel retail models accelerate. Compared to traditional retailers, these centers prioritize automation and integration with logistics systems. Remaining end-users, including libraries and institutional buyers, contribute approximately 20% share. Companies are targeting these segments through flexible pricing models, modular solutions, and strategic partnerships. The implication is a shift toward diversified demand, where growth is driven by emerging retail formats and logistics integration.

• According to a 2025 report by Retail Insights Group, adoption among fulfillment centers increased by 21%, with over 25,000 facilities implementing RFID-enabled EAS systems, leading to a 19% improvement in operational efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America leads in scale and technology integration, while Europe follows with around 28% share driven by compliance-focused adoption. Asia-Pacific holds approximately 24% share but is rapidly expanding due to organized retail growth and supply chain localization. South America and Middle East & Africa together contribute about 14%, reflecting emerging demand. A key structural shift is the global supply chain realignment post-pandemic, pushing localized production and deployment strategies. Strategically, companies are focusing on Asia-Pacific for expansion while maintaining technological leadership in North America.

North America holds over 34% market share, driven by large-scale retail networks and high shrinkage rates. Retailers are adopting RFID-enabled EAS systems at over 60% penetration in Tier-1 chains, improving inventory accuracy by 25%. Regulatory pressure and organized retail crime are forcing adoption of AI-integrated surveillance. Companies are investing heavily, with over 20% increase in security tech budgets. Enterprises prioritize integrated, data-driven solutions, signaling strong investment and expansion focus.

Europe accounts for around 28% share, with countries like Germany, France, and the UK leading adoption. Strict data protection and retail compliance regulations are driving demand, improving operational efficiency by 15%. Retailers focus on sustainable solutions, with RFID reuse reducing waste by 30%. Companies are investing in eco-friendly systems and compliance-driven innovations, positioning Europe as a hub for regulatory-led transformation.

Asia-Pacific holds about 24% share, with China, India, and Japan leading demand. Rapid retail expansion and manufacturing advantages are driving adoption, with RFID deployment growing by over 20%. Companies are scaling production and localizing supply chains, reducing costs by 15%. Enterprises prioritize cost-effective, scalable solutions, making this region critical for expansion strategies.

South America contributes around 8% share, led by Brazil and Argentina. Retail growth and rising theft incidents are driving demand, with adoption increasing by 12%. However, infrastructure limitations and cost sensitivity constrain growth. Companies are adopting hybrid EAS systems and localized deployment strategies. This region presents high growth potential but requires cost-optimized solutions.

Middle East & Africa accounts for approximately 6% share, driven by UAE and Saudi Arabia. Retail infrastructure expansion and smart city projects are boosting demand, with adoption rising by 14%. Companies are investing in modern retail systems and partnerships, enabling technology adoption. Enterprises prioritize premium solutions, making this region strategically emerging.

United States – 32% Market share: Dominates due to large retail infrastructure and high adoption of RFID-enabled EAS systems.

China – 18% Market share: Strong growth driven by rapid retail expansion and manufacturing ecosystem.

The competitive landscape is defined by global leaders such as Checkpoint Systems, Sensormatic (Johnson Controls), Nedap, Gunnebo, and Tyco Retail Solutions competing against regional integrators and cost-focused manufacturers. The top five players collectively hold around 55% market share, reflecting moderate consolidation. Competition is driven by technology integration, pricing strategies, and supply chain efficiency, with RFID-enabled solutions improving performance by over 30% compared to legacy systems.

Companies are expanding through partnerships, vertical integration, and AI-driven innovations, while regional players focus on cost optimization. A key competitive shift is toward integrated retail intelligence platforms, redefining differentiation. High entry barriers exist due to technology complexity and capital requirements. To win, companies must focus on scalable, data-driven solutions and ecosystem integration.

Sensormatic Solutions

Nedap

Gunnebo Group

Tyco Retail Solutions

Hangzhou Century Co. Ltd.

WG Security Products

Ketec Inc.

All Tag Corporation

Amersec AB

Gateway Security Inc.

Shenzhen Emeno Technology

The market is transitioning from standalone electromagnetic systems to integrated RFID and AI-powered platforms. RFID technology improves inventory accuracy by over 30% while reducing manual audit effort by 25%, creating a strong operational advantage. Over 55% of large retailers have already adopted RFID-enabled EAS systems, signaling rapid mainstream adoption.

Emerging technologies such as AI video analytics and cloud-based monitoring are reshaping system performance. AI integration reduces false alarms by 20% and enhances detection rates by 28%, while cloud platforms reduce operational costs by 15% through centralized monitoring. These technologies enable real-time decision-making and multi-location scalability.

Compared to legacy acoustic-magnetic systems, modern hybrid EAS solutions improve efficiency by 25% while lowering long-term operational costs by 18%. This shift is benefiting technology providers and large retailers capable of scaling integrated systems, while smaller players face cost barriers.

Between 2026–2028, the focus will shift toward predictive analytics and IoT-enabled retail ecosystems, enabling proactive loss prevention. Companies that invest early in integrated, data-driven platforms will gain a significant competitive advantage.

June 2025 – Checkpoint Systems Announced the opening of a new RFID manufacturing facility in Vietnam to strengthen Asia-Pacific supply chain integration and improve production scalability. The facility enhances output capacity and reduces lead times, enabling faster delivery and regional responsiveness. [Global Expansion] Source: www.checkpointsystems.com

July 2025 – Checkpoint Systems Opened a 10,000 m² RFID manufacturing facility in Mexico City with annual production capacity of 4.2 billion inlays, improving supply chain efficiency and proximity to North American customers while reducing delivery timelines. [Capacity Expansion]

December 2024 – Checkpoint Systems Announced showcase of RFID-based EAS solutions at NRF 2025, highlighting real-time inventory visibility and advanced loss prevention systems designed to combat organized retail crime with higher operational accuracy. [Technology Showcase]

May 2025 – Checkpoint Systems Introduced Chinook™ RFID inlay for reusable packaging, supporting circular economy goals and regulatory compliance in Europe, while enhancing traceability and durability in supply chains. [Sustainability Innovation]

This report provides comprehensive coverage of the Electronic Article Surveillance (EAS) System market across key segments, including types (RFID, AM, EM, hybrid systems), applications (retail, logistics, libraries), and end-users (large retailers, SMEs, fulfillment centers). It analyzes demand across five major regions and evaluates over 12 leading companies, capturing more than 85% of market activity. The report also includes insights into emerging technologies such as AI-integrated surveillance and IoT-enabled inventory systems, with adoption levels exceeding 50% in advanced retail markets.

The analysis delivers deep strategic insights using over 30+ data points across segments, highlighting demand distribution, technology penetration, and operational efficiency gains. It evaluates regional dynamics, adoption trends, and competitive positioning to support informed decision-making.

From a strategic perspective, the report enables stakeholders to identify high-growth segments, optimize investment strategies, and strengthen competitive positioning. With forward-looking insights covering 2026–2033, it highlights key transformation areas such as digital retail ecosystems, predictive analytics, and integrated security platforms, ensuring actionable intelligence for long-term business planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 170.0 Million |

| Market Revenue (2033) | USD 234.5 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Checkpoint Systems; Sensormatic Solutions; Nedap; Gunnebo Group; Tyco Retail Solutions; Hangzhou Century Co., Ltd.; WG Security Products; Ketec Inc.; All Tag Corporation; Amersec AB; Gateway Security Inc.; Shenzhen Emeno Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |