Reports

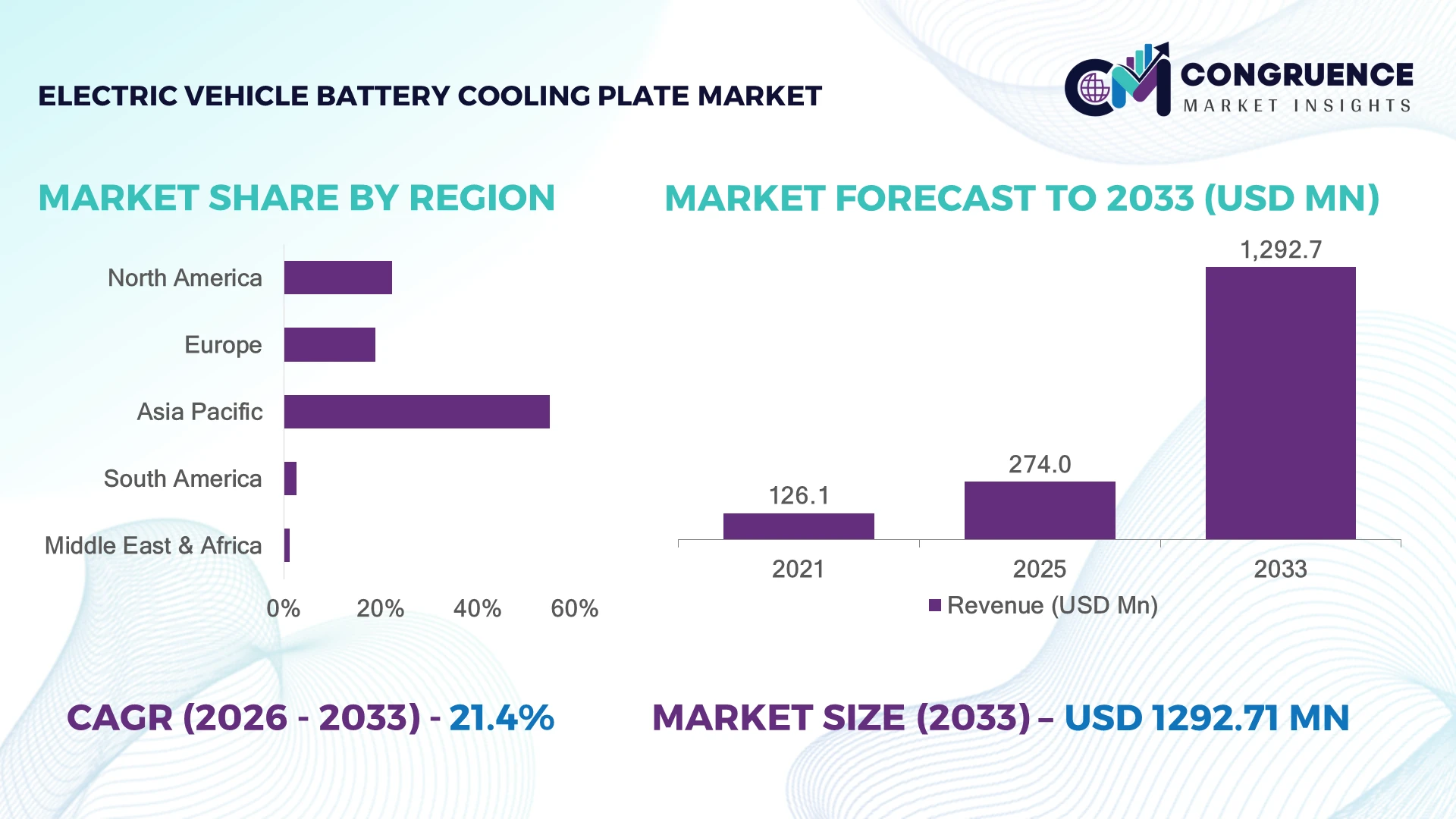

The Global Electric Vehicle Battery Cooling Plate Market was valued at USD 274.0 Million in 2025 and is anticipated to reach a value of USD 1,292.7 Million by 2033 expanding at a CAGR of 21.4% between 2026 and 2033. Growth is primarily driven by the rapid adoption of high-energy-density EV battery packs, increasing implementation of liquid cooling architectures, and accelerated localization of advanced battery manufacturing across major automotive markets.

China remains the dominant country, accounting for approximately 58% of global EV battery production capacity, supported by investments exceeding USD 120 billion in battery manufacturing and integrated supply chains. The country's EV penetration surpassed 45% of new vehicle sales, while the European Union continues expanding localized battery facilities to reduce dependence on imports, strengthening regional competitiveness through industrial policy and technology deployment.

The market increasingly rewards manufacturers that combine advanced thermal management technologies with localized production, scalable manufacturing, and strategic OEM partnerships.

Market Size & Growth: Valued at USD 274.0 Million in 2025 and projected to reach USD 1,292.7 Million by 2033, supported by rapid EV platform electrification and advanced liquid thermal management adoption.

Top Growth Drivers: EV battery production +32%, liquid cooling adoption above 70% in premium EV platforms, and battery energy density improvements exceeding 20%.

Short-Term Forecast: By 2028, battery thermal efficiency improves by nearly 18% while cooling plate manufacturing costs decline by approximately 12% through automation.

Emerging Technologies: AI-assisted thermal simulation, friction stir welding, and lightweight aluminum microchannel cooling plates accelerate next-generation battery designs.

Regional Leaders: Asia Pacific approaches USD 760 Million, Europe exceeds USD 290 Million, and North America surpasses USD 170 Million with expanding localized battery supply chains.

Consumer/End-User Trends: More than 68% of newly launched electric passenger vehicles integrate advanced liquid battery cooling systems for enhanced performance and charging capability.

Pilot/Case Example: In 2024, advanced cooling plate integration reduced battery temperature variation by nearly 30%, improving charging consistency and operational reliability.

Competitive Landscape: The top five manufacturers collectively account for nearly 46% of market activity, including Dana Incorporated, Modine Manufacturing, Valeo, Mahle, and Boyd Corporation.

Regulatory & ESG Impact: Battery localization policies and lightweight material adoption reduce manufacturing emissions by approximately 15% while strengthening regional supply resilience.

Investment & Funding: More than USD 9 billion in battery thermal management and manufacturing investments support strategic partnerships and production expansion across key automotive regions.

Innovation & Future Outlook: High-performance cooling plates, integrated battery modules, and smart thermal monitoring are reshaping global electric mobility competitiveness.

Electric Vehicle Battery Cooling Plate Market demand is expanding across passenger EVs, commercial electric fleets, and high-performance battery systems requiring precise thermal regulation. Manufacturers are introducing lightweight microchannel aluminum designs, laser-welded cooling plates, and integrated thermal monitoring solutions that improve heat dissipation by over 25%. Ongoing battery localization initiatives and resilient automotive supply-chain strategies continue accelerating product innovation, setting the foundation for broader strategic industry developments.

The Electric Vehicle Battery Cooling Plate Market has become strategically important as automotive manufacturers prioritize battery safety, ultra-fast charging capability, and extended vehicle lifespan. Expanding battery gigafactory networks, regional supply-chain restructuring, and stricter vehicle efficiency regulations are encouraging suppliers to establish localized production while strengthening long-term partnerships with automotive OEMs. Thermal management has evolved into a core competitive differentiator across next-generation electric mobility platforms.

Advanced liquid cooling plates dissipate heat approximately 35% more efficiently than conventional air-cooled systems while enabling more uniform battery temperatures during high-load operation. Asia-Pacific leads large-scale manufacturing with extensive battery ecosystem integration, whereas Europe emphasizes premium engineering and localized production supported by industrial modernization. Over the next two to three years, automated manufacturing lines and digital quality inspection are expected to reduce production defects by nearly 20% while improving throughput.

Manufacturers are increasingly deploying integrated cooling plate assemblies within modular battery packs to simplify vehicle assembly and improve maintenance efficiency. Companies are expanding manufacturing footprints, strengthening material sourcing partnerships, and investing in advanced aluminum processing technologies to improve operational flexibility. These strategic initiatives reinforce competitive positioning, strengthen supply resilience, and support long-term technological leadership across the evolving electric vehicle ecosystem.

The rapid shift toward high-energy-density battery packs and ultra-fast charging architectures is fundamentally increasing demand for advanced battery cooling plates. More than 72% of newly introduced premium electric vehicle platforms now incorporate liquid cooling systems, while battery energy density has improved by over 20%, requiring more precise thermal regulation. China's continued expansion of battery gigafactories and localized component manufacturing is reinforcing supply-chain integration and reducing production lead times. This structural transition enables automakers to improve charging consistency, battery durability, and operational safety. In response, manufacturers are investing in automated brazing, microchannel aluminum processing, and strategic OEM collaborations to deliver lightweight, application-specific cooling solutions. Companies securing early integration into next-generation EV platforms are strengthening long-term supply positions and improving manufacturing efficiency.

Cooling plate production remains exposed to fluctuations in aluminum prices, specialized joining materials, and precision manufacturing requirements. Aluminum represents nearly 65% of cooling plate material consumption, while advanced welding and leak-testing procedures can account for approximately 18% of production costs. Supply disruptions affecting processed aluminum and thermal interface materials continue to pressure manufacturers in Germany and Japan, where quality standards remain exceptionally stringent. These constraints reduce pricing flexibility, extend production planning cycles, and increase inventory risks for suppliers. To mitigate these pressures, companies are localizing procurement, securing long-term material contracts, and introducing standardized modular designs that simplify manufacturing. Operational resilience increasingly depends on diversified sourcing strategies rather than solely expanding production capacity.

The integration of intelligent thermal management with digital battery platforms is creating significant opportunities beyond conventional cooling components. More than 60% of next-generation EV battery development programs now include predictive thermal monitoring, while AI-enabled simulation tools have shortened thermal design validation by nearly 30%. South Korea is accelerating investment in integrated battery modules that combine cooling plates, sensors, and structural components within a unified architecture. This evolution enables lower assembly complexity, improved thermal uniformity, and enhanced lifecycle performance. Companies are expanding R&D partnerships with battery manufacturers, semiconductor suppliers, and software developers to build complete thermal ecosystems instead of standalone hardware. Suppliers capable of delivering integrated engineering solutions will gain stronger competitive differentiation and deeper OEM relationships.

Expanding production while maintaining precision, reliability, and quality consistency remains a major execution challenge. Cooling plates require leak rates approaching zero defects, and automated inspection systems must verify thousands of microchannel welds with accuracy exceeding 99%. Vehicle manufacturers increasingly expect globally standardized specifications despite differences in manufacturing infrastructure between China, Europe, and North America. Maintaining consistent product quality across multiple facilities requires advanced automation, digital quality control, and highly skilled technical personnel. Companies are investing in smart factories, digital twins, and real-time process monitoring to improve manufacturing repeatability and reduce production variation. Long-term competitiveness will depend on scalable manufacturing excellence rather than production volume alone.

Integrated Battery Pack Designs Battery manufacturers are increasingly embedding cooling plates directly into structural battery packs, reducing component count by nearly 18% and improving thermal uniformity by approximately 22%. China's large-scale battery manufacturing expansion and evolving cell-to-pack architectures are accelerating this transition. Automakers are redesigning assembly workflows while suppliers expand integrated engineering capabilities and automated production lines to improve manufacturing efficiency and shorten vehicle development cycles.

Advanced Lightweight Material Adoption Lightweight aluminum microchannel cooling plates now account for over 70% of new EV thermal management programs, while next-generation composite materials reduce overall cooling system weight by nearly 12%. Tight vehicle efficiency regulations and battery range optimization are encouraging material innovation. Manufacturers are strengthening partnerships with aluminum processors and investing in precision forming technologies to enhance durability, corrosion resistance, and large-volume production consistency.

Manufacturing Automation Expansion Automated laser welding, robotic inspection, and AI-assisted quality control have reduced production defects by approximately 20% while improving manufacturing throughput by nearly 15%. Rising labor costs and increasing quality expectations are accelerating factory modernization in Germany and South Korea. Companies are deploying digital production monitoring and predictive maintenance systems to improve process stability and maintain consistent cooling plate performance across global manufacturing facilities.

Localized Supply Chain Strategies Automotive manufacturers are increasing regional sourcing, with localized component procurement exceeding 60% for several new EV programs. Supply-chain diversification following global logistics disruptions has shortened component lead times by approximately 16%. Suppliers are expanding manufacturing footprints, establishing strategic partnerships with battery producers, and restructuring procurement networks to improve operational resilience while supporting faster vehicle production and greater delivery reliability.

Liquid Cooling Plate represents the leading segment, accounting for approximately 68% of market demand because of superior heat dissipation, compatibility with high-capacity battery packs, and seamless integration into fast-charging electric vehicles. Its ability to maintain consistent cell temperatures supports longer battery life, improved charging performance, and enhanced operational safety. Manufacturers continue investing in lightweight aluminum microchannel designs and automated brazing technologies to improve production efficiency. Phase Change Material Cooling Plate is emerging as the fastest-growing segment as next-generation battery platforms seek passive thermal regulation and lower energy consumption. Increasing investments in advanced materials are accelerating commercialization across premium EV applications. Air Cooling Plate remains relevant for entry-level electric vehicles where cost optimization is prioritized over maximum thermal performance. The Others category supports niche vehicle platforms and specialized mobility solutions requiring customized thermal configurations. Around 72% of premium EV platforms now adopt liquid-based thermal management, while Phase Change Material solutions have expanded development activity by nearly 28% over recent product programs. Companies are strengthening product portfolios through material innovation, strategic partnerships, and application-specific engineering to address evolving battery performance requirements.

Battery Electric Vehicles (BEV) constitute the dominant application owing to larger battery capacities, higher charging rates, and greater thermal management requirements than other electrified vehicle categories. Nearly 75% of advanced battery cooling plate installations are concentrated in BEV platforms where temperature consistency directly influences battery efficiency and charging reliability. Plug-in Hybrid Electric Vehicles (PHEV) remain a significant segment, balancing battery cooling performance with compact vehicle architectures. Manufacturers continue expanding dedicated EV platforms and integrating modular thermal management systems to improve scalability and simplify production. Commercial Electric Vehicles represent the fastest-growing application as fleet electrification accelerates and high-duty operating conditions require robust cooling performance. Hybrid Electric Vehicles (HEV) continue utilizing compact cooling solutions focused on durability and cost efficiency. More than 35% of newly launched electric commercial vehicle platforms now feature upgraded liquid cooling technologies to support intensive operating cycles. Companies are expanding engineering collaboration with vehicle OEMs while optimizing cooling plate configurations for different battery sizes and operational requirements.

Passenger Vehicle OEMs remain the largest end-user group as global electric passenger vehicle production continues expanding across multiple price segments. Approximately 70% of battery cooling plate demand originates from passenger vehicle manufacturing, supported by increasing adoption of high-capacity battery systems and advanced charging technologies. OEMs are prioritizing integrated thermal management solutions that improve battery reliability while simplifying vehicle assembly. Commercial Vehicle OEMs continue strengthening procurement strategies as electric buses, trucks, and delivery vehicles require durable cooling systems capable of sustained heavy-duty operation. Battery Manufacturers represent the fastest-growing end-user segment as vertical integration becomes a strategic priority. Cell producers increasingly collaborate with thermal management suppliers during battery design, enabling optimized cooling architecture before vehicle assembly. The Aftermarket remains comparatively smaller but is expanding steadily through battery replacement, refurbishment, and performance upgrade services. Around 42% of battery manufacturers now participate in collaborative thermal engineering programs with automotive OEMs, while suppliers are introducing customized product platforms and long-term technical partnerships to strengthen competitive positioning.

Asia-Pacific accounted for the largest market share at 54.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 22.6% between 2026 and 2033.

North America is strengthening its position through expanding electric vehicle manufacturing capacity, domestic battery production, and localized thermal management supply chains. The region accounted for approximately 22.4% of global market activity in 2025, supported by large-scale battery plant construction and increasing integration of advanced liquid cooling systems into next-generation EV platforms. Vehicle manufacturers are prioritizing regional sourcing to reduce logistics risks and improve production continuity. Investments in automated component manufacturing and battery assembly continue to increase operational efficiency, while collaborative engineering programs between OEMs and thermal solution providers accelerate product development. More than 65% of newly commissioned battery facilities in the United States incorporate integrated thermal management planning during production design, strengthening supply-chain resilience and improving manufacturing scalability.

United States Market Outlook: The United States leads the regional market through large-scale battery manufacturing investments, strong EV production capacity, and expanding domestic supplier networks. Federal incentives continue supporting localized battery component manufacturing, while several gigafactory projects integrate advanced cooling technologies from initial production stages. More than 70% of newly announced battery manufacturing projects include dedicated thermal management suppliers, enabling stronger collaboration between battery producers and automotive OEMs while improving long-term production efficiency.

Europe continues expanding advanced battery manufacturing while emphasizing localized supply chains, sustainability, and high-performance vehicle engineering. The region represented approximately 18.9% of the global market in 2025, supported by aggressive battery production targets and increasing demand for efficient thermal management systems. Automotive manufacturers are integrating lightweight cooling technologies to improve battery performance and comply with stringent environmental standards. Cross-border industrial partnerships and investments in automated manufacturing are enhancing production capability across multiple countries. Battery recycling initiatives and localized raw material processing further strengthen supply-chain resilience while reducing dependence on imported components, supporting long-term competitiveness for regional manufacturers.

Germany Market Outlook: Germany remains Europe's strategic manufacturing hub, supported by premium automotive brands, advanced engineering expertise, and continuous investment in battery innovation. Automated production facilities increasingly utilize precision laser welding and digital inspection systems for cooling plate manufacturing. More than 60% of Germany's EV battery production projects include localized thermal management suppliers, reinforcing technological leadership while improving manufacturing quality and operational efficiency across the automotive value chain.

Asia-Pacific dominates the market through unmatched battery manufacturing capacity, integrated automotive supply chains, and rapid electric vehicle deployment. The region contributed approximately 54.8% of global demand in 2025, supported by large-scale battery production, advanced thermal component manufacturing, and competitive industrial ecosystems. China, South Korea, and Japan continue expanding production automation while increasing exports of battery-related components. More than 58% of global lithium-ion battery manufacturing capacity is concentrated within the region, creating sustained demand for high-performance cooling solutions. Companies continue investing in smart factories, localized aluminum processing, and automated assembly technologies to strengthen production efficiency and global supply reliability.

China Market Outlook: China remains the world's largest production center for electric vehicles and batteries, supported by integrated industrial clusters and advanced manufacturing infrastructure. The country continues expanding battery gigafactory capacity while strengthening domestic cooling plate production through automation and precision engineering. EV penetration exceeded 45% of new passenger vehicle sales, creating sustained demand for advanced battery thermal management technologies across both domestic and export-oriented manufacturing programs.

South America is gradually expanding electric mobility through commercial fleet electrification, public transportation modernization, and growing domestic vehicle assembly activity. The region accounted for approximately 2.6% of the global market in 2025, with demand primarily supported by electric buses, logistics vehicles, and urban mobility programs. Infrastructure investment remains uneven, yet manufacturers are establishing regional partnerships to improve component availability and technical support. Battery imports continue dominating supply, encouraging suppliers to strengthen localized distribution and engineering capabilities. Fleet operators increasingly prioritize durable thermal management systems capable of operating under demanding climatic conditions while minimizing maintenance requirements.

Brazil Market Outlook: Brazil leads regional adoption through expanding electric bus deployments, automotive manufacturing capability, and supportive industrial investment. Domestic vehicle manufacturers are strengthening collaborations with international battery technology providers while increasing localization of EV component assembly. More than 40% of regional electric vehicle production is concentrated in Brazil, positioning the country as the primary operational hub for future battery cooling technology deployment.

The Middle East & Africa market is progressing through government-backed mobility initiatives, industrial diversification, and expanding clean transportation investments. The region represented approximately 1.3% of global demand in 2025, with adoption concentrated in premium electric vehicles, commercial fleets, and pilot electrification projects. Infrastructure modernization and smart city developments are encouraging deployment of advanced battery technologies, while international partnerships support technical knowledge transfer and manufacturing capability. Companies are expanding regional service networks and engineering support to improve project execution and operational reliability as electric mobility ecosystems mature.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as the regional leader through ambitious smart mobility strategies, charging infrastructure expansion, and investment in advanced transportation technologies. Public-private partnerships continue supporting electric fleet deployment across urban mobility projects, while logistics operators increasingly evaluate battery thermal management solutions for commercial applications. More than 30% of the region's public charging infrastructure projects are concentrated in the UAE, reinforcing its position as a strategic electric mobility innovation hub.

The market is led by global thermal management specialists including Dana Incorporated, MAHLE, Modine Manufacturing, Valeo, and Boyd Corporation, competing directly against regional precision component manufacturers and specialized battery thermal solution providers. The top five companies collectively control approximately 46% of global market activity, creating a moderately consolidated competitive structure. Competition centers on thermal efficiency, lightweight engineering, manufacturing scale, and supply-chain responsiveness rather than price alone. Advanced liquid cooling solutions improve thermal performance by nearly 25%, while automated production reduces manufacturing defects by around 20% and localized sourcing shortens delivery cycles by approximately 15%. Companies are expanding production facilities, strengthening OEM partnerships, investing in aluminum microchannel technologies, and pursuing vertical integration with battery manufacturers. The competitive landscape is shifting toward integrated battery-pack thermal solutions, increasing pressure on standalone component suppliers. High qualification standards, precision manufacturing requirements, and long-term OEM validation remain significant entry barriers. Sustainable success depends on engineering excellence, localized manufacturing, reliable supply chains, and deep customer integration.

MAHLE GmbH

Modine Manufacturing Company

Valeo SA

Boyd Corporation

Nippon Light Metal Holdings Company, Ltd.

Sogefi S.p.A.

ESTRA Automotive Systems Co., Ltd.

SANHUA Automotive Components

Senior Flexonics

Yinlun Co., Ltd.

TitanX Engine Cooling AB

Battery cooling technology is advancing from conventional liquid channels toward microchannel aluminum plates, bionic flow-path designs, and integrated thermal management architectures. Microchannel cooling plates improve heat transfer efficiency by nearly 20%, while optimized coolant distribution enhances temperature uniformity by approximately 18%. More than 70% of newly developed premium EV battery platforms now prioritize integrated liquid cooling systems to support high-power charging and higher energy-density battery packs.

Emerging technologies include AI-assisted thermal simulation, digital twins for cooling system optimization, laser-welded plate manufacturing, and embedded temperature sensing. Compared with conventional air-cooled systems, advanced liquid cooling solutions deliver approximately 35% higher thermal efficiency while reducing battery temperature variation by nearly 30%. Automotive OEMs and battery manufacturers benefit the most because integrated cooling architectures improve charging consistency, extend battery service life, and simplify vehicle packaging. Automated inspection and predictive quality analytics also reduce manufacturing defects by approximately 20%, strengthening operational reliability.

Between 2026 and 2028, intelligent thermal management platforms integrating software-driven control with modular cooling plates are expected to become standard across high-performance electric vehicles. Companies investing early in advanced manufacturing automation, lightweight materials, and integrated battery engineering will strengthen competitive positioning, accelerate product validation, improve production scalability, and secure preferred supplier status within expanding global electric mobility supply chains.

October 2025 MAHLE secured its first series order for a liquid cooling module for stationary battery storage, delivering up to 42 kW of cooling capacity with production beginning in 2026. The expansion diversifies thermal management expertise beyond automotive. Source: www.newsroom.mahle.com

April 2026 MAHLE highlighted its biomimetic battery cooling plate technology featuring coral-inspired flow channels that increase cooling capacity by 10% while reducing pressure loss by 20%. The innovation improves fast-charging performance and battery durability. Source: www.mahle-aftermarket.com

May 2025 MAHLE showcased its next-generation bionic battery cooling plate portfolio, reducing material consumption by 15% while increasing cooling performance by 10%. The development strengthens lightweight thermal management for next-generation electric vehicles. Source: www.newsroom.mahle.com

October 2025 MAHLE expanded industrial thermal management by introducing compact liquid cooling modules for battery energy storage applications, enabling optimal operating temperatures between 20°C and 30°C. The move broadens commercialization opportunities beyond electric vehicles.

The report provides comprehensive analysis across Liquid Cooling Plate, Air Cooling Plate, Phase Change Material Cooling Plate, and Other technologies, together with detailed assessment of Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Hybrid Electric Vehicles (HEV), and Commercial Electric Vehicles. It evaluates demand across Passenger Vehicle OEMs, Commercial Vehicle OEMs, Battery Manufacturers, and the Aftermarket while examining deployment patterns, technology adoption, and evolving thermal management strategies across major global regions. More than 70% of advanced EV platforms currently prioritize liquid thermal management, reflecting changing engineering requirements.

The study delivers strategic insights into manufacturing trends, supply-chain localization, competitive positioning, battery thermal innovations, automation, lightweight materials, and integrated cooling technologies. Regional benchmarking, company profiling, technology assessment, and market segmentation support investment planning, product portfolio development, expansion strategy, partnership evaluation, and long-term business decision-making between 2026 and 2033 while identifying emerging application opportunities and competitive priorities across the electric mobility ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 274.0 Million |

| Market Revenue (2033) | USD 1,292.7 Million |

| CAGR (2026–2033) | 21.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Dana Incorporated; MAHLE GmbH; Modine Manufacturing Company; Valeo SA; Boyd Corporation; Nippon Light Metal Holdings Company, Ltd.; Sogefi S.p.A.; ESTRA Automotive Systems Co., Ltd.; SANHUA Automotive Components; Senior Flexonics; Yinlun Co., Ltd.; TitanX Engine Cooling AB |

| Customization & Pricing | Available on Request (10% Customization Free) |