Reports

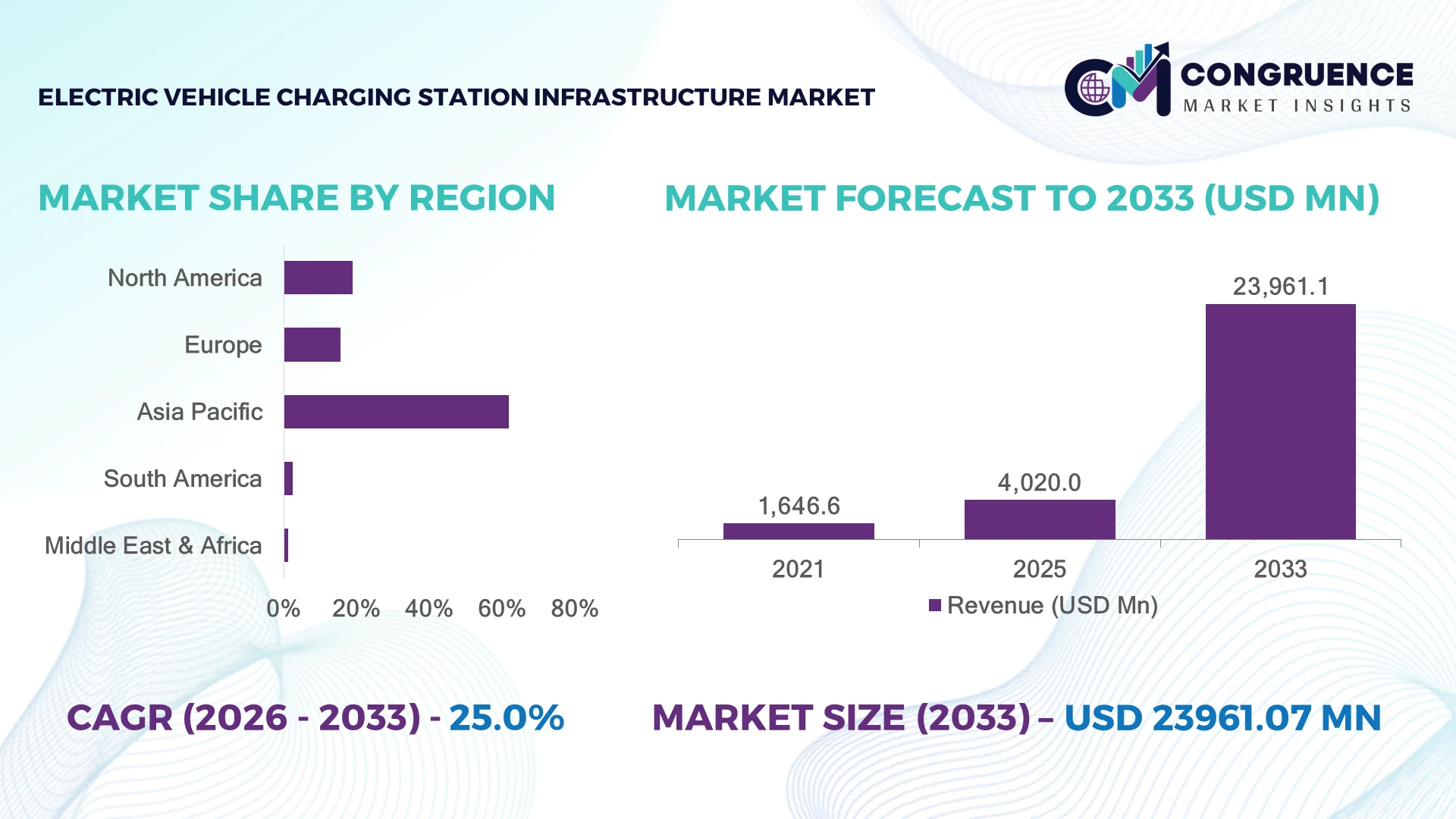

The Global Electric Vehicle Charging Station Infrastructure Market was valued at USD 4,020.0 Million in 2025 and is anticipated to reach a value of USD 23,961.1 Million by 2033 expanding at a CAGR of 25% between 2026 and 2033. Government-backed EV adoption mandates, expansion of ultra-fast DC charging corridors, and grid modernization programs are accelerating large-scale charging infrastructure deployment worldwide.

China dominates the global market with approximately 58% of installed public EV charging points, supported by investments exceeding USD 15 billion in charging infrastructure and strong demand from the automotive and renewable energy sectors. Compared with the United States, China deploys charging stations at a significantly faster pace, while Europe leads in interoperable charging standards, strengthening network accessibility and cross-border mobility.

The market increasingly rewards companies capable of combining scalable charging networks, smart energy management, and strategic infrastructure partnerships.

Market Size & Growth: USD 4,020.0 Million (2025) to USD 23,961.1 Million (2033) at 25% CAGR, driven by rapid ultra-fast charging deployment and national electrification strategies.

Top Growth Drivers: Public fast-charging expansion (45%), EV sales growth (30%), and government infrastructure incentives (25%).

Short-Term Forecast: By 2028, average DC fast-charging session time is projected to decline by 30% through higher-power chargers and smarter load balancing.

Emerging Technologies: AI-enabled energy management, vehicle-to-grid (V2G) integration, and 350 kW ultra-fast charging enhance network performance.

Regional Leaders: Asia Pacific (~USD 13.8 Billion), Europe (~USD 5.1 Billion), and North America (~USD 3.9 Billion) lead through charging corridor expansion and fleet electrification.

Consumer/End-User Trends: More than 70% of new public charging installations support mobile payment and connected digital services.

Pilot/Case Example: In 2024, high-power charging corridor deployments reduced average charging wait times by nearly 35% on major highway routes.

Competitive Landscape: ChargePoint holds approximately 14% market presence alongside Tesla, ABB, Siemens, Shell Recharge, and EVgo.

Regulatory & ESG Impact: Zero-emission transport policies target over 50% reduction in transport emissions while accelerating nationwide charger deployment.

Investment & Funding: More than USD 35 Billion has been committed globally through public funding, strategic partnerships, and private infrastructure expansion.

Innovation & Future Outlook: Bidirectional charging, AI-powered predictive maintenance, and renewable-powered charging hubs strengthen long-term network resilience amid global supply-chain localization.

The Electric Vehicle Charging Station Infrastructure Market continues expanding across passenger vehicles, commercial fleets, logistics hubs, public transit, and highway charging corridors. Recent innovations include AI-enabled charger management, megawatt charging systems, and vehicle-to-grid integration that improve network utilization by nearly 20%. Domestic manufacturing incentives and grid modernization initiatives are reinforcing supply-chain resilience while enabling smarter, interoperable charging ecosystems, setting the foundation for broader strategic market transformation.

Electric vehicle charging infrastructure has become a strategic pillar of global transportation electrification as governments, utilities, automotive manufacturers, and infrastructure developers accelerate investments in nationwide charging ecosystems. Competition increasingly depends on network reliability, charging speed, digital connectivity, and energy management rather than charger deployment alone. Grid modernization, domestic equipment manufacturing, and interoperability regulations are reshaping investment priorities while reducing infrastructure bottlenecks across major economies.

Modern 350 kW DC fast chargers can reduce charging time by nearly 60% compared with conventional 50 kW systems, significantly improving fleet utilization and customer convenience. Asia Pacific leads deployment through large-scale public infrastructure programs, while Europe emphasizes interoperable charging networks and North America prioritizes interstate fast-charging corridors. Over the next two to three years, intelligent load management platforms and predictive maintenance are expected to improve charger availability beyond 98% across advanced networks.

Leading operators are expanding partnerships with utilities, renewable energy providers, and commercial real estate developers to deploy integrated charging hubs supporting passenger vehicles and commercial fleets. These investments strengthen operational efficiency, improve energy optimization, and enhance competitive positioning while creating scalable infrastructure capable of supporting long-term electric mobility expansion.

National electrification strategies and rapid deployment of high-power charging infrastructure are transforming charging availability and utilization. More than 65% of newly installed public charging stations now support DC fast charging, while chargers rated above 150 kW reduce charging time by nearly 60% compared with conventional AC systems. China continues expanding highway charging corridors under large-scale transport modernization programs, encouraging private operators to accelerate deployment. This infrastructure expansion improves driver confidence, increases charger utilization, and supports commercial fleet electrification. In response, leading companies are investing in AI-enabled energy management, battery-buffered charging stations, and utility partnerships that optimize grid stability while reducing peak-load constraints. A key strategic advantage increasingly lies in integrating charging infrastructure with renewable energy and intelligent load-balancing platforms rather than simply expanding charger numbers.

Electrical distribution capacity remains one of the largest barriers to rapid charging deployment, particularly in dense urban locations where grid upgrades often account for nearly 40% of total installation timelines. Approximately 30% of public charging operators continue facing interoperability challenges across payment platforms and charging protocols, reducing network efficiency and customer convenience. In countries such as the United States, permitting delays and utility connection queues frequently postpone large charging projects. These structural limitations increase deployment costs, delay asset utilization, and complicate nationwide network expansion. To reduce operational exposure, companies are localizing equipment sourcing, adopting open charging standards, securing long-term component contracts, and deploying battery-integrated charging systems that reduce dependence on immediate grid reinforcement while improving installation flexibility.

Vehicle-to-grid (V2G) technology and intelligent energy management are creating new value streams beyond conventional charging services. Studies indicate that smart charging platforms can lower peak electricity demand by approximately 25%, while predictive energy optimization improves charger utilization by nearly 20%. Japan continues advancing commercial V2G pilots, demonstrating how electric vehicles can stabilize electricity networks during periods of fluctuating renewable generation. Charging infrastructure providers are expanding software capabilities, cloud-based energy platforms, and utility collaborations to support bidirectional energy exchange. A less obvious opportunity lies in integrating charging hubs with distributed solar generation and stationary battery storage, enabling operators to reduce operating costs, improve energy resilience, and develop recurring service-based business models rather than relying solely on charging transactions.

As charging ecosystems become increasingly connected, maintaining network reliability across thousands of distributed assets presents significant execution challenges. Industry assessments indicate that charger uptime exceeding 97% has become a critical performance benchmark, while cybersecurity incidents targeting connected infrastructure have increased by more than 20% in recent years. Germany's expanding public charging network highlights the operational complexity of coordinating software updates, grid communications, payment systems, and remote diagnostics across multiple operators. Inconsistent maintenance standards and skilled workforce shortages further affect deployment consistency and customer experience. Companies must strengthen cybersecurity architecture, invest in predictive maintenance, standardize digital platforms, and expand technical service partnerships to ensure scalable, resilient infrastructure capable of supporting long-term electric mobility adoption.

Ultra-Fast Charging Expansion: Deployment of 150–350 kW DC chargers increased by nearly 40% over the past year as highway corridor projects accelerated in China and the United States. Standardized charging protocols and improved power electronics have shortened installation cycles by almost 20%, enabling operators to improve charger utilization while expanding nationwide networks. Companies are scaling high-power charging hubs through utility partnerships and infrastructure modernization programs.

AI-Driven Network Optimization: More than 55% of large charging operators are integrating AI-based monitoring, predictive maintenance, and dynamic load balancing into charging networks. Automated diagnostics have reduced unexpected charger downtime by approximately 25%, improving service availability and maintenance efficiency. Technology providers are expanding cloud platforms and digital service partnerships to optimize energy distribution while supporting larger charging portfolios with lower operating costs.

Renewable Energy Integration: Nearly 35% of newly commissioned charging hubs now incorporate on-site solar generation or battery energy storage systems to reduce grid dependence. Grid modernization initiatives and electricity price volatility are encouraging operators to deploy hybrid energy architectures. Infrastructure providers are restructuring project designs around distributed energy resources, creating more resilient charging ecosystems while improving long-term operational stability.

Interoperable Digital Ecosystems: Open charging protocols, unified payment platforms, and roaming agreements now support over 60% of public charging networks across advanced EV markets. Regulatory standardization and enterprise fleet requirements are accelerating seamless cross-network access. Charging companies are investing in software integration, mobile applications, and strategic collaborations, enabling higher customer retention and creating competitive advantages beyond physical charger deployment.

DC Fast Charging represents the leading segment, accounting for approximately 62% of public charging infrastructure deployment due to its ability to deliver rapid charging for passenger vehicles, logistics fleets, and highway corridors. Charging capacities exceeding 150 kW significantly reduce charging duration, making the technology indispensable for commercial mobility and long-distance transportation. Infrastructure operators continue prioritizing high-power charging installations through utility collaborations, equipment upgrades, and digital energy management platforms. AC Charging remains widely deployed across residential and workplace environments because of its lower installation costs, grid compatibility, and suitability for overnight charging. Wireless Charging is emerging as the fastest-growing segment, supported by pilot deployments in autonomous mobility, premium passenger vehicles, and urban transit applications. Although representing less than 8% of current installations, enterprise investment continues increasing as automation and hands-free charging gain strategic importance. Equipment manufacturers are expanding R&D activities, developing standardized wireless charging systems, and partnering with automotive OEMs to accelerate commercial deployment while diversifying future infrastructure portfolios.

Public Charging dominates the application landscape with nearly 57% of installed charging points serving urban mobility, highway corridors, retail destinations, and municipal infrastructure. Growing EV ownership, public accessibility requirements, and government-supported charging programs continue concentrating investment in this segment. Charging operators are expanding interoperable networks, implementing smart payment platforms, and integrating remote monitoring technologies to improve customer experience and asset utilization. Commercial Charging is the fastest-growing application as businesses electrify logistics fleets, delivery operations, and workplace transportation. Enterprise charging deployments have expanded by nearly 30% over recent years, supported by fleet optimization initiatives and corporate sustainability targets. Meanwhile, Residential Charging remains fundamental for daily vehicle charging, particularly in detached housing markets where overnight charging offers operational convenience and lower electricity costs. Manufacturers are responding with scalable home charging solutions, connected software platforms, and integrated energy management systems that strengthen long-term customer engagement across multiple charging environments.

Commercial Operators constitute the dominant end-user segment, representing approximately 52% of charging infrastructure demand due to large-scale deployment across retail centers, workplaces, fuel stations, and dedicated charging networks. Continuous expansion of public charging ecosystems and increasing EV traffic encourage operators to invest in intelligent charging software, predictive maintenance, and energy optimization platforms. Network providers are strengthening competitive positioning through strategic partnerships with utilities, real estate developers, and automotive manufacturers. Fleet Operators/Public Transport is the fastest-growing end-user segment as logistics companies, municipal transit agencies, and ride-hailing operators accelerate fleet electrification. Fleet charging infrastructure utilization has increased by nearly 35%, supported by depot charging, route optimization, and centralized energy management systems. Residential Users continue representing a stable demand base through home charging installations and connected energy solutions. Equipment manufacturers are tailoring charging products with flexible pricing models, smart connectivity, and integrated software services that address the distinct operational requirements of residential, commercial, and fleet customers.

Asia-Pacific accounted for the largest market share at 61.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 26.8% between 2026 and 2033.

North America accounted for approximately 18.9% of the global market in 2025, supported by rapid expansion of interstate charging corridors, commercial fleet electrification, and increasing deployment of high-power DC charging stations. Public-private collaborations are accelerating installation across highways, logistics hubs, and retail locations while utilities continue investing in grid modernization to accommodate higher charging loads. More than 70% of newly announced public charging projects emphasize interoperable payment systems and remote network management. Fleet charging demand is reshaping deployment priorities as logistics operators require dependable high-capacity charging infrastructure. Charging equipment manufacturers are expanding domestic production, strengthening utility partnerships, and integrating AI-based energy optimization to improve network reliability and reduce operating costs.

United States Market Outlook: The United States remains the region's largest market due to its extensive interstate highway network, strong utility investment, and expanding commercial EV ecosystem. Federal infrastructure initiatives continue supporting nationwide charging deployment, while private operators accelerate installation of ultra-fast charging stations. More than 200,000 public charging connectors are now operational, and increasing investment in domestic charger manufacturing is strengthening supply-chain resilience. Technology companies are prioritizing intelligent energy management, predictive maintenance, and software integration to improve charger availability and support large-scale fleet electrification.

Europe represented nearly 15.7% of the global market in 2025, benefiting from strict emission regulations, mature electric mobility policies, and harmonized charging standards. Cross-border charging interoperability continues improving network accessibility, while governments prioritize high-capacity charging corridors connecting major transport routes. More than 60% of recently commissioned public chargers support digital payment integration and smart-grid communication. Utilities, charge point operators, and automotive manufacturers are strengthening strategic partnerships to accelerate deployment while improving renewable energy integration. Investment increasingly targets scalable charging ecosystems capable of supporting passenger vehicles, commercial fleets, and future bidirectional charging capabilities.

Germany Market Outlook: Germany leads the European market through its advanced automotive industry, dense highway infrastructure, and strong investment in public charging expansion. Nationwide deployment of ultra-fast charging stations continues alongside domestic manufacturing of charging equipment and power electronics. Approximately 30% of Europe's high-power charging installations are concentrated in Germany, reflecting strong industrial capabilities. Enterprise collaborations between utilities, automotive OEMs, and charging operators continue enhancing network reliability and accelerating commercial fleet electrification.

Asia-Pacific dominated the global market with approximately 61.8% share in 2025, driven by extensive public charging deployment, large EV manufacturing capacity, and government-supported electrification initiatives. The region maintains the world's highest concentration of public charging infrastructure, supported by continuous investments in urban mobility and highway charging networks. Nearly 65% of newly installed chargers are integrated with digital monitoring and intelligent load management systems. Charging infrastructure providers continue expanding manufacturing capacity while strengthening supply chains for power modules, connectors, and charging software. Rapid deployment scale enables lower installation costs and faster infrastructure expansion than most global markets.

China Market Outlook: China remains the world's largest charging infrastructure market, accounting for nearly 58% of global public charging installations. Extensive investment in highway charging corridors, urban charging hubs, and domestic charger manufacturing supports nationwide EV adoption. More than 3.5 million public charging points are operational, reinforcing China's leadership in charging infrastructure deployment. Domestic manufacturers continue advancing ultra-fast charging technologies, intelligent charging platforms, and integrated renewable energy solutions while expanding exports of charging equipment worldwide.

South America accounted for approximately 2.4% of the global market in 2025 as governments and private operators expand charging infrastructure around major metropolitan areas. Public transportation electrification, commercial fleet modernization, and increasing EV imports are driving charger deployment despite uneven grid readiness across several countries. Approximately 45% of new charging projects are concentrated around major urban logistics corridors and commercial districts. Infrastructure developers increasingly partner with utilities and retail operators to optimize installation efficiency while improving charger accessibility. Although deployment remains at an earlier stage than developed markets, operational momentum continues strengthening through targeted infrastructure investment.

Brazil Market Outlook: Brazil leads regional deployment through expanding electric bus programs, commercial fleet electrification, and improving charging infrastructure across major cities. Utility companies and private charging operators continue investing in public fast-charging stations supporting long-distance mobility. More than 40% of South America's installed public charging infrastructure is located in Brazil, reflecting its large automotive market and expanding clean transportation policies. Companies increasingly localize equipment sourcing while forming strategic partnerships with energy providers to improve deployment efficiency.

Middle East & Africa represented approximately 1.2% of the global market in 2025, with investment concentrated in smart cities, premium mobility corridors, and commercial charging infrastructure. National sustainability initiatives and transport diversification strategies are encouraging deployment of public charging stations integrated with renewable energy systems. More than 35% of recently announced charging projects are linked to mixed-use developments, airports, and tourism infrastructure. International technology providers are collaborating with local utilities and infrastructure developers to establish scalable charging ecosystems while strengthening digital network management and maintenance capabilities.

United Arab Emirates Market Outlook: The United Arab Emirates leads the regional market through proactive electric mobility policies, smart city development, and strong investment in charging infrastructure. Dubai and Abu Dhabi continue expanding public charging networks supporting passenger vehicles, commercial fleets, and tourism mobility. Public charging availability has increased by more than 30% over recent years through coordinated government and private-sector initiatives. Companies are integrating renewable-powered charging stations, digital payment platforms, and intelligent energy management to strengthen long-term infrastructure performance.

The competitive landscape is led by ChargePoint, ABB, Siemens, Tesla Supercharger, and EVgo, while regional charging network operators and hardware specialists compete aggressively on localized deployment and service integration. Global technology leaders compete against cost-focused regional infrastructure providers, whereas automotive-backed charging ecosystems increasingly challenge independent network operators. The top five companies collectively account for approximately 42% of the global market, reflecting moderate consolidation. Competition centers on charging speed, network uptime, software interoperability, installation efficiency, and lifecycle service capabilities. Operators offering 350 kW ultra-fast charging solutions achieve up to 60% shorter charging times, while AI-enabled predictive maintenance improves charger availability by nearly 25%. Companies continue expanding through utility partnerships, fleet agreements, software integration, and vertical integration across hardware, cloud platforms, and energy management. Competition is shifting toward intelligent charging ecosystems and grid-connected services rather than standalone hardware. High capital requirements, grid interconnection complexity, and nationwide service capabilities remain significant entry barriers. Sustainable competitive advantage increasingly depends on integrated digital platforms, reliable infrastructure, and scalable deployment execution.

ChargePoint Holdings, Inc.

Siemens AG

EVgo Inc.

Blink Charging Co.

Wallbox N.V.

Tritium DCFC Limited

Alpitronic GmbH

Delta Electronics, Inc.

Shell Recharge Solutions

bp pulse

FLO Services USA Inc.

Kempower Oyj

Webasto Group

Ultra-fast DC charging, AI-enabled energy management, and vehicle-to-grid (V2G) technologies are redefining charging infrastructure performance. Modern 350 kW chargers reduce charging time by nearly 60% compared with conventional 50 kW systems, while intelligent load balancing improves electricity utilization by approximately 20%. More than 55% of newly deployed public charging networks now incorporate cloud-based monitoring and predictive diagnostics, allowing operators to maximize charger availability and reduce maintenance interventions.

Emerging technologies increasingly integrate battery energy storage, renewable energy, Plug & Charge authentication, and ISO 15118 communication protocols. AI-driven predictive maintenance lowers unexpected equipment downtime by almost 25%, while modular charging architectures shorten installation timelines by approximately 15%. Independent charging operators, utilities, and automotive-backed charging networks gain the greatest operational advantage through integrated hardware-software ecosystems capable of managing distributed charging assets more efficiently than legacy standalone installations.

Between 2026 and 2028, bidirectional charging, edge-based energy optimization, and digital twin asset management are expected to become mainstream deployment priorities. Companies investing early in cybersecurity, interoperable software platforms, and cloud-native charging management will strengthen competitive positioning, improve network reliability, accelerate commercial fleet electrification, and unlock new energy-service business models as smart grid integration expands globally.

December 2025:EVgo announced that more than 40% of its newly deployed stations during 2025 utilized domestically manufactured prefabricated modular charging skids, reducing installation costs by approximately 15% and accelerating nationwide deployment. Source: www.evgo.com

March 2025:EVgo and Toyota Motor North America opened their first co-branded 350 kW DC fast charging stations in California, with each site capable of serving eight vehicles simultaneously, strengthening public charging accessibility and supporting broader EV adoption. Source: www.evgo.com

December 2024: General Motors and ChargePoint announced plans to deploy up to 500 ultra-fast charging ports across the United States using ChargePoint's Express Plus platform and Omni Port technology, improving interoperability for CCS and NACS-equipped vehicles. Source: www.theverge.com

March 2025:Pilot Company, General Motors, and EVgo expanded their nationwide charging collaboration to more than 130 fast-charging locations across 25+ states, significantly strengthening interstate EV travel corridors and improving long-distance charging accessibility.

This report provides comprehensive analysis of the Electric Vehicle Charging Station Infrastructure Market across AC Charging, DC Fast Charging, and Wireless Charging, covering deployment trends, technology evolution, competitive positioning, and operational developments. It evaluates Residential Charging, Commercial Charging, and Public Charging applications together with demand across Residential Users, Commercial Operators, and Fleet Operators/Public Transport. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting infrastructure deployment patterns, enterprise participation, and evolving investment priorities.

The study examines intelligent charging platforms, AI-enabled network management, vehicle-to-grid integration, renewable-powered charging systems, interoperability standards, and ultra-fast charging technologies. It profiles leading industry participants, assesses deployment concentration, adoption trends, and strategic partnerships, while identifying emerging opportunities across mature and developing EV ecosystems. The report supports investment planning, market entry, expansion strategy, product positioning, competitive benchmarking, and long-term decision-making for stakeholders navigating the evolving charging infrastructure landscape between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,020.0 Million |

| Market Revenue (2033) | USD 23,961.1 Million |

| CAGR (2026–2033) | 25.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ABB Ltd.; ChargePoint Holdings, Inc.; Siemens AG; EVgo Inc.; Blink Charging Co.; Wallbox N.V.; Tritium DCFC Limited; Alpitronic GmbH; Delta Electronics, Inc.; Shell Recharge Solutions; bp pulse; FLO Services USA Inc.; Kempower Oyj; Webasto Group |

| Customization & Pricing | Available on Request (10% Customization Free) |