Reports

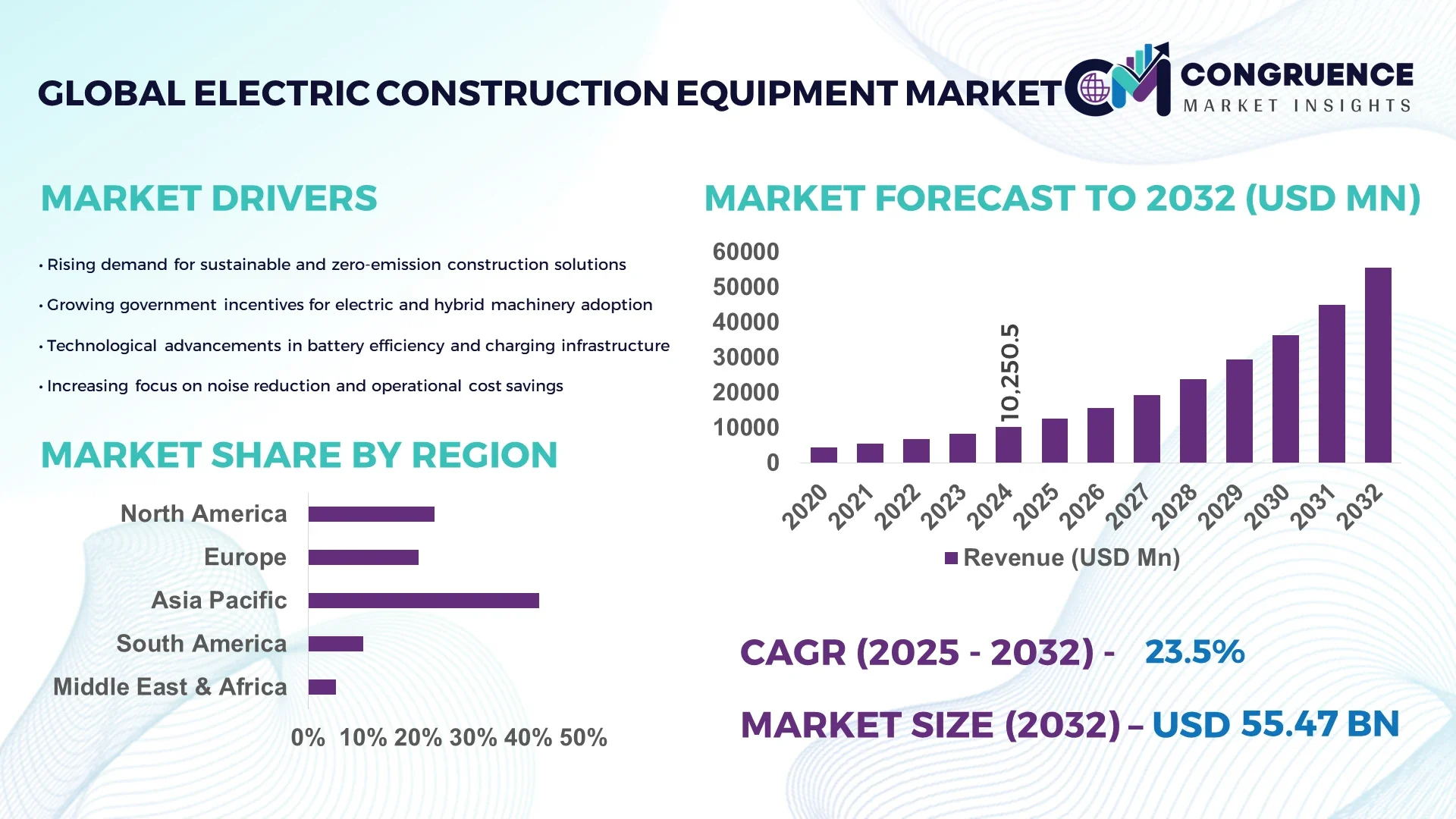

The Global Electric Construction Equipment Market was valued at USD 10,250.5 Million in 2024 and is anticipated to reach a value of USD 68,509 Million by 2032 expanding at a CAGR of 23.5% between 2025 and 2032. The growth is driven by increasing electrification of heavy machinery to meet zero-emission goals and reduce operational costs.

