Reports

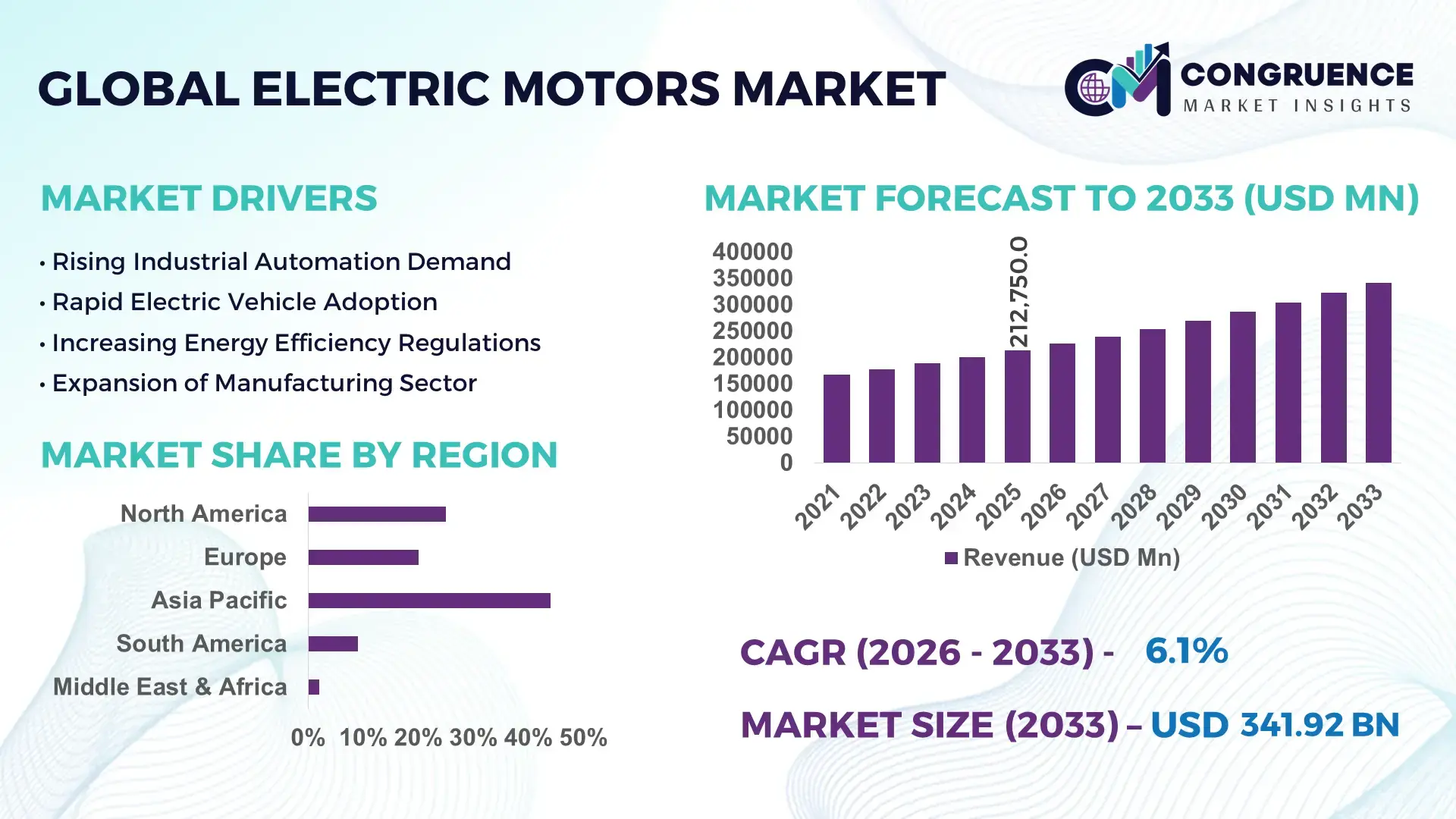

The Global Electric Motors Market was valued at USD 212750 Million in 2025 and is anticipated to reach a value of USD 341916.52 Million by 2033 expanding at a CAGR of 6.11% between 2026 and 2033. This growth is primarily driven by accelerating electrification across industrial automation, electric vehicles, and energy-efficient infrastructure.

China continues to lead the global electric motors market with substantial manufacturing capacity exceeding 3 billion units annually, supported by large-scale investments in industrial automation and EV production. The country has deployed over 13 million electric vehicles, significantly boosting demand for high-efficiency motors. Industrial applications account for nearly 60% of motor consumption in China, particularly in manufacturing, HVAC systems, and robotics. Government-backed energy efficiency standards have pushed adoption of IE3 and IE4 motors, while domestic manufacturers are investing heavily in rare-earth magnet technologies and smart motor systems integrated with IoT-enabled predictive maintenance.

Market Size & Growth: USD 212750 Million in 2025, projected to reach USD 341916.52 Million by 2033 at 6.11% CAGR, driven by rising demand for energy-efficient and electrified systems.

Top Growth Drivers: Industrial automation adoption up by 28%, EV motor demand growth at 35%, energy efficiency improvements at 22%.

Short-Term Forecast: By 2028, smart motor integration is expected to improve operational efficiency by 18% and reduce maintenance costs by 15%.

Emerging Technologies: Integration of IoT-enabled motors, development of brushless DC motors, and adoption of AI-based predictive maintenance systems.

Regional Leaders: Asia-Pacific projected to reach USD 165000 Million by 2033 with strong manufacturing demand; North America at USD 78000 Million driven by automation; Europe at USD 65000 Million with sustainability-focused adoption.

Consumer/End-User Trends: Industrial manufacturing accounts for over 45% usage, followed by automotive and HVAC sectors with increasing adoption of energy-efficient solutions.

Pilot or Case Example: In 2024, a smart factory deployment reduced motor downtime by 30% and improved energy efficiency by 20% through AI-driven monitoring systems.

Competitive Landscape: Market leader holds approximately 14% share, followed by major players including Siemens, ABB, Nidec, WEG, and Toshiba.

Regulatory & ESG Impact: Global efficiency regulations mandate IE3 and above motors, with carbon reduction targets pushing 25% improvement in industrial energy use by 2030.

Investment & Funding Patterns: Over USD 18 Billion invested in electrification and motor innovation projects globally, with increasing focus on sustainable manufacturing.

Innovation & Future Outlook: Advancements in rare-earth-free motors, digital twins, and high-efficiency drive systems are shaping next-generation electric motor applications.

The electric motors market is strongly influenced by industrial manufacturing, which contributes over 40% of total demand, followed by automotive applications at approximately 25% and HVAC systems accounting for nearly 15%. Technological advancements such as brushless DC motors, synchronous reluctance motors, and AI-enabled predictive maintenance systems are reshaping operational efficiency. Environmental regulations mandating energy-efficient motors are accelerating upgrades to IE4 and IE5 standards globally. Asia-Pacific dominates consumption due to rapid industrialization, while Europe emphasizes sustainability-driven adoption. Emerging trends include integration with renewable energy systems, electrification of mobility, and development of compact, high-torque motors, positioning the market for long-term technological transformation.

The electric motors market holds strategic importance as a foundational component of global electrification, industrial automation, and energy transition initiatives. High-efficiency brushless DC motors deliver up to 30% energy savings compared to traditional induction motors, making them a preferred choice across manufacturing and electric mobility sectors. Asia-Pacific dominates in volume due to large-scale production capabilities, while Europe leads in adoption with over 65% of enterprises implementing high-efficiency motor systems aligned with sustainability goals.

The integration of AI-driven predictive maintenance and IoT-enabled monitoring systems is transforming operational performance. By 2028, smart motor technologies are expected to reduce unplanned downtime by 25% and enhance system reliability by over 20%. Firms are committing to ESG targets, including reducing industrial energy consumption by 30% and increasing recyclable motor components by 40% by 2030. These commitments are driving investments in advanced materials, including rare-earth alternatives and high-efficiency magnetic systems.

In 2024, Germany implemented an AI-integrated motor optimization initiative across manufacturing plants, achieving a 22% reduction in energy consumption and a 17% increase in operational efficiency. Such measurable outcomes highlight the role of digitalization in reshaping the market. As electrification accelerates across transportation, infrastructure, and renewable energy systems, the electric motors market is emerging as a critical pillar of resilience, regulatory compliance, and sustainable industrial growth.

Industrial automation is significantly boosting demand for electric motors, particularly in robotics, conveyor systems, and precision manufacturing equipment. Over 70% of modern industrial machinery now relies on electric motors as core components. The global deployment of industrial robots has surpassed 3.5 million units, each requiring multiple high-performance motors. Automation increases productivity by up to 40%, creating a strong incentive for industries to adopt advanced motor systems. Additionally, the shift toward Industry 4.0 is driving demand for smart motors with embedded sensors, enabling real-time performance monitoring and predictive maintenance, thereby enhancing operational efficiency.

The electric motors market faces constraints due to high upfront costs associated with advanced motor technologies, particularly those using rare-earth magnets. Materials such as neodymium and dysprosium are subject to supply volatility, with price fluctuations exceeding 25% annually in some cases. This dependency increases manufacturing costs and limits affordability for small and medium enterprises. Additionally, upgrading existing infrastructure to accommodate high-efficiency motors requires significant capital investment. Maintenance complexities associated with advanced motor systems also pose challenges, especially in regions with limited technical expertise.

The global shift toward electrification and renewable energy presents substantial opportunities for electric motor manufacturers. Wind turbines, solar tracking systems, and electric vehicle drivetrains rely heavily on high-efficiency motors. The number of electric vehicles globally has exceeded 40 million units, each utilizing multiple motor systems. Renewable energy installations are growing at over 10% annually, increasing demand for specialized motors in energy generation and storage systems. Furthermore, government incentives for energy-efficient equipment are encouraging industries to replace legacy motors, creating a strong replacement market.

Technological advancements in electric motors, while beneficial, introduce complexity in design, integration, and maintenance. High-performance motors require precise engineering and compatibility with digital control systems, increasing development time and costs. Regulatory compliance, particularly with energy efficiency standards such as IE4 and IE5, demands continuous innovation and testing. Manufacturers must also adhere to environmental regulations related to material usage and recycling, which can increase operational costs by up to 15%. Additionally, ensuring interoperability across diverse industrial systems remains a challenge, especially in legacy infrastructure environments.

• Rapid Adoption of High-Efficiency IE4 and IE5 Motors:

Industrial sectors are increasingly transitioning toward premium-efficiency motors to comply with stringent energy regulations. Over 65% of newly installed industrial motors in developed regions now meet IE3 or higher standards, while IE4 adoption has grown by more than 28% in the last three years. These advanced motors reduce energy consumption by up to 20% compared to IE2 models, making them critical for cost optimization. In energy-intensive industries, motors account for nearly 70% of electricity usage, reinforcing the urgency of efficiency upgrades.

• Expansion of Electric Vehicle Motor Integration:

The surge in electric vehicle production is significantly boosting demand for traction motors and auxiliary motor systems. Global EV deployment has crossed 40 million units, with each vehicle utilizing 2–5 electric motors depending on configuration. Permanent magnet synchronous motors account for approximately 60% of EV motor usage due to their high torque density and efficiency. Additionally, motor power density improvements of 25% over the past five years are enabling compact and lightweight vehicle designs, accelerating automotive electrification.

• Growth in Smart and IoT-Enabled Motor Systems:

Digital transformation is driving the integration of smart motors equipped with sensors and connectivity features. Around 35% of industrial facilities have adopted IoT-enabled motor systems to enhance predictive maintenance capabilities. These systems reduce unplanned downtime by up to 30% and extend equipment lifespan by 15–20%. Cloud-based monitoring platforms allow real-time performance tracking across multiple facilities, improving operational transparency and efficiency in sectors such as manufacturing and logistics.

• Increasing Use in Renewable Energy and Infrastructure Projects:

Electric motors are playing a vital role in renewable energy systems and infrastructure modernization. Wind turbines and solar tracking systems collectively utilize millions of specialized motors, with renewable installations growing by over 12% annually. In large-scale infrastructure projects, motor-driven systems improve energy efficiency by up to 18%. Demand is particularly strong in Asia-Pacific and Europe, where over 50% of new infrastructure developments incorporate energy-efficient motor technologies to meet sustainability targets.

The electric motors market segmentation reflects a diverse and highly application-driven landscape, structured across types, applications, and end-user industries. By type, the market includes AC motors, DC motors, and emerging brushless motor technologies, each catering to specific operational requirements. AC motors dominate industrial applications due to durability and cost efficiency, while DC and brushless motors are gaining traction in precision-driven and battery-powered systems.

From an application perspective, industrial machinery accounts for the largest share, followed by automotive, HVAC, and consumer appliances. The rapid electrification of mobility and increasing demand for energy-efficient cooling systems are reshaping application dynamics. End-user segmentation highlights manufacturing, automotive, energy, and commercial sectors as key contributors, with manufacturing alone accounting for a substantial portion of global motor utilization. Regional consumption patterns indicate strong demand in Asia-Pacific due to industrial growth, while Europe and North America focus on efficiency upgrades and sustainability-driven deployments.

AC motors hold the dominant position in the electric motors market, accounting for approximately 68% of total adoption due to their robustness, lower maintenance requirements, and suitability for continuous industrial operations. In comparison, DC motors represent around 20% of usage, primarily in applications requiring variable speed and precise control. However, brushless DC motors are emerging as the fastest-growing segment, with an estimated growth rate of 8.5% annually, driven by increasing demand in electric vehicles, robotics, and consumer electronics. These motors offer efficiency improvements of up to 30% compared to traditional brushed motors and have longer operational lifespans. Other motor types, including stepper motors and servo motors, collectively contribute nearly 12% of the market, serving niche applications such as automation, medical devices, and aerospace systems where precision and responsiveness are critical. The increasing use of synchronous reluctance motors is also notable, particularly in industrial energy-saving applications.

Industrial machinery remains the leading application segment, accounting for approximately 45% of electric motor usage, driven by widespread deployment in manufacturing, material handling, and processing equipment. Automotive applications follow with around 25% share, supported by rising electric vehicle adoption and increasing integration of motor-driven systems in modern vehicles. HVAC systems account for nearly 15% of the market, as energy-efficient heating and cooling solutions gain traction globally. Electric vehicle applications represent the fastest-growing segment, with an estimated annual growth rate exceeding 10%, fueled by government incentives, emission regulations, and advancements in battery technologies. EV motors are becoming more efficient, with torque density improvements of over 20% in recent years, enhancing vehicle performance and range. Other applications, including consumer appliances and renewable energy systems, collectively contribute about 15% of the market, reflecting steady demand across residential and infrastructure sectors.

The manufacturing sector leads the electric motors market, accounting for approximately 40% of total demand due to extensive use in production lines, robotics, and heavy machinery. Automotive end-users represent around 22% of the market, driven by the rapid expansion of electric vehicle production and increasing motor integration in conventional vehicles. The energy sector, including renewable energy and utilities, contributes nearly 18%, reflecting growing reliance on motor-driven systems for power generation and distribution. The electric vehicle industry is the fastest-growing end-user segment, with an estimated growth rate of 11% annually, supported by rising EV adoption and technological advancements in motor efficiency and design. Commercial buildings and HVAC systems collectively account for about 12% of demand, while other sectors such as agriculture and mining contribute the remaining 8%, highlighting the broad applicability of electric motors.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific’s dominance is supported by annual production volumes exceeding 3 billion electric motors, driven by strong industrial manufacturing in China, Japan, and India. North America holds approximately 22% share, with over 65% of industrial facilities integrating energy-efficient motors. Europe contributes nearly 20% of the global market, with over 70% of installations meeting IE3 or higher efficiency standards. South America accounts for around 6%, while the Middle East & Africa collectively represent close to 6% of total demand, driven by infrastructure and energy sector investments. Industrial applications dominate across all regions, accounting for over 60% of motor usage globally, while automotive applications contribute approximately 25%, reflecting increasing electrification trends.

How is advanced industrial automation shaping demand for high-efficiency motor systems?

North America accounts for approximately 22% of the global electric motors market, with strong demand driven by manufacturing, automotive, and HVAC industries. Over 68% of industrial facilities in the region have upgraded to energy-efficient motors, reflecting a strong push toward operational cost reduction and sustainability. Government initiatives promoting energy efficiency standards, including mandatory adoption of IE3-level motors in several applications, are accelerating market growth. Technological advancements such as IoT-enabled motor systems and AI-based predictive maintenance are widely adopted, with nearly 40% of enterprises integrating smart motor technologies. A key regional player, Regal Rexnord, has expanded its portfolio of high-efficiency motors, focusing on digital monitoring capabilities that improve uptime by up to 25%. Consumer behavior reflects higher enterprise adoption in sectors such as healthcare, data centers, and financial services, where reliability and energy optimization are critical performance factors.

What role do sustainability regulations play in accelerating energy-efficient motor adoption?

Europe holds nearly 20% of the electric motors market, with leading countries including Germany, the UK, and France driving demand through industrial automation and sustainability initiatives. Over 72% of installed motors in the region meet IE3 or higher standards, reflecting strict regulatory enforcement by energy efficiency directives. Policies targeting a 32% reduction in energy consumption by 2030 are pushing industries to adopt advanced motor technologies. Emerging technologies such as synchronous reluctance motors and digital twin systems are gaining traction, improving efficiency by up to 20% in industrial applications. Companies like Siemens are investing heavily in smart motor systems integrated with cloud-based analytics platforms. Consumer behavior in the region shows a strong preference for environmentally compliant solutions, with over 60% of enterprises prioritizing low-emission and recyclable motor components in procurement decisions.

How is large-scale manufacturing expansion driving motor demand across industrial sectors?

Asia-Pacific dominates the electric motors market in terms of volume, accounting for over 46% of global consumption. China, India, and Japan are the top consuming countries, collectively contributing more than 70% of regional demand. Rapid industrialization, supported by over 15% annual growth in manufacturing output in key economies, is driving large-scale motor deployment across factories and infrastructure projects. The region is also a hub for technological innovation, with increasing adoption of brushless DC motors and high-efficiency AC motors. Companies such as Nidec are expanding production capacities to meet rising global demand, with output increases exceeding 20% in recent years. Consumer behavior reflects strong growth driven by e-commerce, urbanization, and mobile-based industrial applications, with over 50% of new installations linked to automation and smart manufacturing initiatives.

How are energy sector investments influencing industrial motor adoption trends?

South America accounts for approximately 6% of the global electric motors market, with Brazil and Argentina serving as key contributors. The region’s demand is largely driven by energy, mining, and agricultural sectors, where motor-driven equipment is essential for operations. Over 55% of industrial installations rely on electric motors for energy-intensive processes, particularly in mining and oil extraction. Government incentives supporting renewable energy projects are boosting demand for specialized motors in wind and hydroelectric applications. Local manufacturers such as WEG are expanding production capabilities and focusing on energy-efficient motor solutions tailored to regional needs. Consumer behavior indicates that demand is closely tied to infrastructure development and energy sector expansion, with increasing adoption of cost-efficient motor systems across emerging industrial hubs.

What impact do infrastructure modernization and energy projects have on motor demand?

The Middle East & Africa region represents approximately 6% of the electric motors market, with significant demand driven by oil & gas, construction, and water management sectors. Countries such as the UAE and South Africa are leading growth, with infrastructure investments increasing by over 12% annually. Electric motors are widely used in pumping systems, desalination plants, and industrial processing units. Technological modernization is evident through the adoption of high-efficiency motors and automated control systems, improving operational efficiency by up to 18%. Regional trade partnerships and regulatory frameworks promoting energy efficiency are encouraging the transition to advanced motor technologies. A notable trend is the increasing use of smart motor systems in large-scale projects, enhancing performance monitoring and reducing downtime by nearly 20%. Consumer behavior reflects growing demand for durable, high-performance motors suited for extreme environmental conditions.

China Electric Motors Market – 34% share: Dominance driven by massive production capacity exceeding 3 billion units annually and strong demand from manufacturing and electric vehicle sectors.

United States Electric Motors Market – 16% share: Leadership supported by advanced industrial automation, high adoption of smart motor technologies, and strong demand from HVAC and automotive industries.

The electric motors market is moderately fragmented, with over 150 active global and regional competitors competing across industrial, automotive, and consumer segments. The top five companies collectively account for approximately 38% of the global market, indicating a competitive yet consolidated structure among leading players. Major participants focus on product innovation, strategic partnerships, and geographic expansion to strengthen their market positions.

Technological differentiation plays a critical role, with companies investing heavily in high-efficiency motors, IoT integration, and AI-driven predictive maintenance solutions. Over 60% of leading manufacturers have introduced smart motor portfolios, reflecting the growing importance of digitalization. Strategic mergers and acquisitions have increased by nearly 18% over the past three years, enabling companies to expand capabilities and access new markets.

Product launches in brushless DC motors and synchronous reluctance motors are accelerating, with efficiency improvements of up to 25% compared to conventional designs. Additionally, sustainability initiatives are influencing competition, as companies align product development with global energy efficiency standards and carbon reduction targets. The market is characterized by continuous innovation, strong R&D investments, and increasing collaboration between manufacturers and technology providers.

Siemens

ABB

Nidec Corporation

WEG Industries

Toshiba Corporation

Regal Rexnord Corporation

Johnson Electric Holdings

Rockwell Automation

Mitsubishi Electric Corporation

Franklin Electric

TECO Electric & Machinery

Hyundai Electric

CG Power and Industrial Solutions

Brook Crompton

AMETEK Inc.

Technological advancements in the electric motors market are centered on improving efficiency, reliability, and digital integration across industrial and automotive applications. High-efficiency motor classes such as IE4 and IE5 are becoming industry standards, delivering energy savings of up to 20–25% compared to conventional IE2 motors. These motors are increasingly adopted in energy-intensive sectors where electric motors account for nearly 70% of total electricity consumption. Advanced materials, including high-grade silicon steel and rare-earth magnets, are enhancing torque density by over 30%, enabling compact and high-performance motor designs.

The rapid adoption of brushless DC (BLDC) and permanent magnet synchronous motors (PMSM) is transforming sectors such as electric vehicles and robotics. These motors offer efficiency levels exceeding 90% and reduce maintenance requirements by eliminating mechanical brushes. In electric vehicles, PMSMs are used in approximately 60% of modern drivetrains due to their superior power-to-weight ratio and precision control capabilities.

Digitalization is another key technological driver, with over 35% of industrial motors now integrated with IoT sensors and smart controllers. These systems enable predictive maintenance, reducing downtime by up to 30% and extending motor lifespan by nearly 20%. Digital twin technology is also gaining traction, allowing real-time simulation and performance optimization of motor systems. Furthermore, advancements in power electronics, such as variable frequency drives (VFDs), are improving energy efficiency by 15–25% in industrial operations. Emerging innovations, including rare-earth-free motor designs and advanced cooling systems, are expected to further enhance sustainability and operational efficiency in the coming years.

• In March 2025, ABB announced the expansion of its IE5 ultra-premium efficiency motor portfolio, introducing new synchronous reluctance motors designed to reduce energy losses by up to 40% compared to IE3 motors, supporting industrial decarbonization goals. Source: www.abb.com

• In September 2024, Siemens launched an upgraded range of SIMOTICS SD motors featuring enhanced digital connectivity, enabling real-time monitoring and predictive maintenance, reducing unplanned downtime by approximately 20% in industrial applications. Source: www.siemens.com

• In January 2025, Nidec Corporation unveiled a next-generation traction motor system for electric vehicles, achieving a 30% improvement in power density and reducing system weight by 15%, enhancing overall vehicle efficiency and performance. Source: www.nidec.com

• In July 2024, WEG introduced a new line of W23 Sync+ motors, incorporating synchronous reluctance technology to deliver energy efficiency gains of up to 25% and lower operating temperatures, improving reliability in heavy industrial environments. Source: www.weg.net

The Electric Motors Market Report provides a comprehensive analysis of the global landscape, covering a wide range of segments, technologies, and end-use industries. The report evaluates key motor types, including AC motors, DC motors, and advanced brushless configurations, which collectively account for over 85% of total installations worldwide. It also examines specialized motor categories such as servo and stepper motors, which contribute approximately 10–12% of niche applications in automation and precision engineering.

From an application perspective, the report encompasses industrial machinery, automotive systems, HVAC equipment, consumer appliances, and renewable energy installations. Industrial applications dominate with over 60% share, while automotive applications contribute around 25%, reflecting the rapid growth of electric mobility. The report further analyzes emerging use cases, including electric aircraft systems and smart infrastructure, where motor efficiency improvements of 15–20% are being achieved through advanced designs.

Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing 100% of global market activity. Asia-Pacific alone accounts for nearly half of global consumption, while developed regions focus on energy-efficient upgrades and regulatory compliance.

Technological scope includes advancements in IoT-enabled motors, digital twins, and AI-based predictive maintenance systems, with over one-third of industrial installations now incorporating smart features. The report also addresses regulatory frameworks, energy efficiency standards, and sustainability initiatives influencing product development and adoption. Overall, it delivers a structured, data-driven overview of the electric motors market, enabling stakeholders to make informed strategic decisions across manufacturing, energy, and mobility sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.11% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, ABB, Nidec Corporation, WEG Industries, Toshiba Corporation, Regal Rexnord Corporation, Johnson Electric Holdings, Rockwell Automation, Mitsubishi Electric Corporation, Franklin Electric, TECO Electric & Machinery, Hyundai Electric, CG Power and Industrial Solutions, Brook Crompton, AMETEK Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |