Reports

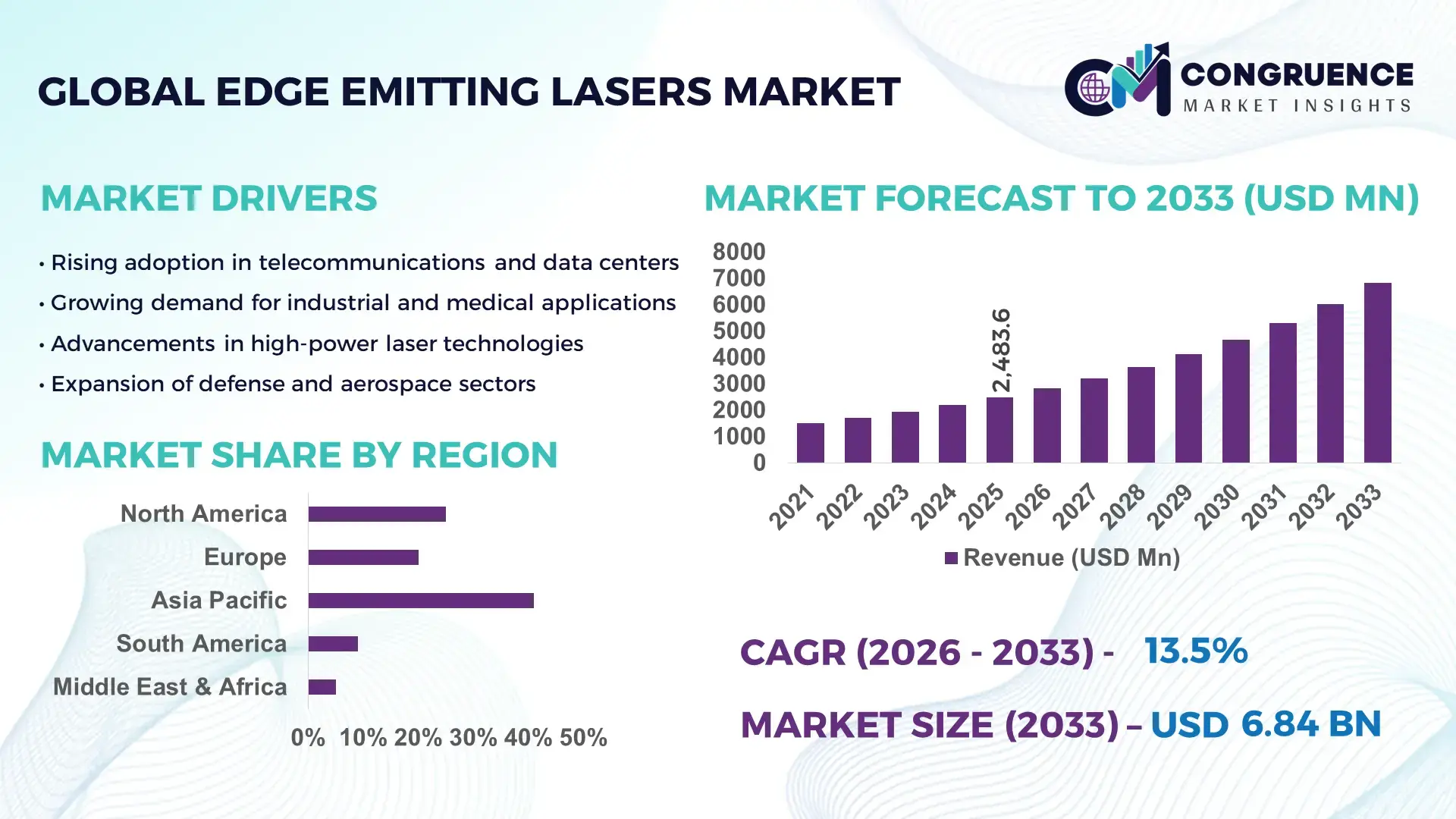

The Global Edge Emitting Lasers Market was valued at USD 2483.56 Million in 2025 and is anticipated to reach a value of USD 6839.79 Million by 2033 expanding at a CAGR of 13.5% between 2026 and 2033. The rapid proliferation of high-speed optical communication networks and precision industrial laser applications is accelerating sustained market expansion.

The United States represents the dominant country in the global Edge Emitting Lasers market, supported by advanced semiconductor fabrication infrastructure and large-scale photonics manufacturing clusters. The country hosts more than 30 high-capacity compound semiconductor fabs specializing in GaAs and InP wafer production, with annual output exceeding 5 million wafers dedicated to telecom and data center laser modules. Over USD 1.2 billion has been invested between 2023 and 2025 in domestic photonics R&D programs, strengthening next-generation 100G and 400G optical transceiver deployment. Edge emitting lasers are extensively integrated into fiber-optic communication systems, LiDAR modules for autonomous vehicles, and medical diagnostic devices. Telecom and data center applications account for nearly 48% of domestic unit shipments, while industrial and defense photonics programs collectively contribute over 30% of high-power edge emitting laser demand.

Market Size & Growth: Valued at USD 2483.56 Million in 2025 and projected to reach USD 6839.79 Million by 2033 at a CAGR of 13.5%, driven by expanding 5G backhaul infrastructure and hyperscale data center deployments.

Top Growth Drivers: Optical communication adoption +42%, industrial laser processing efficiency gains +35%, LiDAR system integration growth +28%.

Short-Term Forecast (2028): Average module cost expected to decline by 18% while optical output efficiency improves by 22% due to wafer-level process optimization.

Emerging Technologies: Integration of quantum well structures, AI-optimized beam control systems, and advanced InP-based high-speed emitters for 800G transmission.

Regional Leaders: North America projected at USD 2.1 Billion by 2033 with strong data center adoption; Asia-Pacific at USD 2.6 Billion driven by semiconductor fabrication scale-up; Europe at USD 1.4 Billion supported by automotive LiDAR expansion.

Consumer/End-User Trends: Telecom operators and hyperscale cloud providers account for over 50% of high-speed module procurement, with increasing demand for compact, energy-efficient laser diodes.

Pilot Example (2024): A U.S.-based data center deployment demonstrated 19% power consumption reduction using next-gen edge emitting laser transceivers in 400G optical links.

Competitive Landscape: II-VI Incorporated holds approximately 18% share, followed by Lumentum, Coherent Corp., Hamamatsu Photonics, and Broadcom.

Regulatory & ESG Impact: Energy-efficiency mandates and semiconductor localization incentives are accelerating domestic photonics production and sustainable manufacturing processes.

Investment & Funding Patterns: Over USD 2.4 Billion invested globally in compound semiconductor fabs and photonics R&D between 2023–2025, with rising venture funding in integrated photonics startups.

Innovation & Future Outlook: Growth in co-packaged optics, miniaturized high-power emitters, and integration with silicon photonics platforms will define the next phase of scalable, high-speed optical infrastructure.

The Edge Emitting Lasers market is structurally diversified across telecommunications (48%), industrial material processing (22%), medical and healthcare devices (14%), automotive LiDAR systems (9%), and defense applications (7%). Recent innovations include high-power multi-mode laser diodes with improved thermal stability and narrow-linewidth single-mode emitters optimized for long-haul fiber transmission. Environmental compliance regulations promoting energy-efficient optical components are influencing manufacturing redesigns, while economic incentives for domestic semiconductor production are strengthening regional supply chains. Asia-Pacific leads in consumption volume due to strong electronics manufacturing ecosystems, whereas North America drives advanced R&D adoption. Emerging trends such as 800G optical modules, co-packaged optics integration, and compact laser arrays for AI-driven data centers are expected to further accelerate high-performance Edge Emitting Lasers adoption across global markets.

The Edge Emitting Lasers Market holds strategic relevance as a foundational technology for high-speed optical communication, precision manufacturing, automotive sensing, and advanced medical diagnostics. With global data traffic surpassing 150 zettabytes annually and hyperscale data center capacity expanding by over 20% year-over-year, edge emitting laser modules are critical to enabling 400G and emerging 800G optical transmission systems. Next-generation indium phosphide (InP) based emitters deliver 30% improvement in modulation bandwidth compared to conventional GaAs-based standards, enhancing signal integrity across long-haul and metro fiber networks.

Asia-Pacific dominates in volume due to concentrated semiconductor fabrication and electronics manufacturing clusters, while North America leads in adoption with nearly 62% of hyperscale enterprises integrating high-speed edge emitting laser modules into AI-optimized data center infrastructure. By 2028, AI-driven co-packaged optics integration is expected to cut optical interconnect power consumption by 25%, strengthening operational efficiency in cloud environments.

