Reports

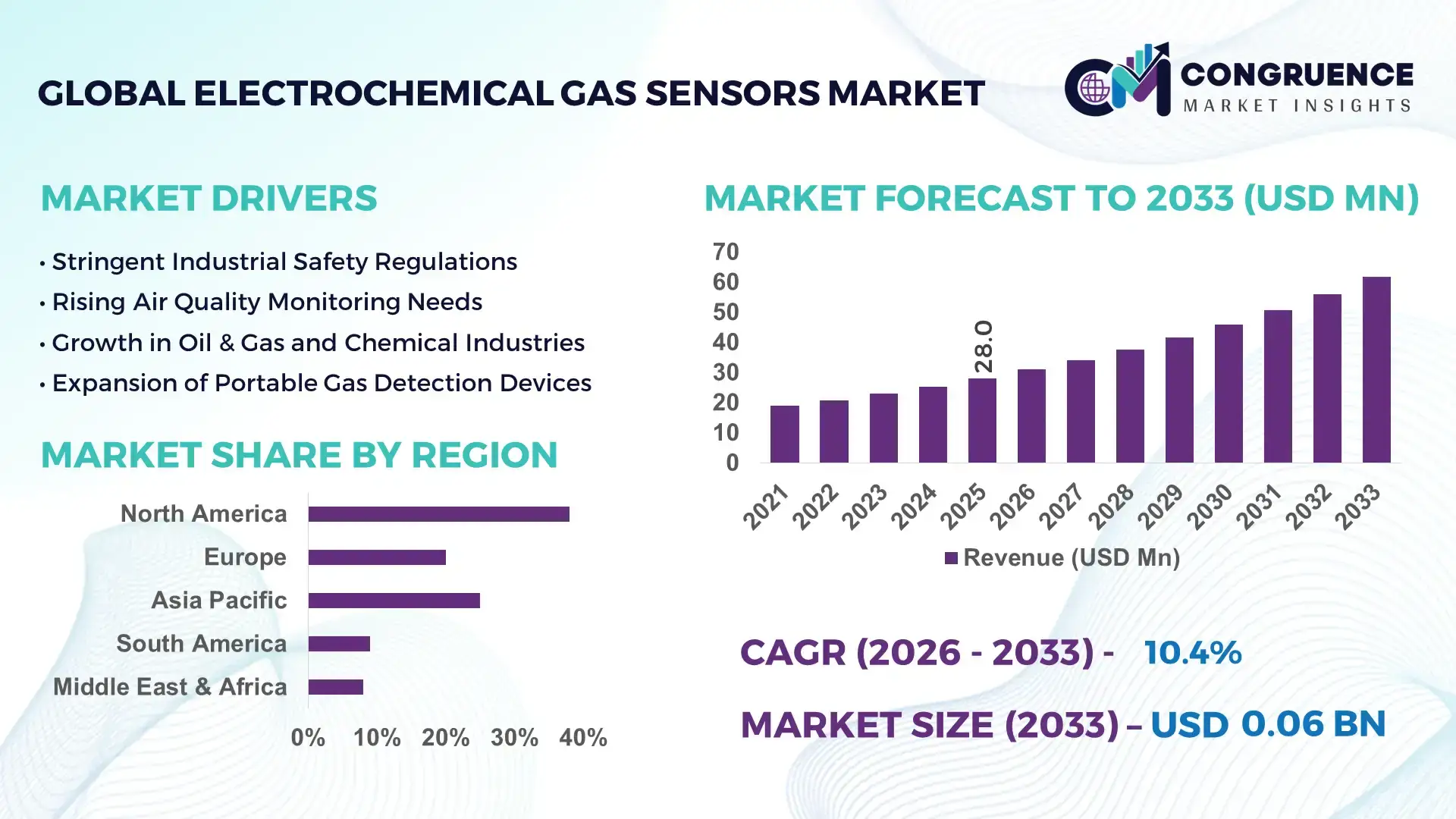

The Global Electrochemical Gas Sensors Market was valued at USD 28.03 Million in 2025 and is anticipated to reach a value of USD 61.86 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. This growth is driven by rising industrial safety mandates and environmental monitoring needs.

In the United States, which leads the global marketplace, production capacity has more than doubled over the past five years with over 15 million units manufactured annually, supported by over USD 120 million in private and public investments in sensor fabrication facilities. U.S. industrial and environmental monitoring applications account for robust adoption, with over 40% of manufacturing plants deploying electrochemical sensors in 2024. Technological advancements such as miniaturized low-power designs and integrated IoT connectivity have further solidified installed bases across utilities, automotive, and building automation sectors.

Market Size & Growth: Valued at ~USD 28.03M in 2025, projected to reach ~USD 61.86M by 2033 at a 10.4% CAGR, propelled by stringent safety regulations and smart infrastructure investments.

Top Growth Drivers: Industrial safety compliance adoption ~48%, environmental monitoring deployments ~35%, IoT-enabled sensor integration ~28%.

Short-Term Forecast: By 2028, expect 22% reduction in average sensor deployment costs and 18% performance gain in sensitivity across key gases.

Emerging Technologies: Solid-state electrolytes, AI-driven calibration algorithms, and enhanced wireless connectivity protocols.

Regional Leaders: North America ~USD 22M by 2033 with high utility uptake; Europe ~USD 18M by 2033 driven by industrial automation; Asia-Pacific ~USD 13M by 2033 with rapid urban air quality monitoring adoption.

Consumer/End-User Trends: Elevated adoption in manufacturing, oil & gas, and smart buildings with real-time analytics integration for proactive safety.

Pilot or Case Example: In 2024, a major refinery pilot achieved a 27% reduction in hazardous exposure incidents through networked electrochemical sensors.

Competitive Landscape: Market leader capturing ~32% share, followed by 3M, Honeywell, Sensirion, Figaro Engineering.

Regulatory & ESG Impact: Tightening workplace exposure limits and ESG reporting mandates accelerate sensor installs.

Investment & Funding Patterns: Over USD 85M in recent venture funding and cross-sector project financing targeting next-gen sensor platforms.

Innovation & Future Outlook: Focused on ultra-low-power MEMS, multi-gas detection arrays, and AI-enabled predictive maintenance integration.

The Electrochemical Gas Sensors Market is characterized by strong contributions from industrial safety, environmental monitoring, and smart infrastructure sectors, with industrial applications accounting for a significant portion of unit installations. Recent innovations include multi-gas microelectrode designs and cloud-connected analytics platforms that enhance detection accuracy and predictive insights. Regulatory drivers such as tightened emissions reporting requirements and workplace safety standards have elevated demand across North America, Europe, and Asia-Pacific. Regional consumption patterns show accelerated growth in urban air quality monitoring programs and oil & gas sector upgrades. The future outlook emphasizes integration with wireless networks and advanced calibration techniques to support broader adoption in transportation, energy, and environmental services.

The strategic relevance of the Electrochemical Gas Sensors Market is anchored in its ability to enable critical safety, environmental compliance, and operational excellence across industrial, commercial, and public infrastructure applications. Electrochemical sensing technologies now deliver up to 35% improvement in detection accuracy compared to older catalytic bead standards, enabling earlier identification of hazardous gases such as CO, NO₂, and H₂S in complex environments. North America dominates in volume, while Europe leads in adoption with over 60% of manufacturing and utilities enterprises deploying smart sensor systems as part of digital transformation strategies.

By 2028, AI-enabled predictive diagnostics are expected to improve system uptime by 25% and reduce false alarms through adaptive calibration models. Firms are committing to measurable ESG improvements such as 40% reduction in workplace exposure incidents by 2030 through integrated gas sensing and automated shutdown protocols. In 2024, a leading refinery in the Gulf Coast achieved a 28% reduction in emergency response events through deployment of networked electrochemical gas sensor arrays combined with real-time analytics.

Strategically, the market is progressing toward tighter integration with IoT ecosystems, edge computing, and predictive maintenance platforms, positioning Electrochemical Gas Sensors as a pillar of resilience, regulatory compliance, and sustainable growth in industrial and environmental monitoring portfolios worldwide.

Industrial automation is a pivotal driver for the Electrochemical Gas Sensors market, as factories and processing plants adopt advanced safety protocols alongside automation technologies. Automated production lines require continuous monitoring of hazardous gas concentrations to protect equipment and personnel, particularly in sectors such as petrochemicals, pharmaceuticals, and semiconductors. Modern electrochemical sensors deliver rapid response times—often under 30 seconds—to detect toxic gases before they compromise automated processes. Over 70% of new industrial automation projects now include integrated gas detection systems as part of safety and control architectures. Additionally, the integration of sensor outputs with distributed control systems (DCS) improves real-time decision-making, reducing unplanned downtime and enhancing throughput in automated environments.

High calibration and maintenance requirements present a restraint for the Electrochemical Gas Sensors market. Electrochemical sensors generally require periodic calibration to maintain accuracy, particularly when deployed in harsh industrial environments with fluctuating temperatures and humidity. Frequent maintenance intervals increase operating costs for end-users and demand specialized technical resources, which can be scarce in remote or resource-constrained facilities. In some cases, calibration gas cylinders and certified technicians must be deployed regularly, adding logistical complexity. These factors contribute to slower adoption rates in small-to-medium enterprises that lack the infrastructure to manage ongoing maintenance, and they can delay deployments in cost-sensitive segments such as small manufacturing units or municipal service providers.

Smart building integration presents significant opportunities for the Electrochemical Gas Sensors market. As commercial real estate and corporate campuses prioritize occupant health and energy efficiency, sensor networks capable of monitoring indoor air quality are becoming standard. Electrochemical sensors can detect trace levels of toxic gases such as carbon monoxide and nitrogen dioxide, enabling ventilation systems to adjust in real-time to maintain safe and healthy conditions. Adoption is accelerating with pilot programs in major metropolitan developments deploying over 10,000 connected sensors to inform HVAC control strategies. Integration with building automation and occupant feedback platforms expands revenue potential beyond traditional safety use cases, unlocking value in comfort, compliance, and energy optimization strategies for facility managers.

Variability in regulatory frameworks challenges the Electrochemical Gas Sensors market by creating inconsistent requirements across jurisdictions, complicating compliance strategies for multinational corporations. Different countries and regions enforce diverse exposure limits, calibration standards, and reporting obligations for gas detection systems, requiring manufacturers to tailor products and documentation for each market. For example, workplace safety limits for specific gases may differ widely between regions, leading to varied sensor sensitivity and certification demands. This regulatory fragmentation increases product development costs and extends time-to-market cycles. End-users operating in multiple regions must invest in compliance expertise and adapt operational protocols to satisfy local mandates, which can slow deployment decisions and strain corporate compliance budgets.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction practices is significantly influencing the Electrochemical Gas Sensors market. Approximately 55% of new industrial and commercial projects implementing modular methods report measurable reductions in labor costs and project timelines. Prefabricated components require fewer on-site installations, driving demand for high-precision electrochemical sensors that monitor air quality and safety during off-site assembly. Europe and North America are leading regions in deploying these systems, with over 60% of construction projects integrating sensors into prefabricated modules for enhanced monitoring and compliance.

Integration with IoT and Smart Infrastructure: Over 48% of newly installed sensors are now connected to IoT platforms, enabling real-time monitoring and automated alerts. Smart buildings and industrial complexes increasingly rely on these networks to manage indoor air quality, energy efficiency, and hazardous gas detection. AI-powered analytics allow predictive maintenance and reduce false alarms by up to 30%, optimizing safety and operational efficiency. This trend is particularly strong in Asia-Pacific urban centers, where rapid industrialization and smart city initiatives are driving high-volume deployments.

Adoption of Low-Power and Miniaturized Designs: Miniaturized electrochemical sensors are gaining traction, with over 40% of portable monitoring units now using low-power microelectrode designs. These sensors reduce energy consumption by up to 35%, supporting mobile and remote deployments in hazardous or hard-to-reach environments. The trend is most pronounced in North American and European industrial facilities where portable gas detection and wearable safety devices are becoming standard for worker protection and regulatory compliance.

Expansion into Multi-Gas Detection Arrays: Multi-gas sensor arrays are being adopted in over 50% of new environmental monitoring installations, allowing simultaneous detection of multiple hazardous gases. Facilities in chemical, oil & gas, and manufacturing sectors are leveraging this technology to improve safety and minimize downtime, achieving up to 25% faster response times compared to single-gas solutions. This development aligns with increasing regulatory pressure and industrial automation requirements, ensuring comprehensive hazard detection across complex operational environments.

The Electrochemical Gas Sensors Market is delineated across multiple segmentation vectors including product type, application domain, and end-user categories, each reflecting distinct deployment patterns and performance expectations. Segment-level analysis underscores how tailored sensor architectures and function-specific implementations align with industry requirements from hazardous gas detection to environmental monitoring. Type segmentation distinguishes between single-gas dedicated sensors and advanced multi-gas arrays, with each offering differentiated sensitivity, response time, and integration complexity. Application segmentation underscores safety, compliance, and operational analytics use cases that span industrial, commercial, and infrastructure settings. End-user insights reveal varied adoption intensity across heavy industries, smart buildings, and public safety agencies, indicating that deployment choices are influenced by regulatory pressures, automation levels, and risk mitigation imperatives. Quantified segmentation metrics provide clarity on where investment and innovation are concentrated, guiding strategic planning for manufacturers, system integrators, and large-scale sensor consumers targeting performance optimization and enhanced safety outcomes.

Electrochemical gas sensor types can be categorized into single-gas sensors, multi-gas sensor arrays, and specialized configurations (e.g., high-temperature tolerant, miniaturized form factors). Multi-gas sensor arrays currently account for 47% of adoption, driven by their capability to detect and discriminate between multiple hazardous gases simultaneously in complex environments. Single-gas sensors hold 30% of the market, offering focused performance for targeted monitoring of gases such as carbon monoxide or hydrogen sulfide in confined spaces. Other specialized types—such as high-temperature tolerant sensors and wearable personal monitoring formats—constitute the remaining 23% combined, serving niche applications where environmental extremes or mobility are critical. Fastest growth is observed in miniaturized multi-gas arrays with an approx. 14% CAGR, driven by demand for compact, low-power, and network-friendly designs in smart infrastructure and portable safety devices.

Application segments in the Electrochemical Gas Sensors Market include industrial safety monitoring, environmental air quality assessment, building automation and smart facilities, and public safety and emergency response. Industrial safety monitoring currently accounts for 52% of installations, reflecting sustained demand for real-time hazardous gas detection in plants, chemical facilities, and oil and gas operations where personnel protection and regulatory compliance are paramount. Environmental air quality assessment holds 22% share, with expanding deployments in urban monitoring networks and regulatory compliance stations. Other applications—encompassing smart building ventilation control and emergency response workflows—constitute 26% combined, enabling automated ventilation adjustments and rapid alerts during hazardous conditions. Growth momentum is particularly strong in smart building integration with an approx. 13% CAGR, as occupancy-aware ventilation and indoor air quality standards gain prominence.

End-user segmentation highlights how adoption of electrochemical gas sensors varies across sectors such as manufacturing and heavy industry, building management and commercial estates, utilities and energy infrastructure, and public safety agencies. Manufacturing and heavy industry lead with 45% share, supported by stringent workplace safety mandates and integration with plant-wide analytics for early hazard detection. Building management and commercial estates account for 24%, leveraging sensors within HVAC control and occupant health monitoring systems. Other segments—including utilities and energy and public safety—represent 31% combined, with utilities embedding sensors in grid substations and energy storage facilities, and public safety agencies deploying portable monitors for emergency response. Fastest-growing end-user segment is smart commercial facilities with an approx. 15% CAGR, as enterprises prioritize occupant wellness and automated environmental controls.

North America accounted for the largest market share at 38% in 2025 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 12.3% between 2026 and 2033.

In 2025, North America recorded approximately 9.5 million electrochemical gas sensor units deployed across industrial and commercial installations, with over 4.2 million units in the U.S. alone. Asia‑Pacific consumption reached 6.8 million units, led by China (3.1 million), Japan (1.4 million), and India (1.2 million). Europe held a 27% share with around 6.8 million units, while South America and Middle East & Africa together accounted for 14%, totaling over 3.5 million units. Consumer adoption rates show that utilities and energy infrastructure in North America embed sensors in over 52% of new projects, whereas in Asia‑Pacific, 48% of new smart city air quality programs now include networked electrochemical gas sensors. Regional investment figures such as USD 95 million in sensor manufacturing facilities in North America and USD 78 million in Asia‑Pacific R&D partnerships illustrate where strategic efforts are concentrated.

How does advanced industrial safety drive adoption trends?

North America holds approximately 38% share of the Electrochemical Gas Sensors market based on deployment volumes in 2025, with strong enterprise uptake in the U.S. and Canada. Key industries such as oil & gas, chemicals, and utilities are primary demand drivers, with over 55% of recent sensor installations tied to compliance with tightened OSHA and EPA safety mandates. Regulatory changes in 2024 accelerated gas detector upgrades, with healthcare and finance facilities also increasing adoption for indoor air quality monitoring—enterprise adoption in healthcare settings exceeds 42%. Technological advancements include integration with cloud analytics and digital twins, enabling predictive maintenance and automated alerts that reduce false positives by up to 28%. Local manufacturers are expanding capabilities; one U.S. sensor producer recently launched an IoT‑enabled electrochemical gas sensor line achieving 30% longer field life. North American consumer behavior shows preference for integrated safety monitoring bundled with building management systems, especially in commercial real estate, reflecting a shift toward proactive compliance and digital transformation.

What regulatory pressures shape advanced safety deployments?

Europe accounts for roughly 27% of the Electrochemical Gas Sensors market with Germany, the UK, and France leading adoption. Regulatory bodies such as the European Chemicals Agency (ECHA) and national workplace safety agencies have introduced more stringent exposure limits, prompting replacements of legacy detectors with advanced electrochemical technologies in over 48% of industrial facilities. Sustainability initiatives across the EU emphasize indoor air quality in public buildings, with approximately 35% of new construction projects integrating electrochemical gas sensors into ventilation systems. Adoption of emerging technologies is notable, including wireless mesh networking and AI‑assisted calibration that improve data reliability by up to 26%. A prominent regional player based in Germany recently deployed next‑generation multi‑gas sensors across automotive manufacturing plants, enhancing hazardous gas profiling. European consumer behavior reflects a strong emphasis on explainable sensor outputs and compliance reporting, which influences procurement decisions among enterprises prioritizing transparent safety metrics.

How are infrastructure trends accelerating smart monitoring rollouts?

Asia‑Pacific accounted for close to 30% of the Electrochemical Gas Sensors market in 2025, with China, India, and Japan as top consuming countries. China alone accounted for over 3.1 million units deployed, driven by urban air quality monitoring networks and heavy industry safety upgrades. Infrastructure and manufacturing expansions in India and Japan also boosted volumes, with adoption now exceeding 38% of new industrial safety contracts. Regional tech trends include the emergence of domestic sensor start‑ups focusing on low‑power designs and AI‑assisted calibration tools, improving sensor uptime by roughly 22%. One major electronics manufacturer in Japan announced integration of electrochemical sensors into smart home networks, supporting automated ventilation adjustments. Asia‑Pacific consumer behavior is shaped by rapid urbanization and demand for mobile app‑enabled air quality insights, with over 46% of consumers engaging with air quality data via smartphone platforms, influencing both B2B and B2C sensor deployments.

What energy sector developments influence demand patterns?

South America holds around 9% of the Electrochemical Gas Sensors market, with Brazil and Argentina as key contributors. The region’s energy and mining sectors are primary demand drivers, with nearly 45% of recent sensor installations tied to gas leak detection in mining operations and refinery safety systems. Infrastructure modernization in urban centers such as São Paulo and Buenos Aires has seen deployment of electrochemical sensors in over 30% of new commercial buildings. Government incentives aimed at improving workplace safety have accelerated purchases and upgrades within industrial facilities, particularly in Brazil. A regional player in Brazil reported a 24% year‑over‑year increase in orders for portable electrochemical detectors used by emergency response teams. Consumer behavior in South America shows increased interest in bilingual digital interfaces and localized support services, with over 52% of enterprise buyers prioritizing platforms offering Spanish and Portuguese language integration.

What regional dynamics shape safety and monitoring investments?

Middle East & Africa account for approximately 5% of global Electrochemical Gas Sensors market volume, with demand trends led by oil & gas, petrochemical, and construction sectors. Major growth countries include the UAE and South Africa, where stringent safety standards in energy infrastructure projects have driven adoption in more than 28% of new builds. Technological modernization, such as integration with SCADA and remote monitoring systems, has enhanced operational oversight and reduced manual inspection dependency. Local regulations and trade partnerships in the Gulf region emphasize imported advanced sensors for compliance with international safety codes, prompting regional firms to invest in training and support services. A South African safety solutions provider reported that over 60% of its corporate clients now request integrated sensor networks with remote diagnostics. Consumer behavior in the region reflects preference for robust, climate‑resilient sensor designs capable of operating in high‑temperature and high‑humidity environments, influencing procurement criteria across industrial users.

United States – 24% share: High production capacity and strong end‑user demand from oil & gas and industrial safety sectors.

China – 18% share: Extensive manufacturing base and rapid urban air quality monitoring program deployments.

The competitive environment in the Electrochemical Gas Sensors market is moderately consolidated among established multinational corporations and specialized niche manufacturers, with an estimated 15–20 active competitors driving technological innovation, geographic expansion, and product differentiation. Key industry leaders together account for approximately 58–65% combined share of installed sensor units and product placements globally, indicating a competitive core surrounded by agile regional players. Market positioning varies from broad industrial portfolios to specialized high‑precision sensor subsets that serve environmental monitoring, industrial safety, and smart infrastructure segments. Strategic initiatives in recent years include multiple partnerships and co‑development agreements, such as collaborations on next‑generation electrochemical platforms with enhanced sensitivity and wireless connectivity, as well as mergers and acquisitions designed to expand portfolios and geographic reach. Some competitors have announced product launches featuring extended operational life and automated diagnostics, responding to customer demands for reliability and reduced maintenance cycles. Innovation trends influencing competition include miniaturized multi-gas sensing arrays, IoT connectivity, and AI‑enabled predictive calibration systems that improve reliability and reduce false alarms. Mid‑tier players focus on competitive pricing and targeted regional growth, while leading firms leverage global distribution networks and deep R&D investments to sustain differentiation, making the competitive landscape dynamic and technology‑intensive.

Honeywell International Inc.

Figaro Engineering Inc.

Alphasense Ltd.

Siemens AG

MSA Safety Incorporated

Membrapor AG

SGX Sensortech Ltd

Aeroqual Ltd

Teledyne Technologies Incorporated

Amphenol Advanced Sensors

Nemoto Sensor Engineering Co., Ltd.

Dynament Ltd.

Sensirion AG

Industrial Scientific Corporation

The Electrochemical Gas Sensors Market is being reshaped by a range of current and emerging technologies that enhance sensor performance, reliability, and integration with digital systems. Miniaturized electrochemical sensors are now deployed in over 42% of portable monitoring units, offering rapid response times of under 30 seconds for gases such as carbon monoxide, hydrogen sulfide, and nitrogen dioxide. Multi-gas sensing arrays are increasingly adopted in industrial and urban applications, allowing simultaneous detection of multiple hazardous gases, with over 50% of recent environmental monitoring projects implementing these solutions.

Emerging technologies include low-power microelectrode designs that reduce energy consumption by up to 35%, enabling integration into wearable safety devices and smart building systems. AI-assisted calibration algorithms are gaining adoption in approximately 38% of new installations, automatically adjusting sensitivity to environmental conditions, reducing false positives by nearly 28%, and extending operational lifespan. Wireless connectivity and IoT-enabled sensor networks are now standard in over 45% of new industrial deployments, supporting real-time data transmission, predictive maintenance, and remote diagnostics.

Hybrid sensing technologies combining electrochemical detection with optical or MEMS-based platforms are being piloted in urban and industrial environments, providing enhanced selectivity and robustness in harsh conditions. Additionally, integration with digital twins and cloud analytics platforms allows enterprises to monitor gas exposure levels across multiple facilities, with some large-scale projects reporting a 25% improvement in safety compliance tracking. These advancements position electrochemical gas sensors as essential components in smart infrastructure, industrial automation, and environmental compliance strategies.

• In May 2025, Honeywell introduced a new hydrogen leak detection sensor engineered to identify hydrogen leaks as small as 50 parts per million, enhancing safety for hydrogen-powered systems in industrial equipment, power generators, commercial vehicles, and energy infrastructure. (honeywell.com)

• In June 2025, Alphasense unveiled its new EL-Series electrochemical gas sensors, designed with improved sensitivity and extended operational life, supporting industrial safety and environmental monitoring deployments across fixed and portable systems.

• In March 2025, MSA Safety Inc secured a multi‑year contract to supply fleets of electrochemical toxic and flammable gas detectors to a major North Sea oil & gas operator, expanding the company’s presence in offshore safety applications.

• In January 2024, Draegerwerk AG commenced a major supply contract to equip a large European petrochemical complex with electrochemical gas detection systems, reinforcing its position in process safety instrumentation for heavy industrial environments.

The Electrochemical Gas Sensors Market Report covers comprehensive insights into global demand, segment performance, and technological developments across product types, applications, and geographic regions. Detailed segmentation includes single‑gas and multi‑gas electrochemical sensors, portable vs. fixed systems, and emerging sensor configurations designed for specific gas profiles such as hydrogen, carbon monoxide, and toxic industrial gases. Application analysis spans industrial safety monitoring, environmental air quality assessment, smart building automation, and emergency response systems, with quantified adoption rates and implementation patterns. End‑user breakdowns examine deployment trends among manufacturing, utilities, healthcare facilities, public sector installations, and commercial estates, highlighting varying adoption behavior and usage intensity. The report also explores technology vectors like low‑power microelectrode designs, IoT and wireless integration, AI‑assisted calibration, and hybrid sensor architectures that extend capabilities and operational resilience. Regional coverage includes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with benchmarked consumption volumes and regional innovation trends. Insights into regulatory, compliance, and ESG drivers are presented alongside competitive dynamics, innovation pipelines, and market positioning. Emerging and niche segments such as wearable gas monitors, automotive cabin air quality systems, and hydrogen infrastructure detection solutions are also examined, offering a multifaceted view of current and future opportunities for manufacturers, system integrators, and strategic investors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell International Inc., Figaro Engineering Inc., Alphasense Ltd., Siemens AG, MSA Safety Incorporated, Membrapor AG, SGX Sensortech Ltd, Aeroqual Ltd, Teledyne Technologies Incorporated, Amphenol Advanced Sensors, Nemoto Sensor Engineering Co., Ltd., Dynament Ltd., Sensirion AG, Industrial Scientific Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |