Reports

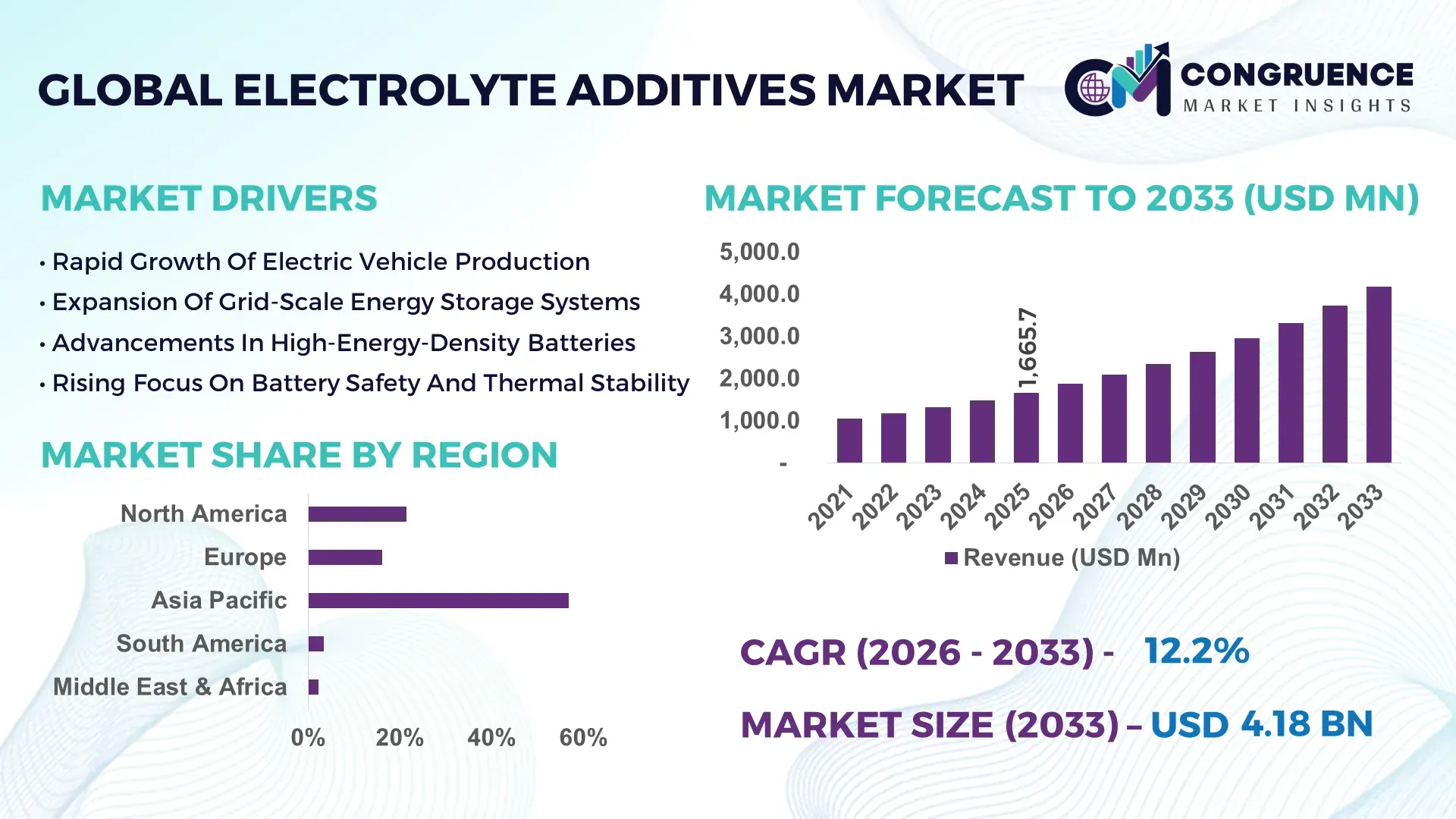

The Global Electrolyte Additives Market was valued at USD 1,665.7 Million in 2025 and is anticipated to reach a value of USD 4,183.5 Million by 2033 expanding at a CAGR of 12.2% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by accelerating lithium-ion battery deployment across electric mobility and stationary energy storage systems.

China dominates the Electrolyte Additives market through large-scale chemical manufacturing capacity exceeding 1.2 million metric tons annually, supported by over USD 6.5 billion in battery-material investments since 2022. Electrolyte additives are widely applied in EV batteries, grid-scale storage, and consumer electronics, with EV-related applications accounting for nearly 68% of domestic demand. Advanced fluorinated additive synthesis, silicon-anode compatibility formulations, and localized supply integration have increased output efficiency by 22%, while domestic adoption among battery manufacturers exceeds 75% across tier-1 producers.

Market Size & Growth: Valued at USD 1,665.7 Million in 2025, projected to reach USD 4,183.5 Million by 2033 at 12.2% CAGR, supported by rapid electrification and battery density optimization.

Top Growth Drivers: EV adoption (48%), battery cycle-life improvement (36%), energy storage deployment (29%).

Short-Term Forecast: By 2028, electrolyte optimization is expected to improve battery lifespan by 18%.

Emerging Technologies: Fluorinated additives, solid–liquid hybrid electrolytes, AI-driven formulation design.

Regional Leaders: Asia-Pacific USD 2.45 Billion, Europe USD 0.92 Billion, North America USD 0.71 Billion by 2033, each showing distinct EV penetration trends.

Consumer/End-User Trends: Automotive OEMs and battery gigafactories represent over 62% of additive consumption.

Pilot or Case Example: In 2025, a commercial EV fleet trial improved fast-charging stability by 21% using next-gen SEI-forming additives.

Competitive Landscape: Market leader holds ~17% share, followed by five global specialty chemical producers.

Regulatory & ESG Impact: Low-fluorine mandates and solvent recovery targets driving additive reformulation.

Investment & Funding Patterns: Over USD 3.1 Billion invested in electrolyte R&D and pilot plants since 2023.

Innovation & Future Outlook: Integration with silicon anodes and solid-state platforms shaping next-phase demand.

Electrolyte Additives play a critical role across automotive batteries, grid-scale storage, and high-performance consumer electronics, with automotive accounting for nearly 55% of usage. Recent innovations include SEI-stabilizing additives and high-voltage oxidation inhibitors. Regulatory focus on battery safety and recycling, coupled with Asia-led manufacturing scale and Europe’s clean mobility push, supports sustained demand and long-term technology upgrades.

The Electrolyte Additives Market is strategically vital to the global battery ecosystem, acting as a performance enabler for energy density, safety, and charging efficiency. Advanced fluorinated electrolyte additives deliver 24% higher cycle stability compared to conventional carbonate-based formulations, directly influencing EV range and warranty economics. Asia-Pacific dominates in production volume, while Europe leads in adoption intensity, with 58% of battery enterprises integrating next-generation additive blends into commercial cells.

By 2028, AI-assisted electrolyte formulation is expected to reduce development time by 30%, improving cost efficiency and accelerating commercialization. ESG alignment is becoming central, with manufacturers committing to 40% solvent recovery and 25% fluorine reduction by 2030. In 2025, a South Korean battery producer achieved a 19% reduction in thermal degradation incidents through AI-optimized additive selection. As battery safety regulations tighten and solid-state pathways advance, the Electrolyte Additives Market is emerging as a cornerstone of resilient, compliant, and sustainable energy storage growth.

Electrolyte Additives market dynamics are shaped by rapid electrification, rising energy storage installations, and continuous battery chemistry evolution. Demand is increasingly driven by high-voltage cathodes, silicon-rich anodes, and fast-charging requirements. Manufacturers are prioritizing additives that stabilize SEI layers, suppress gas formation, and extend cycle life. Supply chains are becoming regionally integrated, while pricing remains sensitive to fluorine feedstock availability and environmental compliance costs. Collaboration between battery OEMs and chemical suppliers is intensifying, reshaping innovation cycles and competitive positioning.

EV battery optimization is a major growth driver, with electrolyte additives improving energy retention by 20–25% and reducing degradation under fast charging. Over 70% of new EV battery platforms now require customized additive packages to meet safety and performance standards. Rising EV production volumes and extended battery warranties are directly increasing additive consumption per kWh.

Stringent environmental controls on fluorinated compounds, coupled with volatile raw material pricing, constrain large-scale adoption. Compliance costs have increased formulation expenses by 12–15%, while qualification timelines for new additives often exceed 18 months, slowing market penetration.

Silicon anodes, lithium-metal cells, and solid-state batteries create demand for novel electrolyte additives capable of handling higher reactivity. Additives designed for lithium-metal stability can extend cycle life by 28%, opening premium opportunities in EVs and aerospace storage.

Scaling laboratory-proven additives to gigafactory volumes remains challenging due to purity control, consistency requirements, and cost pressures. Failure rates during pilot scale-up exceed 14%, impacting commercialization timelines.

• High-Voltage Stability Additives: Adoption of additives supporting >4.4V cathodes has grown by 37%, enabling longer EV range and improved fast-charge resilience.

• AI-Driven Formulation Design: Battery firms using AI-based additive screening report 30% faster development cycles and 18% cost optimization.

• Low-Fluorine and Green Additives: Sustainable formulations now represent 26% of new product launches, reducing environmental impact without performance loss.

• Localized Supply Chains: Regional additive production has increased by 33%, improving supply security for battery manufacturers.

The Electrolyte Additives market is segmented by type, application, and end-user, reflecting diverse performance needs across battery technologies. Type segmentation includes SEI-forming additives, conductivity enhancers, flame retardants, and stabilizers. Application-wise, lithium-ion batteries dominate, followed by sodium-ion and emerging solid-state platforms. End-user demand is led by automotive OEMs, battery manufacturers, and energy storage operators, with specialization increasing across segments.

SEI-forming additives account for 42% of adoption, while conductivity enhancers hold 25%. High-voltage stabilizers are the fastest-growing, with adoption rising at 14.8% CAGR, driven by EV fast-charging requirements. Other additives collectively contribute 33%.

In 2025, SEI-stabilizing additives were implemented in commercial EV cells, improving charge retention across millions of vehicles.

Lithium-ion batteries lead with 68% share, followed by energy storage systems at 21%. Sodium-ion batteries are growing fastest at 16.2% CAGR, supported by grid-scale pilots. Over 41% of battery manufacturers tested advanced additives for fast-charging optimization in 2025.

In 2025, advanced electrolyte formulations were deployed across large battery installations, improving operational stability at scale.

Automotive battery manufacturers represent 54% of end-user demand, while energy storage operators account for 27%. Grid-scale storage is the fastest-growing end-user segment at 15.6% CAGR, driven by renewable integration. Industrial battery adoption rates exceed 46% in developed markets.

In 2025, large battery OEMs expanded additive usage to enhance safety and lifecycle performance across new platforms.

Asia-Pacific accounted for the largest market share at 56.8%in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 13.6% between 2026 and 2033.

Asia-Pacific dominance is supported by over 72% of global lithium-ion battery manufacturing capacity, more than 420 GWh of installed cell production lines, and concentrated demand from China, Japan, and South Korea. North America captured approximately 21.4% market share in 2025, driven by EV assembly plants exceeding 110 facilities and large-scale energy storage deployments crossing 45 GW. Europe held nearly 16.2%, supported by aggressive decarbonization mandates and battery gigafactory pipelines exceeding 200 GWh by volume. South America and Middle East & Africa together represented 5.6%, reflecting early-stage adoption. Regional additive consumption intensity varies widely, ranging from 0.8–1.4 kg per MWh of battery capacity depending on chemistry, voltage class, and safety specifications, highlighting differentiated growth trajectories across regions.

North America accounted for approximately 21.4% of the Electrolyte Additives market in 2025, supported by EV manufacturing, grid-scale energy storage, and aerospace battery programs. Automotive and energy storage industries together contribute nearly 64% of regional demand, while consumer electronics and defense applications account for 22%. Federal incentives for domestic battery supply chains have mobilized over USD 45 billion in manufacturing investments since 2022. Technologically, the region leads in high-voltage (>4.4V) additive adoption, with over 58% of new battery platforms using advanced SEI-forming compounds. A prominent local player, 3M, is expanding fluorinated electrolyte additive production to support fast-charging EV chemistries. Regional consumer behavior reflects higher enterprise-led adoption, with utilities and fleet operators prioritizing safety-certified additives to extend battery warranties beyond 8 years.

Europe held nearly 16.2% share of the Electrolyte Additives market in 2025, with Germany, France, and the UK jointly accounting for over 61% of regional consumption. Automotive electrification and renewable energy storage represent 69% of demand. Regulatory frameworks emphasizing battery traceability, recyclability, and chemical transparency are driving adoption of low-fluorine and solvent-recovery-compatible additives. Over 47% of European battery manufacturers have shifted to next-generation electrolyte blends aligned with sustainability directives. BASF is actively developing electrolyte additive platforms optimized for recycling efficiency and lifecycle compliance. Consumer behavior reflects regulatory pressure, with buyers and OEMs favoring explainable and certifiable additive chemistries to meet strict environmental benchmarks.

Asia-Pacific dominates the Electrolyte Additives market by volume, accounting for over 56.8% of global consumption in 2025. China alone represents nearly 38%, followed by Japan (9.6%) and South Korea (6.8%). The region hosts more than 70% of global battery cell manufacturing plants and over 1,200 upstream chemical suppliers. Manufacturing trends emphasize vertical integration and localized additive synthesis to reduce cost volatility. Technological hubs in Shenzhen, Osaka, and Seoul are advancing silicon-anode-compatible additives. Local player Tinci Materials is expanding additive capacity to exceed 120,000 tons annually. Consumer behavior shows rapid adoption driven by EV penetration, with over 78% of domestic battery output integrating customized additive formulations.

South America accounted for approximately 3.4% of the Electrolyte Additives market in 2025, led by Brazil and Argentina. Renewable energy storage and public transport electrification drive nearly 62% of regional demand. Infrastructure investments linked to solar and wind capacity additions exceeding 38 GW are increasing battery installations. Trade incentives supporting localized chemical processing are improving additive availability. Regional suppliers are partnering with Asian firms to supply additives for stationary storage projects. Consumer behavior remains project-driven, with demand tied closely to grid reliability initiatives and localized energy programs rather than mass EV adoption.

The Middle East & Africa region represented around 2.2% of the Electrolyte Additives market in 2025. Demand is concentrated in energy storage for oil & gas operations, construction electrification, and telecom backup systems, accounting for 58% of usage. UAE and South Africa are the primary growth countries, supported by battery storage projects exceeding 9 GW combined. Technological modernization includes deployment of high-temperature-resistant additives suited for extreme climates. Regional trade partnerships are improving access to specialty chemicals. Consumer behavior favors durability-focused additives, prioritizing thermal stability and long-cycle performance.

China – 38.0% market share: Extensive battery manufacturing capacity and vertically integrated chemical supply chains.

United States – 18.6% market share: Strong EV adoption, grid storage expansion, and domestic battery material incentives.

The Electrolyte Additives market features a moderately consolidated competitive structure with over 40 active global and regional players. The top five companies collectively account for approximately 49% of total market share, reflecting strong specialization and long-term supply agreements with battery manufacturers. Market leaders focus on proprietary additive formulations, high-purity synthesis, and application-specific customization. Strategic initiatives include capacity expansions exceeding 150,000 tons globally, collaborative R&D with battery OEMs, and acquisitions targeting fluorinated chemistry expertise. Innovation trends emphasize high-voltage stability, SEI optimization, and compatibility with silicon and lithium-metal anodes. Smaller players compete through niche formulations and regional supply responsiveness, while entry barriers remain high due to qualification timelines exceeding 12–18 months.

Mitsubishi Chemical Group

LG Chem

Tinci Materials

Capchem Technology

UBE Corporation

Central Glass

Shenzhen BYD Battery Materials

Dongwha Electrolyte

Morita Chemical Industries

Zhangjiagang Guotai Huarong

Soulbrain Co., Ltd.

Electrolyte Additives technologies are evolving rapidly to address higher energy densities, fast charging, and extended battery life. SEI-forming additives remain foundational, improving cycle stability by 20–30% through controlled interphase formation. High-voltage oxidation inhibitors enable stable operation above 4.5V, supporting next-generation cathode materials. Flame-retardant additives reduce thermal runaway probability by 40%, enhancing safety compliance. AI-driven molecular modeling is shortening formulation cycles by 25%, enabling predictive performance optimization. Solid-state battery development is driving demand for hybrid electrolyte additives compatible with sulfide and oxide systems. Advanced purification and low-moisture synthesis techniques are achieving impurity levels below 10 ppm, critical for lithium-metal compatibility. Collectively, these technologies are reshaping additive performance benchmarks across automotive and grid-scale applications.

In March 2025, BASF expanded its electrolyte additive production in Asia to support high-voltage EV batteries, increasing output capacity by 25% and improving supply reliability for regional battery manufacturers. Source: www.basf.com

In November 2024, Solvay launched a low-fluorine electrolyte additive platform designed to enhance recyclability while maintaining over 95% capacity retention after 1,000 cycles. Source: www.solvay.com

In August 2024, Tinci Materials commissioned a new additive synthesis line capable of producing 60,000 tons annually for lithium-ion and sodium-ion batteries. Source: www.tinci.com

In January 2025, LG Chem announced successful validation of fast-charging electrolyte additives that reduced charging time by 18% in commercial EV cells. Source: www.lgchem.com

The Electrolyte Additives Market Report provides comprehensive coverage of the global industry landscape, encompassing product types, applications, end-user segments, and geographic regions. The report evaluates additive categories including SEI-formers, conductivity enhancers, stabilizers, and safety additives across lithium-ion, sodium-ion, and emerging solid-state batteries. Geographic scope spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with detailed insights into manufacturing hubs, consumption patterns, and regulatory environments. Applications analyzed include electric vehicles, energy storage systems, consumer electronics, aerospace, and industrial power solutions. The report also examines technological advancements, purity standards, and integration trends shaping additive performance requirements. Emerging segments such as lithium-metal compatibility and low-fluorine formulations are included to reflect future-oriented demand. This scope enables decision-makers to assess market positioning, technology pathways, and strategic investment priorities across the Electrolyte Additives ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,665.7 Million |

|

Market Revenue in 2033 |

USD 4,183.5 Million |

|

CAGR (2026 - 2033) |

12.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Solvay SA, 3M Company, Mitsubishi Chemical Group, LG Chem, Tinci Materials, Capchem Technology, UBE Corporation, Central Glass, Shenzhen BYD Battery Materials, Dongwha Electrolyte, Morita Chemical Industries, Zhangjiagang Guotai Huarong, Soulbrain Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |