Reports

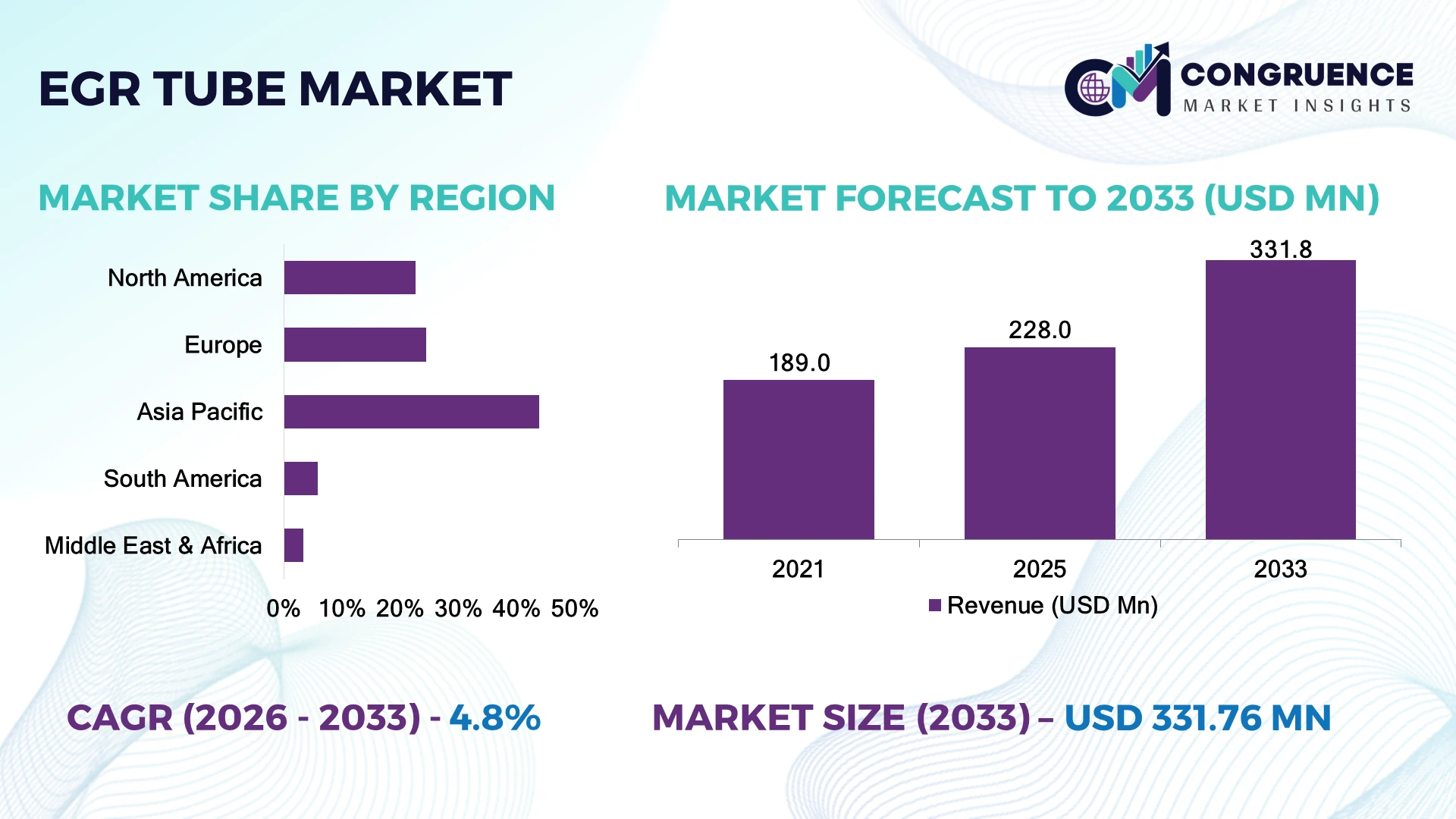

The Global EGR Tube Market was valued at USD 228.0 Million in 2025 and is anticipated to reach a value of USD 331.8 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033. Stringent vehicle emission regulations and the continued production of diesel and gasoline engines in commercial vehicles are accelerating demand for advanced corrosion-resistant EGR tube systems with improved thermal durability.

China accounts for nearly 34% of global EGR tube manufacturing capacity, supported by investments exceeding USD 2.5 billion across automotive component clusters serving passenger and commercial vehicles. Compared with Germany, where high-performance stainless-steel EGR solutions dominate premium vehicle production, China delivers more than 2.3 times higher component output while automated production lines exceed 70% across major manufacturing facilities. The transition toward stricter China VI and Euro 6/7 emission standards continues to strengthen technology adoption and regional competitiveness.

Manufacturers prioritizing localized production, advanced materials, and emission-compliant product innovation are strengthening long-term competitive positioning across global automotive supply chains.

Market Size & Growth: USD 228.0 Million in 2025, projected to reach USD 331.8 Million by 2033 at 4.8% growth, driven by stricter emission compliance and advanced engine technologies.

Top Growth Drivers: Euro 7 readiness, commercial vehicle production rising above 6%, and stainless-steel component adoption exceeding 35%.

Short-Term Forecast: By 2028, automated tube manufacturing is expected to reduce production defects by nearly 18% while improving throughput by 15%.

Emerging Technologies: Robotic tube bending, laser welding, and high-temperature stainless alloys are improving durability and manufacturing precision.

Regional Leaders: Asia-Pacific exceeds USD 110 Million through expanding automotive production, Europe approaches USD 72 Million through emission upgrades, and North America surpasses USD 55 Million with fleet modernization.

Consumer/End-User Trends: More than 62% of heavy-duty engine manufacturers prioritize high-temperature corrosion-resistant EGR tube assemblies.

Pilot/Case Example: In 2024, automated laser welding deployment reduced production cycle time by 20% while improving weld consistency across automotive manufacturing lines.

Competitive Landscape: Top manufacturers collectively control nearly 42% of the market, including Benteler, Tenneco, Continental, Faurecia, and Hutchinson.

Regulatory & ESG Impact: Advanced EGR systems support NOx reduction exceeding 40% under evolving emission regulations across major automotive markets.

Investment & Funding: More than USD 900 Million has been allocated toward automotive emission-control manufacturing expansion through strategic partnerships and production localization.

Innovation & Future Outlook: Lightweight alloys, digital quality inspection, and localized supply-chain expansion are strengthening next-generation emission component competitiveness.

EGR Tube Market demand is expanding across passenger vehicles, commercial trucks, and off-highway equipment requiring reliable exhaust gas recirculation systems. Manufacturers are introducing laser-welded stainless-steel designs and improved thermal coatings that enhance durability and corrosion resistance. More than 45% of newly developed premium systems incorporate advanced material technologies, while regional supply-chain localization and stricter emission compliance continue reshaping procurement and production strategies, setting the stage for broader strategic transformation.

The EGR Tube Market has become strategically important as automotive manufacturers strengthen emission compliance while improving engine efficiency and production resilience. Supply-chain restructuring has encouraged regional sourcing of stainless steel and precision-formed components, reducing procurement risks and shortening manufacturing lead times. Competition increasingly depends on engineering capability, manufacturing automation, and compliance with evolving global emission standards.

Advanced laser-welded EGR tubes deliver approximately 20% higher thermal fatigue resistance than conventionally welded assemblies while reducing manufacturing scrap by nearly 12%. Europe emphasizes premium emission technologies and regulatory compliance, whereas Asia-Pacific leads high-volume production supported by extensive automotive manufacturing infrastructure and automated fabrication systems. Over the next two to three years, automated inspection technologies are expected to exceed 65% adoption among major component manufacturers, improving quality consistency and operational efficiency.

Automotive suppliers are expanding localized production facilities and forming strategic partnerships with vehicle manufacturers to secure long-term supply contracts. A recent deployment of robotic tube-forming equipment significantly improved dimensional accuracy while reducing production downtime across large manufacturing plants. Companies combining advanced manufacturing, localized supply strategies, and material innovation will secure stronger competitive positioning as emission standards continue advancing across global automotive markets.

Tightening emission standards and sustained production of internal combustion engines continue to reinforce demand for advanced EGR tube assemblies. More than 65% of newly manufactured heavy-duty diesel engines incorporate high-temperature stainless-steel EGR systems, while automated tube-forming processes have improved production efficiency by nearly 18% and reduced defect rates by over 15%. China's implementation of China VI standards and Europe's transition toward Euro 7 have accelerated investment in durable emission-control components across automotive supply chains. This regulatory shift increases demand for precision-engineered tubing capable of withstanding extreme thermal cycles. Manufacturers are expanding laser-welding capacity, investing in corrosion-resistant alloys, and strengthening OEM partnerships to secure long-term supply contracts. Companies integrating material innovation with localized manufacturing are achieving stronger operational resilience and faster product qualification cycles.

Persistent fluctuations in stainless-steel and nickel prices continue to challenge cost stability for EGR tube manufacturers. Raw materials account for nearly 45% of total component production costs, while energy-intensive metal processing contributes approximately 20% of manufacturing expenditure. Germany and Japan have experienced periodic supply constraints caused by global alloy procurement disruptions and transportation bottlenecks, creating uncertainty in production planning and inventory management. These pressures reduce pricing flexibility, compress operating margins, and complicate long-term procurement strategies for suppliers serving multiple automotive platforms. To reduce exposure, manufacturers are expanding multi-country sourcing networks, negotiating long-term material contracts, increasing recycled alloy utilization, and localizing fabrication operations. Strategic procurement has become a competitive differentiator rather than a traditional cost-management function.

Growing adoption of lightweight, high-strength alloys presents significant opportunities for premium EGR tube manufacturers. Advanced stainless-steel grades can improve thermal durability by nearly 25% while reducing component weight by approximately 12%, supporting better engine efficiency and extended service life. India is rapidly expanding automotive component manufacturing under production-linked incentive programs, encouraging suppliers to establish advanced fabrication facilities and automated production lines. Digital quality inspection, predictive manufacturing analytics, and robotic forming technologies are further improving production consistency and lowering rejection rates. Companies are increasing investment in R&D, collaborating with material science specialists, and developing modular EGR solutions compatible with multiple engine platforms. The strongest competitive advantage increasingly comes from engineering performance rather than production scale alone.

Automotive platform diversification is increasing engineering complexity for EGR tube manufacturers serving global OEMs. More than 40% of vehicle platforms now require customized routing geometries, while validation and durability testing can represent over 15% of total product development timelines. The rapid expansion of hybrid powertrains in countries such as South Korea and Japan is adding new thermal management requirements, forcing suppliers to redesign components for multiple engine configurations. Maintaining dimensional precision, material consistency, and production scalability across varied applications remains a significant operational challenge. Manufacturers must invest in digital simulation, flexible manufacturing systems, advanced validation laboratories, and engineering partnerships to shorten development cycles. Companies capable of standardizing production while supporting platform customization will secure stronger long-term competitiveness in the evolving automotive supply chain.

Laser Welding Gains Momentum Modern EGR tube production is rapidly shifting toward automated laser welding, with adoption exceeding 58% among leading automotive component manufacturers. Precision welding has reduced dimensional deviations by nearly 20% while lowering material waste by approximately 14%. Germany and Japan continue expanding automated production cells to meet tighter emission-compliance requirements. Suppliers are increasing investments in digital inspection systems and robotics to improve throughput, shorten validation cycles, and maintain consistent product quality across multiple vehicle platforms.

Localized Supply Networks Expand Automotive suppliers are restructuring procurement by regionalizing stainless-steel sourcing and component manufacturing. More than 46% of tier-one suppliers have diversified material sourcing to reduce logistics disruptions, while localized fabrication has shortened delivery lead times by nearly 18%. Supply-chain adjustments following global logistics disruptions have encouraged manufacturers in India and Mexico to expand domestic processing capabilities. Companies are strengthening supplier partnerships and inventory planning to improve operational continuity and procurement flexibility.

Advanced Alloys Improve Durability High-temperature stainless alloys and enhanced corrosion-resistant coatings are becoming standard across premium EGR tube applications. New material formulations improve thermal fatigue resistance by approximately 24% and extend service life by nearly 19% under demanding operating conditions. Automotive manufacturers are responding to stricter emission requirements by specifying longer-life components that reduce maintenance frequency. Component suppliers are expanding material engineering programs and collaborating with metallurgy specialists to accelerate commercial deployment.

Digital Quality Control Accelerates AI-enabled inspection, machine vision, and real-time production analytics are transforming EGR tube manufacturing workflows. Automated inspection systems now identify more than 95% of dimensional defects while reducing manual inspection time by approximately 35%. China's large automotive manufacturing facilities are integrating connected production platforms to improve traceability and process consistency. Manufacturers are scaling smart factory initiatives, combining predictive maintenance with production analytics to strengthen quality assurance and increase manufacturing efficiency.

Flexible EGR Tube remains the dominant segment, accounting for approximately 44% of total market demand due to its ability to accommodate engine vibration, thermal expansion, and compact engine layouts. OEMs increasingly specify flexible designs because they simplify installation and improve long-term durability under fluctuating operating temperatures. Corrugated EGR Tube represents the fastest-growing segment, supported by rising deployment in high-performance diesel engines where superior flexibility and fatigue resistance are essential. Adoption of corrugated configurations has increased by nearly 16% across newly developed commercial vehicle platforms. Meanwhile, Rigid EGR Tube continues serving applications requiring structural stability and simplified routing, while the Others category supports specialized industrial and customized engine systems. Manufacturers are expanding portfolios with lightweight stainless-steel materials and automated forming technologies to improve durability and manufacturing precision. Investment priorities increasingly favor flexible and corrugated solutions as emission standards become stricter and engine packaging grows more complex. Companies are strengthening OEM partnerships while optimizing production processes to support platform-specific product customization and improved lifecycle performance.

Passenger Vehicles represent the leading application, contributing nearly 52% of overall demand because of large production volumes and stringent emission-control requirements across gasoline and diesel models. Manufacturers continue integrating advanced EGR systems into compact and mid-size vehicles to improve combustion efficiency and regulatory compliance. Heavy Commercial Vehicles form the fastest-growing application, supported by increasing freight activity and stricter heavy-duty engine standards. Advanced EGR integration across newly introduced heavy-duty platforms has expanded by approximately 18%, encouraging greater use of high-temperature corrosion-resistant tube assemblies. Light Commercial Vehicles maintain stable adoption through urban logistics expansion, while Off-Highway Equipment increasingly requires durable EGR solutions for agricultural and construction machinery. Automotive suppliers are scaling dedicated production lines, investing in automated quality inspection, and strengthening engineering collaboration with vehicle manufacturers to address diverse application requirements. Product development increasingly focuses on thermal durability, weight reduction, and simplified installation, allowing manufacturers to serve both mature passenger vehicle programs and expanding heavy-duty applications more efficiently.

OEMs remain the dominant end-user segment, representing approximately 67% of market demand because EGR tubes are integrated directly during vehicle manufacturing and engine assembly. Long-term supply agreements, strict quality standards, and platform-specific engineering continue concentrating procurement within original equipment manufacturers. The Aftermarket segment is the fastest-growing, supported by increasing vehicle parc age and replacement demand for corrosion-resistant exhaust components. Replacement activity has increased by nearly 14% across aging commercial vehicle fleets, creating sustained opportunities for premium replacement products. Fleet Operators continue emphasizing component reliability to reduce maintenance intervals, while Automotive Service Providers expand installation capabilities to support increasingly sophisticated emission-control systems. Manufacturers are introducing differentiated product ranges, strengthening distribution partnerships, and expanding regional inventories to improve service responsiveness across OEM and replacement channels. Customized pricing programs, technical support, and digital catalog integration are helping suppliers improve customer retention while addressing the evolving maintenance needs of commercial and passenger vehicle operators.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

North America represents approximately 22.6% of the global EGR tube market, supported by advanced automotive manufacturing, stringent emission compliance, and strong commercial vehicle production. OEMs continue upgrading exhaust system architectures with high-temperature stainless-steel EGR tubes capable of supporting extended service intervals. More than 68% of heavy-duty engine production incorporates advanced emission-control assemblies with automated quality inspection integrated into manufacturing operations. Investment in digital manufacturing and robotic welding has improved production consistency while reducing component rework across major automotive facilities. Strategic collaboration between vehicle manufacturers and tier-one suppliers is strengthening localized sourcing, improving inventory resilience, and accelerating qualification of next-generation emission-control components.

United States Market Outlook: The United States leads the regional market through its extensive automotive manufacturing base, commercial truck production, and established supplier ecosystem. More than 60% of North American heavy-duty engine manufacturing is concentrated in the country, supporting continuous demand for precision-engineered EGR tube assemblies. Manufacturers continue investing in automated production equipment, advanced metallurgy, and supplier localization while expanding engineering partnerships to improve durability, reduce warranty costs, and comply with evolving emission standards across passenger and commercial vehicle platforms.

Europe accounts for nearly 24.4% of global market demand, supported by advanced automotive engineering, premium vehicle manufacturing, and rigorous emission legislation. Vehicle manufacturers continue integrating corrosion-resistant EGR tube systems into new engine platforms to improve thermal efficiency and regulatory compliance. Automated tube-forming technologies are now deployed across more than 72% of major emission-component production facilities, improving manufacturing precision and operational consistency. Ongoing modernization of automotive supply chains has encouraged greater collaboration between OEMs and specialized exhaust component suppliers, enabling faster product validation and improved production flexibility for evolving engine platforms.

Germany Market Outlook: Germany remains the region's strategic manufacturing hub due to its concentration of premium automotive brands, advanced component suppliers, and engineering expertise. More than 45% of Europe's premium vehicle production is supported by German manufacturing facilities, encouraging continuous adoption of high-performance EGR tube technologies. Suppliers are strengthening investments in laser welding, lightweight alloy processing, and automated quality assurance while collaborating closely with OEM engineering teams to accelerate development of advanced emission-control systems.

Asia-Pacific leads the global market with approximately 43.8% share, driven by extensive automotive manufacturing capacity, competitive production economics, and expanding domestic vehicle demand. China, India, Japan, and South Korea collectively account for the majority of regional component output, supported by integrated supply networks and large-scale industrial clusters. More than 70% of leading regional manufacturers have implemented automated tube-forming and robotic welding technologies to improve productivity and reduce manufacturing variability. Continued investment in localized material processing and export-oriented production enables manufacturers to respond efficiently to both domestic and international automotive demand.

China Market Outlook: China dominates regional production through its extensive automotive manufacturing ecosystem, large supplier base, and ongoing industrial modernization. The country contributes nearly 34% of global EGR tube manufacturing capacity, supported by high-volume passenger and commercial vehicle production. Manufacturers continue expanding smart manufacturing facilities, improving digital quality management, and increasing investment in advanced stainless-steel processing technologies to strengthen export competitiveness and meet increasingly demanding emission-control specifications.

South America represents approximately 5.8% of the global market, supported by commercial transportation, agricultural equipment manufacturing, and gradual modernization of vehicle emission systems. Brazil and Argentina continue strengthening regional automotive production while increasing localization of emission-control components. More than 55% of regional EGR tube demand originates from commercial vehicle applications, reflecting continued investment in freight transportation and industrial logistics. Manufacturers are improving supplier integration and expanding regional production capabilities to reduce import dependency while maintaining cost competitiveness across evolving automotive supply chains.

Brazil Market Outlook: Brazil serves as the region's largest automotive manufacturing center with strong commercial vehicle production and an established network of component suppliers. More than half of South America's automotive output is produced within Brazil, supporting sustained demand for durable emission-control components. Local manufacturers are increasing production automation, strengthening partnerships with global OEMs, and expanding domestic sourcing strategies to improve manufacturing resilience and support future regulatory compliance requirements.

Middle East & Africa accounts for approximately 3.4% of global market activity, with demand supported by commercial vehicle fleets, industrial transportation, and expanding automotive assembly operations. Infrastructure modernization and industrial diversification programs are encouraging gradual development of regional automotive supply capabilities. More than 30% of newly established automotive component facilities emphasize localized production and improved manufacturing efficiency. Companies are strengthening regional partnerships, expanding technical service capabilities, and investing in workforce development to support growing demand for reliable emission-control components while improving operational self-sufficiency.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through industrial diversification initiatives, expanding vehicle assembly operations, and investments in advanced manufacturing infrastructure. New automotive manufacturing projects continue strengthening domestic supplier opportunities while encouraging technology transfer and localized production. Manufacturers are prioritizing precision fabrication, workforce training, and strategic international partnerships to establish a competitive automotive component ecosystem capable of supporting long-term industrial development.

The market is characterized by competition between global engineering suppliers including BENTELER, BorgWarner, Tenneco, Continental, and Rheinmetall, while regional tube manufacturers compete primarily on cost, delivery speed, and localized production. The top five players collectively account for approximately 46% of the global market, reflecting moderate consolidation with strong OEM-driven procurement. Competition centers on thermal durability, corrosion resistance, manufacturing precision, and supply-chain responsiveness. Automated production has reduced manufacturing defects by nearly 20%, while localized sourcing strategies have shortened delivery lead times by approximately 18%. Premium suppliers differentiate through proprietary forming technologies, laser welding, and integrated exhaust solutions, whereas regional manufacturers emphasize pricing flexibility and rapid customization. Companies are expanding manufacturing capacity, strengthening OEM partnerships, and increasing vertical integration to secure material availability and reduce supply risks. Rising qualification requirements, advanced metallurgy expertise, and long validation cycles remain significant entry barriers. Sustainable competitive success depends on engineering capability, manufacturing automation, dependable supply networks, and long-term OEM relationships.

BorgWarner Inc.

Tenneco Inc.

Continental AG

Rheinmetall AG

MAHLE GmbH

Hutchinson SA

Senior plc

TI Fluid Systems plc

Yutaka Giken Co., Ltd.

Maruyasu Industries Co., Ltd.

Futaba Industrial Co., Ltd.

Manufacturing technology is advancing through automated laser welding, robotic tube forming, and AI-enabled dimensional inspection. Laser-welded EGR tubes provide approximately 20% higher thermal fatigue resistance than conventional welded assemblies while reducing production scrap by nearly 12%. More than 60% of leading automotive component plants have integrated automated inspection systems, enabling faster quality validation, improved repeatability, and greater manufacturing consistency for high-volume vehicle programs.

Material innovation is reshaping product performance through advanced ferritic stainless steels, corrosion-resistant coatings, and optimized internal flow geometries. Compared with conventional tube designs, new-generation engineered structures improve heat transfer efficiency by approximately 15% while extending service life by nearly 18%. Global OEM suppliers benefit from these technologies through lower warranty exposure, improved emission compliance, and simplified integration across passenger and commercial vehicle platforms. Digital manufacturing platforms further strengthen traceability and predictive quality management.

Between 2026 and 2028, manufacturers are expected to accelerate deployment of digital twins, AI-assisted process optimization, and predictive maintenance across production facilities. Smart manufacturing adoption is projected to exceed 70% among major suppliers, reducing unplanned downtime by approximately 25%. Companies investing early in intelligent production, advanced metallurgy, and integrated engineering capabilities will strengthen competitive positioning as emission-control requirements become increasingly sophisticated.

May 2025 – BorgWarner extended four Exhaust Gas Recirculation (EGR) contracts with a major North American OEM, securing production across passenger and light commercial vehicle platforms through 2029. The agreement expands long-term manufacturing stability and reinforces its emission-system leadership. Source: www.borgwarner.com

March 2025 – BENTELER reported a 26% reduction in Scope 1 and Scope 2 production emissions while continuing strategic investment in sustainable steel tube technologies and automotive product innovation. The achievement strengthens manufacturing efficiency and supports environmentally focused OEM partnerships. Source: www.benteler.com

August 2024 – Rheinmetall secured a new three-digit million-euro order for exhaust gas recirculation valves covering production from 2026 through 2031. The contract strengthens long-term production utilization and reinforces its commercial vehicle emission-control portfolio. Source: www.rheinmetall.com

April 2025 – BENTELER and PHINIA introduced the world's first series-production 500-bar gasoline fuel rail, enabling finer fuel atomization and supporting compliance with advanced emission standards. The innovation enhances combustion efficiency and strengthens next-generation engine system competitiveness.

The report provides comprehensive analysis of the global EGR Tube market across Flexible EGR Tube, Rigid EGR Tube, Corrugated EGR Tube, and Other product categories, together with Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, and Off-Highway Equipment applications. It further evaluates demand across OEMs, Aftermarket, Fleet Operators, and Automotive Service Providers while examining operational developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 65% of market demand remains concentrated within OEM procurement channels, while advanced manufacturing adoption continues expanding across leading production facilities.

The study assesses competitive positioning, manufacturing strategies, material innovation, supply-chain developments, and technology adoption expected to influence business decisions between 2026 and 2033. It evaluates deployment trends, regional production concentration, enterprise expansion strategies, and emerging opportunities across premium emission-control components. The report supports investment prioritization, product development, geographic expansion, supplier evaluation, and long-term competitive planning through detailed segmentation, technology assessment, and strategic market intelligence.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 228.0 Million |

| Market Revenue (2033) | USD 331.8 Million |

| CAGR (2026–2033) | 4.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | BENTELER International AG; BorgWarner Inc.; Tenneco Inc.; Continental AG; Rheinmetall AG; MAHLE GmbH; Hutchinson SA; Senior plc; TI Fluid Systems plc; Yutaka Giken Co., Ltd.; Maruyasu Industries Co., Ltd.; Futaba Industrial Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |