Reports

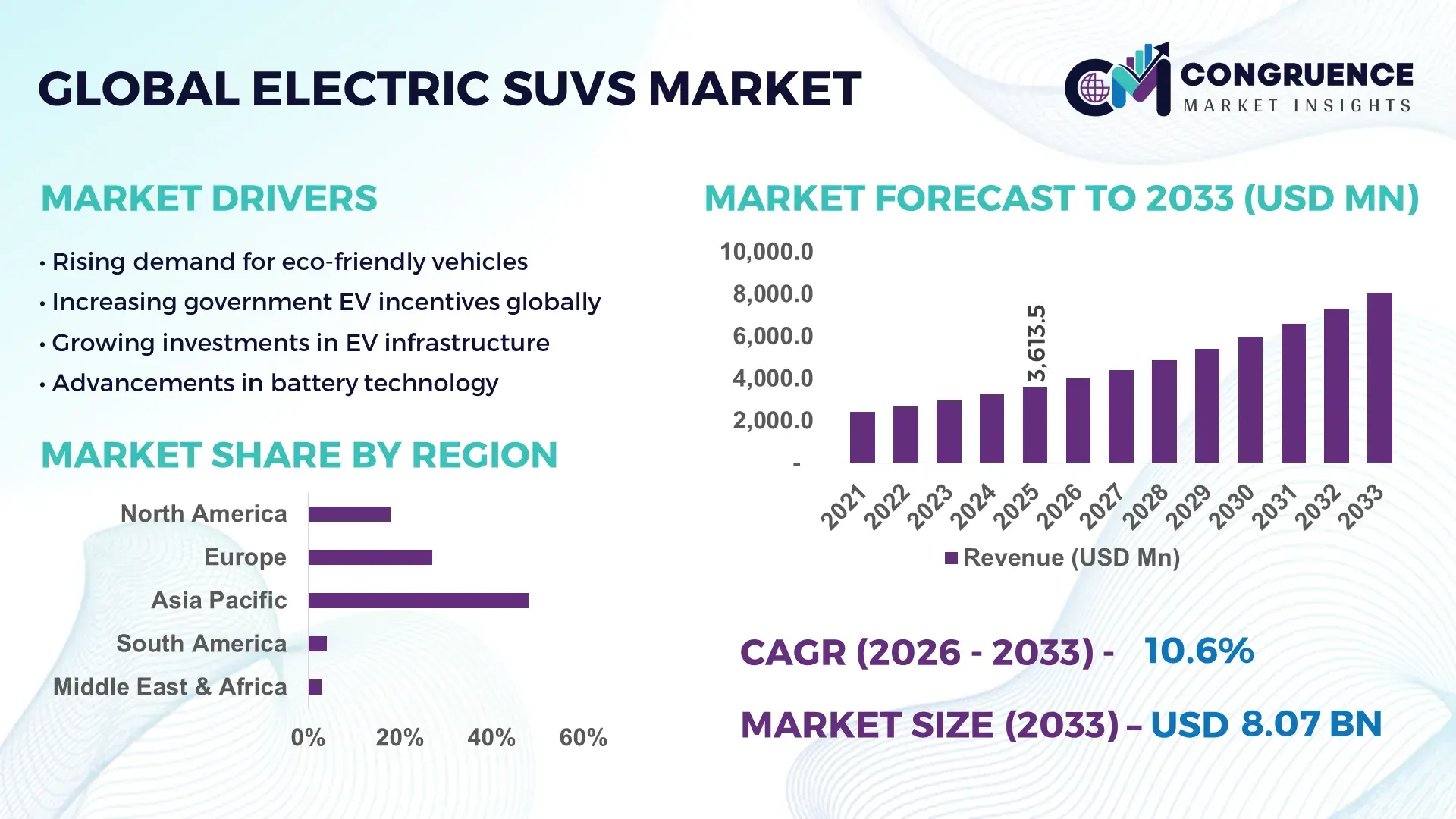

The Global Electric SUVs Market was valued at USD 3,613.5 Million in 2025 and is anticipated to reach a value of USD 8,067.0 Million by 2033 expanding at a CAGR of 10.56% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerating electrification policies and rising consumer demand for high-performance, low-emission vehicles.