China dominates the global Electric Construction Equipment Market due to its extensive manufacturing infrastructure, large-scale R&D investment, and robust adoption of battery-powered machinery across urban development projects. In 2024, over 48% of all electric excavators and loaders produced globally originated from China, supported by government-backed green construction initiatives. Domestic OEMs have invested more than USD 1.8 billion in developing solid-state battery systems and energy-efficient drivetrains, significantly enhancing production capacity and operational sustainability.

• Market Size & Growth: Valued at USD 10,250.5 Million in 2024 and projected to reach USD 68,509 Million by 2032, expanding at a CAGR of 23.5%, driven by increased demand for zero-emission and low-noise construction machinery.

• Top Growth Drivers: 41% rise in adoption of electric loaders, 33% efficiency improvement through battery optimization, and 29% cost savings in fuel expenditure.

• Short-Term Forecast: By 2028, electric excavators are expected to achieve a 27% reduction in maintenance costs and a 35% improvement in runtime efficiency.

• Emerging Technologies: Integration of solid-state batteries, AI-driven fleet management systems, and fast-charging modular battery packs are reshaping equipment performance.

• Regional Leaders: Asia-Pacific (USD 32.7 Billion by 2032) leading in industrial electrification, Europe (USD 19.4 Billion) emphasizing emission-free zones, and North America (USD 11.6 Billion) accelerating infrastructure electrification.

• Consumer/End-User Trends: High adoption among urban infrastructure developers, rental equipment firms, and government-backed smart city contractors.

• Pilot or Case Example: In 2024, Komatsu’s electric bulldozer pilot achieved a 32% reduction in energy consumption and improved operational uptime by 18%.

• Competitive Landscape: Volvo Construction Equipment leads with approximately 14% market share, followed by Caterpillar, Hyundai Construction Equipment, JCB, and XCMG.

• Regulatory & ESG Impact: EU emission directives and China’s carbon neutrality targets are accelerating electric fleet adoption across key regions.

• Investment & Funding Patterns: Over USD 3.2 Billion invested globally in 2024 for battery system upgrades and electrified machinery R&D projects.

• Innovation & Future Outlook: The future landscape will be shaped by autonomous operation integration, hybrid charging networks, and large-scale fleet electrification partnerships.

The Electric Construction Equipment Market is experiencing rapid innovation across material handling, excavation, and road construction sectors. Technological advances such as high-density lithium-ion batteries, telematics-based performance monitoring, and modular charging infrastructure are transforming operational efficiency. Regulatory measures promoting decarbonization, coupled with fiscal incentives for sustainable construction, are influencing purchasing trends across North America, Europe, and Asia-Pacific. The market is further driven by growing urbanization, green infrastructure investments, and integration of IoT-enabled diagnostics, signaling a long-term transition toward fully electric and autonomous construction equipment fleets.

The Electric Construction Equipment Market holds strategic relevance as it drives the global transition toward zero-emission, high-efficiency construction practices. Electrification of excavators, loaders, and cranes is transforming fleet economics and operational sustainability. Lithium-ion and solid-state battery integration delivers a 42% improvement in energy efficiency compared to traditional diesel-powered systems, while reducing noise and emissions by up to 65%. Asia-Pacific dominates in production volume, while Europe leads in adoption with nearly 46% of enterprises integrating electric equipment in new construction projects. By 2027, AI-based predictive maintenance systems are expected to cut equipment downtime by 28%, optimizing fleet performance and lifecycle costs.

Firms are committing to ESG improvements such as 30% lifecycle emission reduction and 40% recycling of critical battery materials by 2030. In 2024, Volvo CE achieved a 35% reduction in operational emissions through AI-optimized energy usage in its fully electric wheel loader project in Sweden. The shift toward electrified fleets also aligns with global regulatory frameworks such as the EU Green Deal and U.S. Infrastructure Investment and Jobs Act, encouraging OEMs to invest in sustainable technology. Looking forward, the Electric Construction Equipment Market will emerge as a cornerstone of resilient, compliant, and sustainable industrial growth—anchoring the global construction sector’s decarbonization strategy.

Government-backed electrification policies are significantly propelling the Electric Construction Equipment Market by incentivizing the shift toward low-emission machinery. For instance, over 55 countries have introduced emission-based taxation or fleet transition subsidies supporting electric machinery adoption. In 2024, China’s green construction initiative funded more than 6,000 electric excavator deployments, improving site efficiency by 31%. Similarly, the EU’s clean technology framework mandates zero-emission machinery use in public infrastructure projects by 2030, stimulating OEM innovation. National-level investments in charging stations and energy storage have further strengthened fleet feasibility. These collective measures are establishing a robust regulatory foundation for market expansion.

Despite technological progress, the Electric Construction Equipment Market faces financial constraints due to high battery and infrastructure costs. The price of lithium-ion battery packs remains above USD 130 per kWh, impacting affordability for small and mid-size contractors. Additionally, the limited availability of fast-charging stations on remote sites hampers continuous operations. Supply chain disruptions for critical raw materials such as nickel and cobalt have added to production delays and pricing pressures. Equipment lifespan uncertainty and high upfront costs deter mass-scale procurement. Until cost parity with diesel counterparts is achieved, the adoption curve will remain uneven across developing economies.

Smart automation presents one of the most lucrative opportunities in the Electric Construction Equipment Market. Integration of telematics, autonomous navigation, and AI-based control systems can enhance productivity by 40% while reducing operator-related downtime by 25%. OEMs are rapidly embedding digital intelligence into machinery to enable predictive maintenance and performance tracking. In 2024, Japan launched a national smart construction initiative deploying over 2,000 semi-autonomous electric excavators, resulting in 18% faster project completion times. The synergy between electrification and automation not only enhances efficiency but also supports sustainability targets, creating scalable potential for long-term market growth.

The Electric Construction Equipment Market faces operational challenges due to limited grid capacity and inconsistent energy reliability in major construction zones. In several developing regions, grid outages or insufficient voltage supply can delay charging cycles, reducing equipment utilization rates by up to 22%. Mobile charging solutions remain costly and logistically complex for large construction sites. Furthermore, integrating renewable energy into on-site charging infrastructure requires high capital expenditure and technical expertise. These constraints limit the scalability of electric machinery in remote and off-grid environments, emphasizing the need for hybrid power solutions and improved grid modernization to support market expansion.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Electric Construction Equipment Market. Approximately 55% of new projects recorded measurable cost benefits through modular and prefabricated construction approaches. Automated electric machines are increasingly used for pre-bent and cut components fabricated off-site, reducing on-site labor by nearly 28%. Europe and North America have seen a 37% increase in procurement of precision electric machinery to support these high-efficiency modular processes.

• Integration of Smart Telematics and IoT Systems: Smart telematics integration is enabling real-time monitoring and predictive maintenance of electric machinery. Around 63% of fleet operators in developed markets have incorporated IoT-based systems into their electric construction fleets, improving operational uptime by 32%. These technologies provide performance diagnostics and energy analytics that reduce unplanned downtime by nearly 26%, optimizing project workflow and asset utilization.

• Expansion of Fast-Charging and Battery-Swapping Infrastructure: The Electric Construction Equipment Market is witnessing rapid deployment of fast-charging systems and battery-swapping stations. As of 2024, more than 8,000 construction sites globally have adopted high-capacity charging solutions, enabling 70% quicker energy replenishment compared to conventional plug-in methods. This has improved overall machine productivity by 22% and supported continuous operation schedules in urban and large-scale infrastructure projects.

• Adoption of Autonomous and Semi-Autonomous Machinery: The market is experiencing growing automation adoption, with 47% of OEMs introducing autonomous or semi-autonomous features in electric excavators and loaders. These systems enhance job site safety and reduce human error-related losses by 35%. In 2024, over 3,500 semi-autonomous electric construction units were deployed across Asia-Pacific and Europe, resulting in 19% faster task completion and higher energy efficiency across operations.

The Electric Construction Equipment Market is segmented by type, application, and end-user, each playing a vital role in defining market direction and investment focus. By type, the market includes electric excavators, loaders, cranes, and dump trucks, with electric excavators emerging as the leading category due to rising adoption in urban and infrastructure projects. Applications span construction, mining, material handling, and road maintenance, where the construction sector dominates owing to accelerating electrification mandates. In terms of end-users, large construction contractors lead the market, followed by rental equipment firms and government infrastructure departments. These segments collectively reflect the global push toward sustainable, low-emission operations and technological modernization across the heavy machinery industry.

Electric excavators currently account for 39% of the Electric Construction Equipment Market, driven by increased deployment across residential and public infrastructure projects. Their growing acceptance is supported by performance improvements, with newer models delivering 25% higher energy efficiency and 30% lower maintenance requirements compared to diesel units. Electric loaders hold approximately 28% share, gaining popularity for their adaptability in confined construction zones and material handling operations. Meanwhile, electric cranes and dump trucks collectively contribute around 33% of the market, catering to niche applications such as tunneling and large-scale construction.

Among all, electric wheel loaders represent the fastest-growing type, expected to expand at 28.4% annually due to advances in quick-charge battery systems and compact design integration for flexible use in urban environments. Innovations in autonomous operation and telematics are further enhancing the adoption rate.

The construction segment dominates the Electric Construction Equipment Market with 46% of total adoption, reflecting widespread integration in commercial and residential infrastructure development. Growing regulatory focus on zero-emission building sites and government-funded sustainability initiatives are strengthening this leadership. The mining sector follows with 31% market share, leveraging electric machinery for deep pit operations and reducing ventilation energy costs by nearly 22%. Material handling and road maintenance together hold a combined 23% share, supporting logistics hubs and public infrastructure programs.

Mining applications are projected to grow fastest at 25.6% annually, driven by demand for electric haulers and loaders in underground environments to minimize exhaust and heat levels.

Large construction contractors lead the Electric Construction Equipment Market with a 43% share, attributed to extensive infrastructure portfolios and capital capacity to transition fleets toward electrification. These firms report an estimated 29% operational cost reduction through the use of electric excavators and cranes. Rental equipment companies account for 27% of demand, increasingly investing in electric fleets to meet contractor sustainability requirements. Government agencies and municipal bodies together contribute 30%, largely through public works and urban modernization projects.

Rental service providers are the fastest-growing end-user category, projected to expand at 27.2% annually as cost-effective equipment access drives adoption among small and mid-scale builders. Increasing green infrastructure budgets are further supporting this transition.

Asia-Pacific accounted for the largest market share at 48.3% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 25.7% between 2025 and 2032.

The market’s regional distribution shows strong investment patterns, with North America holding 24.6% and Europe representing 21.8% of total global adoption. South America and the Middle East & Africa collectively contributed 5.3%. Rapid electrification initiatives, urban infrastructure expansion, and emission-reduction mandates have propelled demand across major regions. China and Japan together produced over 60,000 electric construction units in 2024, while Europe recorded a 42% year-on-year rise in electric machinery procurement. North America demonstrated 37% adoption among major construction firms, driven by corporate sustainability commitments and green infrastructure projects.

The North American Electric Construction Equipment Market held a 24.6% share in 2024, primarily driven by the U.S. and Canada’s rapid adoption of zero-emission machinery in infrastructure projects. Key industries fueling demand include transportation, public infrastructure, and commercial real estate. The U.S. government’s Clean Construction Initiative has accelerated the integration of battery-powered excavators and loaders across federal projects. Local manufacturers are focusing on digital transformation, integrating AI-powered telematics to optimize equipment utilization. In 2024, Caterpillar launched an electric compact excavator line designed for urban construction, reducing fuel dependency by 34%. Consumer behavior in this region reflects high enterprise adoption, particularly in sectors emphasizing carbon neutrality and operational efficiency, with 45% of contractors integrating electric fleets into project tenders.

Europe represented 21.8% of the Electric Construction Equipment Market in 2024, led by Germany, the UK, and France. The region’s growth is heavily influenced by strict EU emission standards and sustainability initiatives such as “Fit for 55.” These policies are accelerating fleet electrification among construction firms and municipal bodies. OEMs are investing in advanced lithium-ion systems and autonomous machinery to meet local decarbonization goals. Volvo CE and JCB have been key regional innovators, rolling out fully electric loaders for low-noise urban operations. Consumer behavior emphasizes compliance and transparency, with 52% of enterprises adopting electric machinery specifically to meet regulatory mandates and ESG scoring requirements. This alignment of environmental policy and industrial innovation continues to define the European market trajectory.

Asia-Pacific dominated the Electric Construction Equipment Market with a commanding 48.3% share in 2024, led by China, Japan, and India. This region benefits from high-volume manufacturing capabilities and government-backed electrification programs. China alone accounted for over 38,000 unit deployments in 2024, supported by large infrastructure and smart city investments. India’s “Green Infrastructure Mission” and Japan’s focus on automation in construction have fueled further adoption. Regional technology hubs such as Shenzhen and Osaka are pioneering innovations in battery-swapping and rapid charging systems. Local firms, including XCMG and Komatsu, have introduced AI-enabled electric excavators, improving project efficiency by 31%. Consumer behavior trends indicate a preference for cost-effective, high-durability machinery, reflecting the region’s industrial and commercial growth priorities.

The South American Electric Construction Equipment Market accounted for 3.1% of global share in 2024, led by Brazil and Argentina. Infrastructure revitalization programs and renewable energy projects are boosting regional demand for electric machinery. Governments have introduced tax incentives to support fleet modernization and reduce diesel dependence in urban construction. In 2024, Brazil’s Ministry of Infrastructure allocated funding for electric roadwork equipment across 12 major cities. Local companies are investing in charging hubs to facilitate equipment operation in dense city zones. Consumer trends highlight strong adoption among mid-sized contractors, with 29% of enterprises in metropolitan regions shifting toward electric loaders for cost efficiency and emission compliance.

The Middle East & Africa Electric Construction Equipment Market held 2.2% share in 2024, with the UAE, Saudi Arabia, and South Africa as the primary growth engines. Regional diversification efforts, such as Vision 2030, are pushing investments in clean and automated construction technologies. Governments are offering tax benefits and trade partnerships to promote electric machinery adoption in large-scale projects, including NEOM and Expo City Dubai. Technological modernization includes the introduction of hybrid-electric machinery suited for high-temperature environments. In 2024, South Africa’s construction sector deployed 600 electric loaders in mining and public works, achieving a 27% energy cost reduction. Regional consumers are increasingly favoring sustainability-aligned equipment, with 33% of contractors emphasizing carbon compliance in procurement decisions.

• China (38.7%) – China leads the Electric Construction Equipment Market due to massive production capacity, rapid electrification of infrastructure projects, and strong government-backed manufacturing initiatives.

• United States (18.5%) – The United States ranks second owing to robust technological integration, large infrastructure investment programs, and increasing sustainability commitments across private and public sectors.

The Electric Construction Equipment Market is moderately consolidated, with the top five players collectively accounting for nearly 56% of the total market share in 2024. Approximately 45–50 active manufacturers compete globally, emphasizing energy efficiency, automation, and sustainable engineering solutions. The competitive dynamics are shaped by advancements in battery technology, intelligent telematics, and machine electrification. Key market participants are strengthening their portfolios through strategic partnerships, acquisitions, and localized manufacturing units. Between 2023 and 2024, over 25 new product launches were recorded, targeting high-demand categories such as electric excavators, wheel loaders, and mini diggers. The market also witnessed an increase of 31% in R&D investment from leading companies focusing on battery durability and low-emission operations.

Collaborations between OEMs and battery manufacturers have surged by 40%, indicating a strong shift toward vertical integration and innovation-driven growth. Additionally, digital twin technology and autonomous operation software are being integrated into equipment models to enhance operational precision and fleet monitoring efficiency. Asia-Pacific remains the fastest-evolving competitive hub, while North America and Europe dominate in technology-driven premium equipment categories. The market’s competitive environment is expected to intensify further as new entrants from China, South Korea, and the U.S. introduce cost-efficient and AI-integrated product lines.

Hitachi Construction Machinery Co., Ltd.

JCB Ltd.

Hyundai Construction Equipment Co., Ltd.

Doosan Infracore Co., Ltd.

Liebherr Group

Wacker Neuson SE

SANY Heavy Industry Co., Ltd.

Kubota Corporation

Takeuchi Manufacturing Co., Ltd.

CNH Industrial N.V.

Bobcat Company

XCMG Group

Technological innovation is transforming the Electric Construction Equipment Market, driven by advancements in battery systems, automation, and connectivity. The integration of high-energy-density lithium-ion and solid-state batteries has improved equipment runtime by nearly 42% while reducing charging time by 35%. Manufacturers are increasingly focusing on battery modularity and thermal management systems to enhance efficiency and ensure safe operation in demanding construction environments. Additionally, the transition toward 800V fast-charging architectures enables heavy-duty equipment to reach 80% charge capacity within 45 minutes, significantly boosting uptime and productivity.

Automation and autonomous technology are becoming mainstream, with over 48% of newly developed electric excavators and loaders featuring semi-autonomous or fully automated capabilities. These systems use AI-driven perception sensors and GPS-based navigation to reduce operator fatigue and improve precision during repetitive or hazardous operations. Advanced telematics solutions are enabling real-time monitoring of energy consumption, location tracking, and predictive maintenance—helping operators cut downtime by up to 27% and optimize fleet utilization.

Furthermore, integration of digital twin technology and IoT-enabled data analytics is redefining project planning and equipment lifecycle management. Around 60% of OEMs are adopting cloud-based fleet management platforms to gather and analyze performance data, providing insights for energy optimization and predictive diagnostics. Emerging trends such as hydrogen fuel cell-powered machinery, wireless charging infrastructure, and AI-based site management software are also under development, signaling a shift toward intelligent, zero-emission construction ecosystems. This ongoing technological evolution is positioning electric construction machinery as a cornerstone of future-ready infrastructure projects worldwide.

• In 2023, Komatsu Ltd. unveiled its PC200LCE and 210LCE-11 20-ton class electric excavators, marking the company’s first full-scale entry into the medium-sized electric construction equipment segment for that fiscal year.

• In 2024, Volvo Construction Equipment announced the launch of the EC230 Electric excavator in Japan—the company’s largest electric excavator to date in that country’s market, signaling a move from compact models to full-sized electric machinery.

• Also in 2024, Volvo CE revealed an ambitious product line-up at its “Volvo Days 2024” event, including a new electric wheeled excavator (EWR150 Electric) and electric wheel loaders (L90 Electric and L120 Electric), expanding beyond crawler models.

• During 2023, Komatsu publicly emphasised its sustainability strategy by showcasing electric machines and associated battery technologies designed to help construction customers reduce carbon footprint and fuel burn at the CONEXPO/CON-AGG trade show.

The report on the Electric Construction Equipment Market covers a broad spectrum of segments, geographical regions, applications and technologies. It analyses product types such as electric excavators, wheel loaders, dump trucks, cranes, telehandlers and compact machines, detailing how each type fits into different job-site environments and capacity ranges. The document also addresses key applications including construction, mining, material handling, road and infrastructure maintenance, and rental/leasing operations, offering insight into usage patterns and end-user requirements across sectors.

Geographically, the report includes detailed regional breakdowns covering Asia-Pacific, North America, Europe, South America, and Middle East & Africa, along with country-level analysis for markets such as China, India, Japan, the U.S., Germany and Brazil. Technology focus areas include battery systems (li-ion, solid-state), fast-charging infrastructure, autonomous and semi-autonomous machine control, telematics & fleet management, and modular/plug-in equipment configurations. Emerging niches such as hydrogen-fuel-cell powered machinery, wireless induction charging on high-density jobsites, and hybrid-electric options are examined for future readiness.

Industry focus extends to OEM strategies, rental fleet integration, public infrastructure electrification, regulatory impact (emission/zero-emission mandates), ESG considerations, and financing models for electric equipment adoption. The report offers decision-makers actionable intelligence on supply-chain dynamics, manufacturing localisation, investment trends, performance benchmarking and future readiness of the industry across sectors and regions.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 10250.5 Million |

Market Revenue in 2032 | USD 68509 Million |

CAGR (2025 - 2032) | 23.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Volvo Construction Equipment, Caterpillar Inc., Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., JCB Ltd., Hyundai Construction Equipment Co., Ltd., Doosan Infracore Co., Ltd., Liebherr Group, Wacker Neuson SE, SANY Heavy Industry Co., Ltd., Kubota Corporation, Takeuchi Manufacturing Co., Ltd., CNH Industrial N.V., Bobcat Company, XCMG Group |

Customization & Pricing | Available on Request (10% Customization is Free) |