Reports

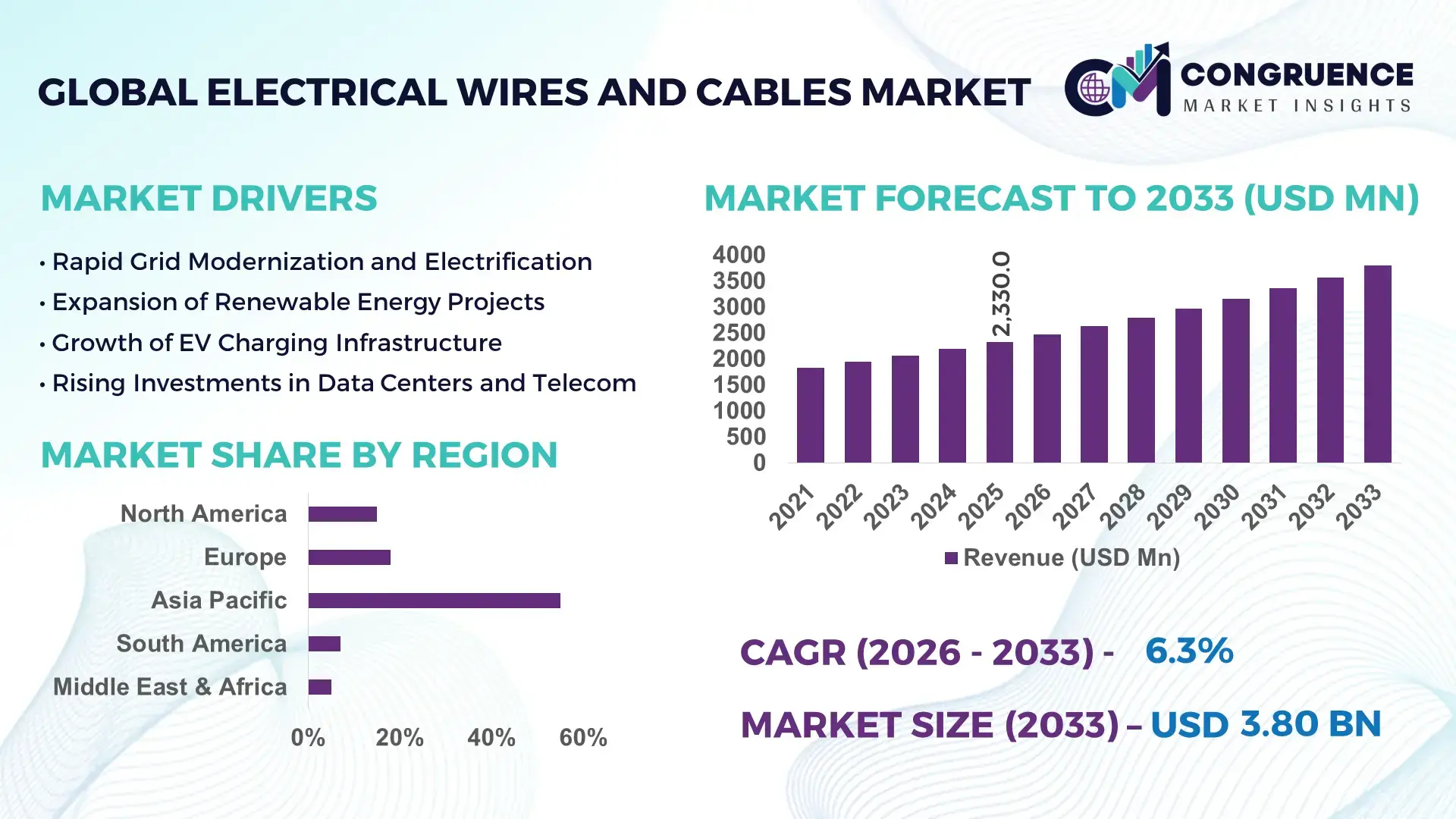

The Global Electrical Wires and Cables Market was valued at USD 2,330.0 Million in 2025 and is anticipated to reach a value of USD 3,798.6 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033, according to an analysis by Congruence Market Insights—driven by accelerating grid modernization, electrification of transport, and industrial automation.

China remains the most influential production hub for electrical wires and cables. The country operates more than 1,200 large-scale cable manufacturing facilities, collectively producing over 25 million tons of copper and aluminum cable annually. China’s ultra-high-voltage (UHV) transmission network now exceeds 45,000 km, requiring continuous upgrades in high-performance conductors and insulation materials. Industrial investment in smart cable manufacturing surpassed USD 8 billion in 2023–2024, focused on automated extrusion lines, digital quality control, and recyclable insulation compounds. Applications in renewable energy are expanding rapidly: installations for wind and solar projects consumed nearly 3.5 million tons of specialty cables in 2024. Major cities such as Shenzhen and Shanghai are deploying fire-resistant, low-smoke zero-halogen (LSZH) cables across metro systems and high-rise buildings, while EV charging infrastructure expansion added over 8 million charging points that rely on advanced power cabling and heat-resistant conductors.

Market Size & Growth: USD 2,330.0 Mn in 2025 to USD 3,798.6 Mn by 2033; growth supported by grid upgrades, EV expansion, and renewable integration.

Top Growth Drivers: Renewable integration 32%, EV charging rollouts 28%, industrial automation 22%.

Short-Term Forecast: By 2028, smart-grid cabling expected to cut outage durations by 20% through better fault detection.

Emerging Technologies: Fiber-sensing power cables, recyclable thermoplastics, and AI-based cable diagnostics.

Regional Leaders (2033): Asia-Pacific USD 2,200 Mn (utility mega-projects); North America USD 820 Mn (grid hardening); Europe USD 650 Mn (green buildings).

Consumer/End-User Trends: Utilities and construction increasingly prefer fire-safe, low-loss, and recyclable cables.

Pilot/Case Example: In 2024, Tata Power’s smart feeder pilot reduced downtime by 18% using sensor-embedded cables.

Competitive Landscape: Prysmian (~15%) leads; key players include Nexans, LS Cable, Sumitomo Electric, and General Cable.

Regulatory & ESG Impact: Stricter fire codes and mandates for 30% recycled content in insulation by 2030.

Investment & Funding Patterns: About USD 4.6 Bn invested in 2023–24 across grid, EV, and offshore wind cabling.

Innovation & Future Outlook: Hybrid power-fiber cables and AI maintenance platforms are becoming industry standards.

Power utilities contribute roughly 40% of demand, construction 28%, industrial machinery 18%, and transportation 14%. Adoption of LSZH insulation, recyclable thermoplastics, and aluminum alloy conductors is accelerating, cutting material intensity by 10–15% in new installations. Stricter fire-safety codes, carbon-reduction mandates, and incentives for grid resilience are reshaping procurement. Asia-Pacific leads in consumption, while Europe shows faster uptake of green-certified cables and North America prioritizes storm-resilient grids, signaling a shift toward smarter, safer, and more sustainable cabling systems.

The Electrical Wires and Cables Market sits at the intersection of energy transition, digital infrastructure, and industrial competitiveness, making it strategically critical for national resilience and corporate productivity. Modern economies depend on reliable electrification for manufacturing, mobility, data centers, and public services; any weakness in cabling infrastructure directly translates into energy losses, downtime, and safety risks. Governments are therefore treating power cabling as a core asset rather than a commodity input, embedding it into long-term energy security and climate strategies.

Technologically, the shift from conventional XLPE cables to sensor-embedded smart cables delivers ~18% faster fault localization compared to older standards, reducing repair times and operational costs for utilities. High-temperature aluminum alloy conductors are replacing pure copper in selected applications, enabling longer spans with 12–15% lower weight while maintaining performance. Digital twins of cable networks—integrated with AI analytics—are increasingly used to predict aging, moisture ingress, and thermal stress before failures occur.

Regionally, Asia-Pacific dominates in installation volume, driven by mega-grid projects and urban rail, while Europe leads in adoption with roughly 35% of utilities integrating smart cable monitoring across critical corridors. North America is prioritizing storm-hardened underground cables for wildfire and hurricane resilience, while the Middle East is rapidly expanding high-capacity desert-rated cables for renewable mega-parks.

In the short term, by 2028, AI-based cable health monitoring is expected to improve asset utilization by 15% and cut emergency repair costs by 20%. From a compliance and ESG perspective, major manufacturers have committed to achieving 25–40% recycled polymer content in insulation by 2030, alongside a 30% reduction in manufacturing emissions.

A micro-scenario illustrates this trajectory: in 2024, a European transmission operator deployed fiber-sensing cables on a 120-km corridor and reduced unplanned outages by 22% within twelve months, proving the economic value of digitalized cabling.

Looking ahead, the Electrical Wires and Cables Market will be a pillar of resilient grids, safe cities, and low-carbon industries—integrating power, data, and sustainability into a single durable backbone for global growth.

The Electrical Wires and Cables Market is shaped by rapid electrification, infrastructure renewal, and evolving safety standards. Utilities are replacing aging grids with high-capacity, low-loss conductors while expanding underground networks to reduce climate-related outages. Construction trends favor fire-resistant, halogen-free cables as building codes tighten worldwide. Industrial automation and data centers are boosting demand for precision power and signal cables with superior thermal stability. Material shifts from copper to advanced aluminum alloys are influencing pricing and design, while recycling mandates are pushing manufacturers toward circular supply chains. Renewable energy projects require longer, more durable subsea and onshore transmission lines, increasing technical complexity. At the same time, digital monitoring, predictive maintenance, and smart-grid integration are transforming cables from passive components into data-generating assets, fundamentally altering procurement, installation, and lifecycle management strategies across the value chain.

The global transition to electric mobility is one of the strongest structural drivers for the Electrical Wires and Cables Market. Every electric vehicle requires 1.5–2 times more internal wiring than an internal combustion car, while public charging infrastructure demands high-capacity, heat-resistant power cables. By 2024, more than 14 million EVs were sold worldwide, creating massive incremental demand for specialty automotive wiring, high-voltage harnesses, and fast-charging cabling. Rapid chargers operating at 150–350 kW require thicker conductors, advanced insulation, and improved thermal management, pushing manufacturers to upgrade materials and production processes. Urban transit electrification—metro lines, trams, and e-buses—has added thousands of kilometers of traction and feeder cables across major cities. In parallel, battery manufacturing plants are being built at scale, each consuming large volumes of industrial-grade cabling for automation, robotics, and power distribution. This electrification wave is structurally embedding higher cable intensity across transport and energy ecosystems, ensuring sustained demand growth.

Fluctuating prices of copper and aluminum create significant cost uncertainty for cable manufacturers and end-users. Copper prices have shown swings exceeding 30% within single years, complicating long-term procurement contracts and squeezing margins. Many projects—especially in public utilities—operate on fixed budgets, forcing delays or material substitutions when prices spike. Manufacturers often hedge through futures, but smaller players lack the financial capacity to manage this risk effectively. Additionally, mining and refining bottlenecks, geopolitical tensions, and energy-intensive smelting processes contribute to supply instability. While aluminum alloys are increasingly used as alternatives, they are not suitable for all high-performance applications, limiting substitution flexibility. Volatile raw material markets also discourage investment in premium, low-loss cables, as buyers may prioritize short-term cost over long-term efficiency, slowing adoption of advanced products.

Offshore wind expansion represents a transformative opportunity for high-voltage subsea and export cables. Each large wind farm requires hundreds of kilometers of armored, water-resistant cabling capable of withstanding extreme marine conditions. Global offshore wind capacity surpassed 75 GW in 2024, with pipelines of over 200 GW planned, ensuring sustained demand for specialized cables. Grid modernization programs are simultaneously replacing aging overhead lines with underground systems that reduce outage risks by up to 60% in storm-prone regions. Smart-grid investments are also driving demand for sensor-integrated cables that provide real-time performance data. Moreover, interregional power interconnectors—linking countries and renewable hubs—require ultra-high-voltage transmission lines, opening new markets for premium conductors and advanced insulation technologies.

Modern high-performance cables are increasingly complex to install, requiring specialized equipment and trained technicians. Underground and subsea installations involve heavy machinery, precise jointing, and strict safety protocols, extending project timelines and costs. Many regions face shortages of certified cable jointers and line workers, leading to project delays and higher wages. Training programs are costly and time-consuming, limiting workforce scalability. Harsh environmental conditions—deserts, deep seas, or mountainous terrain—further complicate deployment and increase failure risks. Additionally, improper installation can reduce cable lifespan by 20–30%, creating liability concerns for contractors. These operational constraints can slow infrastructure rollouts, even when demand and financing are available.

Rise in Modular and Prefabricated Construction: Modular building methods are reshaping cable demand patterns, with about 55% of new modular projects reporting cost savings through off-site prefabrication. Pre-cut and pre-bent wiring harnesses assembled by automated machines have reduced on-site labor by 25–35% while shortening project timelines by up to 20%. In Europe and North America, large contractors are standardizing plug-and-play electrical modules that require high-precision, factory-tested cabling systems, boosting demand for quality-controlled products.

Shift to LSZH and Fire-Resistant Cables: Adoption of low-smoke zero-halogen (LSZH) cables is accelerating in transport and high-rise buildings, where new fire codes now cover 70% of urban construction in major EU cities. These cables can reduce toxic gas emissions by up to 80% during combustion and limit smoke density by roughly 60%, improving evacuation safety. Rail metros and airports are increasingly mandating LSZH materials in retrofits and new builds.

Aluminum-to-Copper Optimization: Hybrid conductor designs using aluminum alloys with copper cladding are cutting material costs by 12–18% while keeping electrical performance within 5% of pure copper lines. Utilities in hot climates are deploying these conductors to reduce sag and increase current capacity by 10–15% without expanding tower spacing, lowering overall grid upgrade costs.

Embedded Sensing in Power Cables: Smart cables with integrated fiber sensors are gaining traction; pilot networks show 15–22% faster fault detection and up to 18% fewer unplanned outages. Over 9,000 km of such cables were installed globally in 2024 across transmission and urban distribution grids, enabling real-time temperature, strain, and moisture monitoring for predictive maintenance.

The Electrical Wires and Cables Market is segmented primarily by type, application, and end-user, reflecting diverse performance requirements across voltage levels, environments, and usage contexts. Type segmentation spans low-, medium-, and high-voltage power cables alongside communication and specialty cables, each optimized for conductivity, insulation, and durability. Application segmentation is shaped by grid infrastructure, construction activity, transportation electrification, and digital connectivity needs. End-user demand varies between utilities, industrial operators, builders, telecom firms, and transport agencies, with differing priorities around safety, reliability, and lifecycle costs. Increasing urbanization, renewable integration, and data-intensive infrastructure are blurring boundaries between segments, creating hybrid products—such as power cables with embedded sensing—that serve multiple use cases while tightening performance standards across all categories.

Low-voltage power cables dominate the market, accounting for roughly 45% share, as they are indispensable in residential wiring, commercial buildings, industrial machinery, and small-scale renewable installations where safety codes mandate flame-retardant and LSZH insulation. Their leadership stems from massive construction volumes, easier installation, and standardized specifications across countries.

The fastest-growing type is high-voltage (HV) and extra-high-voltage (EHV) cables with an estimated ~7% CAGR, driven by underground grid expansion, offshore wind export systems, and long-distance interconnectors that require higher capacity, better thermal performance, and superior insulation materials.

Medium-voltage cables remain critical for urban distribution networks and industrial plants, while communication/fiber-optic hybrid cables are gaining traction in smart grids and data centers. Specialty cables—such as heat-resistant, submarine, and rail traction lines—serve niche but strategically important markets. Together, these remaining segments account for about 55% combined share, reflecting a fragmented but technologically diverse landscape.

• In 2025, Japan’s Ministry of Economy reported that new subsea high-voltage links connecting offshore wind zones in the Sea of Japan used advanced EHV cables capable of operating above 525 kV while reducing transmission losses by more than 10%.

Power utilities lead applications with approximately 40% share, as utilities are rapidly replacing aging overhead lines with resilient underground and high-capacity transmission systems to reduce outage risks and integrate renewables.

The fastest-growing application is EV charging and electrified transport infrastructure (~8% CAGR), supported by the rollout of ultra-fast chargers, electric bus depots, and metro expansions that require high-temperature, high-current cabling.

Building & construction remains a large segment due to urbanization and stricter fire codes; industrial machinery drives demand for flexible, oil-resistant cables; and telecom/data centers rely on hybrid power–fiber systems for reliable connectivity. These other applications together represent roughly 60% combined share.

Consumer and enterprise adoption trends are reshaping demand: in 2025, about 37% of global enterprises reported upgrading internal power cabling to support automation and data-heavy operations, while over 58% of Gen Z consumers preferred buildings branded as “fire-safe and energy-efficient,” indirectly boosting LSZH cable uptake.

• In 2025, the U.S. Department of Energy documented that smart-grid feeder upgrades using advanced power cables in California cut average outage duration by more than 20% across wildfire-prone districts.

Electric utilities are the leading end-user segment with around 38% share, as they invest heavily in undergrounding, renewable integration, and digitalized grid monitoring. Their procurement prioritizes durability, thermal stability, and predictive maintenance capabilities.

The fastest-growing end-user is data centers and digital infrastructure (~9% CAGR), fueled by AI workloads, cloud expansion, and hyperscale campuses that require dense, low-loss power distribution with integrated sensing.

Construction contractors, industrial manufacturers, transportation authorities, and telecom operators collectively account for about 62% share. Among them, industrial plants show adoption rates of roughly 34% for advanced heat-resistant cabling, while telecom operators report about 29% uptake of hybrid power–fiber lines in 5G backhaul networks.

In 2025, nearly 36% of large enterprises globally piloted smart cabling systems for predictive maintenance, and 41% of major hospitals in the U.S. upgraded critical power lines to fire-resistant cables during electrical retrofits.

• In 2025, the U.S. Federal Energy Regulatory Commission noted that several regional grid operators reduced emergency repair callouts by over 18% after deploying sensor-embedded power cables across high-risk corridors.

Asia-Pacific accounted for the largest market share at 55% in 2025; however, the Middle East & Africa region is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

Regional performance in the Electrical Wires and Cables Market is shaped by infrastructure intensity, industrialization pace, and energy-transition priorities. Asia-Pacific leads in absolute volumes due to mega-grid programs, mass urban construction, and large-scale manufacturing capacity, with annual cable consumption exceeding 18 million tons in 2025. North America represents roughly 18% of global demand, driven by grid hardening, data centers, and EV charging expansion, with more than 1.2 million miles of distribution lines under modernization. Europe holds about 15% share, propelled by stringent fire-safety codes, offshore wind projects exceeding 75 GW pipeline, and circular-economy mandates. South America contributes approximately 7%, supported by renewable transmission corridors and urban electrification, particularly in Brazil’s 5,000+ km grid expansion plan. The Middle East & Africa accounts for around 5% today but is scaling rapidly through smart cities, oil & gas electrification, and giga-projects such as NEOM and massive desert solar parks exceeding 50 GW planned capacity. Across regions, undergrounding rates are rising—averaging 22% globally—with the highest penetration in Europe at 34% and the fastest increase in MEA at 28% year-on-year.

North America holds roughly 18% of the global Electrical Wires and Cables Market, with demand concentrated in the United States and Canada. Power utilities remain the largest consumer, investing heavily in undergrounding and wildfire-resilient networks across California, Texas, and the Northeast. More than 1.2 million miles of distribution lines are currently being modernized, favoring high-temperature, low-sag conductors and sensor-embedded cables. Data centers are a powerful demand engine: hyperscale campuses in Virginia, Arizona, and Texas are installing high-capacity, low-loss cabling to support AI workloads, driving premium product uptake. Regulatory momentum is strong—federal grid resilience funding has allocated over USD 10 billion since 2022 for hardening and modernization, while new fire codes in major cities mandate LSZH cables in transit and high-rise buildings. Technologically, utilities are accelerating deployment of fiber-sensing power lines; several operators now monitor thousands of kilometers in real time for temperature and strain. Local manufacturers such as Southwire are expanding automated cable plants in Georgia and investing in recyclable insulation compounds. Consumer behavior skews toward safety and reliability: enterprises in healthcare and finance show higher adoption of fire-resistant and smart cables, prioritizing uptime and compliance over upfront cost.

Europe represents about 15% of the global market, with Germany, France, the UK, Italy, and Spain as key demand centers. Construction standards are among the strictest worldwide, pushing rapid adoption of LSZH and flame-retardant cables across transport hubs, hospitals, and high-rise buildings. The European Union’s Circular Economy Action Plan is forcing manufacturers to increase recycled polymer content and reduce lifecycle emissions, reshaping material choices and supply chains. Offshore wind is a major catalyst: Europe has over 75 GW installed or planned, requiring thousands of kilometers of armored subsea export cables and inter-array lines. Grid interconnectors such as North Sea links are accelerating demand for extra-high-voltage underground systems. Digitalization is advancing through smart-grid pilots in Germany and the Nordics, where utilities are embedding sensors into new transmission corridors. Local champions like Prysmian are investing heavily in next-generation submarine cable factories in Italy and the UK. Rail electrification programs across France and Spain are upgrading traction cabling, while urban metro expansions in Paris and Berlin favor high-precision prefabricated wiring modules. European consumers and enterprises exhibit strong compliance-driven behavior—regulatory pressure leads to preference for transparent, certified, and traceable cable products with documented environmental performance.

Asia-Pacific is the largest volume market globally, accounting for roughly 55% of consumption in 2025. China, India, Japan, and South Korea dominate demand, supported by massive grid buildouts, metro expansions, and industrial clusters. China alone operates more than 1,200 cable factories and has deployed over 45,000 km of ultra-high-voltage lines. India is rapidly scaling underground distribution under its Revamped Distribution Sector Scheme, covering hundreds of cities. Manufacturing intensity is a defining trend: automated extrusion lines, AI quality inspection, and recyclable insulation production are becoming standard across leading plants. Offshore wind in China, Japan, and South Korea is boosting demand for high-performance subsea cables, while urban rail projects in Mumbai, Shenzhen, and Seoul are driving traction cable consumption. Innovation hubs in Shenzhen, Yokohama, and Bengaluru are piloting sensor-embedded smart cables for predictive maintenance. Local players such as LS Cable in South Korea are expanding high-voltage manufacturing capacity and exporting to global projects. Consumer behavior is shaped by rapid digitalization—growth is strongly driven by e-commerce logistics hubs, EV charging rollouts, and mobile-data infrastructure that requires dense, reliable power cabling.

South America holds about 7% of the global Electrical Wires and Cables Market, led by Brazil, Argentina, Chile, and Colombia. Brazil dominates regional demand due to extensive hydroelectric transmission corridors and expanding wind and solar capacity in the Northeast. Over 5,000 km of new transmission lines are planned through 2027, requiring high-capacity overhead and underground cables. Argentina is modernizing urban distribution in Buenos Aires and Córdoba, while Chile is investing heavily in long-distance renewable interconnectors linking desert solar zones to consumption centers. Governments are offering tax incentives for local cable manufacturing and renewable grid components, strengthening domestic supply chains. Technologically, utilities are shifting toward aluminum alloy conductors to reduce costs and improve sag performance in hot climates. Prefabricated wiring systems are gaining traction in commercial construction across major cities. Local firms such as Prysmian Brazil are expanding production of fire-resistant and medium-voltage cables for infrastructure projects. Consumer behavior is closely tied to media, telecom, and language localization industries, which are increasing demand for hybrid power–fiber cabling in broadcast and digital networks.

The Middle East & Africa region currently represents around 5% of global demand but is the fastest-growing at about 8.2% CAGR. Growth is concentrated in the UAE, Saudi Arabia, Qatar, and South Africa. Oil & gas electrification projects are replacing legacy systems with high-temperature, corrosion-resistant cables across refineries and offshore platforms. Mega urban developments—such as NEOM, Red Sea projects, and smart districts in Dubai—are deploying fire-safe, high-capacity underground networks. Desert solar parks exceeding 50 GW planned capacity are driving demand for heat-resistant, UV-stable cabling and long-distance transmission lines. Technological modernization is evident in digital substations, sensor-integrated cables, and automated installation techniques to reduce labor bottlenecks. Regional trade partnerships with Europe and East Asia are improving access to advanced materials and manufacturing know-how. Local manufacturers in the UAE are expanding LSZH and medium-voltage production for domestic infrastructure. Consumer behavior varies widely: in the Gulf, demand is tied to luxury real estate and smart buildings, while in Sub-Saharan Africa it is driven by rural electrification and mini-grid expansion.

China — 32% Market Share: Unmatched manufacturing scale, ultra-high-voltage grid expansion, and massive renewable buildout.

United States — 18% Market Share: Aggressive grid modernization, wildfire resilience programs, and hyperscale data-center growth.

The Electrical Wires and Cables Market is moderately consolidated at the top with a long tail of regional and specialist players. Approximately 150+ active competitors operate globally, ranging from large diversified conglomerates to niche manufacturers focused on specific voltage classes or technology niches. The combined share of the top 5 companies — including industry leaders like Prysmian Group, Nexans S.A., Sumitomo Electric Industries, LS Cable & System, and Southwire Company — is estimated at around 40–45% of total global volume, highlighting strong competition at the high end but significant fragmentation overall.

Major players are pursuing aggressive strategic initiatives. Prysmian’s planned acquisition of Encore Wire for over $4.1 billion in 2024 underscores its push to expand North American electrical wire and power cable footprint and diversify product offerings. Nexans and other European manufacturers have secured multi-year grid electrification contracts, supplying over 5,200 km of underground cables under centralized frameworks in large markets. Partnerships and supply agreements, such as long-term copper rod supply contracts in Hamburg, reflect efforts to stabilize raw material access and strengthen supply chain resilience.

Innovation is reshaping the competitive landscape: advanced high-voltage dynamic cable systems are now offered up to 245 kV for floating offshore wind applications, while others are deploying HVDC SF6-free terminations for greener grid connectivity. These moves are intensifying differentiation beyond basic commodity products into performance and sustainability-oriented segments. The dynamics reveal a market where scale, technological breadth, supply chain control, and regional operational agility are decisive competitive advantages.

Sumitomo Electric Industries Ltd.

LS Cable & System Ltd.

Belden Inc.

Leoni AG

Furukawa Electric Co., Ltd.

TE Connectivity Ltd.

Encore Wire Corporation

KEI Industries Ltd.

Finolex Cables Ltd.

Havells India Ltd.

Polycab India Ltd.

Electrical wires and cables are increasingly integrating advanced material science and digital technologies to meet performance, safety, and sustainability demands. Traditional copper and aluminum conductors continue to serve as the backbone, but developments in advanced alloys, composite conductors, and next-generation insulation compounds are improving thermal performance, corrosion resistance, and flexibility. For example, ultra-lightweight aluminum-based extra-high voltage cables are engineered to reduce tower loading by up to 33% while maintaining conductivity comparable to copper, enabling cost-effective long-distance transmission.

In high-voltage applications, dynamic cable systems rated up to 245 kV for floating offshore wind platforms are being deployed, offering enhanced mechanical durability under severe marine conditions while facilitating renewable energy integration. At the opposite end of the spectrum, hybrid power-fiber cable solutions and embedded sensor technologies are gaining traction for predictive diagnostics and grid health monitoring, capturing real-time temperature, strain, and moisture data to reduce downtime and maintenance costs.

Emerging technologies also include eco-engineered materials such as bio-based sheaths and recycled insulation compounds that reduce environmental impact and CO₂ intensity. Data communications and smart infrastructure trends are fostering the adoption of fiber-optic integrated cabling in smart grids, 5G backhaul networks, and data centers, where low-loss, high-bandwidth capacity is essential. Digital manufacturing — including AI-assisted extrusion and automated quality inspection — is boosting yield rates while cutting defect margins and production variance. Collectively, these technologies are elevating cables beyond passive transmission components into intelligent, durable, and sustainable infrastructure enablers.

• In June 2025, Prysmian Group announced a $500 million investment to expand electrification capacity and support U.S. power grid demand through the expansion of its Encore Wire facility in McKinney, Texas, creating up to 120 new jobs as part of its North America growth strategy. Source: www.prysmian.com

• On April 29, 2025, Nexans revealed it was awarded a contract to deliver the high-voltage subsea cable for Malta’s second Malta-Sicily interconnector, with production slated at its Charleston, USA facility, reinforcing energy security and grid resiliency. Source: www.nexans.com

• October 23, 2025, Nexans reported that its Electrification business segment delivered +9.4% organic growth in the first nine months of 2025, with a strong subsea and transmission backlog of approximately €7.9 billion, and announced the acquisition of Electro Cables in Canada to strengthen PWR-Connect capabilities.

• February 3, 2026, Nexans completed and entered the long-term maintenance phase for the 225 kV export cable system for the Dieppe-Le Tréport offshore wind farm, marking a key milestone in operational delivery for offshore renewable infrastructure. Source: www.nexans.co

The scope of the Electrical Wires and Cables Market Report encompasses a comprehensive analysis of product types, application segments, end-user industries, technologies, and geographic regions shaping the global landscape. The report covers a broad spectrum of product categories including low-, medium-, high-, and extra-high-voltage cables, alongside communication and hybrid power-fiber solutions. It addresses diverse installation contexts such as overhead, underground, subsurface, and submarine environments, reflecting varied technical and regulatory requirements.

Geographically, the report examines regional performance across Asia-Pacific, North America, Europe, South America, and Middle East & Africa, delivering granular insights into consumption patterns, infrastructure projects, manufacturing trends, and regulatory frameworks that influence market dynamics. Within regions, the report highlights key national markets, infrastructure programs, and investment trends shaping demand, such as urban grid modernization in North America, offshore wind requirements in Europe, and electrification projects in Asia-Pacific.

Applications analyzed include power transmission & distribution, building & construction, industrial machinery, telecom and data centers, transportation electrification, renewable energy projects, and specialized sectors (oil & gas, aerospace, defense). The report also explores technology categories such as advanced materials, sensor-embedded cables, eco-engineered insulation, and digital monitoring systems, detailing how innovation is transforming performance, safety, and sustainability.

The analytical framework includes segment share breakdowns, competitive positioning, supply chain insights, and innovation trends, offering decision-makers visibility on strategic opportunities and execution challenges across market segments. Emerging niches like bio-based sheath cables, HVDC systems, and smart infrastructure integration are also captured to articulate future growth pathways and investment priorities, making the report relevant for corporate strategy, product planning, procurement, and policy formulation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,330.0 Million |

| Market Revenue (2033) | USD 3,798.6 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Prysmian Group; Nexans; Southwire; Sumitomo Electric; LS Cable & System; Belden; Leoni; Furukawa Electric; TE Connectivity; Encore Wire; KEI Industries; Finolex Cables; Havells; Polycab |

| Customization & Pricing | Available on Request (10% Customization Free) |