China remains the dominant country in the Electric SUVs Market, supported by its large-scale EV manufacturing ecosystem and advanced battery supply chain. In 2025, China accounted for over 55% of global EV production volume, with electric SUVs representing nearly 48% of total EV sales domestically. The country operates more than 6 million public charging points, enabling widespread consumer adoption. Investments exceeding USD 120 billion have been directed toward EV infrastructure and battery innovation between 2020 and 2025. Leading manufacturers such as BYD and NIO are expanding production capacity beyond 3 million EV units annually, with electric SUVs forming a substantial share. Additionally, over 35% of urban households in Tier-1 cities have adopted electric SUVs, reflecting strong consumer penetration and advanced technological integration such as autonomous driving features and AI-based battery management systems.

Market Size & Growth: Valued at USD 3,613.5 Million in 2025, projected to reach USD 8,067.0 Million by 2033, expanding at 10.56% CAGR, driven by electrification mandates and consumer shift toward sustainable mobility.

Top Growth Drivers: EV adoption increased by 42%, battery efficiency improved by 28%, charging infrastructure expanded by 35%.

Short-Term Forecast: By 2028, battery costs are expected to decline by 22%, improving affordability and adoption rates.

Emerging Technologies: Solid-state batteries, AI-driven energy management systems, and vehicle-to-grid (V2G) integration.

Regional Leaders: Asia-Pacific to reach USD 3,500 Million by 2033 driven by mass adoption; North America USD 2,100 Million with premium EV demand; Europe USD 1,800 Million led by strict emission norms.

Consumer/End-User Trends: Urban consumers represent over 60% adoption, with increasing preference for mid-range and luxury electric SUVs.

Pilot or Case Example: In 2024, a European EV fleet project improved energy efficiency by 18% through AI-powered route optimization.

Competitive Landscape: Market leader holds ~18% share, followed by Tesla, BYD, Volkswagen, Hyundai, and Ford.

Regulatory & ESG Impact: Over 70 countries have EV incentives; emission reduction targets mandate 30% lower fleet emissions by 2030.

Investment & Funding Patterns: Over USD 200 billion invested globally in EV infrastructure and battery innovation since 2020.

Innovation & Future Outlook: Integration of autonomous driving and connected vehicle ecosystems expected to enhance performance by 25%.

Electric SUVs are increasingly integrated across passenger mobility, ride-hailing, and logistics sectors, with passenger vehicles contributing nearly 65% of demand. Innovations such as fast-charging batteries and AI-enabled driving systems are reshaping product offerings. Regulatory mandates, urbanization trends, and sustainability goals are accelerating adoption, particularly in Asia-Pacific and Europe, while North America sees rising demand for premium electric SUVs and advanced mobility solutions.

The Electric SUVs Market holds strong strategic relevance as global automotive ecosystems transition toward electrification and sustainability targets. Governments and corporations are aligning with zero-emission goals, with over 65% of automakers committing to fully electric portfolios by 2035. Electric SUVs, combining utility with sustainability, are becoming central to product strategies, particularly in urban and semi-urban mobility segments. Battery-electric powertrains deliver 35% higher energy efficiency compared to internal combustion engine (ICE) vehicles, significantly reducing operating costs and emissions.

Technological advancements such as solid-state batteries deliver 40% improvement compared to traditional lithium-ion systems in terms of energy density and charging speed. Asia-Pacific dominates in volume, while Europe leads in adoption with over 52% of new vehicle buyers considering EVs as their primary option. By 2028, AI-driven battery optimization systems are expected to improve vehicle range by 25%, enhancing consumer confidence and usability.

From an ESG perspective, firms are committing to reducing carbon emissions by 45% by 2030 through electrified fleets and sustainable manufacturing practices. In 2024, Tesla achieved a 20% increase in battery efficiency through advanced cell design innovations, showcasing measurable technological progress.

The future pathways of the Electric SUVs Market include integration with smart grids, expansion of ultra-fast charging infrastructure, and deployment of autonomous driving technologies. These developments position the market as a key pillar for resilient, compliant, and sustainable mobility transformation across global automotive ecosystems.

The Electric SUVs Market is shaped by rapid technological evolution, regulatory interventions, and shifting consumer preferences toward sustainable mobility solutions. Governments across major economies are implementing stricter emission standards and offering financial incentives to accelerate EV adoption. The expansion of charging infrastructure, which has grown by over 30% globally between 2022 and 2025, is significantly improving accessibility and convenience for electric SUV users. Additionally, advancements in battery technology have increased average vehicle range by over 20%, addressing one of the primary concerns of consumers.

Automakers are diversifying their electric SUV portfolios across price segments, with mid-range models accounting for nearly 50% of new launches. Digital integration, including AI-based navigation and energy management systems, is enhancing vehicle performance and user experience. However, supply chain constraints, particularly in lithium and semiconductor availability, continue to influence production timelines. Overall, the market reflects strong forward momentum supported by innovation, policy support, and evolving consumer expectations.

The surge in electric vehicle adoption is a major driver of the Electric SUVs Market, with global EV sales surpassing 14 million units in 2025, representing a 35% year-on-year increase. Electric SUVs account for nearly 45% of these sales due to their versatility and consumer preference for larger vehicles. Governments in over 60 countries are offering subsidies covering up to 25% of vehicle costs, making electric SUVs more accessible. Additionally, advancements in charging infrastructure—growing at a rate of 30% annually—have reduced range anxiety significantly. Corporate fleet electrification is also contributing, with over 40% of logistics companies integrating electric SUVs into their operations. These factors collectively enhance adoption rates and accelerate market growth.

Despite technological progress, high battery costs remain a critical restraint in the Electric SUVs Market. Lithium-ion batteries account for approximately 30–40% of the total vehicle cost, significantly impacting pricing. Raw material prices, particularly lithium and cobalt, have experienced volatility, with lithium prices increasing by over 70% between 2021 and 2024. Additionally, limited recycling infrastructure means only about 15% of EV batteries are currently recycled globally, increasing dependency on raw material extraction. These cost challenges limit affordability, especially in emerging markets, where price sensitivity remains high. Furthermore, supply chain disruptions and geopolitical factors continue to affect battery production and availability.

The rapid expansion of EV charging infrastructure presents significant opportunities for the Electric SUVs Market. By 2025, global public charging points exceeded 7 million units, growing by more than 35% annually. Fast-charging stations, capable of delivering 80% charge within 20 minutes, are being deployed across highways and urban centers. Governments are investing heavily, with the European Union allocating over USD 30 billion toward EV infrastructure development. Private sector participation is also increasing, with energy companies and automotive firms collaborating to build integrated charging networks. This infrastructure growth reduces range anxiety and enhances consumer confidence, opening new avenues for market expansion, particularly in emerging economies.

Supply chain disruptions remain a significant challenge for the Electric SUVs Market, particularly in sourcing critical materials such as lithium, cobalt, and semiconductors. Over 60% of global lithium processing is concentrated in a few countries, creating supply vulnerabilities. Semiconductor shortages have impacted vehicle production, delaying deliveries by up to 20% in certain regions. Additionally, geopolitical tensions and trade restrictions have disrupted global supply chains, affecting component availability and manufacturing efficiency. Logistics costs have also increased by nearly 25% since 2022, further impacting production timelines. These challenges require strategic diversification of supply sources and investment in local manufacturing capabilities.

Rapid Expansion of Fast-Charging Infrastructure: Global fast-charging stations increased by over 40% between 2023 and 2025, with ultra-fast chargers (150 kW+) accounting for nearly 35% of new installations. This has reduced average charging time by 50%, significantly improving convenience for electric SUV users and boosting long-distance travel feasibility.

Integration of Advanced Driver Assistance Systems (ADAS): Over 65% of newly launched electric SUVs in 2025 are equipped with Level 2 or higher ADAS features, enhancing safety and driving efficiency. AI-based systems have reduced accident rates by approximately 20%, driving consumer preference toward technologically advanced models.

Surge in Battery Innovation and Energy Density Improvements: Battery energy density has improved by nearly 30% since 2022, enabling electric SUVs to achieve ranges exceeding 500 km per charge. Solid-state battery prototypes demonstrate up to 50% higher energy efficiency, indicating a significant shift in future product capabilities.

Rising Demand for Premium and Luxury Electric SUVs: Premium electric SUVs account for over 38% of total sales in developed markets, with consumer preference shifting toward high-performance vehicles offering advanced connectivity and autonomous features. This segment has seen a 25% increase in adoption among high-income urban consumers.

The Electric SUVs Market is segmented based on type, application, and end-user categories, reflecting diverse demand patterns across global regions. Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs) dominate the type segment, with BEVs gaining higher traction due to zero-emission capabilities and expanding charging infrastructure. Applications primarily include personal mobility, commercial fleet usage, and ride-hailing services, with personal mobility contributing the majority of demand. End-user segmentation highlights individual consumers, fleet operators, and corporate users, each exhibiting distinct adoption trends. Increasing urbanization, regulatory incentives, and technological advancements are influencing segmentation dynamics, with mid-range and premium electric SUVs gaining prominence across developed and emerging markets.

Battery Electric Vehicles (BEVs) dominate the Electric SUVs Market, accounting for approximately 62% of total adoption due to their zero-emission capability and growing charging infrastructure. Plug-in Hybrid Electric Vehicles (PHEVs) hold around 28% share, offering flexibility through combined electric and fuel-based systems, particularly in regions with limited charging networks. However, adoption in BEVs is rising fastest, expected to grow at a CAGR of 12.8% due to advancements in battery technology and increasing government incentives. Fuel Cell Electric Vehicles (FCEVs) and hybrid electric SUVs collectively contribute nearly 10% of the market, primarily serving niche segments where hydrogen infrastructure is being developed. BEVs remain the preferred choice in urban regions, where over 70% of consumers prioritize sustainability and lower operational costs.

• In 2025, a government-backed EV initiative enabled deployment of over 500,000 BEV SUVs across urban transport networks, improving urban air quality by reducing emissions by 18%.

Personal mobility leads the Electric SUVs Market, accounting for approximately 65% of total usage, driven by rising consumer demand for eco-friendly transportation and improved vehicle performance. Fleet operations represent around 20% of the market, supported by corporate sustainability initiatives and logistics electrification. Ride-hailing and shared mobility services contribute nearly 15%, benefiting from lower operational costs and regulatory incentives. Fleet applications are growing fastest, with a CAGR of 13.5%, as companies increasingly adopt electric SUVs for last-mile delivery and employee transportation. In 2025, over 38% of global enterprises reported integrating electric SUVs into their fleet operations, while 60% of urban consumers preferred EV-based ride-hailing services.

• In 2024, a global ride-hailing platform deployed electric SUVs across 120 cities, achieving a 22% reduction in fuel costs and a 30% improvement in operational efficiency.

Individual consumers dominate the Electric SUVs Market, accounting for nearly 58% of total demand, driven by increasing environmental awareness and government incentives. Corporate and fleet operators contribute around 30%, leveraging electric SUVs for cost-efficient and sustainable operations. Government and public sector entities represent approximately 12%, focusing on electrifying public transportation systems. Fleet operators are the fastest-growing segment, with a CAGR of 14.2%, supported by corporate ESG commitments and cost-saving benefits. In 2025, more than 42% of enterprises globally reported adopting electric SUVs for logistics and employee mobility, while over 55% of urban consumers showed preference for electric vehicles over traditional ICE vehicles.

• In 2025, a national transportation program electrified over 25% of its government vehicle fleet using electric SUVs, reducing fuel consumption by 20%.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

Asia-Pacific recorded over 6 million electric SUV unit sales in 2025, driven by China, India, and Japan. Europe held approximately 27% share with over 3 million units, supported by strict emission regulations. North America accounted for 18%, with increasing adoption of premium electric SUVs. South America and Middle East & Africa collectively contributed around 7%, reflecting emerging adoption. Charging infrastructure surpassed 7 million global installations, with Asia-Pacific leading deployment. Technological advancements and policy support continue to shape regional growth patterns.

North America holds approximately 18% share of the Electric SUVs Market, driven by strong demand for premium and high-performance electric vehicles. The United States leads regional adoption, with over 1.5 million electric SUVs sold in 2025. Government incentives, including tax credits of up to USD 7,500, have significantly boosted consumer adoption. Advanced technologies such as autonomous driving and connected vehicle systems are widely integrated, with over 60% of new models featuring ADAS capabilities. Tesla remains a key player, expanding production capacity and launching new electric SUV variants. Consumer behavior indicates higher adoption among urban professionals and corporate fleets, with over 45% of enterprises incorporating electric SUVs into mobility solutions.

Europe accounts for around 27% of the Electric SUVs Market, with Germany, the UK, and France leading adoption. Stringent emission regulations and carbon neutrality targets have accelerated EV adoption, with over 50% of new vehicle buyers considering electric options. Government incentives and subsidies cover up to 20% of vehicle costs. Technological advancements such as smart charging and vehicle-to-grid integration are gaining traction. Volkswagen is a key regional player, expanding its electric SUV portfolio. Consumer behavior reflects strong preference for eco-friendly vehicles, with over 55% of urban consumers prioritizing sustainability in purchasing decisions.

Asia-Pacific leads the Electric SUVs Market with approximately 48% share, driven by high production volumes and strong domestic demand. China dominates regional sales, followed by India and Japan. The region produced over 8 million EVs in 2025, with electric SUVs accounting for nearly half. Infrastructure development is robust, with over 60% of global charging stations located in this region. BYD is a key player, expanding manufacturing capacity and introducing advanced electric SUV models. Consumer behavior shows high adoption rates in urban areas, with over 35% of households owning electric vehicles.

South America holds around 4% share of the Electric SUVs Market, with Brazil and Argentina leading adoption. Infrastructure development, including expansion of charging networks, is progressing steadily, with over 15,000 charging stations installed across the region. Government incentives and import duty reductions are supporting EV adoption. Local players are collaborating with global automakers to introduce affordable electric SUVs. Consumer behavior indicates growing interest in sustainable mobility, particularly in urban centers, where EV adoption has increased by 25% over the past two years.

The Middle East & Africa region accounts for approximately 3% of the Electric SUVs Market, with the UAE and South Africa leading adoption. Energy diversification strategies and investments in renewable energy are driving EV adoption. Charging infrastructure is expanding, with over 10,000 stations installed by 2025. Governments are offering incentives such as reduced registration fees and tax benefits. Local players are partnering with global manufacturers to introduce electric SUVs. Consumer behavior reflects growing awareness of sustainability, with increasing adoption among high-income consumers and corporate fleets.

China – 55% Market share: Driven by large-scale production capacity and strong domestic demand

United States – 18% Market share: Supported by high consumer adoption and advanced EV infrastructure

The Electric SUVs Market is moderately consolidated, with the top five companies accounting for approximately 52% of the global market share. The competitive landscape is characterized by strong presence of established automotive manufacturers and emerging EV-focused companies. Over 40 major players are actively competing, focusing on innovation, product differentiation, and strategic partnerships.

Key players are investing heavily in battery technology, autonomous driving systems, and digital connectivity to enhance vehicle performance and user experience. Strategic initiatives such as mergers, joint ventures, and collaborations with technology firms are common, enabling companies to strengthen their market position. For instance, partnerships between automakers and battery manufacturers have increased by over 30% since 2022, ensuring stable supply chains.

Product launches remain a critical competitive strategy, with over 60 new electric SUV models introduced globally between 2024 and 2025. Companies are also expanding manufacturing capacities, with investments exceeding USD 150 billion in EV production facilities. Innovation trends such as solid-state batteries and AI-based vehicle systems are reshaping competition, positioning technologically advanced companies as market leaders.

BYD

Volkswagen

Hyundai Motor Company

Ford Motor Company

General Motors

Nissan Motor Corporation

BMW Group

Mercedes-Benz Group

Kia Corporation

Rivian Automotive

Lucid Motors

SAIC Motor Corporation

Tata Motors

Technological advancements are central to the evolution of the Electric SUVs Market, with innovations spanning battery systems, vehicle connectivity, and autonomous driving capabilities. Lithium-ion batteries remain the dominant technology, but energy density improvements of nearly 30% since 2022 have significantly enhanced vehicle range, now exceeding 500 km in many models. Solid-state batteries are emerging as a transformative technology, offering up to 50% higher energy efficiency and improved safety due to reduced flammability.

Charging technologies are also advancing rapidly, with ultra-fast chargers capable of delivering 80% charge in under 20 minutes. Vehicle-to-grid (V2G) technology is gaining traction, enabling electric SUVs to feed energy back into the grid, improving energy efficiency and grid stability. AI-driven battery management systems optimize energy usage, extending battery life by up to 25%.

Autonomous driving technologies are increasingly integrated, with over 65% of electric SUVs featuring Level 2 or higher automation. Connectivity features such as real-time diagnostics, predictive maintenance, and over-the-air updates are enhancing user experience and operational efficiency. These technologies collectively position electric SUVs as advanced, sustainable, and intelligent mobility solutions for the future.

• In April 2025, Tesla introduced the redesigned Model Y electric SUV featuring improved aerodynamics, a new full-width lightbar, upgraded interior materials, and enhanced efficiency. The update focused on maximizing range and comfort through engineering refinements and lightweight components. Source: www.tesla.com

• In January 2026, Tesla reported producing 1,654,667 vehicles globally in 2025, with Model 3 and Model Y accounting for over 1.6 million units, reinforcing the Model Y’s dominance as a high-volume electric SUV platform within its portfolio.

• In June 2025, Tesla launched its Robotaxi service using Model Y-based electric vehicles equipped with Full Self-Driving (FSD) technology in Austin, enabling autonomous ride-hailing operations and demonstrating real-world deployment of AI-integrated electric SUVs.

• In June 2025, Tesla updated its Model X electric SUV with new front bumper cameras, adaptive headlights, increased third-row space, and enhanced ambient lighting, improving safety, visibility, and passenger comfort in premium electric SUV segments.

The Electric SUVs Market Report provides a comprehensive analysis of the global industry, covering key segments such as vehicle types, applications, end-users, and regional markets. The report evaluates Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and emerging fuel cell technologies, offering insights into their adoption patterns and technological advancements. It also examines application areas including personal mobility, fleet operations, and ride-hailing services, highlighting usage trends and industry-specific requirements.

Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, analyzing regional demand patterns, infrastructure development, and policy frameworks. The study includes over 20 countries, providing detailed insights into production capacity, consumer adoption, and technological innovation.

The report further explores key industry trends such as battery advancements, charging infrastructure expansion, and integration of autonomous driving technologies. It also assesses competitive dynamics, profiling major market participants and their strategic initiatives. Additionally, the report highlights emerging opportunities in smart mobility, vehicle-to-grid systems, and sustainable transportation solutions.

Overall, the scope of the report is designed to support decision-makers by providing actionable insights, data-driven analysis, and a forward-looking perspective on the Electric SUVs Market, enabling informed strategic planning and investment decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,613.5 Million |

| Market Revenue (2033) | USD 8,067.0 Million |

| CAGR (2026–2033) | 10.56% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tesla; BYD; Volkswagen; Hyundai Motor Company; Ford Motor Company; General Motors; Nissan Motor Corporation; BMW Group; Mercedes-Benz Group; Kia Corporation; Rivian Automotive; Lucid Motors; SAIC Motor Corporation; Tata Motors |

| Customization & Pricing | Available on Request (10% Customization Free) |