Reports

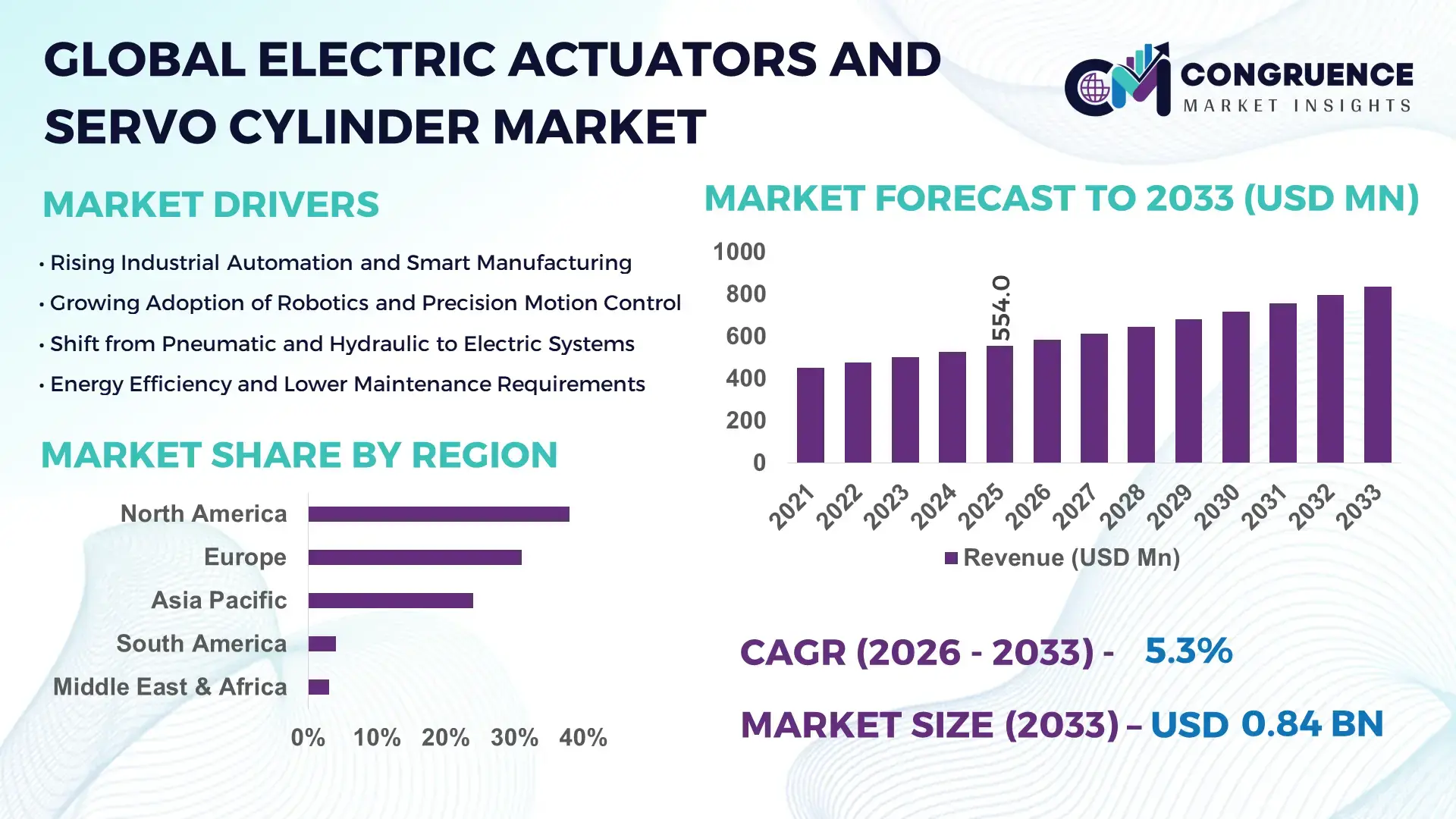

The Global Electric Actuators and Servo Cylinder Market was valued at USD 554.0 Million in 2025 and is anticipated to reach a value of USD 837.4 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by accelerated industrial automation adoption and the shift toward energy-efficient, precision-controlled motion systems across manufacturing and process industries.

The United States dominates the Electric Actuators and Servo Cylinder Market through its strong production base, high automation intensity, and sustained capital investment in advanced manufacturing. The U.S. hosts over 40% of North America’s industrial automation facilities, with electric actuators widely deployed across automotive assembly lines, aerospace systems, food processing, and semiconductor fabrication. Annual industrial automation investment in the U.S. exceeded USD 15 billion, with motion control systems accounting for a significant share. Servo cylinders are increasingly integrated into robotics, CNC machining centers, and warehouse automation, supporting payload precision below ±0.01 mm. Additionally, more than 65% of U.S. manufacturing plants have adopted smart actuator systems with embedded sensors, enabling predictive maintenance and real-time performance optimization.

Market Size & Growth: USD 554.0 Million in 2025, projected to reach USD 837.4 Million by 2033 at a CAGR of 5.3%, driven by automation upgrades and electrification of motion systems.

Top Growth Drivers: Industrial automation adoption 48%, energy efficiency improvement 32%, precision control demand 27%.

Short-Term Forecast: By 2028, lifecycle maintenance costs are expected to decline by 18% due to smart actuator integration.

Emerging Technologies: AI-enabled motion control, digital twin-based actuator modeling, and high-torque compact servo designs.

Regional Leaders: North America USD 285.0 Million by 2033 with robotics adoption focus; Europe USD 248.6 Million driven by Industry 4.0 retrofits; Asia Pacific USD 223.8 Million led by factory automation expansion.

Consumer/End-User Trends: Automotive, electronics, and logistics sectors account for over 62% of total actuator deployments.

Pilot or Case Example: In 2024, a U.S. automotive plant reduced assembly downtime by 21% using servo-driven actuators.

Competitive Landscape: Siemens leads with ~18% share, followed by Rockwell Automation, Bosch Rexroth, SMC, and Parker Hannifin.

Regulatory & ESG Impact: Energy efficiency standards are accelerating replacement of pneumatic systems with electric alternatives.

Investment & Funding Patterns: Over USD 3.2 Billion invested globally in electric motion control modernization since 2022.

Innovation & Future Outlook: Integration with IIoT platforms and autonomous production cells will define next-generation deployments.

Electric Actuators and Servo Cylinder systems are widely used across automotive manufacturing (29%), electronics and semiconductors (21%), food and beverage processing (12%), logistics and warehousing (10%), and aerospace and defense (8%). Recent innovations include integrated servo drives, regenerative braking mechanisms, and compact high-load designs supporting higher duty cycles. Regulatory emphasis on energy efficiency and emissions reduction is reshaping procurement decisions, while Asia Pacific shows the fastest consumption growth due to large-scale factory automation investments and smart industrial infrastructure expansion.

The Electric Actuators and Servo Cylinder Market holds strategic relevance as industries prioritize precision, efficiency, and digital controllability in motion systems. Electric actuation is increasingly replacing hydraulic and pneumatic solutions due to lower energy consumption, cleaner operation, and superior positional accuracy. Servo-based electric actuators deliver up to 35% efficiency improvement compared to traditional pneumatic cylinders, while reducing unplanned downtime through sensor-enabled diagnostics.

From a competitive standpoint, Asia Pacific dominates in production volume, while Europe leads in adoption with over 58% of large manufacturing enterprises deploying electric servo motion systems across core operations. By 2027, AI-driven motion control algorithms are expected to improve actuator performance optimization by 22%, particularly in adaptive manufacturing environments. ESG compliance is also shaping market strategies, with firms committing to 30% reductions in compressed-air energy usage and improved recyclability of actuator components by 2030.

In 2024, Germany-based manufacturing clusters achieved a 19% throughput improvement by integrating digital twin-enabled servo cylinders into automotive body-in-white lines. Looking ahead, the Electric Actuators and Servo Cylinder Market is positioned as a foundational pillar for resilient manufacturing, regulatory compliance, and sustainable industrial growth, enabling intelligent, data-driven motion control across next-generation production ecosystems.

The Electric Actuators and Servo Cylinder Market dynamics are shaped by accelerating industrial automation, rising demand for precision motion control, and the global transition toward electrified manufacturing systems. Electric Actuators and Servo Cylinder solutions are increasingly preferred for their controllability, energy efficiency, and compatibility with digital manufacturing architectures. Demand is influenced by modernization of legacy plants, expansion of robotics and material handling systems, and stricter workplace safety and energy regulations. Supply-side dynamics are driven by innovation in compact actuator design, integration of sensors and drives, and advancements in control software. Meanwhile, cost optimization, standardization challenges, and skilled workforce availability continue to influence adoption rates across regions.

Industrial automation is a primary driver of the Electric Actuators and Servo Cylinder Market, as manufacturers seek higher throughput, repeatability, and operational transparency. Over 70% of newly installed industrial robots rely on electric actuators for axis control and end-effector positioning. Servo cylinders enable precise force and speed regulation, supporting micro-assembly, high-speed packaging, and CNC machining. Automated production lines using electric actuators have demonstrated productivity improvements of 20–25%, while also reducing manual intervention and safety incidents. The expansion of smart factories and lights-out manufacturing models further strengthens demand for digitally controlled actuation systems.

Despite operational benefits, high initial costs remain a restraint in the Electric Actuators and Servo Cylinder Market. Electric servo systems require advanced drives, controllers, and software integration, increasing capital expenditure compared to conventional pneumatic solutions. For small and mid-scale manufacturers, upfront system costs can be 30–40% higher, delaying replacement cycles. Additionally, retrofitting legacy equipment often involves customization, downtime, and skilled engineering resources, which can discourage rapid adoption, particularly in cost-sensitive emerging markets.

Smart manufacturing presents significant opportunities for the Electric Actuators and Servo Cylinder Market through the convergence of IIoT, AI, and predictive analytics. Actuators equipped with sensors enable real-time condition monitoring, reducing maintenance interventions by up to 25%. Integration with manufacturing execution systems supports adaptive motion control, improving yield consistency in electronics and pharmaceutical production. Emerging applications in collaborative robotics, automated warehouses, and battery manufacturing are expanding addressable demand, particularly for compact, high-precision servo cylinders.

A key challenge in the Electric Actuators and Servo Cylinder Market is the complexity of system configuration and the shortage of skilled automation professionals. Programming servo motion profiles, tuning control loops, and integrating multiple communication protocols require specialized expertise. Lack of standardization across actuator interfaces and control platforms further complicates multi-vendor deployments. These challenges can extend commissioning timelines by 15–20%, impacting project ROI and slowing adoption in regions with limited automation talent pools.

Expansion of Smart Actuators with Embedded Intelligence: Over 60% of newly launched electric actuators now feature integrated sensors and onboard diagnostics, enabling real-time health monitoring and reducing unplanned downtime by 23%. Manufacturers are embedding torque, temperature, and vibration sensing directly into servo cylinders, improving asset utilization across automotive and electronics plants.

Shift Toward Compact High-Load Designs: Compact electric actuators capable of delivering loads above 20 kN have increased adoption by 31% since 2022. These designs support space-constrained robotic cells and modular production lines, particularly in semiconductor and battery manufacturing facilities.

Integration with Digital Twins and Simulation Platforms: Approximately 45% of large manufacturers now simulate actuator performance using digital twins before deployment. This approach has reduced commissioning errors by 28% and accelerated line ramp-up timelines, especially in Europe and East Asia.

Electrification of Material Handling and Logistics Systems: Electric servo cylinders are replacing hydraulic systems in automated warehouses, contributing to energy consumption reductions of 26% and noise level reductions exceeding 40%, supporting safer and more sustainable logistics operations.

The Electric Actuators and Servo Cylinder Market is segmented by type, application, and end-user, reflecting varied performance requirements, automation intensity, and operational environments across industries. By type, the market spans linear electric actuators, rotary electric actuators, and electric servo cylinders, each addressing distinct force, speed, and precision needs. Application-wise, deployment ranges from industrial automation and robotics to material handling, automotive manufacturing, packaging, food processing, and energy systems. End-user adoption is shaped by sector-specific priorities such as accuracy, cleanliness, duty cycle, and digital integration readiness. Manufacturing-led industries continue to favor servo-driven solutions for repeatability and control, while logistics and warehousing increasingly adopt electric actuation for energy efficiency and low maintenance. This segmentation highlights how demand is driven not by a single use case, but by a convergence of precision engineering, electrification, and smart factory transformation across multiple verticals.

Linear electric actuators represent the leading product type, accounting for approximately 44% of total adoption, due to their widespread use in automated assembly lines, packaging equipment, and adjustable industrial machinery. Their dominance is supported by high load-handling capability, repeatable positioning, and ease of integration into PLC-controlled environments. Electric servo cylinders follow closely with about 36% share, favored in high-precision applications requiring synchronized motion, force feedback, and dynamic speed control. Rotary electric actuators account for the remaining share and are primarily used in valve control, indexing tables, and rotational positioning tasks.

While linear actuators lead in adoption, electric servo cylinders are the fastest-growing type, expanding at an estimated 7.1% CAGR, driven by rising deployment in robotics, CNC machining, and battery manufacturing lines where sub-millimeter accuracy is critical. Rotary actuators and niche variants together contribute a combined 20% share, serving specialized motion requirements in process industries and utilities.

In 2025, a national manufacturing modernization program deployed servo cylinders in automated machining centers, achieving positioning accuracy improvements below ±0.01 mm across more than 8,000 industrial units.

Industrial automation is the leading application segment, representing nearly 39% of total adoption, as electric actuators and servo cylinders are integral to robotic arms, assembly systems, and automated inspection lines. Automotive manufacturing follows with around 26% share, where electric actuation supports welding, painting, and body-in-white operations. Material handling and logistics account for approximately 18%, driven by automated storage and retrieval systems and conveyor controls.

Logistics automation is the fastest-growing application, with adoption expanding at an estimated 7.4% CAGR, supported by rapid growth in e-commerce fulfillment centers and demand for energy-efficient, low-noise systems. Other applications—including food and beverage processing, pharmaceuticals, and energy infrastructure—collectively contribute about 17%, emphasizing hygiene, precision dosing, and remote operability.

In 2025, over 41% of global manufacturing enterprises reported piloting electric actuation systems as part of smart factory upgrades. Additionally, nearly 34% of automated warehouses globally transitioned from hydraulic to electric actuation to reduce maintenance intervals and energy consumption.

In 2024, a large-scale automated logistics hub implemented electric servo cylinders across conveyor diverter systems, reducing mechanical downtime by 22% and improving order throughput consistency.

Manufacturing enterprises form the largest end-user segment, accounting for approximately 46% of total market adoption, reflecting high demand from automotive, electronics, and machinery producers. These users prioritize precision, reliability, and digital controllability to support continuous production and quality assurance. Logistics and warehousing operators represent about 24% share, leveraging electric actuators for scalable automation and lower total cost of ownership. Process industries, including food, pharmaceuticals, and chemicals, contribute nearly 18%, valuing clean operation and precise force control.

Logistics operators are the fastest-growing end-user group, with adoption expanding at an estimated 7.6% CAGR, fueled by global fulfillment network expansion and same-day delivery models. Remaining end-users—including energy, aerospace, and healthcare equipment manufacturers—collectively hold around 12%, often deploying electric actuators in specialized, high-reliability environments.

In 2025, more than 37% of global logistics companies reported increasing capital allocation toward electric motion systems. Additionally, over 52% of electronics manufacturers indicated a preference for servo-driven actuators in new production lines due to reduced calibration time.

In 2025, a national postal and logistics operator deployed electric actuators across automated sorting facilities, achieving a 19% improvement in parcel handling efficiency and reduced maintenance interventions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

North America’s leadership is supported by early automation adoption, high penetration of servo-driven systems, and strong investments in smart manufacturing. Europe followed with nearly 31% share, driven by sustainability-led retrofitting of industrial systems and Industry 4.0 mandates. Asia-Pacific held around 24% share in 2025, supported by rapid industrialization, electronics manufacturing expansion, and large-scale factory automation programs in China, Japan, and India. South America and Middle East & Africa together accounted for approximately 7%, reflecting emerging adoption tied to infrastructure, energy, and logistics modernization. Across regions, electric actuators are increasingly replacing pneumatic and hydraulic systems, with more than 52% of new industrial installations globally now specifying electric motion solutions for precision, energy efficiency, and digital controllability.

The region accounted for approximately 38% of global demand in 2025, supported by strong uptake across automotive manufacturing, aerospace, electronics, food processing, and logistics automation. Over 65% of large manufacturing plants in this market operate with digitally controlled motion systems integrated into MES and IIoT platforms. Regulatory emphasis on energy efficiency and workplace safety has accelerated the shift from pneumatic to electric actuation. Federal and state-level incentives for smart manufacturing and reshoring initiatives have further supported capital investment. Technologically, adoption of servo cylinders with embedded sensors and predictive diagnostics has exceeded 58% in new production lines. A leading local player has expanded high-load electric actuator production capacity by over 20%, targeting robotics and warehouse automation. Enterprise buyers in this region show higher adoption in automotive, healthcare equipment, and advanced machinery, prioritizing lifecycle cost reduction and precision reliability.

Europe represented nearly 31% of the market in 2025, with Germany, France, the UK, and Italy as key contributors. Strong regulatory frameworks focused on carbon reduction and industrial efficiency are driving replacement of hydraulic systems with electric alternatives. More than 60% of manufacturing firms in Western Europe have integrated servo-driven actuators into at least one core production process. Sustainability initiatives under EU industrial policies are pushing adoption of low-energy, recyclable actuator components. Emerging technologies such as digital twins and closed-loop motion control are now used by over 45% of large manufacturers. Regional players are investing in modular actuator platforms to support flexible production lines. Consumer behavior reflects strong preference for compliant, explainable, and energy-efficient industrial technologies, with procurement increasingly influenced by lifecycle sustainability metrics.

Asia-Pacific ranked second in volume in 2025, accounting for around 24% of global installations, led by China, Japan, South Korea, and India. China alone accounted for over 45% of regional demand, supported by electronics, EV, and heavy machinery manufacturing. Japan remains a technology leader, with more than 70% of industrial robots relying on electric servo actuation. India is emerging rapidly, supported by manufacturing corridor development and automation penetration still below 35%, indicating strong upside. Innovation hubs across East Asia are advancing compact, high-speed servo designs and AI-enabled motion control. Regional enterprises increasingly favor electric actuators for scalability and reduced maintenance, with adoption strongly linked to e-commerce fulfillment, electronics exports, and mobile-device-driven consumption patterns.

South America accounted for approximately 4% of global market share in 2025, with Brazil and Argentina as the primary contributors. Demand is closely tied to mining, oil & gas, food processing, and infrastructure modernization. Brazil represented nearly 55% of regional demand, driven by industrial automation in automotive assembly and renewable energy projects. Government incentives for energy efficiency and industrial modernization are supporting gradual adoption of electric actuation. Local manufacturers are focusing on ruggedized electric actuators for harsh operating environments. Consumer and enterprise adoption remains selective, with purchasing decisions strongly influenced by durability, local service availability, and compatibility with existing systems.

The Middle East & Africa region held close to 3% share in 2025, with the UAE, Saudi Arabia, and South Africa leading adoption. Demand is driven by oil & gas automation, water treatment, construction, and logistics infrastructure. Over 40% of new industrial projects in the Gulf Cooperation Council now specify electric actuators to improve reliability and reduce maintenance. Smart city initiatives and industrial diversification strategies are accelerating modernization. Local system integrators are expanding partnerships with global actuator suppliers to support digital transformation. Consumer behavior reflects growing preference for automated, remotely monitored systems, particularly in energy and utilities applications.

United States – 26% Market Share: Dominance supported by high automation density, advanced manufacturing capacity, and strong industrial digitalization initiatives.

Germany – 14% Market Share: Leadership driven by precision engineering expertise, strong automotive and machinery sectors, and regulatory-driven adoption of energy-efficient motion systems.

The competitive environment in the Electric Actuators and Servo Cylinder Market is dynamic and moderately consolidated, with more than 120 active competitors globally ranging from multinational conglomerates to specialized motion control firms. Top-tier players dominate a significant portion of total activity, with the combined share of the top 5 companies exceeding ~55%–60% of installed solutions worldwide, while the remainder of the market is served by mid‑tier and emerging technology specialists, reflecting a competitive yet diversifying landscape. Leading firms routinely pursue strategic initiatives such as partnerships, product launches, and acquisitions to strengthen portfolios and enhance technological capability. For example, Siemens AG announced a strategic partnership with sensor specialist Sick AG in 2025 to co‑develop smarter motion control solutions, and Parker Hannifin completed the acquisition of Motion Control Solutions in early 2025 to broaden its electric actuation offerings. Product innovation trends include integration of IoT connectivity, embedded predictive diagnostics, closed‑loop servo control, and digital twins for real‑time monitoring and configuration. These trends are influencing competition by shifting emphasis toward smart, energy‑efficient actuators and servo cylinders that support predictive maintenance and Industry 4.0 interoperability. A number of mid‑tier firms are pursuing niche specialization in compact, high‑precision designs for robotics, semiconductor fabrication, and logistics automation, contributing to rich competitive dynamics where scale, innovation velocity, and integration partnerships are key differentiators.

SMC Corporation

Honeywell International Inc.

Festo AG

Emerson Electric Co.

Schneider Electric

Rockwell Automation

Yaskawa Electric Corporation

THK Co., Ltd.

CurtissWright Corporation

Kollmorgen Corporation

Moog Inc.

The Electric Actuators and Servo Cylinder Market is undergoing significant technological evolution, driven by the imperative for precision motion control, energy efficiency, real‑time operational visibility, and seamless integration into digital manufacturing ecosystems. Current technologies include servo‑driven electric actuators with closed‑loop control, enabling highly controllable positioning and force regulation, and integrated sensors for torque, temperature, and vibration feedback that support predictive maintenance and reduce unplanned downtime. Digital transformation trends such as AI‑enhanced motion control algorithms, cloud‑connected diagnostics, and digital twin technology are enabling remote performance simulation and fine‑tuning of actuator parameters before physical deployment. The integration of smart control modules, IO‑Link connectivity, and standardized communication protocols improves interoperability with PLCs and MES systems, enhancing responsiveness and allowing real‑time adjustments across multi‑axis installations.

Emerging technologies include AI‑assisted predictive analytics, advanced wearable interfaces for mobile commissioning, and plug‑and‑play modular actuator kits that significantly reduce integration complexity and time to deployment. For servo cylinders, closed‑loop feedback with high‑resolution encoders and real‑time data streaming are enabling sub‑millimeter accuracy in automotive assembly lines, semiconductor manufacturing, and automated warehousing. Electromechanical designs that minimize friction and heat generation are being adopted to improve lifecycle durability and lower maintenance intervals. Additionally, edge computing capabilities embedded in actuation modules are facilitating on‑device decision logic, reducing latency and enhancing responsiveness in high‑speed automation applications. This technological progression supports manufacturers in achieving higher throughput, enhanced uptime, lower energy consumption, and adaptive operational control tailored to evolving industrial demands.

• In March 2025, Bosch Rexroth AG expanded its electromechanical cylinder portfolio (EMC‑HP) to include new high‑power sizes capable of delivering forces up to 250 kN for heavy‑duty industrial applications, with optional integrated sensor packages for lubrication and temperature monitoring via IO‑Link connectivity. Source: www.boschrexroth.com

• In May 2025, Festo SE featured its latest multi‑axis positioning systems at Automate 2025, showcasing next‑generation electric tooth belt and ball‑screw actuator families with up to 30% lighter compact profiles for precise motion control, underlining advances in performance and integration speed. Source: www.press.festo.com

• In July 2025, Yaskawa Electric introduced the new MOTOMAN‑GP10 robot with a 10 kg payload and 1101 mm reach, incorporating enhanced motion precision technologies closely related to servo actuator performance for improved responsiveness in manufacturing and logistics automation. Source: www.yaskawa-global.com

• In May 2025, Yaskawa Electric began sales of AC Servo Drive Σ‑X Series 400 V input models, bringing advanced electrical drive performance and digital data capabilities to global markets for motion control and automation applications, signaling expanded electrification and data‑driven control in servo solutions. Source: www.yaskawa-global.com

The scope of the Electric Actuators and Servo Cylinder Market Report encompasses a comprehensive analysis of product types, applications, end‑user industries, regional markets, and technological trends shaping the evolution of precision motion control systems. Product segmentation includes linear actuators, rotary actuators, electric servo cylinders, compact electric actuators, and specialized high‑force designs, enabling stakeholders to understand performance characteristics, integration considerations, and suitability for diverse operational environments. Application categories cover industrial automation, robotics, material handling, packaging, automotive, aerospace, electronics manufacturing, energy infrastructure, and process industries, highlighting how varying operational requirements influence selection and deployment of electric motion systems.

The report’s geographic coverage spans key markets in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering insight into regional demand patterns, industrial priorities, regulatory influences, and technology adoption behaviors. It also examines integration technologies such as IoT connectivity, embedded diagnostics, AI‑assisted motion control, digital twin simulation, and real‑time sensor feedback, which are enabling smarter and more resilient systems. The end‑user analysis includes manufacturing enterprises, logistics and warehousing operators, process and discrete industrial sectors, detailing their specific operational drivers and performance expectations.

Additionally, the scope includes an evaluation of competitive dynamics, profiling major global players, strategic initiatives, and innovation trends that define market positioning. Emerging and niche segments such as micro‑actuation for medical devices, servo actuators for renewable energy systems, and predictive analytics‑enabled solutions are highlighted to support long‑term planning. This breadth ensures decision‑makers gain a holistic understanding of current market structures, future readiness factors, and investment priorities critical to navigating the evolving landscape of electric actuation and servo cylinder technologies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 554.0 Million |

| Market Revenue (2033) | USD 837.4 Million |

| CAGR (2026–2033) | 5.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Siemens AG, Parker Hannifin Corporation, Bosch Rexroth AG, SMC Corporation, Honeywell International Inc., Festo AG, Emerson Electric Co., Schneider Electric, Rockwell Automation, Yaskawa Electric Corporation, THK Co., Ltd., CurtissWright Corporation, Kollmorgen Corporation, Moog Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |