Reports

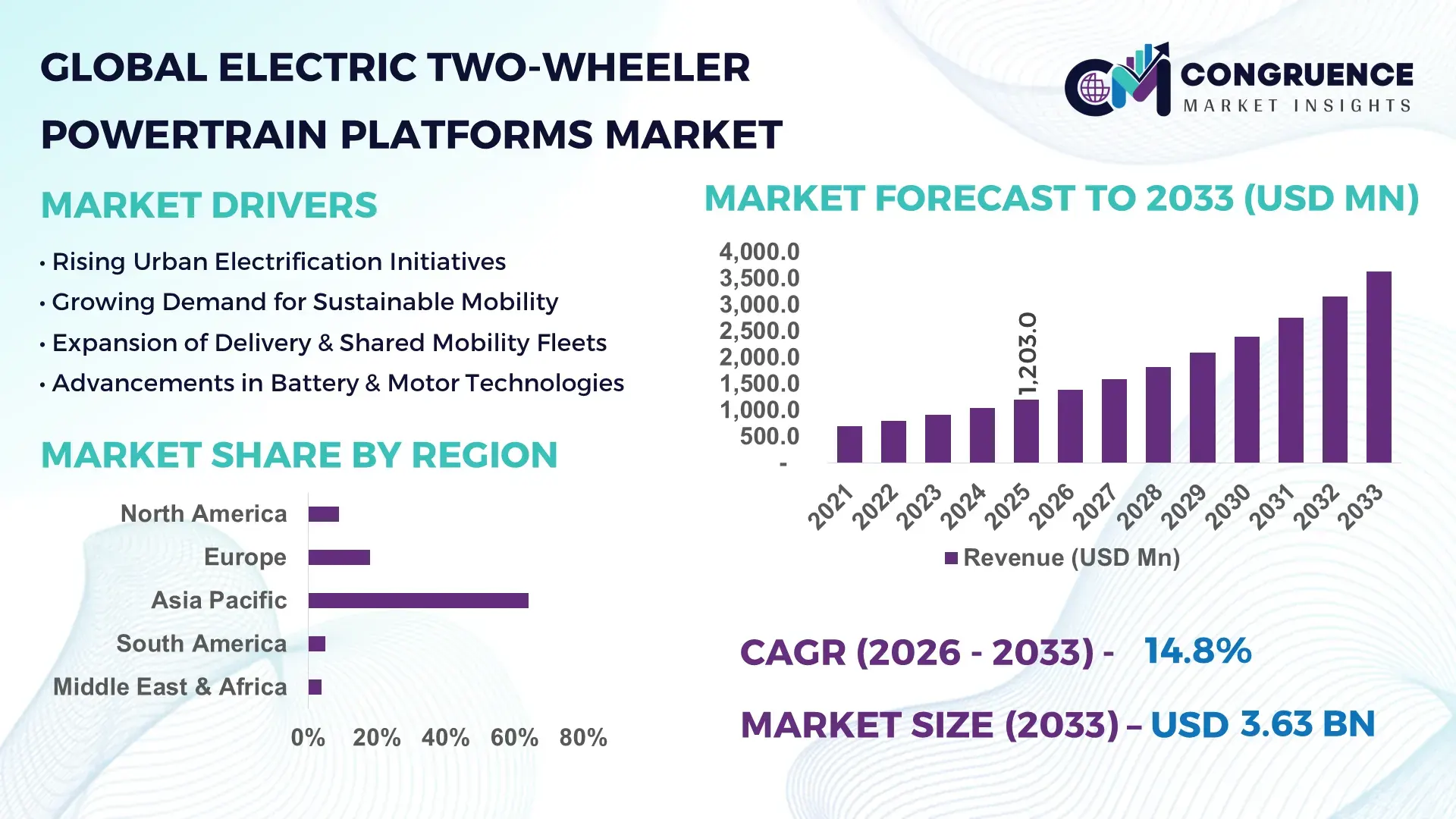

The Global Electric Two-Wheeler Powertrain Platforms Market was valued at USD 1,203.0 Million in 2025 and is anticipated to reach a value of USD 3,621.1 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by accelerating electrification of urban mobility supported by battery cost optimization and policy-backed EV infrastructure expansion.

China continues to dominate the Electric Two-Wheeler Powertrain Platforms Market in terms of manufacturing scale and industrial capacity. In 2025, China produced over 38 million electric two-wheelers, supported by more than 300 specialized EV component manufacturers. The country’s lithium-ion battery production capacity exceeded 900 GWh annually, enabling vertically integrated powertrain manufacturing. Government-backed investments in EV infrastructure surpassed USD 15 billion over the past three years, supporting over 2.5 million public charging points nationwide. Advanced motor technologies such as high-efficiency hub motors and integrated controller systems are widely deployed, with domestic suppliers exporting to Southeast Asia and Europe. Urban adoption remains strong, with electric two-wheelers accounting for nearly 55% of total two-wheeler sales in major metropolitan provinces.

Market Size & Growth: Valued at USD 1,203.0 Million in 2025, projected to reach USD 3,621.1 Million by 2033 at 14.8% CAGR, driven by urban mobility electrification and battery price reductions exceeding 35% in the past decade.

Top Growth Drivers: EV adoption rate growth 28%; lithium-ion efficiency improvement 18%; government subsidy coverage expansion 22%.

Short-Term Forecast: By 2028, integrated powertrain systems are expected to reduce system weight by 12% and improve energy efficiency by 15%.

Emerging Technologies: Silicon-carbide inverters, AI-based battery management systems, modular swappable battery platforms.

Regional Leaders: Asia Pacific projected USD 1,950 Million by 2033 with mass urban adoption; Europe USD 890 Million with premium e-scooter uptake; North America USD 610 Million driven by fleet electrification.

Consumer/End-User Trends: Over 48% of urban commuters prefer electric scooters for sub-10 km travel; delivery fleets show 35% conversion to electric platforms.

Pilot Example: In 2025, a Southeast Asian fleet pilot improved energy efficiency by 17% and reduced maintenance downtime by 21% using integrated controller platforms.

Competitive Landscape: Market leader holds ~24% share; key competitors include Bosch, Nidec, Yamaha Motor, BYD, and Delta Electronics.

Regulatory & ESG Impact: Over 40 countries offer purchase incentives; manufacturers target 30% lifecycle emission reduction by 2030.

Investment Patterns: More than USD 4.5 Billion invested globally in EV powertrain R&D and gigafactory expansion since 2023.

Innovation & Outlook: Integration of smart diagnostics, high-density batteries, and digital twin simulation is reshaping system-level efficiency.

The Electric Two-Wheeler Powertrain Platforms Market integrates battery packs, motors, controllers, and drivetrain systems, serving urban commuting (52%), commercial delivery (28%), and shared mobility (14%). Recent innovations include integrated hub motor systems reducing weight by 10% and smart BMS improving cycle life by 20%. Regulatory emission targets and fuel cost volatility continue to influence adoption. Asia Pacific leads consumption, while Europe shows strong growth in premium electric motorcycles, reinforcing long-term electrification strategies.

The Electric Two-Wheeler Powertrain Platforms Market holds strong strategic relevance as cities worldwide pursue carbon-neutral transportation systems and energy diversification. Electric two-wheelers consume nearly 70% less operating energy per kilometer compared to internal combustion engine (ICE) scooters, positioning advanced powertrain platforms as core enablers of cost-efficient mobility. Silicon-carbide inverter technology delivers 8% higher power efficiency compared to traditional IGBT-based systems, while advanced lithium iron phosphate batteries extend lifecycle durability by nearly 25% compared to earlier lithium-ion chemistries.

Asia Pacific dominates in production volume, while Europe leads in adoption with nearly 42% of urban micro-mobility enterprises integrating electric fleets. By 2028, AI-driven battery management systems are expected to reduce unexpected battery failures by 20% and improve thermal performance stability by 18%. Firms are committing to ESG targets including 30% recyclable battery material usage by 2030 and 25% reduction in supply-chain emissions.

In 2025, India achieved a 16% improvement in fleet uptime through smart telematics-enabled powertrain optimization in urban logistics operations. Such initiatives demonstrate measurable productivity gains through digital integration.

Looking forward, the Electric Two-Wheeler Powertrain Platforms Market will function as a pillar of resilience, regulatory compliance, and sustainable growth by combining electrification, digitalization, and localized manufacturing strategies.

The Electric Two-Wheeler Powertrain Platforms Market is influenced by urban congestion trends, battery innovation cycles, supply chain localization policies, and environmental compliance mandates. Lithium-ion battery pack energy density has increased by nearly 30% over the past five years, directly enhancing vehicle range performance. Public charging infrastructure has expanded by over 40% globally since 2022, supporting daily commuter reliance. OEMs are increasingly adopting integrated motor-controller architectures to reduce assembly complexity by approximately 15%. Additionally, raw material price volatility, especially lithium and cobalt, remains a key variable impacting production planning. Strategic collaborations between battery manufacturers and motor suppliers are intensifying, enabling modular powertrain ecosystems adaptable across scooter and motorcycle platforms.

Urban areas account for more than 56% of global population concentration, intensifying demand for compact, efficient transportation solutions. Electric two-wheelers offer up to 60% lower operational costs compared to gasoline scooters, encouraging fleet and individual adoption. Government subsidies covering up to 20% of vehicle purchase costs in multiple regions stimulate procurement. Fleet operators report maintenance cost reductions of 25% due to fewer moving components in electric drivetrains. Rising fuel price volatility further accelerates conversion to electric alternatives, reinforcing sustained platform demand.

Lithium carbonate prices experienced fluctuations exceeding 40% in recent years, impacting production cost stability. Dependence on limited geographic mining sources increases supply chain risk. Battery pack components represent nearly 35% of total powertrain system cost, making price volatility a significant challenge. Additionally, recycling infrastructure remains underdeveloped in several regions, limiting material recovery rates to below 20%. These factors constrain predictable scaling of manufacturing capacity.

Battery swapping networks reduce vehicle downtime by over 70% compared to plug-in charging. In dense urban regions, swap stations can serve more than 200 vehicles daily, improving fleet utilization rates by nearly 18%. Modular powertrain compatibility with standardized battery packs enables cross-brand infrastructure integration. Expansion of such networks across Southeast Asia and India is projected to significantly enhance last-mile delivery electrification efficiency.

Rural charging penetration remains below 35% in developing regions, limiting adoption outside metropolitan zones. Grid stability concerns affect high-capacity fast-charging deployment. Additionally, harmonization of technical standards across manufacturers remains limited, increasing interoperability complexity. Training skilled technicians for high-voltage systems remains another constraint, with workforce readiness levels below 50% in several emerging economies.

Integrated Motor-Controller Architectures Improving Efficiency by 15%: Manufacturers are consolidating inverter and motor assemblies into single compact modules, reducing wiring complexity by 20% and improving thermal efficiency by 15%. Lightweight aluminum casings lower overall vehicle mass by nearly 8%, enhancing driving range.

Rapid Expansion of Battery Swapping Networks by 40% Annually: Urban swap station installations have grown by over 40% year-on-year in major Asian cities. Average swap time remains under 3 minutes, increasing fleet productivity by 18% compared to traditional charging.

AI-Based Battery Health Monitoring Reducing Failures by 20%: Smart BMS integration enables predictive diagnostics, cutting unexpected battery failures by 20% and extending average battery life cycles beyond 1,500 charge cycles.

Localization of Component Manufacturing Reaching 65% in Key Markets: Domestic sourcing of motors and controllers has reached 65% in Asia Pacific markets, reducing import dependency by 25% and strengthening supply chain resilience.

The Electric Two-Wheeler Powertrain Platforms Market is segmented by type, application, and end-user, reflecting technological specialization and diverse mobility needs. Battery-electric platforms dominate product configurations, while hybrid-assisted systems serve transitional markets. Applications range from personal commuting to commercial logistics and shared mobility operations. End-users include OEM manufacturers, fleet operators, and aftermarket system integrators. Increasing demand for modular architecture supports cross-segment compatibility and cost optimization.

Battery-electric powertrain platforms account for approximately 68% of total adoption due to full electrification benefits and simplified drivetrain design. Hub motor systems contribute nearly 45% within this category because of compactness and reduced maintenance requirements. Mid-drive motor platforms represent around 23%, favored in performance-oriented electric motorcycles for balanced weight distribution and torque optimization. Swappable battery-compatible systems are the fastest-growing segment, expanding at an estimated 18.5% CAGR due to urban fleet demand and reduced charging downtime. Integrated motor-controller units enhance energy conversion efficiency by up to 12%, strengthening adoption among OEMs seeking lightweight architectures. Other configurations, including hybrid-assisted and range-extended variants, collectively account for nearly 9% of installations, serving niche geographies with infrastructure constraints. Continuous R&D in silicon-carbide power modules improves switching efficiency by 8% compared to legacy inverter systems, further strengthening high-performance segments.

In 2025, a national transport research program demonstrated that hub motor-equipped electric scooters reduced maintenance interventions by 22% compared to chain-driven alternatives, accelerating fleet operator preference for integrated systems.

Personal urban commuting dominates with nearly 52% usage share, driven by daily sub-15 km travel requirements and lower total ownership costs. Commercial delivery applications hold around 28%, benefiting from 25% lower maintenance expenditure and 30% quieter operation compared to ICE counterparts. Shared mobility platforms contribute approximately 14%, with adoption expanding at 17.2% CAGR as cities promote low-emission ride-sharing services. Performance and recreational electric motorcycles account for the remaining 6%, supported by rising interest in high-torque electric drivetrains. Fleet electrification programs significantly accelerate commercial adoption, with over 38% of logistics enterprises piloting electric two-wheelers in 2025. Urban commuters report 48% preference for electric scooters due to fuel savings and ease of navigation in congested zones.

In 2025, a government-backed smart mobility initiative deployed over 10,000 electric delivery scooters across metropolitan regions, improving last-mile efficiency by 19% and reducing carbon emissions by 24% annually.

OEM manufacturers represent the leading end-user group, accounting for nearly 61% of total powertrain platform procurement due to direct integration into new vehicle production lines. Fleet operators follow with approximately 27%, driven by cost optimization and regulatory compliance goals. Aftermarket integrators and retrofit solution providers collectively contribute around 12%, supporting legacy vehicle electrification initiatives. Fleet operators are the fastest-growing end-user segment, expanding at an estimated 19.3% CAGR as e-commerce and food delivery demand rises. Over 35% of urban logistics providers transitioned at least part of their fleet to electric platforms in 2025. Among individual consumers, 46% of first-time EV buyers selected electric scooters due to lower operational complexity.

In 2025, a national EV adoption survey reported that more than 40% of small and medium urban delivery enterprises integrated electric two-wheelers to meet emission compliance targets, achieving operational cost reductions of 18% within the first year.

Asia-Pacific accounted for the largest market share at 64% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by annual production exceeding 40 million electric two-wheelers, with China and India collectively contributing over 85% of regional output. More than 70% of global lithium-ion battery cell manufacturing capacity is concentrated in this region, strengthening vertical integration in powertrain systems. Europe accounted for approximately 18% market share in 2025, supported by over 1.5 million registered electric two-wheelers and expanding low-emission urban zones across 200+ cities. North America held nearly 9% share, driven by fleet electrification and technology integration. South America and the Middle East & Africa together represented around 9%, reflecting early-stage adoption but increasing government incentives and infrastructure investments exceeding 25% annual expansion in charging networks.

North America accounted for approximately 9% of the global Electric Two-Wheeler Powertrain Platforms Market in 2025, supported by rising demand in urban delivery, shared mobility, and campus transportation networks. The United States and Canada collectively registered over 250,000 electric scooters and motorcycles in operation. Fleet operators in logistics and food delivery contribute nearly 42% of regional demand. Regulatory measures, including federal tax credits covering up to 30% of eligible EV equipment and state-level zero-emission mandates, encourage adoption. Technological advancements include AI-enabled battery diagnostics and telematics integration improving fleet uptime by 18%. Companies such as Zero Motorcycles are investing in high-performance electric powertrains with torque outputs exceeding 140 Nm for urban and highway use. Regional consumer behavior shows higher adoption among enterprise users in logistics and municipal services, with nearly 37% of fleet operators piloting electrified two-wheelers for last-mile operations.

Europe represented approximately 18% of the Electric Two-Wheeler Powertrain Platforms Market in 2025, with Germany, France, Italy, and the Netherlands leading registrations. Germany alone recorded more than 180,000 electric two-wheelers in active circulation. Over 250 European cities have implemented low-emission or zero-emission zones, driving regulatory-backed electrification. The European Green Deal targets a 55% reduction in transport-related emissions by 2030, reinforcing powertrain innovation. Emerging technologies such as silicon-carbide-based inverters and high-density battery packs are increasingly integrated into premium electric motorcycles. Companies like Bosch are expanding production of compact e-drive units designed for lightweight scooters and motorcycles. European consumer behavior is shaped by environmental compliance awareness, with 48% of urban commuters prioritizing emission-free mobility solutions.

Asia-Pacific ranks first globally in volume, exceeding 40 million annual electric two-wheeler sales. China, India, Japan, and Vietnam are the top-consuming countries. China alone accounts for over 35 million annual units, while India surpassed 1.5 million electric two-wheeler sales in 2025. Regional battery production capacity exceeds 900 GWh annually, supporting localized powertrain manufacturing. Manufacturing hubs in Guangdong, Zhejiang, and Tamil Nadu produce motors, controllers, and integrated drive units at scale, reducing component costs by nearly 20%. Companies such as Nidec are expanding motor production capacity to meet domestic and export demand. Consumer adoption is driven by affordability and high urban density, with electric two-wheelers representing more than 55% of total two-wheeler sales in major Chinese cities.

South America holds approximately 5% share of the Electric Two-Wheeler Powertrain Platforms Market, with Brazil, Colombia, and Argentina leading adoption. Brazil accounts for nearly 60% of regional electric two-wheeler registrations. Charging infrastructure installations increased by 28% in 2025, particularly in São Paulo and Bogotá. Government import tax reductions on EV components and incentives covering up to 15% of purchase cost stimulate demand. Energy diversification policies promoting renewable electricity integration further support electrified mobility. Regional consumer behavior indicates growing interest in cost-effective commuting solutions, with nearly 33% of urban riders considering electric alternatives for daily travel.

Middle East & Africa accounts for roughly 4% of the Electric Two-Wheeler Powertrain Platforms Market. The UAE and South Africa lead regional adoption. The UAE has deployed over 1,200 public charging stations, while South Africa recorded a 22% increase in EV-related registrations in 2025. Smart city initiatives in Dubai and Abu Dhabi integrate electric mobility platforms within sustainability frameworks targeting 30% emission reduction by 2030. Local distributors are partnering with Asian manufacturers to localize assembly operations, reducing import costs by nearly 18%. Consumer demand is concentrated in commercial delivery and tourism-based mobility services.

China – 58% Market Share: Dominates due to high production capacity exceeding 35 million units annually and vertically integrated battery manufacturing.

India – 12% Market Share: Strong growth supported by policy incentives and over 1.5 million annual electric two-wheeler sales.

The Electric Two-Wheeler Powertrain Platforms Market is moderately fragmented, with more than 120 active global and regional participants specializing in motors, battery systems, controllers, and integrated drive units. The top five companies collectively account for approximately 46% of total market share, indicating competitive intensity but room for emerging innovators.

Major players compete on battery efficiency improvements of 10–15%, torque optimization exceeding 20%, and digital BMS capabilities enhancing lifecycle performance by up to 25%. Strategic initiatives include joint ventures between motor manufacturers and battery suppliers, localization of assembly plants reducing logistics costs by 18%, and R&D investments exceeding USD 500 million annually across leading firms.

Partnership-driven ecosystem models are expanding, particularly in battery swapping and fleet electrification networks. Companies are also prioritizing silicon-carbide inverter integration and AI-enabled telematics to differentiate offerings. Continuous product launches in lightweight modular platforms indicate technology-driven competition rather than price-only rivalry.

Nidec Corporation

Yamaha Motor Co., Ltd.

BYD Company Ltd.

Delta Electronics, Inc.

Zero Motorcycles

Gogoro Inc.

Mahle GmbH

Valeo SA

Hero Electric Vehicles Pvt. Ltd.

Ather Energy

TVS Motor Company

Vmoto Limited

NIU Technologies

Technological advancements in the Electric Two-Wheeler Powertrain Platforms Market center on battery chemistry optimization, power electronics efficiency, and digital integration. Lithium iron phosphate batteries now achieve cycle lives exceeding 2,000 cycles, while energy density improvements surpass 30% compared to 2018 standards. Silicon-carbide MOSFET inverters enhance switching efficiency by approximately 8% and reduce thermal losses by 12%.

Integrated motor-controller architectures lower system weight by 10% and improve torque response time by 15%. Hub motor technology remains prevalent in urban scooters, whereas mid-drive motors are increasingly deployed in high-performance motorcycles generating over 25 kW power output. AI-driven BMS platforms enable predictive maintenance, cutting unexpected failures by nearly 20%.

Digital twin simulations reduce prototype development time by 22%, accelerating time-to-market. Battery swapping compatibility and modular design standards further promote interoperability across vehicle models, strengthening scalability and operational efficiency for fleet operators.

• In February 2026, Gogoro Inc. reported its 2025 financial results, showing a significant improvement in operating cash flow to $31.1 million (from $9.9 million in 2024), narrowing its net loss to $(80.8) million, and boosting non-IFRS gross margin to 19.5% as a result of operational streamlining and battery pack upgrades. Gogoro also completed voluntary battery upgrade initiatives that increase long-term battery capacity and second-life potential, reflecting enhanced operational performance and network efficiency. Source: www.prnewswire.com

• In November 2025, Gogoro Inc. released its third quarter 2025 financial results, highlighting operating cash flow improvements to $25.7 million in the first nine months and sequential margin increases, while expanding its product lineup with models such as EZZY and EZZY 500 to broaden market reach across price segments. Additionally, its Powered by Gogoro Network (PBGN) ecosystem saw enhanced partner adoption, including collaboration with Yamaha on the CUXiE model.

• In June 2025, Nidec Corporation officially initiated production at the new Orchard Hub campus in Hubli-Dharwad, Karnataka, India, a major manufacturing facility expected to strengthen electric motor and drivetrain component production with advanced lean manufacturing processes, reinforcing its footprint in a key EV market.

• In August and September 2025, Bosch showcased enhanced mobility innovations at major automotive trade events, including intelligent electric drive systems and software-driven mobility solutions that integrate hardware and software platforms — demonstrating Bosch’s broader electrification strategy. Boschelaborated on new hardware and software integration for electrified vehicle platforms, signaling its ongoing investment in connected and powered electric mobility architectures.

The Electric Two-Wheeler Powertrain Platforms Market Report provides comprehensive coverage of integrated propulsion systems including batteries, electric motors, controllers, inverters, and drivetrain components. The report analyzes segmentation across battery-electric, hybrid-assisted, hub motor, and mid-drive configurations, alongside applications such as personal commuting, shared mobility, logistics delivery, and performance motorcycles.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating country-level insights for major markets including China, India, Germany, the United States, Brazil, and the UAE. The report evaluates over 120 active companies, highlighting technology integration trends such as AI-based battery diagnostics, silicon-carbide power electronics, and modular battery swapping platforms.

Industry focus areas include regulatory frameworks influencing adoption, emission reduction targets, infrastructure expansion exceeding 25% annual growth in key cities, and manufacturing localization rates surpassing 60% in Asia-Pacific. Emerging segments such as fleet electrification, swappable battery ecosystems, and high-performance electric motorcycles are analyzed to provide forward-looking insights for strategic decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,203.0 Million |

| Market Revenue (2033) | USD 3,621.1 Million |

| CAGR (2026–2033) | 14.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bosch; Nidec Corporation; Yamaha Motor Co., Ltd.; BYD Company Ltd.; Delta Electronics, Inc.; Zero Motorcycles; Gogoro Inc.; Mahle GmbH; Valeo SA; Hero Electric Vehicles Pvt. Ltd.; Ather Energy; TVS Motor Company; Vmoto Limited; NIU Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |