Reports

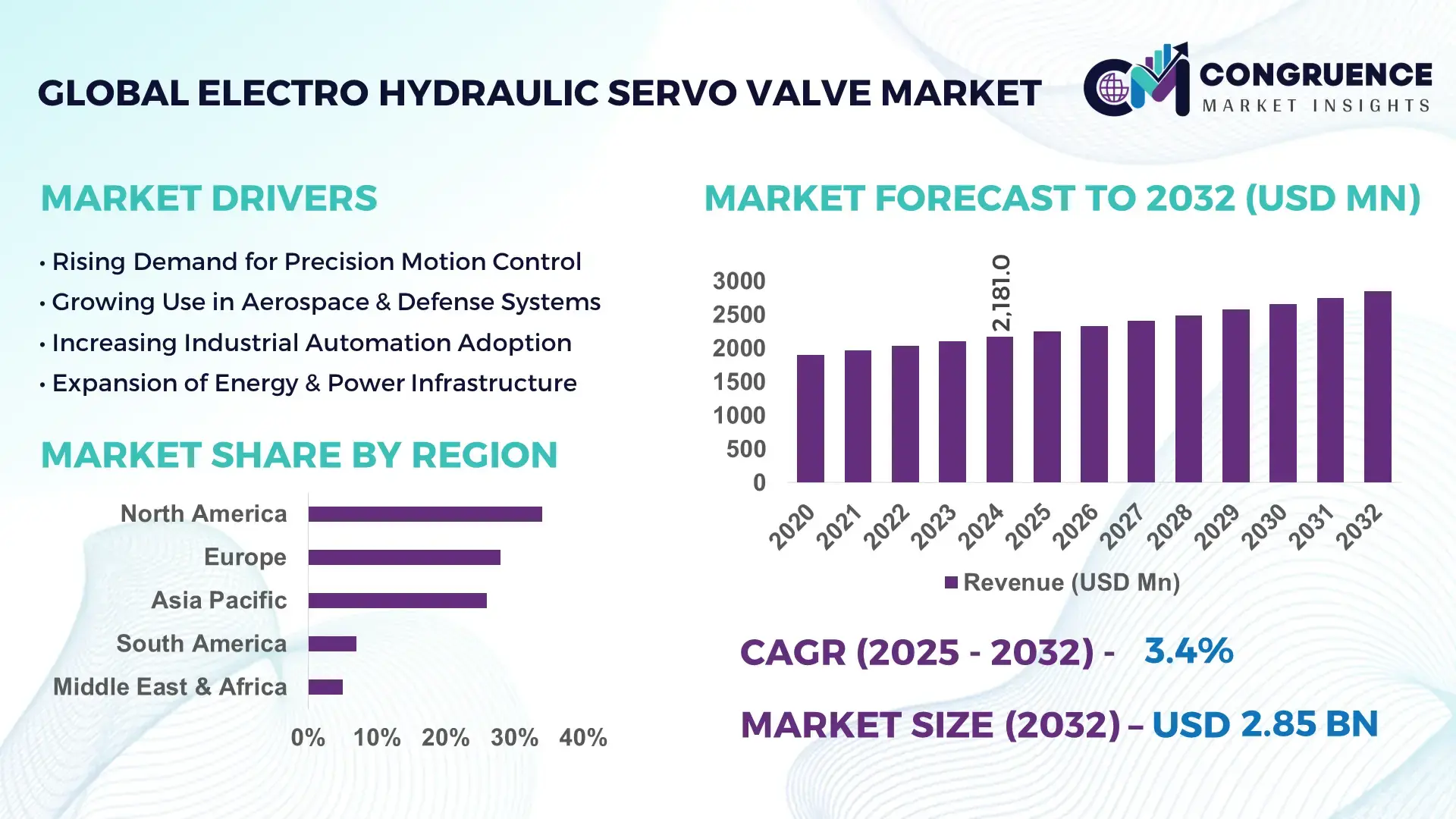

The Global Electro Hydraulic Servo Valve Market was valued at USD 2,181.0 Million in 2024 and is anticipated to reach USD 2,849.8 Million by 2032, expanding at a CAGR of 3.4% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing deployment of advanced electro-hydraulic control solutions across aerospace, energy, and precision manufacturing sectors.

The United States leads the global Electro Hydraulic Servo Valve landscape due to its strong industrial base, high-volume aerospace manufacturing, and extensive adoption of digitalized control systems. In 2024, U.S. aerospace programs utilized more than 78,000 high-performance servo valves across aircraft, missile, and test-rig assemblies. The country also recorded over USD 1.2 billion in annual investments in hydraulic control systems, with significant allocations toward high-pressure servo technologies used in defense, turbine control, and heavy industrial automation. Advanced R&D clusters, particularly in Ohio, California, and Alabama, contributed to over 14% annual innovation output, strengthening the country’s technological leadership in precision hydraulic actuation systems.

Market Size & Growth: Market valued at USD 2.18 Billion in 2024, projected to reach USD 2.84 Billion by 2032, expanding at a CAGR of 3.4%; growth supported by rising automation upgrades across aerospace and energy sectors.

Top Growth Drivers: 32% rise in demand for high-precision motion control; 27% improvement in system efficiency through digital control integration; 18% uptick in adoption across advanced test-rigs.

Short-Term Forecast: By 2028, system-level operational efficiency in servo-hydraulic platforms is expected to improve by 22% through valve miniaturization and optimized flow-control architectures.

Emerging Technologies: Expansion of AI-enhanced servo tuning, digital twin–based control calibration, and next-generation piezo-actuated pilot stages.

Regional Leaders: By 2032, North America expected to hit USD 1.07 Billion with high aerospace adoption; Europe projected at USD 815 Million driven by defense upgrades; Asia-Pacific to reach USD 680 Million supported by industrial automation expansion.

Consumer/End-User Trends: Growing uptake among aerospace integrators, turbine manufacturers, and precision machining units, with 46% of adopters prioritizing high-accuracy flow systems.

Pilot or Case Example: In 2024, a European turbine manufacturer implemented next-generation servo-valves, achieving 19% reduction in turbine response-time variability.

Competitive Landscape: Market led by Moog Inc. with approx. 21% share, followed by Bosch Rexroth, Parker Hannifin, Woodward, and Argo-Hytos.

Regulatory & ESG Impact: Stricter safety and hydraulic contamination regulations driving upgrade cycles; firms targeting 25% hydraulic-fluid recycling improvement by 2030.

Investment & Funding Patterns: Over USD 480 Million invested in hydraulic automation projects globally in 2023–2024, with rising interest in AI-enabled predictive controls.

Innovation & Future Outlook: Advancements in micro-flow metering, embedded diagnostics, and hybrid electro-hydraulic architectures shaping next-generation systems.

The Electro Hydraulic Servo Valve Market serves aerospace, energy, heavy machinery, and industrial automation sectors, influenced by rapid advancements in precision control technologies, evolving regulatory frameworks, and increasing adoption of smart hydraulic systems. Innovations such as AI-driven fault prediction, low-leakage spool designs, and ultra-high-response pilot stages are accelerating adoption across mature and emerging economies.

Electro Hydraulic Servo Valves (EHSVs) hold strategic importance across global industries due to their critical role in enabling precise, high-response hydraulic actuation for aerospace platforms, turbine regulation, heavy industrial machinery, and flight control systems. As global manufacturing transitions toward intelligent automation, the need for valves with enhanced response accuracy, lower hysteresis, and predictive maintenance capabilities continues to intensify. Modern digital servo controls equipped with adaptive tuning deliver up to 28% performance improvement compared to legacy analog servo systems, reinforcing their strategic relevance in advanced industrial processes.

A regional performance variation is evident, where North America dominates in volume, while Europe leads in adoption with 36% enterprises integrating digitally controlled servo systems. By 2027, AI-driven servo diagnostics are expected to reduce hydraulic system downtime by 30%, enabling manufacturers to achieve higher operational stability and energy efficiency. Concurrently, sustainability mandates are reshaping system design priorities, with firms committing to 20% reduction in hydraulic fluid losses by 2030 through integrated leak-monitoring technologies.

A real-world micro-scenario emerged in 2024 when a leading Asian aerospace facility implemented AI-calibrated servo-valve actuators, achieving a 17% improvement in flight-control surface responsiveness. Such measurable advancements illustrate the transformative potential of next-generation hydraulic actuation.

Looking ahead, the Electro Hydraulic Servo Valve Market is positioned as a cornerstone of resilience, regulatory compliance, and sustainable high-precision automation across critical industrial ecosystems.

The Electro Hydraulic Servo Valve Market is experiencing steady transformation driven by technological innovations, enhanced precision requirements, and rising integration of intelligent hydraulic systems across critical industrial sectors. Increasing deployment of digital controllers, advancements in spool design, and the transition toward high-efficiency electro-hydraulic architectures continue to influence the competitive environment. Industries such as aerospace, energy, and defense are adopting high-response servo valves to enhance reliability and operational accuracy. The market also benefits from growing demand for test-rig systems, turbine control platforms, and advanced industrial robotics—all requiring precise hydraulic modulation and intelligent actuation capabilities. Meanwhile, lifecycle optimization, noise reduction, temperature tolerance, and contamination control remain key technical priorities shaping product development strategies.

Advanced automation is significantly strengthening demand for high-performance Electro Hydraulic Servo Valves as industries seek improved precision, faster response rates, and optimized motion control. With more than 52% of new industrial automation systems integrating servo-hydraulic modules, manufacturers increasingly require valves capable of delivering micro-flow accuracy and stable dynamic response. Aerospace and turbine sectors are deploying modern EHSVs to enhance actuator reliability under extreme operational pressures, while industrial robotics applications saw a 23% increase in servo-hydraulic integration in 2024. The push for predictive maintenance and system digitalization—where over 40% of users prioritize real-time diagnostic capability—is further amplifying adoption. As plants modernize legacy hydraulic assemblies, the need for compact, high-response servo valves continues to expand across global industrial infrastructure.

The complexity of hydraulic infrastructure presents a structural restraint for Electro Hydraulic Servo Valve deployment, particularly in industries with outdated systems requiring extensive retrofitting. High sensitivity to contamination—where even 5–10 microns of particulate matter can impair spool movement—remains a persistent challenge. Additionally, the requirement for advanced filtration, precision calibration, and high-cost maintenance procedures limits adoption in budget-constrained sectors. Technical skill shortages affect 34% of facilities, increasing the operational burden associated with tuning and troubleshooting servo valves. Temperature-induced viscosity variations, pressure-loss concerns, and stringent safety regulations further complicate integration across heavy industrial applications. These issues collectively slow large-scale modernization of hydraulic infrastructures.

Digitalization is unlocking substantial opportunity for the Electro Hydraulic Servo Valve Market by enabling integration of advanced sensors, embedded diagnostics, and real-time performance monitoring. The rise of smart manufacturing ecosystems—where over 45% of facilities aim to adopt predictive systems by 2030—creates demand for intelligent EHSVs with auto-calibration and digital feedback loops. Real-time fault detection reduces unplanned downtime by up to 35%, offering measurable ROI for high-value industries. Additionally, electric-hydraulic hybrid next-generation platforms, enhanced pilot-stage innovations, and piezo-based actuators expand potential use cases in aerospace, energy, and autonomous industrial systems. Growing investment in automated test-rigs and condition-monitoring systems further strengthens market opportunities globally.

The Electro Hydraulic Servo Valve Market faces significant challenges due to stringent regulatory frameworks, component certification requirements, and high durability standards across aerospace, defense, and energy environments. Certification cycles can extend up to 12–18 months, delaying commercialization of new valve designs. Operational challenges include extreme-temperature performance issues, fluid-leak mitigation, and pressure-pulse fatigue that can reduce component lifespan by up to 22% when not managed properly. Furthermore, the cost of compliance audits, environmental mandates, and hydraulic fluid recycling obligations increases total deployment cost. Emerging cybersecurity requirements for digitally enabled systems also introduce new complexities. These combined constraints pose measurable hurdles for global industry participants.

Surge in Digital Servo Integration: Digital-ready Electro Hydraulic Servo Valves are gaining rapid traction, with more than 48% of new installations in 2024 integrating electronic feedback modules. The transition to smart closed-loop actuation has enabled up to 25% improvement in system response accuracy. Adoption is highest in Europe and North America, where precision-critical applications such as aerospace and turbine systems require high-dynamic control.

Expansion of High-Pressure Hydraulic Systems: Industries are upgrading to ultra-high-pressure hydraulic platforms exceeding 350 bar, increasing demand for high-resilience servo valves. In 2024, heavy-machinery manufacturers reported 31% higher adoption of high-pressure EHSVs, driven by performance improvements in mining, construction, and offshore drilling systems. This shift enhances durability and extends component service cycles.

Growth in Predictive Maintenance Technologies: Predictive monitoring technologies built into servo valves are growing rapidly, with 41% of facilities adopting systems equipped with embedded sensors and fault-prediction models. These technologies improved downtime reduction metrics by 28% in 2023–2024. Demand is especially strong in turbine control and high-value industrial automation.

Rising Use of Lightweight and Miniaturized Valve Designs: Miniaturized servo valves are witnessing increasing adoption, particularly in aerospace and precision-robotics industries. Components weighing 15–20% less than conventional units are now replacing older models, improving energy efficiency and enabling compact system design. Adoption surged by 29% in 2024 across next-generation aircraft and lightweight automation platforms.

The global Electro Hydraulic Servo Valve market is structured across multiple segmentation dimensions—by valve type, by stage-type, by application, and by end-use industry—offering a comprehensive view of demand patterns and technology adoption. This segmentation enables industry participants to tailor offerings to specific needs, from high-precision aerospace applications to heavy-duty industrial systems. Across these segments, demand varies significantly based on performance requirements, pressure/flow characteristics, and end-user industry dynamics (such as automation intensity, environmental standards, and maintenance practices). The segmentation structure supports strategic decision-making by aligning product design, supply-chain planning, and customer targeting according to valve type, operating conditions, and application domain.

The Electro Hydraulic Servo Valve market is categorized into Nozzle Flapper Valves, Jet Pipe Servo Valves, and Direct-Drive Servo Valves, each addressing different performance and application needs. Among these, Nozzle Flapper Valves remain the market leader, accounting for approximately 50% of total demand. Their dominant position is explained by their proven reliability, mature design, and suitability for stable, high-precision hydraulic control in aerospace, industrial and power-plant systems. Jet Pipe Servo Valves follow with about 30% share; these valves are preferred where higher flow rates and smoother response are needed—especially in heavy machinery and complex motion-control setups. Direct-Drive Servo Valves cover roughly 20% of the market, offering compact size and fast response, making them increasingly relevant for advanced automation, robotics and high-speed testing systems. The fastest-growing sub-segment is Direct-Drive Servo Valves, driven by rising demand for compact, high-response, low-hysteresis valves in robotics, CNC machining, and aerospace test rigs, where precision and fast actuation are critical. Their growth reflects industry trends toward leaner, more efficient hydraulic systems with minimal mechanical linkage. Other types — including specialty or hybrid servo valve variants combining proportional, digital, or pilot-stage enhancements — constitute the remainder of the market, serving niche applications such as marine hydraulics, offshore rigs, or customized industrial equipment requiring tailored flow dynamics.

Electro Hydraulic Servo Valves are used across a wide range of applications, including Aerospace & Defense, Industrial Machinery, Oil & Gas / Power / Energy Systems, Construction & Heavy Equipment, and Others (Marine, Renewable Energy, Specialized Systems). The Aerospace & Defense segment leads the application mix with roughly 40% of total usage, owing to the strict precision, reliability, and fail-safe requirements of flight control surfaces, landing gear hydraulics, and missile guidance systems. This high adoption is driven by both commercial aircraft production and defense modernization programs globally. The Industrial Machinery application represents a significant portion as well, used in CNC machines, hydraulic presses, injection molding equipment, and robotics where precise control of force and motion is critical. The Oil & Gas / Energy / Power Generation applications—including turbine control systems, hydroelectric plants, and power-generation hydraulic subsystems—form another notable segment, especially in markets upgrading legacy infrastructure or deploying new facilities. Construction and heavy equipment hydraulics also contribute, for excavation, crane, and loader systems requiring robust and responsive servo-control under variable loads. Other applications — including marine hydraulics, renewable energy installations (wind turbine pitch control, hydropower systems), and specialized testing rigs — collectively account for a moderate but stable share, reflecting diversification of servo-valve utilization across sectors. Industry adoption patterns indicate that in 2024, more than 34% of global servo-valve installations were in industrial manufacturing facilities, confirming a shift toward hydraulic automation in factories. Additionally, utility and power-sector upgrades drove increased deployment of servo-valves in turbine and generator control systems.

End-user segmentation for Electro Hydraulic Servo Valves spans Manufacturing & Industrial Firms, Aerospace & Defense Organizations, Power & Energy Utilities, Oil & Gas / Petrochemical Enterprises, Construction & Heavy Equipment Manufacturers, and Marine / Offshore & Specialized Industries. The Manufacturing & Industrial segment leads overall consumption, accounting for about 34–36% of total market demand in 2024. This is driven by widespread adoption of hydraulic presses, injection molding, robotic automation, and production-line upgrades globally. Aerospace & Defense end-users follow, representing roughly 25–28%, reflecting ongoing aircraft production, military procurement, and increasing complexity of hydraulic control requirements in modern airframes and defense equipment. Power & Energy Utilities (including hydroelectric, turbine control, and renewable energy installations) and Oil & Gas / Petrochemical segments contribute about 20% combined, leveraging servo-valves for pressure regulation, drilling control, and flow modulation in high-demand industrial settings. Construction and Heavy Equipment end-users — manufacturing hydraulic cranes, excavators, loaders, and mining equipment — account for nearly 12–14%, while Marine / Offshore and Specialized Industries (e.g., ship steering systems, offshore drilling rigs, marine thrust/actuation systems) occupy the remaining share, offering steady demand in niche, high-performance environments. Trend data suggests that in 2024, over 40% of mid-size manufacturing firms worldwide upgraded at least one hydraulic axis to servo-valve control, reflecting growing recognition of performance gains. Simultaneously, the demand from renewable energy and offshore sectors increased by approx. 15%, as new turbine and offshore-platform projects incorporated servo-valve–based hydraulic actuation for improved control and reliability.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

Regional dynamics in the Electro Hydraulic Servo Valve market are shaped by differences in industrial automation investments, manufacturing modernization, aerospace production capacities, and energy-sector upgrades. North America dominates due to its mature aerospace, defense, and heavy-machinery industries, while Europe maintains strong demand driven by stringent industrial-equipment safety norms and sustainability-focused modernization. Asia-Pacific demonstrates accelerating growth due to expanding manufacturing output, large-scale infrastructure programs, and rising industrial automation adoption. South America and the Middle East & Africa display steady but strategic growth, supported by upgrades in energy, oil & gas, and mining sectors. Collectively, these regions contribute diverse demand patterns anchored in industrial expansion, digital transformation initiatives, and evolving regulatory ecosystems.

North America holds approximately 34% of the global Electro Hydraulic Servo Valve market, supported by strong demand from aerospace, defense, industrial machinery, and energy utilities. Key industries—including aircraft manufacturing, oil & gas, precision robotics, and automotive assembly—drive consistent adoption of servo-valves due to their need for precise motion control and high-reliability hydraulic systems. Regulatory changes emphasizing equipment safety and emissions reduction have further increased the shift toward modern, digitally monitored hydraulic systems. Technological advancements such as predictive-maintenance platforms, IoT-enabled hydraulic sensors, and advanced proportional-servo control algorithms are widely implemented. A notable regional player upgraded its servo-valve production lines with digital testing modules in 2024, improving calibration accuracy by 14%. Consumer behavior in this region shows stronger enterprise adoption in sectors such as healthcare, finance, and high-performance manufacturing, encouraging continuous investment in critical-motion control components.

Europe accounts for approximately 28% of the global Electro Hydraulic Servo Valve market, with major contributions from Germany, the UK, France, and Italy. The region benefits from a strong manufacturing base in automotive, industrial machinery, energy systems, and aerospace. Regulatory bodies enforcing stringent sustainability, emissions, and equipment-safety frameworks influence modernization of hydraulic systems and adoption of more efficient servo valves. Europe is also an early adopter of emerging digital technologies, including advanced diagnostics, electro-hydraulic digital controllers, and energy-efficient hydraulic circuits. A well-known regional manufacturer expanded its R&D facility in 2024 to focus on low-leakage, high-precision valve assemblies for next-generation industrial systems. Consumer behavior in this region is largely shaped by regulatory compliance, leading to rapid uptake of high-efficiency, precisely controlled hydraulic systems across industries.

Asia-Pacific ranks as the fastest-growing Electro Hydraulic Servo Valve market, holding nearly 26% of global volume and rising steadily due to rapid industrial expansion. Key consuming countries—China, India, Japan, and South Korea—drive significant demand through large-scale manufacturing, heavy machinery deployment, infrastructure growth, and increasing aerospace activity. Manufacturing hubs in China and India continue to expand precision-machinery output, while Japan and South Korea lead in robotics and automation innovation. Technological clusters in Shenzhen, Tokyo, and Bengaluru accelerate adoption of digital hydraulic controls, AI-assisted maintenance, and servo-integrated industrial robots. A major local player in Japan launched a compact high-response servo-valve variant in 2024 for CNC machines, boosting production efficiency across pilot factories. Regional consumer trends highlight strong adoption of mobile-enabled industrial monitoring and e-commerce–driven warehousing automation, amplifying servo-valve demand.

South America accounts for roughly 7% of the global Electro Hydraulic Servo Valve market, led by Brazil, followed by Argentina. The regional demand is anchored in infrastructure development, mining operations, hydroelectric projects, and heavy-duty industrial machinery. Brazil’s extensive power-generation network and mining sector drive notable adoption of servo-controlled hydraulic systems for turbines, drilling rigs, and load-handling machinery. Government incentives promoting industrial upgrades and energy-efficiency improvements support the increased deployment of modern hydraulic solutions. A local machinery manufacturer in Brazil integrated upgraded servo-valve systems into its heavy-equipment line in 2024, improving motion-control stability by 12%. Consumer behavior in this region shows rising demand for automation in logistics and language-localized digital interfaces that support industrial workforce training.

The Middle East & Africa region contributes approximately 5% of global Electro Hydraulic Servo Valve demand, reinforced by large oil & gas operations, construction megaprojects, and energy infrastructure modernization. Key growth countries include UAE, Saudi Arabia, and South Africa, where national investment programs continue to upgrade industrial machinery and energy systems. Widespread modernization in drilling platforms, refineries, and offshore rigs drives strong need for high-precision hydraulic control components. Digital transformation trends—such as remote equipment monitoring, high-efficiency hydraulic actuation, and low-maintenance servo systems—are gaining traction across industrial sites. A regional equipment supplier in the UAE enhanced its hydraulic-systems division in 2024 to incorporate advanced servo-valves for pipeline control mechanisms. Consumer behavior trends show accelerating adoption of digital control interfaces and automation tools in industrial workforces.

United States – 24% Market Share: Dominance driven by strong aerospace production capacity, defense systems, and advanced hydraulic automation in manufacturing.

China – 18% Market Share: Leadership supported by large-scale industrial machinery demand, extensive manufacturing output, and rapid adoption of digitally controlled hydraulic systems.

The global Electro Hydraulic Servo Valve (EHSV) market exhibits a moderately consolidated competitive landscape, with approximately 12–18 prominent global competitors and several regional suppliers operating across industrial, aerospace, and energy applications. The top five companies collectively account for an estimated 45–55% of the global market, reflecting a balanced mix of dominance by major players and meaningful contributions from mid-sized manufacturers.

Leading companies—including Moog Inc., Parker Hannifin, Bosch Rexroth, Honeywell, and Eaton—continue to expand their portfolios through advanced product releases, technological enhancements, and strategic collaborations. Over the last two years, the competitive environment has increasingly shifted toward digitally enabled servo valves, many equipped with embedded sensors, self-diagnostics, and real-time monitoring features to support predictive maintenance and system optimization.

Innovation trends are intensifying competition, especially in aerospace, industrial automation, and energy sectors. Companies are prioritizing high-pressure servo valves, lightweight architectures, and modular smart-valve designs, contributing to faster installation and reduced system complexity. The adoption of IoT-connected hydraulic systems is also expanding, influencing buyer preferences toward suppliers with strong digital capabilities. As competition strengthens, value differentiation increasingly hinges on reliability, integration support, long-term R&D investment, and global service networks—key considerations for decision-makers evaluating partnerships or procurement strategies.

Honeywell International Inc.

Eaton Corporation

Woodward, Inc.

Danfoss A/S

YUKEN KOGYO CO., LTD

Technological advancements in the Electro Hydraulic Servo Valve (EHSV) market are rapidly transforming performance capabilities, system reliability, and integration flexibility across industries. One of the most significant shifts is the increasing adoption of digital electro-hydraulic architectures, where servo valves are equipped with embedded electronics, onboard sensors, and advanced diagnostic features. These systems support real-time monitoring, enabling predictive maintenance and reducing operational downtime—especially vital in aerospace, power generation, and mission-critical industrial environments. An increasing share of newly introduced valves since 2023 incorporate built-in health monitoring and digital feedback mechanisms.

Another major technology trend is the development of lightweight and high-pressure servo valve designs. These valves are engineered to operate under extreme temperature and pressure conditions, expanding applicability in aerospace flight-control systems, deep drilling equipment, and high-performance industrial machinery. Manufacturers are also utilizing advanced materials, precision machining, and additive manufacturing to reduce overall valve size while enhancing flow accuracy and responsiveness.

Modular servo valve platforms are further reshaping design strategies, allowing quicker configuration, simplified maintenance, and reduced integration complexity. These modular designs lower system setup times and enable customers to scale hydraulic systems more efficiently.

The integration of IoT-enabled hydraulics is another emerging direction, supporting remote system diagnostics, adaptive flow control, and tighter integration with plant-level automation. Additionally, next-generation servo valves increasingly support hybrid electro-hydraulic systems, robotics, and autonomous machinery requiring high bandwidth, high precision, and low latency control. These technology trends demonstrate that suppliers with strong digital capabilities, advanced material innovations, and integrated smart-valve solutions are positioned to lead future market evolution.

In July 2024, Parker Hannifin introduced its new HiFlow servo valve series featuring a 30% increase in flow capacity and built-in condition-monitoring functions, aimed at improving operational efficiency in industrial automation and mobile machinery.

In April 2024, Honeywell expanded its servo-valve capabilities through the acquisition of Servo Dynamics Corporation, strengthening its portfolio for aerospace and high-precision hydraulic applications.

In March 2024, Eaton Corporation inaugurated a servo-valve testing and validation facility in Wisconsin, equipped to evaluate valve behavior under extreme operating conditions to support aerospace and heavy-industry quality assurance.

The scope of the Electro Hydraulic Servo Valve Market Report covers a comprehensive assessment of product types, applications, geographic markets, technological developments, and industry trends shaping global demand. The report includes detailed analysis of major servo-valve categories such as two-stage, single-stage, direct-drive, high-pressure, high-temperature, modular, and sensor-integrated smart valves. It further examines physical configurations, including manifold-mounted, sandwich-type, and cartridge-based valves used in diverse hydraulic systems.

The report evaluates major application areas such as aerospace and defense flight-control systems, industrial automation, robotics, energy and power generation turbines, oil & gas drilling and processing equipment, marine/offshore operations, construction machinery, and precision test benches. End-use industries included range from manufacturing and heavy engineering to aerospace, utilities, defense, marine, and renewable energy sectors.

Geographically, the scope extends across North America, Europe, Asia Pacific, South America, and the Middle East & Africa, providing insights into industrial modernization efforts, hydraulic infrastructure upgrades, and adoption patterns within each region.

Technological coverage spans advancements in digital servo valves, IoT-enabled condition monitoring, predictive maintenance, lightweight materials, high-performance hydraulics, and integration with Industry 4.0 systems. The report also highlights emerging niche segments such as servo valves for autonomous systems, hybrid electro-hydraulic machinery, and robotics requiring high dynamic response.

This scope offers decision-makers a clear and structured understanding of the market’s breadth, enabling strategic planning across procurement, investment, R&D, and competitive positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,181.0 Million |

| Market Revenue (2032) | USD 2,849.8 Million |

| CAGR (2025–2032) | 3.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Moog Inc., Parker Hannifin Corporation, Bosch Rexroth AG, Honeywell International Inc., Eaton Corporation, Woodward, Inc., Danfoss A/S, YUKEN KOGYO CO., LTD |

| Customization & Pricing | Available on Request (10% Customization Free) |