Reports

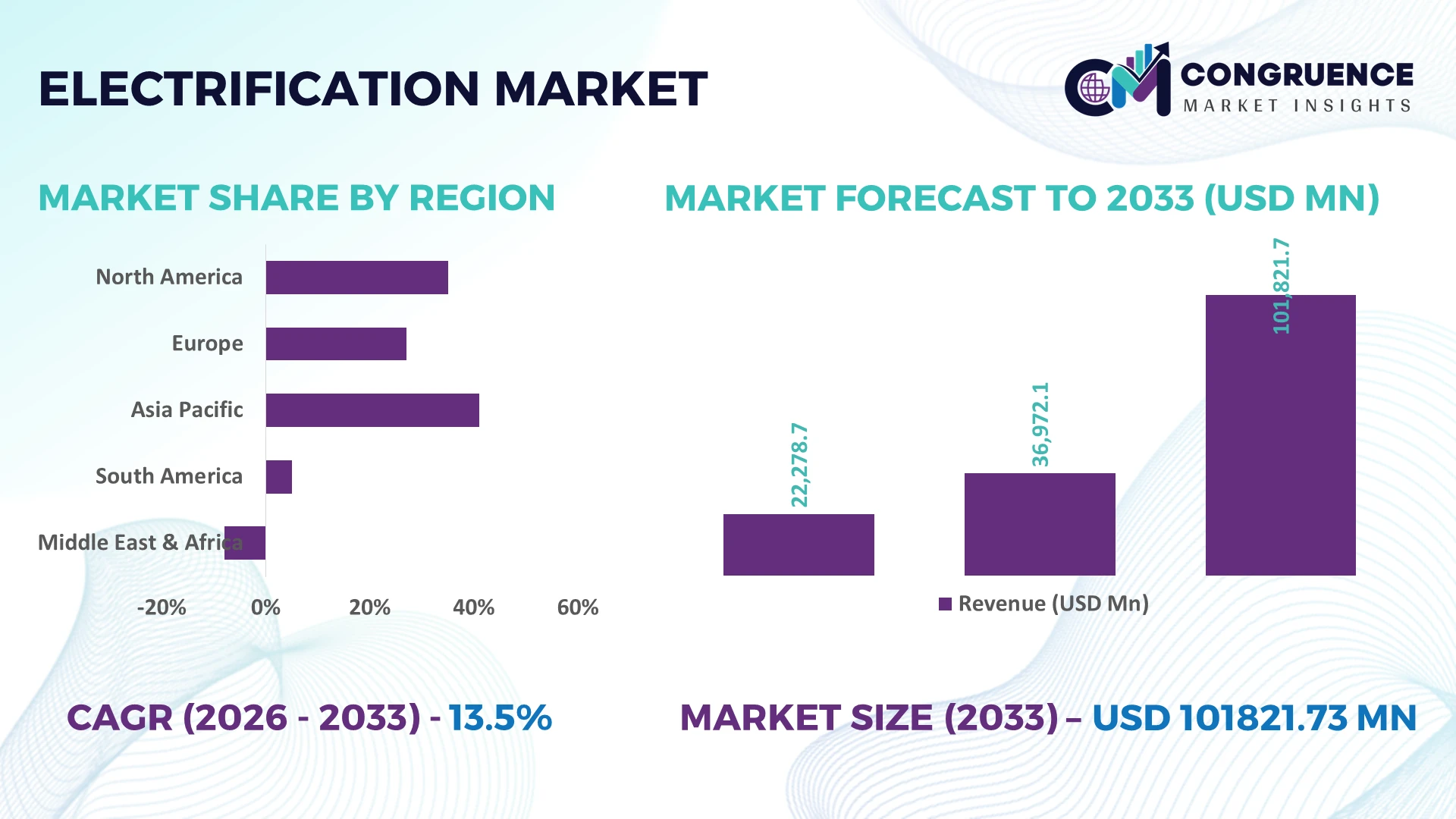

The Global Electrification Market was valued at USD 36972.05 Million in 2025 and is anticipated to reach a value of USD 101821.73 Million by 2033 expanding at a CAGR of 13.5% between 2026 and 2033. Grid modernization, industrial electrification, rapid electric vehicle infrastructure deployment, and expanding digital energy management systems are accelerating long-term market expansion across power, manufacturing, transportation, and commercial sectors.

China remains the dominant country, accounting for approximately 34% of global electrification deployment through large-scale investments in ultra-high-voltage transmission, battery manufacturing, and renewable integration. More than 60% of global lithium-ion battery production capacity supports domestic electrification initiatives, while the United States leads software-driven grid modernization and Europe advances industrial decarbonization under energy security priorities following the Russia-Ukraine conflict. This leadership strengthens technology commercialization and supply-chain resilience.

Strategic investments should prioritize integrated power infrastructure, digital grid technologies, and localized manufacturing ecosystems to secure long-term competitive positioning.

Market Size & Growth: USD 36972.05 Million (2025) to USD 101821.73 Million (2033) at 13.5% CAGR, supported by grid digitalization, EV charging expansion, and industrial automation.

Top Growth Drivers: Grid modernization (+28%), EV charging infrastructure (+24%), renewable power integration (+22%) remain the strongest demand catalysts.

Short-Term Forecast: By 2028, intelligent electrification solutions reduce operating costs by nearly 18% while improving energy efficiency by approximately 21%.

Emerging Technologies: AI-enabled energy management, digital substations, solid-state power electronics, and predictive maintenance improve system performance by over 25%.

Regional Leaders: Asia-Pacific exceeds USD 44 billion, Europe approaches USD 24 billion, and North America surpasses USD 22 billion, driven by industrial electrification and resilient grid investments.

Consumer/End-User Trends: More than 58% of industrial facilities prioritize electrified equipment to reduce energy consumption and improve operational reliability.

Pilot/Case Example: In 2025, smart industrial electrification projects achieved approximately 30% lower energy losses through advanced monitoring and automation platforms.

Competitive Landscape: Top manufacturers collectively hold nearly 38% market share, with ABB, Siemens, Schneider Electric, Eaton, and Hitachi Energy maintaining technology leadership.

Regulatory & ESG Impact: Carbon reduction policies improve clean electricity adoption by over 27%, accelerating infrastructure modernization and industrial compliance.

Investment & Funding: More than USD 40 billion supports transmission upgrades, manufacturing expansion, strategic partnerships, and regional supply-chain localization.

Innovation & Future Outlook: High-voltage DC systems, AI-driven energy optimization, and modular power infrastructure strengthen operational flexibility amid global supply-chain realignment.

Electrification Market demand continues expanding across industrial manufacturing, smart buildings, transportation infrastructure, and utility modernization as digital energy platforms become increasingly integrated. AI-enabled grid optimization and next-generation power electronics improve operational efficiency by nearly 24%, while localized component manufacturing gains momentum under evolving energy security regulations and resilient supply-chain strategies, establishing a strong foundation for the strategic market discussion.

Electrification has become a strategic priority as governments and industries modernize energy infrastructure, strengthen manufacturing resilience, and reduce dependence on fossil-fuel-based operations. Supply-chain localization, digital grid deployment, and industrial decarbonization initiatives are reshaping investment priorities across transportation, utilities, and heavy manufacturing. Companies increasingly compete through integrated electrification ecosystems that combine intelligent power distribution, energy storage, and automation rather than standalone electrical equipment, creating stronger long-term operational differentiation.

Modern digital electrification platforms equipped with AI-based energy management improve power utilization by approximately 20% while reducing maintenance costs by nearly 18% compared with conventional monitoring systems. China leads large-scale deployment through vertically integrated manufacturing and transmission expansion, whereas Germany emphasizes industrial automation and smart factory electrification with higher technology intensity. Over the next two to three years, intelligent grid assets are expected to represent more than 35% of newly commissioned power infrastructure, accelerating operational visibility and network flexibility.

A practical example is the deployment of smart substations integrated with predictive diagnostics, enabling utilities to reduce outage response times by nearly 30% while improving asset utilization. Companies are expanding technology partnerships, strengthening domestic component manufacturing, and investing in software-driven energy management platforms. Organizations that combine digital intelligence with scalable electrification infrastructure will secure stronger competitive positioning, operational resilience, and long-term market leadership.

Grid modernization and industrial electrification remain the strongest structural drivers as utilities and manufacturers replace aging electrical infrastructure with intelligent, connected systems. More than 42% of new substation projects now integrate digital monitoring, while AI-enabled energy optimization reduces transmission losses by approximately 15% and maintenance requirements by nearly 20%. The United States continues expanding grid resilience investments following increasing weather-related disruptions, encouraging utilities to deploy advanced distribution automation. Equipment manufacturers are responding through strategic acquisitions, software integration, and localized production facilities to shorten delivery cycles. A significant operational insight is that companies combining power hardware with digital analytics are securing higher-value service contracts and improving recurring revenue potential through lifecycle asset management.

Electrification deployment continues to face structural pressure from critical mineral supply concentration, grid connection delays, and infrastructure readiness. Approximately 70% of global lithium processing remains concentrated within limited supply networks, while transformer procurement lead times have increased by over 35% in several industrial markets. Grid congestion in countries including the United Kingdom and Canada delays large-scale industrial connections, affecting project scheduling and capital efficiency. Manufacturers are reducing exposure through localized sourcing strategies, long-term procurement agreements, and alternative battery chemistries that lower dependence on constrained materials. A key strategic insight is that supply-chain diversification increasingly influences project competitiveness as much as technology performance.

Next-generation electrification increasingly combines AI, digital twins, edge computing, and distributed energy resources into integrated operational ecosystems. Smart energy management platforms improve industrial energy efficiency by approximately 22%, while predictive asset analytics reduce unexpected equipment failures by nearly 28%. Japan continues investing in intelligent microgrid deployment to strengthen energy security and improve operational flexibility across industrial facilities. Technology providers are expanding software partnerships, investing in digital platforms, and developing interoperable power management architectures. A distinctive strategic opportunity lies in offering electrification as a managed service, enabling customers to optimize performance continuously instead of relying solely on capital-intensive equipment purchases.

Long-term competitiveness depends on successfully integrating increasingly complex electrical, digital, and communication systems across diverse infrastructure environments. More than 45% of industrial operators report interoperability challenges between legacy equipment and modern digital platforms, while cybersecurity incidents targeting operational technology environments have increased by roughly 25% in recent years. Germany and South Korea continue expanding workforce training initiatives to address shortages in power electronics, automation engineering, and cybersecurity expertise. Companies must strengthen digital security frameworks, invest in workforce development, and establish technology partnerships that simplify integration. Organizations capable of delivering standardized, secure, and scalable electrification platforms will achieve stronger deployment consistency and sustainable competitive advantage.

Digital Grid Intelligence Expands: Utilities are embedding AI-based monitoring and edge analytics into transmission and distribution networks, increasing fault detection accuracy by approximately 30% while reducing inspection time by nearly 25%. Grid operators in the United States are accelerating digital workflow integration following resilience mandates, prompting equipment suppliers to expand software partnerships and cloud-enabled asset management platforms that improve maintenance planning and network reliability.

Localized Manufacturing Gains Momentum: Supply-chain diversification is reshaping production strategies as manufacturers reduce dependency on single-country sourcing. Nearly 35% of new electrical equipment investments now include regional manufacturing or assembly capabilities, while component delivery times have improved by about 18% through localized procurement. Companies in India are expanding transformer, switchgear, and power electronics production through strategic partnerships to improve supply continuity and shorten project execution cycles.

Smart Infrastructure Integration Accelerates: Electrification projects increasingly combine charging infrastructure, distributed energy resources, and intelligent building controls within unified operational platforms. Integrated energy management lowers facility power consumption by roughly 20% and improves asset utilization by approximately 16%. Commercial developers are adopting interoperable automation systems, encouraging technology providers to restructure product portfolios around scalable digital ecosystems instead of standalone electrical hardware.

Predictive Service Models Evolve: Equipment suppliers are transitioning from product-focused delivery to lifecycle performance services using remote diagnostics and predictive maintenance. Digital monitoring decreases unexpected equipment failures by nearly 28% while improving maintenance productivity by approximately 22%. Rising shortages of skilled electrical technicians are driving automation investments, with companies expanding service contracts, remote support capabilities, and AI-assisted maintenance solutions to strengthen customer retention and operational resilience.

Industrial Electrification represents the leading segment because manufacturing facilities require continuous power optimization, automation integration, and energy efficiency improvements to remain globally competitive. Nearly 41% of large industrial modernization projects now include comprehensive electrification upgrades, while digital power management reduces operational energy losses by approximately 18%. Grid Electrification remains a mature foundation supporting reliable transmission expansion, whereas Building Electrification continues gaining traction through intelligent energy controls. Rural Electrification maintains strategic relevance by extending reliable electricity access and supporting decentralized economic development. Companies continue investing in advanced switchgear, intelligent substations, and integrated power management platforms to strengthen operational performance.

Transport Electrification is the fastest-growing type as charging infrastructure expansion, fleet electrification, and battery ecosystem development reshape mobility investments. Adoption of commercial electric transport systems has increased by approximately 26% across logistics operations, encouraging manufacturers to strengthen charging partnerships and develop higher-capacity power infrastructure. Investment priorities increasingly favor integrated solutions combining industrial operations, transportation networks, and digital energy management, enabling companies to deliver broader infrastructure ecosystems instead of isolated electrical products.

Power Distribution remains the dominant application because every electrification initiative depends on resilient transmission, substations, and intelligent distribution infrastructure. More than 45% of infrastructure modernization budgets prioritize digital distribution assets, while automated switching systems reduce outage restoration times by nearly 25%. Renewable Energy integration continues expanding alongside distribution upgrades, and Manufacturing applications increasingly deploy intelligent power quality systems to stabilize automated production environments. Companies are scaling digital substations, protection systems, and real-time monitoring technologies to improve operational continuity.

Electric Vehicles represent the fastest-growing application as charging ecosystem deployment accelerates across commercial fleets and public infrastructure. Fast-charging network installations have expanded by approximately 30%, while integrated energy management improves charging efficiency by around 17%. Smart Buildings continue increasing demand through connected energy optimization and automated controls that reduce operating costs. Technology providers are expanding software integration, charging partnerships, and interoperable platforms to support converged infrastructure across transportation, buildings, and distributed power systems.

Utilities remain the dominant end-user because they operate transmission networks, distribution systems, and critical grid infrastructure supporting every electrification deployment. Approximately 48% of large utility capital programs now prioritize digital substations, intelligent grid automation, and network resilience upgrades, while predictive maintenance lowers equipment downtime by nearly 20%. Industrial users remain significant adopters through factory modernization initiatives, whereas Government investments continue supporting national grid resilience and public infrastructure modernization. Companies increasingly customize integrated hardware-software solutions and long-term service agreements for utility operators.

Transportation is the fastest-growing end-user segment as public transit agencies, logistics providers, and fleet operators accelerate charging infrastructure deployment and vehicle electrification. Fleet electrification projects have increased by roughly 27%, encouraging suppliers to expand charging ecosystems, financing partnerships, and energy management services. Commercial facilities continue adopting intelligent electrical systems to improve operational efficiency, while Residential demand steadily expands through home energy management and distributed power technologies. Competitive strategies increasingly emphasize ecosystem partnerships, digital platforms, and sector-specific electrification solutions tailored to operational requirements.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 15.2% CAGR between 2026 and 2033.

Grid resilience and digital infrastructure modernization drive competitive advantage

North America remains a technology-intensive electrification market, supported by advanced transmission upgrades, industrial automation, and expanding electric mobility infrastructure. The region contributes approximately 24% of global deployment activity, with utilities prioritizing intelligent substations, distributed energy management, and cybersecurity-enabled grid operations. More than 40% of newly commissioned utility projects now integrate digital monitoring and predictive diagnostics, improving network reliability and maintenance efficiency. Industrial manufacturers continue expanding electrified production facilities while technology providers strengthen software-hardware integration through strategic collaborations, enabling utilities and enterprises to optimize operational performance across increasingly complex power networks.

United States Market Outlook: The United States leads regional electrification through extensive transmission modernization, domestic manufacturing expansion, and advanced grid digitalization. More than 55% of large utility infrastructure programs incorporate AI-enabled monitoring and automated grid controls. Federal incentives continue supporting domestic production of transformers, batteries, and power electronics, encouraging companies to localize supply chains, strengthen manufacturing resilience, and accelerate deployment of intelligent electrical infrastructure across industrial and commercial sectors.

Industrial decarbonization reshapes infrastructure investment priorities

Europe maintains strong electrification momentum through industrial decarbonization policies, intelligent grid deployment, and advanced building modernization. The region represents nearly 22% of global market activity, with utilities integrating renewable generation into digitally managed transmission systems. More than 38% of industrial facilities are adopting intelligent electrical management platforms to improve energy efficiency and operational flexibility. Equipment suppliers increasingly prioritize interoperable power systems and digital protection technologies while utilities expand cross-border electricity infrastructure to strengthen long-term energy security and improve network resilience.

Germany Market Outlook: Germany remains Europe's operational leader due to its advanced industrial manufacturing ecosystem and smart factory transformation initiatives. Around 45% of major industrial modernization projects include integrated electrification and digital automation technologies. Domestic engineering companies continue expanding intelligent switchgear, industrial power electronics, and grid management solutions, strengthening the country's position as a technology development hub supporting high-performance industrial electrification.

Manufacturing scale and infrastructure expansion sustain leadership

Asia-Pacific dominates the global electrification landscape through unmatched manufacturing capacity, large-scale infrastructure deployment, and integrated supply-chain ecosystems. The region accounts for approximately 43.8% of market activity, supported by extensive investment in transmission networks, electric mobility infrastructure, and industrial modernization. More than 60% of global battery manufacturing capacity is concentrated within the region, while large-scale grid expansion continues supporting industrial growth. Companies are expanding production facilities, strengthening regional supplier networks, and integrating digital energy management technologies to improve operational efficiency and shorten project delivery timelines.

China Market Outlook: China remains the most influential national market owing to its vertically integrated manufacturing ecosystem, ultra-high-voltage transmission expansion, and leadership in battery production. Approximately one-third of global electrification equipment manufacturing capacity is located in China, enabling cost-efficient production and rapid deployment. Domestic enterprises continue investing in intelligent grid infrastructure, industrial automation, and advanced power electronics, reinforcing global competitiveness across the electrification value chain.

Infrastructure expansion strengthens industrial connectivity

South America is steadily expanding electrification through transmission upgrades, renewable energy integration, and industrial infrastructure development. The region contributes approximately 6% of global deployment activity, with governments prioritizing grid expansion and rural connectivity to improve electricity reliability. Utility modernization projects have increased by nearly 19% over recent years, although transmission bottlenecks and financing constraints continue affecting implementation speed. Equipment suppliers are responding through localized partnerships, engineering services, and modular electrical solutions that improve deployment flexibility while supporting industrial and commercial power demand.

Brazil Market Outlook: Brazil leads regional electrification through its extensive electricity network, renewable generation capacity, and expanding industrial sector. Large utilities continue modernizing substations and transmission infrastructure while manufacturers invest in digital power management technologies for mining, manufacturing, and commercial operations. Grid automation programs increasingly improve operational efficiency, supporting stronger integration between renewable generation assets and industrial electricity demand.

Strategic infrastructure investment accelerates modernization

The Middle East & Africa is emerging as the fastest-developing electrification region through major infrastructure investments, industrial diversification, and smart city development. The region accounts for roughly 4% of global market activity, with governments prioritizing transmission expansion, intelligent distribution systems, and utility modernization. More than 20% of recently announced infrastructure programs include advanced electrical automation and digital energy management components. International technology providers are expanding engineering partnerships and localized manufacturing capabilities to support large-scale power infrastructure deployment across rapidly developing economies.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through ambitious infrastructure modernization, industrial diversification, and smart city initiatives. Large utility operators continue deploying intelligent substations, digital transmission monitoring, and high-capacity distribution systems supporting industrial expansion. National development programs are accelerating electrification across manufacturing, commercial infrastructure, and transport networks, encouraging global technology companies to establish regional partnerships and localized operational capabilities.

The Electrification Market is led by ABB, Siemens, Schneider Electric, Eaton, and Hitachi Energy, competing directly against diversified regional manufacturers and specialized power technology providers. Global leaders challenge regional suppliers through integrated digital platforms, while component manufacturers compete with OEMs on delivery speed and localized production. The top five companies collectively control approximately 38% of the market, maintaining leadership through advanced grid technologies and broad product portfolios. Competition increasingly centers on digital intelligence, lifecycle services, and resilient supply chains rather than equipment pricing alone. AI-enabled energy management improves operational efficiency by nearly 20%, localized manufacturing reduces delivery times by approximately 18%, and predictive maintenance lowers service costs by about 22%. Companies are expanding manufacturing capacity, forming software partnerships, and vertically integrating power electronics and automation capabilities to secure supply continuity. Technology convergence and strategic acquisitions continue reshaping competitive positioning, while certification requirements, grid interoperability, and capital-intensive manufacturing remain significant entry barriers. Winning requires scalable digital solutions, resilient supply networks, rapid deployment capability, and integrated hardware-software ecosystems delivering measurable operational value.

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Hitachi Energy Ltd.

Mitsubishi Electric Corporation

General Electric Vernova

Legrand SA

Rockwell Automation, Inc.

Emerson Electric Co.

Toshiba Corporation

Honeywell International Inc.

Fuji Electric Co., Ltd.

Delta Electronics, Inc.

Digital electrification platforms are replacing conventional hardware-centric architectures with software-defined energy management, AI-driven analytics, and intelligent power electronics. More than 46% of newly deployed utility infrastructure now incorporates digital monitoring, while AI-assisted optimization improves grid efficiency by approximately 20% and reduces maintenance interventions by nearly 18%. Utilities and industrial operators increasingly integrate cloud-based asset management with edge computing to improve system visibility, operational resilience, and decision-making speed.

Wide-bandgap semiconductors, digital substations, and solid-state transformers are emerging as the next generation of electrification technologies. Compared with conventional silicon-based systems, silicon carbide and gallium nitride power devices improve energy conversion efficiency by around 12% while reducing thermal losses by approximately 25%. Adoption across high-performance industrial and electric mobility applications has exceeded 35% in advanced manufacturing economies. Equipment manufacturers and technology integrators benefit most by delivering higher-performance, lower-maintenance electrical infrastructure supporting complex industrial operations.

Between 2026 and 2028, autonomous grid management, digital twins, and interoperable energy platforms will become core competitive differentiators. Companies investing in predictive analytics, cybersecurity-enabled electrical infrastructure, and standardized communication protocols will accelerate deployment consistency and reduce commissioning times by nearly 15%. Organizations acting now gain stronger operational flexibility, faster customer integration, and greater resilience against evolving grid complexity and supply-chain disruptions.

October 2024: Schneider Electric launched next-generation Smart Grid solutions at Enlit Europe, expanding DERMS capabilities with utility partners to improve grid flexibility and resilience. The platform enables up to 30% faster grid response for distributed energy integration, strengthening digital utility operations. Source: se.com

January 2025: Hitachi Energy secured a strategic supply agreement with Siemens Mobility to deliver 360 RESIBLOC® onboard traction transformers for Munich's new S-Bahn fleet. The deployment improves rail energy efficiency while supporting 90 next-generation trains, reinforcing sustainable transportation electrification. Source: hitachienergy.com

August 2025: ABB India received a ₹173.55 crore order from Siemens Gamesa Renewable Power to manufacture wind turbine converters and electrical cabinets from its Nelamangala facility. The expansion strengthens localized renewable electrification manufacturing and supports domestic supply-chain resilience. Source: economictimes.indiatimes.com

May 2026: Siemens introduced the latest Gridscale X platform with AI-powered transmission planning, enabling utilities to reduce connection study response times by up to 50% through digital twin integration and advanced automation, accelerating intelligent grid deployment for expanding electricity demand. Source: press.siemens.com

The report provides comprehensive analysis of the global Electrification Market across Grid Electrification, Transport Electrification, Building Electrification, Industrial Electrification, and Rural Electrification. It evaluates demand across Power Distribution, Electric Vehicles, Smart Buildings, Manufacturing, Renewable Energy, and major end-user groups including utilities, industrial enterprises, transportation, residential, commercial, and government sectors. The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining deployment trends, technology adoption, manufacturing capacity, and competitive positioning across more than 10 leading industry participants.

The study delivers strategic insights into digital grid technologies, AI-enabled energy management, intelligent substations, power electronics, distributed energy integration, and smart infrastructure modernization. It highlights deployment patterns, segment leadership, enterprise investment priorities, localization strategies, and emerging electrification ecosystems expected to shape business expansion between 2026 and 2033. The report supports investment planning, product development, competitive benchmarking, partnership evaluation, regional expansion, and long-term decision-making through detailed operational, technology, and industry intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

C111% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

T1 |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

mplayers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |