Reports

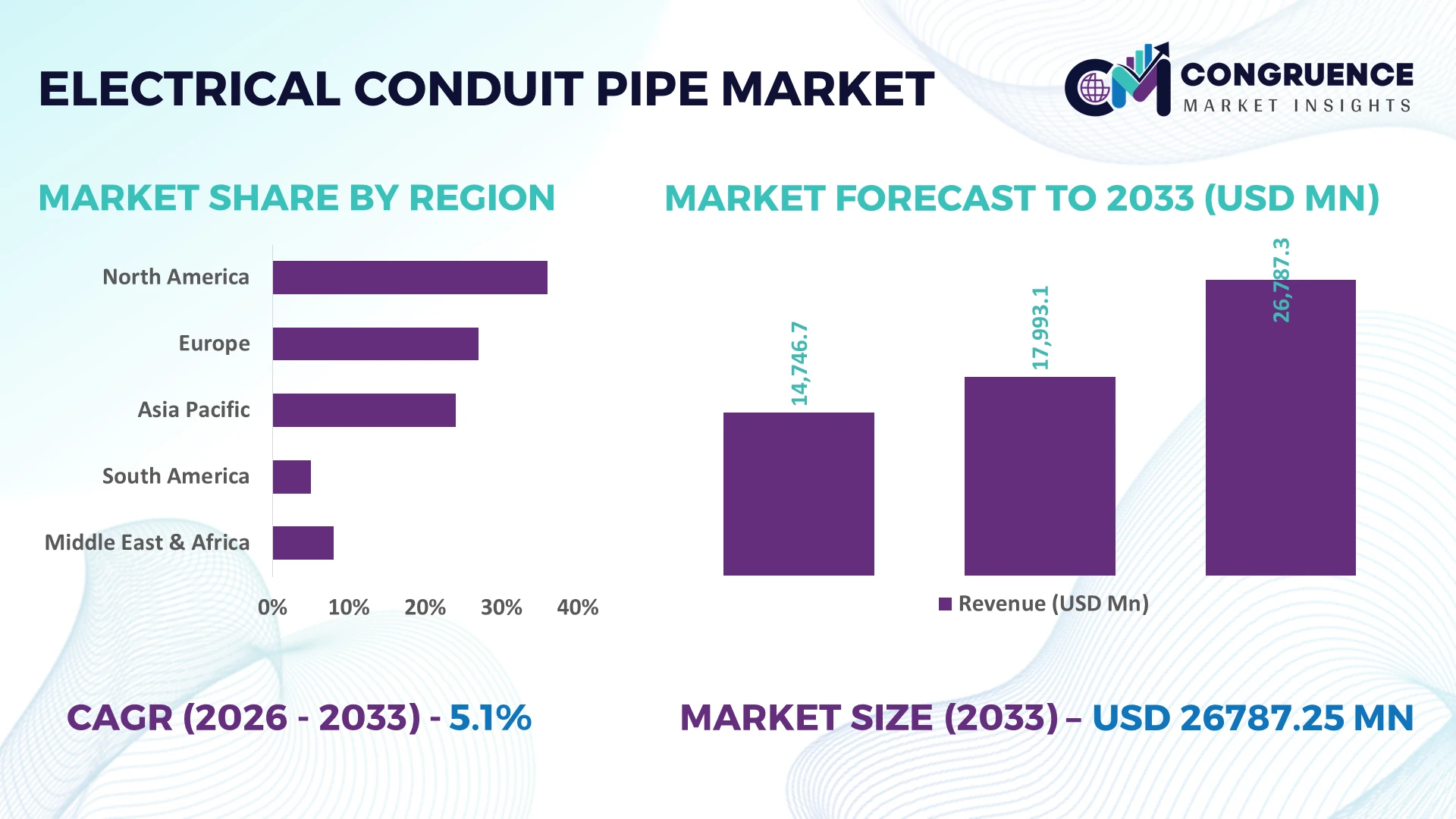

The Global Electrical Conduit Pipe Market was valued at USD 17993.12 Million in 2025 and is anticipated to reach a value of USD 26787.25 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033. Growth is supported by accelerated grid modernization, industrial electrification, high-voltage infrastructure projects, and stricter fire-safety regulations driving advanced conduit installations across commercial, industrial, and utility networks.

China remains the dominant market, accounting for approximately 34% of global manufacturing capacity, supported by large-scale investments in power transmission, smart factories, and urban infrastructure. More than 72% of new industrial electrical installations increasingly utilize high-performance conduit systems, while India continues expanding faster through rapid industrial corridor development and renewable energy projects. Ongoing supply-chain diversification across Asia following global trade realignments further reinforces China's production leadership despite increasing regional competition.

Businesses should prioritize capacity expansion, localized supply networks, and compliant high-performance conduit solutions to strengthen long-term market positioning.

Market Size & Growth: USD 17,993.12 million in 2025, reaching USD 26,787.25 million by 2033 at 5.1% CAGR, supported by accelerating grid modernization and industrial electrification.

Top Growth Drivers: Smart infrastructure (+28%), renewable power installations (+24%), and commercial construction (+19%) continue driving global demand.

Short-Term Forecast: By 2028, automated conduit production is expected to improve manufacturing efficiency by 16% while reducing material waste by 11%.

Emerging Technologies: AI-enabled quality inspection, advanced polymer compounds, and automated extrusion lines improve product consistency and production throughput by over 15%.

Regional Leaders: Asia-Pacific exceeds USD 11.5 billion, North America approaches USD 5.8 billion, and Europe surpasses USD 4.6 billion, driven by infrastructure upgrades and energy transition projects.

Consumer/End-User Trends: Nearly 63% of industrial and commercial projects increasingly specify corrosion-resistant conduit systems for longer asset life.

Pilot/Case Example: In 2026, a smart industrial facility deployment improved installation productivity by 18% through modular conduit routing and digital project planning.

Competitive Landscape: The leading manufacturer holds approximately 10% global share alongside major international producers competing through product innovation and regional expansion.

Regulatory & ESG Impact: Compliance-focused material innovations reduce lifecycle emissions by approximately 14% while supporting stricter building and electrical safety standards.

Investment & Funding: More than USD 2.4 billion supports manufacturing expansion, automation, strategic partnerships, and regional supply-chain localization initiatives.

Innovation & Future Outlook: Advanced recyclable materials, digital manufacturing, and high-performance conduit systems strengthen resilience as global infrastructure investment continues expanding.

Electrical conduit pipe demand is increasingly concentrated in renewable energy facilities, data centers, industrial automation, and urban infrastructure upgrades. Manufacturers are introducing lightweight, fire-resistant, and recyclable conduit systems that improve installation efficiency. Nearly 22% of new product development emphasizes sustainable materials, while regional supply-chain localization and evolving electrical safety regulations continue reshaping procurement strategies, setting the stage for the strategic discussion.

The Electrical Conduit Pipe Market has become strategically important as governments and private utilities accelerate power infrastructure modernization, industrial electrification, and resilient building development. Supply-chain restructuring since recent global trade disruptions has encouraged manufacturers to diversify production across India, Vietnam, and Mexico while maintaining high-capacity operations in China. This shift strengthens procurement flexibility, shortens delivery cycles, and supports competitive pricing for large commercial and industrial projects where compliance and lifecycle performance increasingly influence purchasing decisions.

Advanced conduit manufacturing using automated extrusion and AI-enabled quality inspection delivers approximately 18% higher production efficiency and reduces material waste by nearly 12% compared with conventional production methods. China continues to lead large-scale manufacturing and export capacity, while Germany emphasizes premium engineering standards and recyclable conduit technologies for high-specification industrial applications. Over the next two to three years, more than 35% of newly commissioned smart manufacturing facilities are expected to integrate automated conduit installation planning, improving installation consistency and reducing project delays.

A 2026 industrial campus deployment combined prefabricated conduit assemblies with digital building models, reducing installation time by 20% while improving project coordination. Manufacturers are expanding localized production, strengthening contractor partnerships, and investing in advanced material innovation to improve supply resilience. Companies that combine operational efficiency, regulatory compliance, and high-performance product portfolios will secure stronger competitive positioning as infrastructure investment priorities continue evolving.

Large-scale electrification projects and stricter electrical safety standards continue to reshape demand for high-performance conduit systems. Around 41% of new industrial facilities specify corrosion-resistant and fire-retardant conduit solutions, while automated construction methods reduce installation time by nearly 17%. India's manufacturing expansion and power transmission investments are increasing procurement volumes, supported by industrial corridor development and renewable energy integration. These structural changes improve long-term demand visibility for manufacturers. In response, leading companies are expanding extrusion capacity, introducing recyclable conduit materials, and forming partnerships with engineering contractors to secure infrastructure projects. The strongest competitive advantage increasingly belongs to suppliers capable of delivering certified products with shorter lead times and localized manufacturing support.

Price fluctuations in PVC resins, steel, and specialty polymers remain a structural constraint for conduit manufacturers. Raw material costs have experienced swings exceeding 15% in recent procurement cycles, while shipping disruptions have extended component lead times by approximately 20% for selected imported inputs. Manufacturers in Europe remain exposed to energy-intensive production costs, affecting operational margins and pricing flexibility. These conditions reduce profitability, complicate long-term contracts, and delay project execution for contractors. Companies are responding through supplier diversification, localized sourcing strategies, and longer procurement agreements while increasing recycled material utilization to reduce exposure to commodity volatility and improve operational stability across production networks.

Digital infrastructure expansion and advanced construction methods are creating new opportunities beyond conventional commercial buildings. More than 38% of smart building developments now incorporate integrated electrical protection systems requiring higher-performance conduit solutions. Japan and India are increasing investment in automated manufacturing facilities where precision installation and lifecycle reliability are critical. Manufacturers are accelerating R&D in lightweight composite conduits, recyclable polymers, and digitally traceable products supporting predictive asset management. Strategic partnerships with engineering firms and prefabrication specialists enable faster project execution while reducing installation costs by nearly 14%. Companies investing early in sustainable materials and intelligent manufacturing ecosystems are strengthening differentiation in increasingly specification-driven procurement markets.

Maintaining consistent product quality while scaling automated manufacturing presents a significant execution challenge. Approximately 27% of manufacturers report shortages of technically skilled production and installation personnel, while advanced production equipment requires up to 22% higher initial capital investment than conventional lines. The United States continues expanding data center and industrial construction, increasing demand for highly specialized conduit systems that require precision engineering and certified installation practices. Without standardized digital workflows and workforce development, deployment consistency becomes difficult across complex infrastructure projects. Companies must strengthen automation, workforce training, digital quality control, and collaboration with engineering partners to sustain operational excellence and preserve long-term competitiveness in high-specification applications.

Smart Factory Production Expansion: Manufacturers are accelerating automation across conduit extrusion and inspection lines, with automated quality control improving defect detection by nearly 24% and reducing production downtime by 16%. Labor shortages and tighter delivery schedules are driving digital workflow adoption, while companies in China and India continue scaling intelligent manufacturing facilities to improve output consistency and shorten customer lead times through integrated production planning.

Recyclable Material Adoption Rising: Demand for recyclable PVC compounds and low-impact conduit materials has increased as stricter construction standards influence procurement decisions. Around 31% of newly introduced conduit products now incorporate recycled or resource-efficient materials, while manufacturing scrap has declined by approximately 13% through closed-loop processing. Producers are restructuring supply agreements and expanding material innovation programs to strengthen sustainability credentials without compromising electrical performance.

Prefabricated Installation Accelerates: Contractors are increasingly deploying prefabricated conduit assemblies that reduce onsite installation time by nearly 21% and lower project rework by about 15%. Large commercial developments in the United States and industrial facilities in India are standardizing modular installation workflows to address skilled labor shortages. Manufacturers are partnering with engineering firms to supply customized conduit kits that simplify project execution and improve installation accuracy.

Localized Supply Networks Strengthen: Enterprise procurement strategies increasingly prioritize regional manufacturing hubs, reducing average delivery times by approximately 18% while improving inventory availability by 14%. Ongoing supply-chain restructuring and geopolitical trade adjustments are encouraging manufacturers to establish additional production capacity outside traditional export centers. A notable operational shift is the growing use of dual-sourcing strategies, enabling companies to improve resilience while maintaining competitive pricing and project continuity.

PVC Conduits remain the dominant segment because they combine low installation cost, corrosion resistance, and broad compatibility across residential, commercial, and infrastructure projects. Approximately 48% of new building electrical installations utilize PVC conduit systems due to their lightweight design and simplified installation processes. Steel Conduits continue serving heavy industrial and hazardous environments where mechanical strength remains essential, while Aluminum Conduits maintain relevance in applications requiring reduced structural weight and corrosion protection. Manufacturers continue expanding PVC production capacity while enhancing fire-retardant formulations to meet evolving building standards.

HDPE Conduits represent the fastest-growing type as underground utility networks, renewable energy projects, and fiber-optic deployments increasingly require durable and flexible conduit solutions. Flexible Conduits also continue gaining adoption in automated manufacturing facilities, improving installation flexibility by nearly 19% in complex equipment layouts. Companies are broadening product portfolios, investing in advanced polymer technologies, and collaborating with engineering contractors to address specialized installation requirements while balancing cost efficiency with long-term performance.

Infrastructure remains the leading application as governments and utilities prioritize grid expansion, transportation networks, and urban modernization. Nearly 42% of large-scale electrical conduit demand is linked to infrastructure-related projects where long service life and regulatory compliance are critical. Residential Buildings maintain stable demand through urban housing development, while Commercial Buildings increasingly require higher-capacity electrical pathways supporting intelligent building systems. Manufacturers continue optimizing logistics and production planning to serve large infrastructure contracts with shorter delivery schedules.

Utilities are the fastest-growing application as power distribution upgrades, renewable energy integration, and underground cable deployment expand. Industrial Facilities also continue increasing conduit consumption through factory automation and equipment modernization, improving electrical system reliability by approximately 17%. Companies are introducing application-specific conduit systems, expanding local inventories, and strengthening contractor partnerships to improve deployment efficiency and meet evolving technical specifications across multiple construction environments.

Construction represents the largest end-user segment because every new residential, commercial, and mixed-use development requires compliant electrical routing systems. Approximately 46% of conduit procurement originates from construction projects where installation speed and regulatory compliance strongly influence purchasing decisions. Manufacturing remains an important customer group as production facilities adopt automated equipment requiring higher-capacity electrical infrastructure. Telecommunications continues expanding conduit requirements through fiber deployment and network modernization initiatives. Suppliers increasingly offer project-specific product ranges and technical support to strengthen contractor relationships.

Energy is the fastest-growing end-user segment, supported by renewable generation projects, battery storage facilities, and transmission network upgrades. Utilities continue expanding procurement for underground distribution systems, while manufacturers develop specialized conduit solutions capable of supporting demanding environmental conditions. Companies are enhancing customization capabilities, establishing strategic distribution partnerships, and improving localized inventory management. Nearly 23% of enterprise procurement programs now prioritize long-life conduit systems that reduce maintenance requirements and improve infrastructure reliability throughout operational lifecycles.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Advanced Infrastructure Modernization Driving Premium Product Adoption

North America remains a highly mature Electrical Conduit Pipe Market supported by grid modernization, data center expansion, industrial automation, and commercial redevelopment. The region contributes approximately 24% of global demand, with strong deployment across utility upgrades and mission-critical facilities. More than 36% of newly commissioned industrial projects specify high-performance conduit systems with enhanced fire resistance and durability. Investment in underground power distribution and resilient electrical infrastructure continues to reshape procurement priorities. Manufacturers are expanding regional distribution networks, increasing automation within production facilities, and strengthening partnerships with engineering contractors to improve project execution and reduce delivery timelines.

United States Market Outlook: The United States leads the regional market through extensive construction activity, advanced manufacturing capacity, and continuous investment in electrical infrastructure. Large-scale data center expansion, renewable energy integration, and modernization of aging transmission systems sustain conduit demand across multiple industries. Nearly 40% of large commercial electrical installations now incorporate advanced conduit solutions designed for higher safety compliance and lifecycle performance. Domestic manufacturers continue investing in localized production, automation, and contractor support programs to improve responsiveness and strengthen competitive positioning.

Sustainability Standards Reshaping Industrial Procurement

Europe maintains a strong market position through stringent building regulations, industrial modernization, and increasing adoption of recyclable electrical installation materials. The region accounts for approximately 21% of global deployment, with electrical safety compliance becoming a primary procurement criterion across commercial and industrial construction. Around 33% of new conduit specifications prioritize recyclable or low-impact material formulations. Infrastructure modernization and energy-efficient building upgrades continue supporting demand, while manufacturers focus on advanced production technologies and localized supply strategies to improve operational resilience and product consistency.

Germany Market Outlook: Germany serves as the region's industrial leader through advanced manufacturing, engineering excellence, and extensive industrial automation. Electrical conduit demand remains strong across automotive production, smart factories, and high-performance commercial developments. More than 44% of industrial electrical upgrade projects incorporate premium conduit systems designed for long operational life and strict compliance requirements. Domestic companies continue investing in recyclable material technologies, digital manufacturing, and product innovation to reinforce leadership in technically demanding applications.

Manufacturing Scale and Infrastructure Expansion Strengthen Leadership

Asia-Pacific represents the largest regional market owing to its unmatched manufacturing capacity, urban infrastructure development, and expanding industrial production. The region contributes approximately 43.8% of global market demand while supplying a significant share of worldwide conduit manufacturing. More than 52% of new power infrastructure projects across major economies require advanced conduit systems supporting underground cable deployment and industrial electrification. Ongoing factory expansion, export-oriented manufacturing, and smart city initiatives continue increasing procurement volumes. Companies are expanding production facilities, strengthening regional supply chains, and investing in automated extrusion technologies to improve efficiency.

China Market Outlook: China remains the dominant national market through integrated manufacturing ecosystems, extensive construction activity, and continuous investment in electrical infrastructure. The country produces roughly one-third of global conduit manufacturing output while maintaining strong domestic consumption across industrial and commercial sectors. Increasing adoption of automated manufacturing and high-performance conduit materials supports product quality improvements. Leading manufacturers continue expanding production capacity, enhancing export competitiveness, and accelerating digital manufacturing initiatives to strengthen operational efficiency.

Infrastructure Renewal Supporting Industrial Demand

South America continues strengthening its Electrical Conduit Pipe Market through expanding power infrastructure, industrial modernization, and commercial construction activity. The region contributes approximately 6% of global demand, with electrical network upgrades supporting increasing conduit deployment. Infrastructure investment programs have improved utility project execution, while industrial developments are raising demand for durable conduit systems. Around 18% of new public electrical infrastructure projects now emphasize underground cable protection. Manufacturers are increasing regional inventories, strengthening distribution partnerships, and expanding local processing capabilities to improve delivery performance despite logistical challenges.

Brazil Market Outlook: Brazil leads the regional market due to its extensive construction sector, growing industrial base, and continuing investments in electricity distribution. Utility modernization and renewable energy integration continue increasing conduit deployment across transmission and distribution projects. Approximately 29% of large infrastructure developments incorporate advanced conduit systems designed for long-term durability. Companies are expanding domestic manufacturing capabilities and strengthening contractor partnerships to improve supply reliability and project execution across the country's diverse infrastructure landscape.

Strategic Infrastructure Investment Accelerates Deployment

Middle East & Africa is experiencing rapid market transformation through smart city developments, industrial diversification, and large-scale utility investments. The region represents approximately 5.2% of global demand but records the strongest expansion momentum as governments prioritize resilient electrical infrastructure. Nearly 27% of newly approved infrastructure developments include upgraded underground electrical distribution systems requiring advanced conduit solutions. Manufacturers are increasing regional partnerships, establishing localized distribution hubs, and supporting major engineering projects with application-specific product portfolios to improve delivery efficiency and technical support.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through extensive infrastructure development, industrial expansion, and ambitious urban transformation initiatives. Large-scale economic diversification projects continue driving significant electrical installation activity across commercial, industrial, and utility sectors. More than 30% of new mega-project electrical packages specify high-performance conduit systems supporting long-term operational reliability. Manufacturers are expanding regional partnerships, improving localized inventory availability, and aligning product development with evolving national construction and electrical compliance requirements.

The Electrical Conduit Pipe Market is led by global manufacturers including Atkore, ABB, Wienerberger, Aliaxis, and JM Eagle, competing directly with regional PVC specialists and low-cost domestic producers across Asia and the Middle East. The top five companies collectively account for approximately 34% of global market share, reflecting a moderately consolidated structure where technology, production scale, and distribution reach determine competitiveness. Premium manufacturers differentiate through advanced fire-resistant materials, automated production, and certified product portfolios, while regional suppliers compete aggressively on pricing, often offering costs 10–15% lower. Automated manufacturing improves production efficiency by nearly 18%, and localized supply networks reduce delivery lead times by approximately 20%, creating measurable procurement advantages. Companies are expanding manufacturing capacity, securing long-term raw material agreements, forming contractor partnerships, and investing in recyclable conduit technologies. Competitive pressure is shifting toward supply-chain resilience and product compliance rather than price alone. High certification requirements and capital-intensive manufacturing remain key entry barriers. Winning requires operational efficiency, localized production, technical innovation, and dependable project execution.

Atkore Inc.

ABB Ltd.

Wienerberger AG

Aliaxis SA

JM Eagle

Cantex Inc.

Dura-Line Corporation

National Pipe & Plastics, Inc.

Prime Conduit, Inc.

Astral Limited

Finolex Industries Ltd.

Supreme Industries Limited

Polycab India Limited

Legrand SA

Digital manufacturing, AI-enabled quality inspection, and advanced polymer engineering are transforming electrical conduit production. Automated extrusion systems improve dimensional accuracy while increasing production efficiency by approximately 18% and reducing material waste by nearly 12%. Around 38% of large manufacturing facilities have adopted machine-vision inspection to improve quality consistency and reduce manual intervention. Companies implementing integrated production analytics gain stronger process control, lower rejection rates, and improved delivery reliability, strengthening competitiveness in specification-driven infrastructure and industrial projects.

High-performance recyclable polymers, flame-retardant formulations, and lightweight composite conduit technologies are steadily replacing conventional material systems. Compared with legacy production methods, digitally controlled extrusion delivers approximately 20% higher production consistency and reduces maintenance interruptions by nearly 15%. Manufacturers supplying utility, renewable energy, and data center projects benefit most because advanced conduit systems improve installation efficiency while extending operational durability. Growing adoption of digital product traceability also strengthens regulatory compliance and lifecycle asset management.

Between 2026 and 2028, smart manufacturing integration, predictive maintenance, and digital production twins are expected to become mainstream across leading conduit facilities. More than 45% of newly commissioned production lines are projected to incorporate intelligent process monitoring and automated quality optimization. Early adopters will achieve faster product development, stronger supply-chain responsiveness, and greater customization capability, positioning themselves ahead of cost-focused competitors as infrastructure projects increasingly demand certified, high-performance electrical conduit solutions.

April 2026 – Atkore Inc. announced the sale of its HDPE pipe and conduit business to Infra Pipes, while retaining a 10% equity stake in the combined entity to sharpen focus on core electrical infrastructure products and improve portfolio efficiency.

September 2025 – Atkore Inc. launched a strategic portfolio review that included consolidating 3 manufacturing facilities and evaluating non-core conduit assets, strengthening cost efficiency and increasing emphasis on electrical infrastructure markets.

May 2026 – ABB Ltd. announced a USD 200 million investment across Europe to accelerate grid transformation, expanding electrification capabilities that support growing demand for advanced electrical infrastructure, including conduit and cable management solutions for utilities and industry.

April 2025 – Atkore Inc. reported mid-single-digit volume growth and improved manufacturing productivity despite challenging market conditions, demonstrating operational resilience through production optimization and reinforcing its competitive position in electrical conduit manufacturing.

This report provides comprehensive analysis of the Electrical Conduit Pipe Market across PVC Conduits, Steel Conduits, Aluminum Conduits, Flexible Conduits, and HDPE Conduits, covering applications in residential buildings, commercial buildings, industrial facilities, infrastructure, and utilities. It evaluates demand across construction, utilities, manufacturing, telecommunications, and energy while assessing market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 10 leading industry participants are benchmarked alongside evolving deployment patterns, material innovation, and manufacturing strategies.

The study examines technology adoption, automation trends, recyclable material development, supply-chain transformation, and regional production shifts expected between 2026 and 2033. It highlights operational adoption indicators, competitive positioning, procurement strategies, and enterprise expansion priorities to support investment planning and strategic decision-making. The report also identifies emerging infrastructure opportunities, product innovation pathways, evolving customer requirements, and regional deployment trends, enabling businesses to strengthen market positioning, optimize capacity planning, and improve long-term competitive resilience.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 17993.12 Million |

Market Revenue in 2033 | USD 26787.25 Million |

CAGR (2026 - 2033) | 5.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Atkore Inc., ABB Ltd., Wienerberger AG, Aliaxis SA, JM Eagle, Cantex Inc., Dura-Line Corporation, National Pipe & Plastics, Inc., Prime Conduit, Inc., Astral Limited, Finolex Industries Ltd., Supreme Industries Limited, Polycab India Limited, Legrand SA |

Customization & Pricing | Available on Request (10% Customization is Free) |