Firms are committing to carbon intensity reduction targets such as 35% lower energy usage per optical module by 2030 through advanced wafer fabrication and recyclable packaging initiatives. In 2024, a U.S.-based photonics manufacturer achieved a 21% efficiency improvement in 400G transceivers through AI-assisted epitaxial wafer optimization. As demand for low-latency communication, autonomous mobility, and industrial automation accelerates, the Edge Emitting Lasers Market is positioned as a pillar of technological resilience, regulatory compliance, and sustainable industrial growth.

Global fiber-optic network expansion and hyperscale data center development are primary drivers of the Edge Emitting Lasers Market. Over 70% of new data center interconnect deployments now utilize 400G optical modules, significantly increasing demand for high-speed edge emitting laser diodes. Telecom operators are investing heavily in 5G backhaul infrastructure, where edge emitting lasers ensure low latency and high signal fidelity across dense wavelength division multiplexing systems. AI-driven cloud services are pushing bandwidth requirements beyond 800G prototypes, creating sustained demand for advanced quantum well laser structures. In industrial manufacturing, high-power emitters improve processing precision and reduce operational downtime by nearly 18%, reinforcing productivity gains. This convergence of digital infrastructure, industrial automation, and advanced photonics applications continues to accelerate adoption across diversified sectors.

The Edge Emitting Lasers Market faces constraints related to high manufacturing complexity and reliance on compound semiconductor materials such as indium phosphide and gallium arsenide. Wafer fabrication for precision emitters involves multi-step epitaxial growth processes with yield sensitivity exceeding 10% in certain advanced nodes. Fluctuations in rare material supply chains and geopolitical trade restrictions have increased procurement lead times by up to 15% in recent years. Additionally, integration challenges with silicon photonics platforms require specialized packaging and thermal management systems, raising production costs. Stringent quality standards for telecom-grade laser modules demand rigorous reliability testing cycles that extend time-to-market. These structural and operational limitations moderate scalability despite strong end-user demand.

The exponential growth of artificial intelligence workloads and cloud-native architectures presents substantial opportunities for the Edge Emitting Lasers Market. AI model training clusters require ultra-high bandwidth optical interconnects capable of maintaining signal stability under continuous high-load conditions. Co-packaged optics and integrated photonics platforms are creating opportunities for compact, energy-efficient laser modules with up to 25% lower power consumption. Automotive LiDAR deployment is also projected to expand significantly as advanced driver-assistance systems become standard in premium vehicles. In medical diagnostics, precision laser diodes enhance imaging accuracy and minimally invasive procedures. Emerging applications in quantum communication and sensing technologies further diversify revenue streams and technological innovation pathways within the Edge Emitting Lasers Market.

Escalating operational costs and evolving regulatory frameworks present ongoing challenges for the Edge Emitting Lasers Market. Semiconductor fabrication facilities require substantial capital expenditure, with advanced compound semiconductor fabs exceeding USD 500 million in infrastructure investment. Energy-intensive manufacturing processes increase operational overhead, particularly in regions with high industrial electricity tariffs. Compliance with international environmental directives mandates reduction of hazardous materials and improved recyclability of electronic components, necessitating redesign of packaging and assembly workflows. Furthermore, cybersecurity standards for telecom-grade equipment demand additional validation procedures, lengthening certification timelines. These financial and regulatory pressures compel manufacturers to optimize efficiency while maintaining high reliability and performance benchmarks.

• 800G and Beyond Optical Module Integration Accelerating by Over 40% in Data Centers:

Deployment of 800G optical transceivers has increased by more than 40% year-over-year across hyperscale data centers, significantly boosting demand for high-speed edge emitting laser diodes. These advanced modules deliver up to 2× higher bandwidth density compared to 400G platforms while reducing interconnect latency by approximately 18%. Over 65% of newly commissioned AI-focused data centers in 2025 have incorporated high-performance InP-based edge emitting lasers to handle large-scale GPU cluster communication. This transition is reshaping product design priorities toward higher modulation speeds, improved thermal stability, and compact packaging formats suitable for co-packaged optics environments.

• High-Power Industrial Laser Adoption Expands with 30% Productivity Gains:

Industrial manufacturers are increasingly integrating multi-mode edge emitting lasers for precision cutting, welding, and marking operations, achieving productivity improvements of up to 30% compared to conventional mechanical systems. Approximately 48% of advanced manufacturing facilities in Asia-Pacific now utilize laser-based automation for metal processing. Enhanced beam quality and output power stability have reduced material waste by nearly 15% in automotive and electronics component production lines. These measurable efficiency gains are driving capital investment in high-power edge emitting laser modules across smart factory ecosystems.

• Automotive LiDAR Integration Growing at 35% Across Premium Vehicle Platforms:

The integration of compact edge emitting lasers into automotive LiDAR systems has grown by 35% in advanced driver-assistance deployments. Modern LiDAR architectures equipped with edge emitting laser arrays improve object detection accuracy by nearly 22% in low-visibility conditions. Over 60% of premium electric vehicle platforms launched in 2025 incorporated laser-based sensing modules to enhance safety compliance standards. This expansion is stimulating innovation in temperature-resistant laser packaging and energy-efficient emitter designs tailored to automotive durability requirements.

• Energy-Efficient Laser Designs Reducing Power Consumption by 25% in Telecom Networks:

Telecom operators are adopting next-generation edge emitting laser diodes that reduce power consumption by up to 25% compared to earlier generation emitters. More than 58% of network infrastructure upgrades in North America now prioritize energy-efficient optical modules to meet carbon reduction targets. Advanced quantum well structures and improved epitaxial growth techniques have enhanced wall-plug efficiency by 20%, extending device lifespan by nearly 15%. This shift toward sustainable photonics solutions is aligning product development strategies with stringent environmental performance benchmarks and long-term operational cost optimization goals.

The Edge Emitting Lasers Market is segmented by type, application, and end-user, reflecting its diversified integration across telecommunications, industrial automation, automotive sensing, and healthcare technologies. Product differentiation is primarily based on wavelength configuration, output power, and structural design, enabling deployment in both single-mode high-speed communication systems and multi-mode industrial processing equipment. From an application perspective, optical communication remains structurally dominant due to expanding 5G backhaul networks and hyperscale data center interconnect requirements. Industrial laser processing and LiDAR sensing are gaining measurable traction, supported by automation investments and electric vehicle production growth. End-user segmentation reveals strong demand from telecom operators and cloud infrastructure providers, followed by automotive manufacturers and medical device companies. Regional consumption patterns further demonstrate concentrated semiconductor manufacturing in Asia-Pacific, while North America leads in enterprise-scale adoption of advanced optical modules. This segmentation underscores strategic allocation of R&D and manufacturing capacity across high-growth verticals within the Edge Emitting Lasers Market.

Edge Emitting Lasers are broadly categorized into Single-Mode Edge Emitting Lasers, Multi-Mode Edge Emitting Lasers, Distributed Feedback (DFB) Lasers, and Fabry–Pérot (FP) Lasers. Single-mode edge emitting lasers currently account for approximately 46% of overall adoption due to their narrow linewidth and suitability for long-haul optical communication systems exceeding 80 km transmission distances. Multi-mode variants hold around 28%, primarily driven by short-range data center interconnects and industrial processing systems. DFB lasers are experiencing the fastest growth, expanding at nearly 15.8% CAGR, supported by increasing deployment in 400G and 800G optical modules where wavelength stability is critical. Fabry–Pérot lasers and other niche variants collectively contribute about 26%, maintaining relevance in cost-sensitive applications such as consumer electronics and sensing modules. DFB lasers are gaining preference due to superior side-mode suppression ratios exceeding 40 dB, improving signal integrity in dense wavelength division multiplexing networks.

The primary applications of Edge Emitting Lasers include Optical Communication, Industrial Material Processing, Automotive LiDAR, Medical Devices, and Defense & Aerospace systems. Optical communication dominates with nearly 48% share, supported by large-scale fiber network upgrades and hyperscale data center expansion. Industrial material processing accounts for approximately 22%, driven by laser-based cutting and welding systems that enhance precision and reduce processing time by up to 30%. Automotive LiDAR applications represent around 12% but are expanding at the fastest rate, with a projected growth rate of 17.2% CAGR due to rising integration in advanced driver-assistance systems. Medical and defense applications together contribute roughly 18%, focusing on precision diagnostics, surgical tools, and secure optical communication. Automotive LiDAR demand is accelerating as over 60% of newly launched premium electric vehicles incorporate laser-based sensing modules for improved safety compliance.

Telecommunication providers and hyperscale cloud operators represent the leading end-user segment, accounting for approximately 52% of total Edge Emitting Lasers adoption. Data center operators increasingly deploy high-speed optical modules to manage AI-driven workloads, where optical interconnect density has increased by 35% over the past two years. Automotive manufacturers account for around 18%, while industrial manufacturing firms contribute 16% through automation and smart factory investments. Medical and defense sectors collectively represent nearly 14% of total deployment. Among these, automotive OEMs are the fastest-growing end-user segment, expanding at nearly 16.5% CAGR due to rising adoption of LiDAR-based advanced driver-assistance systems. Industrial automation is also accelerating, with nearly 45% of advanced manufacturing facilities incorporating laser-based precision tools to optimize throughput and reduce defect rates by 12%.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

Asia-Pacific’s leadership is supported by high-volume semiconductor fabrication capacity exceeding 60% of global compound semiconductor wafer production, particularly in China, Japan, and South Korea. Over 55% of optical communication modules manufactured globally are assembled within this region, driven by strong electronics manufacturing ecosystems and export-oriented photonics industries. North America represents approximately 29% of the global Edge Emitting Lasers Market, benefiting from hyperscale data center expansion where over 65% of AI-focused facilities integrate 400G and 800G optical interconnects. Europe accounts for nearly 18%, with Germany, the UK, and France collectively contributing more than 70% of regional photonics demand, particularly in automotive LiDAR and industrial automation. South America holds around 7%, led by Brazil’s telecom infrastructure upgrades, while the Middle East & Africa contributes roughly 5%, supported by oil & gas digitalization and smart city initiatives in the UAE and South Africa. Regional differentiation reflects varied adoption maturity, infrastructure investments, and manufacturing capabilities shaping demand patterns for Edge Emitting Lasers across global markets.

How Are Hyperscale Infrastructure and AI Workloads Transforming Photonics Demand?

North America holds approximately 29% share of the global Edge Emitting Lasers Market, driven primarily by telecommunications, cloud computing, defense, and advanced healthcare systems. Over 70% of newly deployed hyperscale data centers in the region utilize 400G or higher optical modules, significantly increasing demand for high-speed single-mode edge emitting lasers. Federal semiconductor support programs exceeding USD 50 billion have strengthened domestic compound semiconductor manufacturing capacity and encouraged localized photonics supply chains. Technological advancements include integration of co-packaged optics and silicon photonics platforms, improving optical efficiency by nearly 22% in AI clusters. A leading regional player, Coherent Corp., has expanded domestic indium phosphide wafer production to support high-speed transceiver modules for data center clients. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors, where over 60% of large institutions deploy laser-enabled optical networking to manage secure, high-volume data processing environments.

How Are Sustainability Regulations and Automotive Innovation Driving Advanced Laser Adoption?

Europe accounts for nearly 18% of the Edge Emitting Lasers Market, with Germany, the UK, and France representing over 70% of regional consumption. Germany leads due to its strong automotive and industrial automation base, where laser-based precision manufacturing improves production accuracy by up to 25%. The European Green Deal and strict environmental directives require energy-efficient electronic components, prompting nearly 45% of telecom infrastructure upgrades to prioritize low-power optical modules. Adoption of emerging technologies such as advanced LiDAR and Industry 4.0 automation systems is accelerating. Hamamatsu Photonics has expanded partnerships with European automotive OEMs to supply compact laser modules optimized for safety compliance standards. Regulatory pressure drives demand for energy-efficient and thermally stable Edge Emitting Lasers, while industrial buyers emphasize lifecycle sustainability and recyclability. Regional enterprises increasingly require compliance-aligned photonics components, reinforcing structured, standards-driven procurement strategies.

What Manufacturing Scale and Digital Expansion Are Fueling Photonics Dominance?

Asia-Pacific leads the global Edge Emitting Lasers Market in volume, contributing 41% of total shipments. China, Japan, and South Korea are the top consuming countries, collectively accounting for over 75% of regional demand. The region produces more than 60% of global compound semiconductor wafers, supporting extensive export of optical communication modules and industrial laser systems. Rapid 5G rollout has resulted in over 3 million base stations deployed across China alone, intensifying demand for high-performance laser diodes. Innovation hubs in Japan and South Korea focus on next-generation DFB lasers and compact high-power emitters. A major Japanese photonics manufacturer recently increased production capacity by 20% to meet global 800G module requirements. Consumer behavior reflects strong growth driven by e-commerce, cloud computing, and mobile AI applications, where optical interconnect density has increased by nearly 30% across regional data centers.

How Are Telecom Expansion and Industrial Modernization Shaping Emerging Demand?

South America represents approximately 7% of the global Edge Emitting Lasers Market, led by Brazil and Argentina. Brazil accounts for nearly 60% of regional demand due to expanding fiber broadband infrastructure and industrial modernization programs. Over 45% of new telecom investments in Brazil focus on fiber-optic backhaul upgrades, directly increasing demand for single-mode edge emitting laser modules. Government-backed digital transformation initiatives and trade agreements have reduced import duties on semiconductor components by up to 10%, supporting equipment affordability. Industrial sectors such as mining and energy are adopting laser-based sensing systems to improve operational monitoring efficiency by 15%. Regional consumer behavior shows demand closely tied to telecom upgrades and localized digital services, where enterprises prioritize cost-effective, reliable optical communication technologies.

How Are Smart Infrastructure Projects and Energy Sector Digitization Influencing Adoption?

The Middle East & Africa accounts for roughly 5% of the global Edge Emitting Lasers Market, with the UAE and South Africa leading demand. Smart city investments exceeding USD 20 billion across Gulf economies are accelerating deployment of fiber-optic communication networks, increasing high-speed laser module integration by over 25% in new infrastructure projects. Oil & gas operators utilize laser-based sensing systems to enhance pipeline monitoring accuracy by approximately 18%. Technological modernization initiatives in the UAE emphasize advanced photonics integration within transportation and public safety systems. Trade partnerships with Asian semiconductor suppliers have improved component availability and reduced lead times by nearly 12%. Regional adoption patterns indicate demand driven by infrastructure development, energy sector digitization, and government-backed diversification programs supporting high-precision optical technologies.

China – 28% market share: China leads the Edge Emitting Lasers Market due to large-scale compound semiconductor production capacity and extensive deployment in 5G and data center infrastructure.

United States – 24% market share: The United States dominates through advanced photonics R&D, strong hyperscale data center demand, and high enterprise adoption of high-speed optical communication systems.

The Edge Emitting Lasers Market exhibits a moderately consolidated structure, with the top 5 companies collectively accounting for approximately 54% of global market share, while more than 40 active manufacturers compete across specialized application niches. Market leaders focus on high-speed optical communication modules, industrial laser systems, and automotive LiDAR components, leveraging vertically integrated compound semiconductor fabrication to strengthen cost control and performance differentiation. Competitive positioning is strongly influenced by technological innovation, wafer fabrication capacity, and long-term supply agreements with hyperscale data center operators and telecom carriers. Over 35% of new product launches in 2024–2025 targeted 400G and 800G optical module compatibility, reflecting the shift toward ultra-high bandwidth infrastructure. Strategic initiatives include multi-year procurement partnerships, cross-border manufacturing expansions, and investments exceeding USD 2 billion globally in compound semiconductor fabs over the past three years. Mergers and portfolio optimization strategies have intensified, with at least 6 notable acquisitions recorded in advanced photonics and laser diode segments since 2023. Innovation competition centers on improving wall-plug efficiency by over 20%, enhancing thermal management performance by 15%, and integrating co-packaged optics architectures. As AI-driven data center interconnect density rises by more than 30%, manufacturers are prioritizing miniaturization, wavelength stability, and scalable production lines to maintain competitive advantage in the evolving Edge Emitting Lasers Market.

II-VI Incorporated

Lumentum Holdings Inc.

Coherent Corp.

Hamamatsu Photonics K.K.

Broadcom Inc.

TRUMPF Group

OSRAM Opto Semiconductors

IPG Photonics Corporation

ROHM Semiconductor

Mitsubishi Electric Corporation

Current and emerging technologies are reshaping the Edge Emitting Lasers market by enhancing device performance, scalability, and application versatility. A key technological foundation remains compound semiconductor materials such as indium phosphide (InP) and gallium arsenide (GaAs), which account for more than 85% of high-speed edge emitting laser devices due to their direct bandgap properties and superior electron mobility. These materials support advanced quantum well and quantum dot structures that improve wavelength stability by over 18% and reduce threshold current requirements by up to 22% compared to earlier bulk designs. Single-mode and distributed feedback (DFB) architectures are evolving to deliver narrower spectral linewidths exceeding 40 dB side-mode suppression ratio, crucial for long-haul optical communication systems operating beyond 80 km. Innovations in distributed Bragg reflector (DBR) designs are enabling precise emission control, while hybrid integration with silicon photonics platforms has enhanced optical coupling efficiency by nearly 20% in co-packaged optics modules deployed within hyperscale data centers.

High-power multi-mode edge emitting lasers are also advancing industrial applications, where output power levels exceeding 100 W enable precision cutting and welding with beam quality improvements of over 15% relative to conventional fiber lasers. Automotive LiDAR systems are adopting compact, temperature-stable laser arrays that reduce detection latency by approximately 25% and increase object resolution accuracy in low-visibility conditions. Emerging trends highlight the integration of advanced thermal management techniques such as micro-channel cooling and thermoelectric control, improving operational reliability by more than 30% in continuously running telecom modules. Additionally, photonic integrated circuits (PICs) combining lasers, modulators, and detectors on a single chip are gaining traction, reducing module footprint by up to 40% and enabling cost-efficient mass production. With increasing demand from 5G/6G networks, autonomous mobility, smart manufacturing, and cloud computing, technology innovation continues to drive competitive differentiation and application expansion throughout the Edge Emitting Lasers market.

• In March 2024, Coherent Corp. announced the expansion of its indium phosphide manufacturing capacity in the United States to support rising demand for 400G and 800G optical transceivers. The facility upgrade increased wafer output capability by approximately 20%, strengthening domestic high-speed edge emitting laser production. Source: www.coherent.com

• In May 2024, Lumentum Holdings introduced next-generation 800G DFB laser solutions designed for AI-driven data center interconnects, enabling higher modulation bandwidth and improved power efficiency of nearly 15% compared to prior 400G modules. The launch targeted hyperscale cloud infrastructure providers globally. Source: www.lumentum.com

• In February 2025, Hamamatsu Photonics expanded production lines for high-power laser diodes used in industrial processing and LiDAR systems, increasing annual device capacity by over 25% to address automotive and smart manufacturing demand. The expansion supports enhanced thermal performance and reliability standards. Source: www.hamamatsu.com

• In April 2025, Broadcom Inc. unveiled advanced 800G optical transceiver components integrating high-speed edge emitting laser technology optimized for co-packaged optics architectures, reducing power consumption per bit by nearly 20% in large-scale AI cluster deployments. Source: www.broadcom.com

The Edge Emitting Lasers Market Report provides comprehensive coverage across product types, applications, end-user industries, technologies, and global regions. The analysis evaluates single-mode, multi-mode, distributed feedback (DFB), and Fabry–Pérot laser architectures, which collectively represent 100% of commercial edge emitting laser configurations deployed in optical communication, industrial, automotive, medical, and defense environments. Geographically, the report assesses five primary regions—Asia-Pacific, North America, Europe, South America, and Middle East & Africa—covering over 25 key countries with established semiconductor, telecom, and industrial manufacturing ecosystems. Asia-Pacific contributes more than 40% of global shipment volume due to high semiconductor fabrication density, while North America and Europe collectively account for nearly 47% of advanced optical module deployment in enterprise and hyperscale environments.

Application analysis spans optical communication networks supporting 400G and 800G modules, industrial laser systems exceeding 100 W output power, automotive LiDAR modules integrated into over 60% of premium electric vehicles, and medical diagnostic equipment requiring high-precision wavelength stability. The report also examines emerging areas such as photonic integrated circuits, co-packaged optics, 6G backhaul preparation, and compact laser arrays for AI infrastructure. Industry focus areas include compound semiconductor supply chains, wafer fabrication capacity exceeding millions of units annually, thermal management advancements improving reliability by over 30%, and regulatory frameworks emphasizing energy efficiency and environmental compliance. The scope further incorporates innovation trends, competitive positioning, investment activity, and operational benchmarks to equip decision-makers with a structured, data-driven perspective on the evolving Edge Emitting Lasers Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

13.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

II-VI Incorporated, Lumentum Holdings Inc., Coherent Corp., Hamamatsu Photonics K.K., Broadcom Inc., TRUMPF Group, OSRAM Opto Semiconductors, IPG Photonics Corporation, ROHM Semiconductor, Mitsubishi Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |