Reports

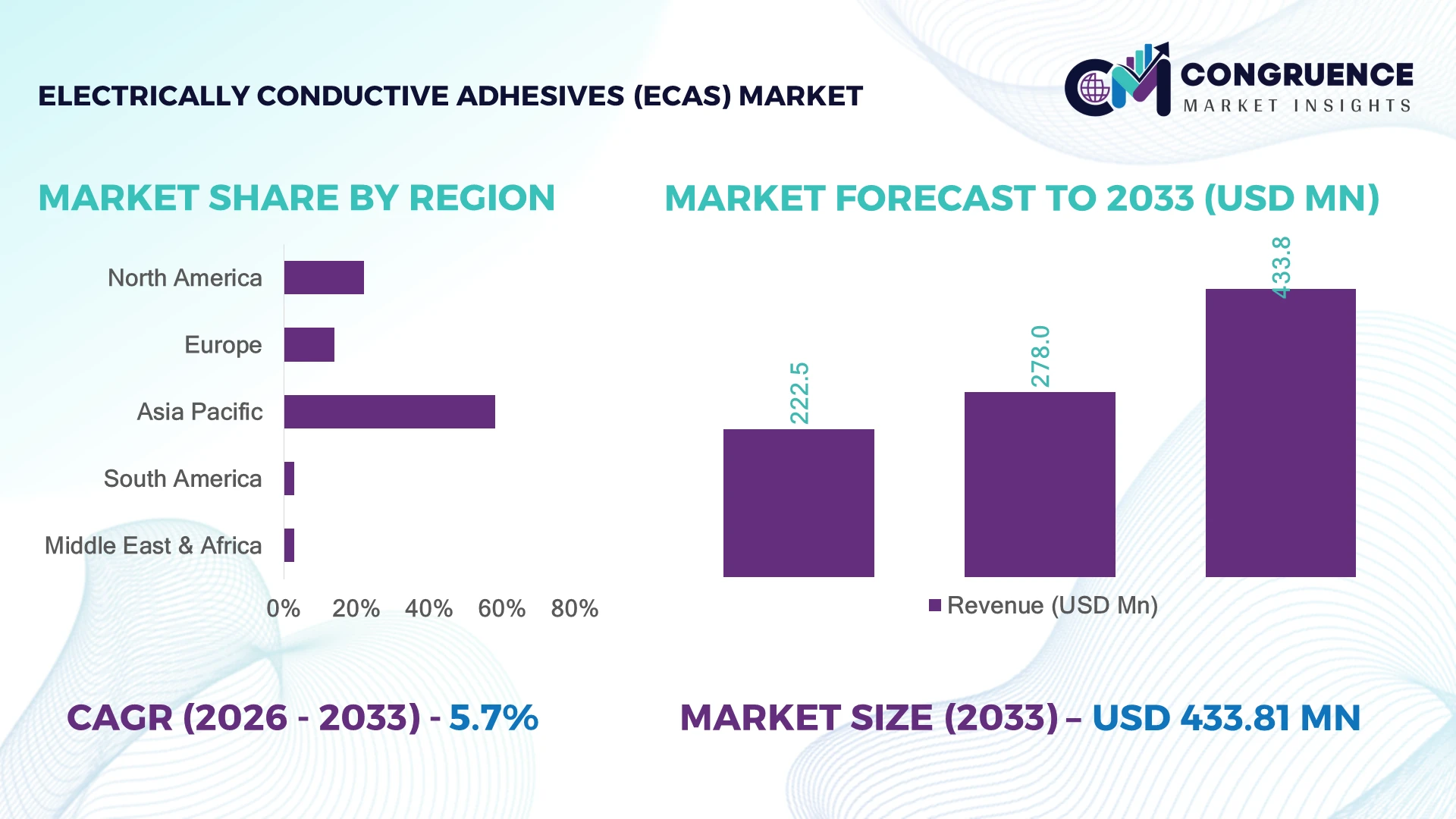

The Global Electrically Conductive Adhesives (ECAs) Market was valued at USD 278.0 Million in 2025 and is anticipated to reach a value of USD 433.8 Million by 2033 expanding at a CAGR of 5.72% between 2026 and 2033. Growth is driven by rising adoption of silver-filled adhesives in semiconductor packaging, flexible electronics, EV battery systems, and lightweight electronic assemblies replacing traditional soldering technologies.

Asia-Pacific dominates the market, accounting for nearly 58% of global consumption, supported by large-scale electronics manufacturing hubs in China, Japan, South Korea, and Taiwan. China’s semiconductor and EV supply chains attract over USD 100 billion annually in advanced electronics investments, while Japan leads in precision adhesive technologies with more than 40% adoption in high-reliability electronic applications. Compared with North America’s expanding EV and aerospace demand, Asia-Pacific maintains a stronger manufacturing advantage through integrated supply networks and high-volume production capacity.

Strategic implication: Companies strengthening regional manufacturing partnerships and advanced material capabilities are positioned to capture the next wave of electronics miniaturization and electrification demand.

Market Size & Growth: USD 278.0 Million in 2025 to USD 433.8 Million by 2033 at 5.72% CAGR, driven by semiconductor miniaturization and EV electronics adoption.

Top Growth Drivers: EV electronics integration (+35%), semiconductor packaging demand (+30%), flexible electronics adoption (+25%) shaping market expansion.

Short-Term Forecast: By 2028, advanced ECAs reduce assembly energy consumption by 15% and improve component reliability by 20% in high-performance electronics.

Emerging Technologies: AI-driven material design, automated adhesive dispensing, nano-silver formulations, and low-temperature curing technologies accelerate innovation.

Regional Leaders: Asia-Pacific reaches USD 250 Million+ by 2033 with electronics expansion; North America exceeds USD 100 Million through EV adoption; Europe advances with sustainable electronics manufacturing.

Consumer/End-User Trends: Over 60% of electronics manufacturers prioritize lightweight bonding solutions for compact and energy-efficient devices.

Pilot/Case Example: 2024 automotive electronics projects using conductive adhesives achieved up to 25% assembly weight reduction compared with conventional solder-based processes.

Competitive Landscape: Henkel leads with approximately 20% share, followed by 3M, Dow, DuPont, Panacol, and H.B. Fuller in advanced adhesive solutions.

Regulatory & ESG Impact: Lead-free electronics regulations and sustainability initiatives drive adoption, reducing hazardous material usage by more than 10% in manufacturing processes.

Investment & Funding: Over USD 500 Million invested globally in advanced electronic materials, focusing on semiconductor supply-chain localization and production expansion.

Innovation & Future Outlook: Next-generation ECAs combine nanomaterials, thermal management, and automation to strengthen strategic positioning across EV, aerospace, and electronics sectors.

Electrically Conductive Adhesives (ECAs) are becoming essential materials for advanced electronics requiring compact designs, thermal stability, and reliable electrical connections. Demand is accelerating in semiconductor interconnects, wearable devices, and EV power modules, with silver-based formulations representing more than 70% of commercial conductive adhesive usage. Recent supply-chain restructuring in semiconductor manufacturing and regional electronics expansion across Asia and North America are encouraging localized adhesive production and innovation partnerships.

Electrically Conductive Adhesives (ECAs) are becoming strategically important as industries transition toward smaller, lighter, and more energy-efficient electronic systems. The shift from traditional soldering toward advanced bonding technologies is reshaping semiconductor packaging, automotive electronics, and renewable energy components. Global supply-chain restructuring after semiconductor shortages has accelerated regional investments in localized materials production and resilient electronics ecosystems.

Advanced ECAs provide measurable advantages over conventional solder systems, including lower processing temperatures by nearly 40% and improved compatibility with heat-sensitive components. Silver-filled adhesives dominate high-performance applications, while emerging copper and hybrid formulations focus on reducing material costs and improving conductivity. Asia-Pacific leads in manufacturing scale, whereas North America and Europe emphasize innovation, EV applications, and sustainable production methods.

Companies are expanding partnerships with semiconductor manufacturers, automotive suppliers, and electronics producers to strengthen deployment capabilities. For example, EV battery module manufacturers increasingly integrate conductive adhesives for improved thermal management and reduced assembly complexity. Over the next few years, investment priorities will center on automation, material efficiency, and localized production networks.

The strategic advantage will belong to companies that combine advanced adhesive chemistry with scalable manufacturing, enabling stronger competitiveness across electrification, semiconductor, and next-generation electronics markets.

The rapid transition toward miniaturized electronic assemblies and high-density semiconductor packaging is reinforcing demand for electrically conductive adhesives across automotive, consumer electronics, and industrial applications. More than 70% of advanced ECAs incorporate silver-based conductive fillers, while nearly 45% of new EV electronic control modules increasingly utilize conductive adhesives to reduce thermal stress and improve component reliability. China's continued investment in domestic semiconductor manufacturing and the implementation of the U.S. CHIPS and Science Act are expanding advanced packaging capacity, strengthening demand for high-performance bonding materials. In response, manufacturers are expanding conductive adhesive portfolios, investing in low-temperature curing formulations, and forming partnerships with semiconductor packaging specialists. A key strategic advantage lies in enabling lightweight, lead-free electronic assembly while improving manufacturing throughput and long-term product reliability.

Market expansion remains constrained by heavy dependence on silver, whose pricing directly influences conductive adhesive production economics. Silver typically accounts for 60–80% of conductive filler content, and raw material expenses can represent nearly 50% of total formulation costs for premium ECAs. Supply disruptions caused by mining fluctuations and geopolitical trade restrictions continue to pressure procurement strategies, particularly for manufacturers in Japan and Germany. These cost pressures reduce pricing flexibility, compress margins, and slow adoption among cost-sensitive electronics producers. Companies are responding by diversifying supplier networks, negotiating long-term procurement contracts, and accelerating development of copper-based and hybrid conductive formulations. An important operational insight is that material substitution has become as strategically important as product innovation in maintaining manufacturing competitiveness.

Next-generation wearable electronics, printed sensors, and flexible display technologies are opening high-value opportunities for conductive adhesive suppliers beyond traditional semiconductor applications. More than 35% of emerging flexible electronic devices now require low-temperature conductive bonding, while printable electronics manufacturing is improving production efficiency by nearly 20% compared with conventional assembly techniques. South Korea and Taiwan continue investing heavily in flexible display manufacturing, supported by national advanced electronics initiatives and automation programs. Leading material suppliers are expanding R&D partnerships with display manufacturers and printed electronics developers to commercialize stretchable conductive adhesives with enhanced conductivity and durability. A distinctive strategic opportunity lies in designing multifunctional adhesives that combine electrical conductivity, thermal management, and mechanical flexibility within a single material platform.

Maintaining consistent electrical conductivity, mechanical durability, and thermal stability across high-volume manufacturing remains a significant long-term execution challenge. Process variability can influence joint resistance by 10–15%, while nearly 30% of quality-control inspections in advanced electronic assembly focus on conductive interconnection integrity. As semiconductor nodes become increasingly compact, manufacturers in the United States and Taiwan face tighter production tolerances and stricter qualification standards for adhesive materials. Companies must strengthen process automation, inline inspection technologies, and advanced material characterization while collaborating with equipment suppliers to standardize manufacturing performance. The strongest competitive position will belong to suppliers capable of delivering highly repeatable conductive performance across multiple electronic platforms without compromising production efficiency or product lifespan.

Low-Temperature Bonding Shift: Electronics manufacturers are accelerating adoption of low-temperature curing ECAs, with usage increasing by nearly 25% in heat-sensitive applications such as flexible circuits and advanced sensors. The shift is reducing thermal damage risks by approximately 15% while improving assembly efficiency. Companies in Japan and South Korea are scaling automated dispensing systems and partnering with material specialists to optimize high-volume production.

Nano-Enhanced Formulation Growth: Conductive adhesive producers are integrating nano-silver and hybrid filler technologies, improving electrical performance by nearly 20% compared with conventional formulations. Around 35% of new R&D programs now focus on advanced filler structures, driven by semiconductor complexity and miniaturization. Companies are expanding laboratory-to-production pipelines to commercialize durable, high-conductivity materials.

Localized Supply Chain Expansion: Semiconductor supply-chain restructuring is pushing manufacturers to localize adhesive production, with approximately 30% of electronics suppliers increasing regional sourcing strategies since recent global component shortages. The United States and China are expanding domestic materials ecosystems to reduce dependency risks. Companies are investing in regional plants, supplier diversification, and long-term material agreements.

Automated Adhesive Processing Adoption: Advanced electronics factories are deploying automated dispensing and inspection technologies, improving material utilization by 10–18% and reducing production inconsistencies. Labor shortages in manufacturing hubs are accelerating automation adoption, particularly in Taiwan’s semiconductor ecosystem. Companies are integrating AI-based quality monitoring and smart production platforms to improve yield stability and operational control.

Silver-based electrically conductive adhesives represent the leading type segment due to superior conductivity, thermal stability, and established compatibility with semiconductor and electronic assembly processes. These formulations account for approximately 70% of commercial ECA applications, supported by widespread use in automotive electronics, consumer devices, and semiconductor packaging. Their mature supply chain and proven reliability continue attracting manufacturers requiring consistent performance at scale. Companies such as Henkel, DuPont, and 3M are strengthening product portfolios through improved curing technologies and enhanced thermal management capabilities. Copper-based and hybrid conductive adhesives are emerging as the fastest-growing types as manufacturers seek cost-efficient alternatives to silver materials. Copper formulations can reduce filler costs by nearly 30–40%, while hybrid technologies improve conductivity and mechanical flexibility. Other conductive adhesive types remain relevant in specialized applications requiring customized electrical or environmental performance. Investment priorities are shifting toward materials that balance conductivity, affordability, and supply-chain resilience.

Semiconductor packaging and assembly represent the leading application area for electrically conductive adhesives due to increasing demand for compact, high-performance electronic components. Advanced packaging applications contribute nearly 45% of ECA consumption, supported by rising chip integration requirements in automotive systems, computing devices, and communication equipment. Manufacturers are adopting ECAs to improve component reliability, reduce thermal stress, and support smaller device architectures. Companies are expanding partnerships with semiconductor manufacturers to develop specialized adhesives for next-generation packaging platforms. Electronic displays, photovoltaic modules, automotive electronics, and other emerging applications are expanding rapidly as industries transition toward lightweight and energy-efficient systems. Automotive electronics adoption is increasing by approximately 25% as EV manufacturers integrate more power control modules and sensors. Display manufacturers in South Korea and Taiwan are adopting flexible conductive bonding solutions to improve production flexibility. Remaining applications continue benefiting from demand for durable, low-profile electrical connections.

Electronics manufacturers represent the dominant end-user segment due to large-scale requirements across smartphones, computing devices, semiconductor systems, and industrial electronics. This group accounts for approximately 60% of ECA demand, driven by high-volume production environments and increasing component density. Major manufacturers in China, Taiwan, and South Korea are integrating conductive adhesives into automated assembly workflows to improve reliability and reduce processing complexity. Companies are responding through customized formulations, technical partnerships, and application-specific solutions. Automotive manufacturers are the fastest-growing end-user group as electric vehicles and advanced driver-assistance systems increase electronic content per vehicle. Automotive adoption of conductive adhesives is expanding by nearly 30% as manufacturers prioritize lightweight assemblies and improved thermal performance. Aerospace, renewable energy, and industrial equipment users continue adopting ECAs for specialized reliability requirements. Suppliers are developing dedicated automotive-grade products and strengthening collaborations with EV component producers.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America accounted for approximately 22% of the global Electrically Conductive Adhesives (ECAs) Market in 2025, supported by semiconductor reshoring, electric vehicle manufacturing, and aerospace electronics demand. The United States represents the largest contributor, driven by investments in domestic chip production and advanced packaging capabilities. More than 50 semiconductor manufacturing projects have been announced across the region, increasing demand for high-performance bonding materials. Automotive and electronics companies are adopting ECAs to improve lightweight assembly and thermal performance. Suppliers are expanding local production capacity and forming partnerships with semiconductor and EV manufacturers to reduce supply-chain dependency.

United States Market Outlook: The United States leads North American demand due to strong semiconductor, aerospace, and EV ecosystems. Domestic electronics manufacturing initiatives are accelerating adoption, with advanced packaging facilities increasingly integrating conductive adhesives for high-reliability applications. More than 40% of new semiconductor investments in the region focus on improving domestic manufacturing resilience, creating long-term opportunities for ECA suppliers.

Europe accounted for approximately 14% of the global Electrically Conductive Adhesives (ECAs) Market in 2025, supported by automotive electrification, renewable energy systems, and strict environmental regulations promoting lead-free assembly technologies. Germany, France, and Italy represent key demand centers due to established automotive and industrial electronics manufacturing. Nearly 35% of European automotive production output is connected to electrification-focused programs, increasing demand for advanced electronic bonding solutions. Companies are investing in sustainable adhesive formulations, localized manufacturing, and partnerships with automotive suppliers to improve supply reliability and meet environmental compliance requirements.

Germany Market Outlook: Germany remains Europe’s largest ECA market due to its automotive engineering base and industrial automation leadership. The country’s EV manufacturing expansion and advanced vehicle electronics integration are increasing demand for conductive bonding materials. More than 60% of German automotive suppliers are actively investing in electrification-related technologies, supporting long-term adoption of specialized adhesives.

Asia-Pacific accounted for approximately 58% of the global Electrically Conductive Adhesives (ECAs) Market in 2025, maintaining leadership through semiconductor production, consumer electronics manufacturing, and EV supply-chain integration. China, Japan, South Korea, and Taiwan collectively represent the majority of regional consumption due to high-volume electronics assembly. China alone contributes more than 30% of global electronics manufacturing capacity, supporting extensive ECA adoption. Companies are expanding production facilities, developing advanced formulations, and establishing collaborations with semiconductor packaging firms to support next-generation devices. The region’s integrated supplier networks provide a major cost and scalability advantage.

China Market Outlook: China dominates Asia-Pacific demand through its extensive electronics manufacturing infrastructure and growing EV ecosystem. The country accounts for over 50% of global EV production, increasing demand for conductive adhesives used in battery systems, sensors, and electronic modules. Local manufacturers are expanding material capabilities to strengthen domestic supply chains and reduce dependency on imported specialty chemicals.

South America accounted for approximately 3% of the global Electrically Conductive Adhesives (ECAs) Market in 2025, with adoption concentrated in Brazil, Argentina, and Chile. Growth is supported by automotive electronics, renewable energy projects, and gradual industrial automation development. Brazil represents the largest market due to its automotive manufacturing base and expanding electronics assembly sector. Approximately 20% of regional electronics demand is linked to industrial and automotive applications requiring advanced bonding solutions. Companies are focusing on distributor partnerships, localized supply networks, and application-specific solutions to overcome limited domestic production capacity.

Brazil Market Outlook: Brazil is the leading South American market due to its automotive manufacturing scale and industrial electronics demand. The country’s automotive sector produces more than 2 million vehicles annually, creating opportunities for conductive adhesive applications in electronic control systems and electrified vehicle components. Suppliers are strengthening local partnerships to improve availability and technical support.

Middle East & Africa accounted for approximately 3% of the global Electrically Conductive Adhesives (ECAs) Market in 2025, with demand emerging from telecommunications, renewable energy, aerospace, and industrial modernization projects. The United Arab Emirates, Saudi Arabia, and South Africa represent key adoption centers due to investments in advanced infrastructure and technology manufacturing. More than 25% of new industrial modernization projects in major Gulf economies incorporate advanced automation and electronic systems requiring reliable bonding technologies. Companies are building regional partnerships and improving distribution networks to support specialized material adoption.

United Arab Emirates Market Outlook: The UAE represents the strongest market position in the region due to investments in smart infrastructure, electronics systems, and advanced manufacturing initiatives. Technology-focused industrial projects and semiconductor ecosystem development programs are increasing demand for high-performance adhesives. The country’s manufacturing diversification strategy is encouraging partnerships with global material suppliers and electronics companies.

The Electrically Conductive Adhesives (ECAs) market features global material leaders such as Henkel, 3M, DuPont, and H.B. Fuller competing against regional specialists and cost-focused conductive material suppliers. The top five players collectively control approximately 55% of the market, creating a moderately consolidated structure. Competition centers on formulation performance, customization, supply reliability, and production scalability, with premium suppliers investing 15–25% more in advanced material development than cost-focused competitors. Companies compete through electronics partnerships, localized manufacturing, and nano-material innovation. The market is shifting toward sustainable formulations, copper-based alternatives, and AI-assisted material design. High qualification requirements, customer validation cycles, and specialized manufacturing expertise create strong entry barriers. Winning requires superior technology, dependable supply chains, application expertise, and rapid collaboration with electronics manufacturers.

3M

DuPont

H.B. Fuller

Panacol-Elosol GmbH

DELO Industrial Adhesives

Dow

Avery Dennison

Bostik

NAMICS Corporation

Creative Materials Inc.

Master Bond Inc.

Electrically conductive adhesive technology is advancing through nano-silver fillers, copper hybrid formulations, low-temperature curing chemistry, and automated dispensing systems. Silver-based ECAs maintain dominance with over 70% adoption in commercial applications, while emerging copper-based solutions reduce material costs by approximately 30%. Compared with traditional soldering, advanced ECAs lower processing temperatures by nearly 40%, improving compatibility with flexible electronics and heat-sensitive components.

AI-assisted formulation design and digital simulation platforms are accelerating adhesive development by reducing testing cycles by around 20%. Manufacturers are integrating automated inspection, smart dispensing equipment, and real-time quality monitoring to improve production consistency. Semiconductor packaging, EV electronics, and wearable devices are becoming primary deployment areas as companies prioritize lightweight and durable interconnection methods.

Between 2026 and 2028, competitive advantage will shift toward suppliers combining material innovation with scalable manufacturing. Companies investing in recyclable formulations, hybrid conductive fillers, and regional production networks will benefit most. The strongest performers will be those enabling higher reliability, faster assembly, and improved cost efficiency across next-generation electronics ecosystems.

February 2025 Henkel launched an Application Engineering Center in Chennai and expanded electronics manufacturing near Pune, India, improving localized support and supply resilience. The expansion strengthens electronics material capabilities under regional diversification strategies. Source: www.henkel.com

November 2024 DuPont showcased advanced electronics solutions at Electronica 2024, including interconnect and thermal management technologies. The portfolio emphasized flexible electronics and reliability improvements across automotive and semiconductor applications. Source: www.dupont.com

April 2025 Henkel introduced AI-enabled adhesive development tools and battery-related bonding innovations, targeting faster design cycles and improved EV component performance. The company highlighted digital simulation capabilities supporting advanced manufacturing efficiency. Source: www.henkel.in

May 2025 Henkel partnered with Sasol on lower-carbon adhesive materials, achieving a reported 35% product carbon footprint reduction through advanced material integration. The collaboration demonstrates increasing sustainability focus across adhesive value chains.

The Electrically Conductive Adhesives (ECAs) Market Report covers comprehensive analysis across types, applications, end-users, technologies, and major geographic markets. The study evaluates silver-based, copper-based, hybrid, and other conductive adhesive formulations along with applications including semiconductor packaging, automotive electronics, displays, photovoltaic systems, and industrial electronic assemblies.

The report examines adoption trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing shifts, supply-chain developments, innovation priorities, and competitive strategies. It analyzes participation from global adhesive manufacturers, electronic material suppliers, and technology innovators. The coverage supports investment planning, expansion decisions, partnership strategies, and competitive positioning through 2033 by identifying emerging opportunities in automation, flexible electronics, EV systems, and next-generation semiconductor manufacturing.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 278.0 Million |

| Market Revenue (2033) | USD 433.8 Million |

| CAGR (2026–2033) | 5.72% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Henkel; 3M; DuPont; H.B. Fuller; Panacol-Elosol GmbH; DELO Industrial Adhesives; Dow; Avery Dennison; Bostik; NAMICS Corporation; Creative Materials Inc.; Master Bond Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |