Reports

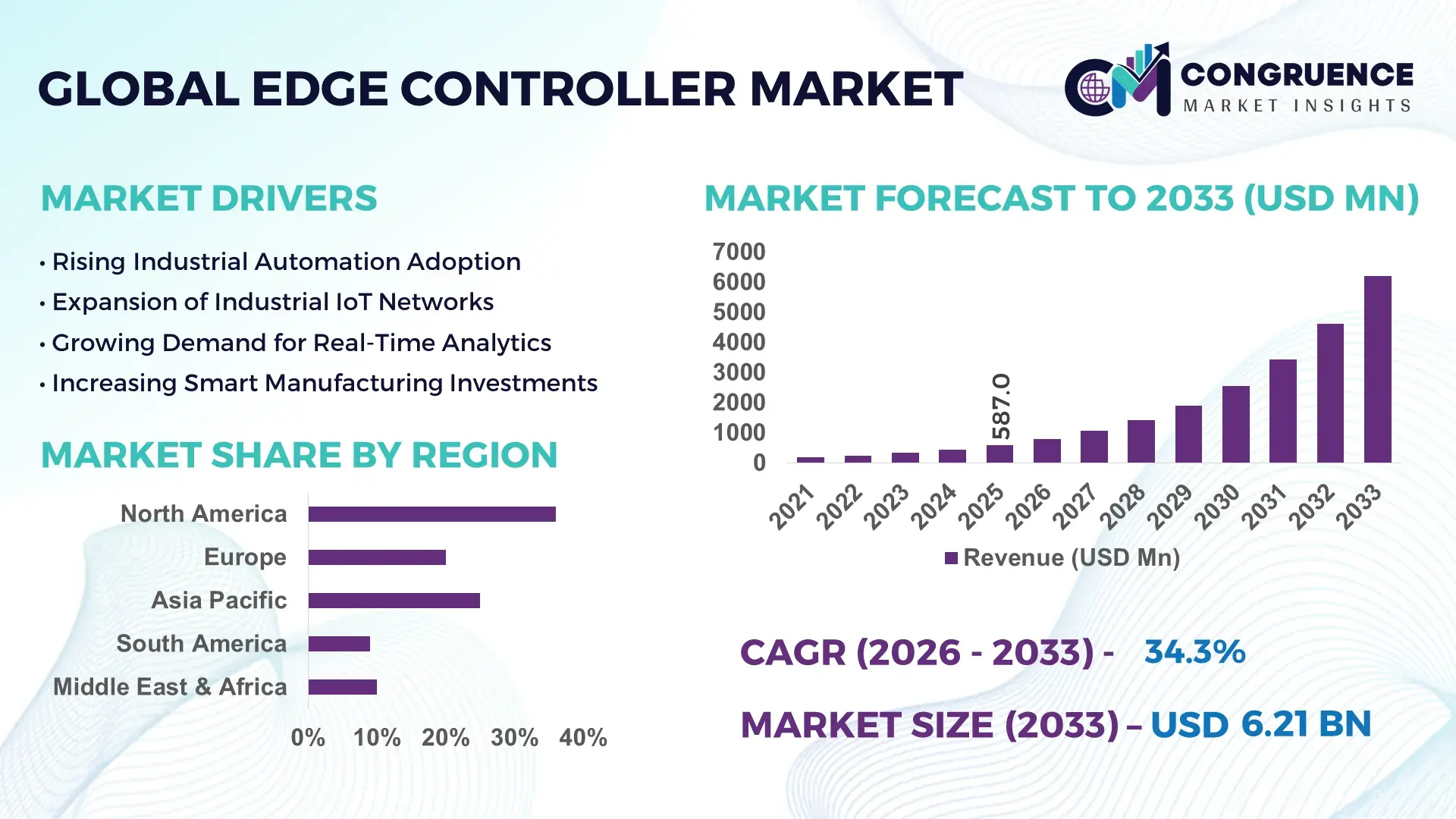

The Global Edge Controller Market was valued at USD 587 Million in 2025 and is anticipated to reach a value of USD 6212.21 Million by 2033 expanding at a CAGR of 34.3% between 2026 and 2033. The market is accelerating as industrial automation networks, distributed energy systems, and AI-enabled manufacturing environments require low-latency edge orchestration capable of processing operational data within milliseconds.

The United States dominates the global edge controller market with nearly 34% share, supported by over USD 9 billion in industrial automation and edge infrastructure investments across automotive, aerospace, semiconductor, and energy sectors during 2025–2026. More than 62% of advanced manufacturing facilities in the country integrated AI-enabled edge control platforms for operational analytics and equipment monitoring, while smart grid modernization projects expanded edge deployment capacity by 26%. Germany follows with strong adoption across precision manufacturing, whereas China leads in high-volume industrial IoT installations linked to electronics and EV battery production ecosystems. Compared with conventional PLC-centered systems, advanced edge controllers deliver up to 40% faster decentralized decision execution in multi-site industrial environments.

Organizations investing early in scalable edge controller ecosystems are securing stronger operational resilience, lower network dependency, and faster industrial intelligence deployment across mission-critical infrastructure.

Market Size & Growth: USD 587 Million in 2025 to USD 6212.21 Million by 2033 at 34.3% growth, driven by industrial AI integration and decentralized automation expansion.

Top Growth Drivers: Smart manufacturing adoption rose 31%, industrial IoT deployment increased 29%, and energy automation integration expanded 24% globally.

Short-Term Forecast: By 2028, edge-enabled production systems reduce latency by 38% and improve operational efficiency by 27% across automated facilities.

Emerging Technologies: AI-enabled edge analytics, containerized industrial software, and TSN-based networking improve controller processing efficiency by over 33%.

Regional Leaders: North America exceeds USD 2.1 Billion with semiconductor automation growth, Europe crosses USD 1.5 Billion through smart factory upgrades, and Asia-Pacific surpasses USD 1.9 Billion via EV manufacturing expansion.

Consumer/End-User Trends: Nearly 58% of industrial operators prioritize edge-native control platforms for predictive maintenance and real-time monitoring.

Pilot/Case Example: In 2025, a smart automotive facility reduced machine downtime by 21% after deploying AI-driven edge controllers across robotic assembly lines.

Competitive Landscape: Top five players control approximately 46% market share, led by advanced automation providers alongside Siemens, ABB, Schneider Electric, Rockwell Automation, and Emerson.

Regulatory & ESG Impact: Industrial energy optimization policies improved power efficiency by 18% in digitally controlled facilities across Europe and East Asia.

Investment & Funding: Global automation and edge infrastructure investments exceeded USD 14 billion in 2025, fueled by strategic manufacturing expansion and supply chain regionalization.

Innovation & Future Outlook: Next-generation software-defined edge controllers and cybersecure industrial platforms accelerate autonomous operations and multi-site orchestration capabilities.

Industrial manufacturing contributes nearly 41% of total edge controller deployment demand, followed by energy and utilities at 24% and transportation automation at 17%. Recent innovation activity centers on AI-assisted edge orchestration, real-time digital twin synchronization, and compact ruggedized controllers optimized for harsh industrial environments. Asia-Pacific continues leading production-scale deployment, while North America drives high-value software-integrated systems. Strengthening cybersecurity regulations and global supply chain diversification are accelerating localized edge infrastructure investment strategies. Advanced software-defined control architectures are expected to redefine industrial responsiveness, enabling faster autonomous decision-making across distributed operational networks.

Edge controllers are becoming strategically critical as manufacturers, utilities, and logistics operators shift toward decentralized operational intelligence to reduce latency, secure industrial data, and stabilize automated workflows. Infrastructure modernization across the United States, Germany, and South Korea is accelerating adoption of edge-native control systems capable of supporting AI-driven industrial coordination. The market is also benefiting from supply-chain restructuring after semiconductor sourcing disruptions pushed enterprises to regionalize automation infrastructure and reduce dependence on centralized cloud processing. More than 57% of large industrial facilities upgraded edge-based monitoring capabilities during 2025 to improve production continuity and predictive maintenance responsiveness.

Advanced edge controllers equipped with AI inference engines process industrial workloads nearly 35% faster than legacy PLC-centered systems while reducing network bandwidth consumption by approximately 28%. Japan leads in high-precision factory integration, whereas China dominates deployment scale through electronics and EV manufacturing ecosystems. A major automotive supplier in Texas recently integrated edge controllers across robotic welding lines, lowering fault-detection time by 24% and improving energy optimization across connected equipment clusters.

Over the next 2–3 years, companies are prioritizing software-defined automation platforms, industrial cybersecurity partnerships, and localized manufacturing agreements to secure long-term operational resilience. Organizations capable of combining edge intelligence, real-time orchestration, and scalable industrial interoperability will strengthen competitive positioning across digitally transformed production ecosystems.

Industrial automation modernization is accelerating edge controller deployment as enterprises prioritize real-time processing, machine synchronization, and autonomous operational control. Nearly 61% of advanced manufacturing facilities in Germany and the United States expanded edge-based industrial monitoring systems during 2025, while AI-enabled controllers reduced production downtime by approximately 22%. The rapid deployment of semiconductor fabs and EV battery plants across South Korea and Texas has intensified demand for low-latency distributed control architectures capable of handling high-volume machine data without centralized cloud dependency. In response, automation vendors are expanding industrial software partnerships and investing in ruggedized edge platforms with integrated cybersecurity layers. A key operational shift involves replacing isolated PLC infrastructures with interoperable edge ecosystems that improve predictive maintenance efficiency and production-line adaptability simultaneously.

Edge controller deployment remains constrained by interoperability fragmentation across legacy industrial systems and ongoing semiconductor component dependency. Nearly 38% of industrial operators report integration delays caused by incompatible communication protocols between older PLC networks and modern edge-native architectures. Japan and Taiwan continue to dominate critical semiconductor supply chains, creating procurement volatility that increased industrial controller lead times by almost 19% during recent electronics manufacturing disruptions. These constraints directly affect deployment scalability, retrofit economics, and operational continuity for mid-sized manufacturers. To reduce exposure, companies are localizing component sourcing, redesigning modular controller architectures, and entering long-term semiconductor procurement agreements. A major strategic challenge involves balancing advanced AI processing requirements with hardware standardization across multi-vendor industrial ecosystems without disrupting existing automation investments.

The transition toward software-defined manufacturing environments is creating substantial opportunities for intelligent edge controller platforms with embedded analytics and adaptive automation capabilities. More than 44% of industrial enterprises in China and the United States are prioritizing containerized edge applications that enable remote updates, predictive diagnostics, and scalable multi-site orchestration. Advanced edge controllers integrated with digital twin frameworks improve asset utilization efficiency by nearly 26% while reducing maintenance scheduling errors by 18%. Governments supporting smart grid modernization and resilient industrial infrastructure are also accelerating adoption of decentralized control technologies. In response, technology providers are expanding industrial AI ecosystems, acquiring cybersecurity firms, and building interoperability alliances with cloud and robotics vendors. A non-obvious opportunity lies in energy-intensive industries using edge controllers to optimize electricity loads and reduce operational power waste across distributed facilities.

As edge controllers become deeply embedded within industrial operations, cybersecurity exposure and deployment complexity are emerging as long-term execution barriers. Nearly 43% of industrial operators identified real-time threat monitoring and secure device authentication as major operational concerns in connected automation environments. The expansion of distributed manufacturing facilities across India, Mexico, and Eastern Europe has increased demand for skilled industrial software engineers capable of managing hybrid edge-cloud infrastructures, yet workforce shortages continue to delay implementation timelines by approximately 17%. Complex integration between operational technology and enterprise IT systems also raises deployment inconsistency risks across multi-site industrial networks. Companies are responding through cyber-resilience investments, workforce training programs, and strategic partnerships with industrial software providers. Long-term competitiveness will depend on building scalable, secure, and interoperable edge ecosystems capable of supporting autonomous industrial decision-making without operational disruption.

AI-Native Edge Processing Expansion Industrial operators are rapidly integrating AI-enabled edge controllers to support real-time analytics and autonomous decision execution inside production environments. More than 52% of smart factories in the United States adopted localized AI inference at the edge during 2025, reducing cloud data transfer loads by nearly 34%. Automotive and semiconductor manufacturers are restructuring operational workflows around low-latency machine orchestration, while vendors are scaling industrial AI partnerships and embedded analytics capabilities to strengthen predictive maintenance precision and production throughput.

Wireless Industrial Infrastructure Adoption Wireless edge controllers are gaining traction as manufacturers modernize brownfield facilities without extensive rewiring costs. Deployment across logistics hubs and warehouse automation sites in Germany increased by 29% during 2025, while installation time dropped nearly 24% compared with wired industrial retrofits. Labor shortages and rising facility upgrade costs are accelerating adoption of industrial Wi-Fi 6 and private 5G architectures. Companies are responding through modular hardware expansion and telecom integration agreements to support scalable distributed automation environments.

Cybersecure Automation Architecture Shift Industrial cybersecurity regulations and operational technology threats are reshaping controller design priorities across energy and manufacturing sectors. Nearly 47% of enterprises expanded zero-trust industrial network frameworks after ransomware attacks disrupted connected operations in 2025. Edge controllers with embedded encryption and secure boot capabilities improved industrial threat detection response time by approximately 31%. Automation suppliers are restructuring product portfolios around cybersecure firmware, remote authentication protocols, and compliance-certified industrial edge ecosystems.

Software-Defined Control Convergence Software-defined automation frameworks are transforming edge controllers from standalone hardware into interoperable orchestration platforms. More than 44% of industrial enterprises in Japan and South Korea shifted toward containerized edge workloads supporting remote updates and adaptive process control. This transition reduced system configuration downtime by 21% and accelerated multi-site deployment consistency across high-volume manufacturing operations. Companies are investing in cloud-edge interoperability partnerships and unified software ecosystems to improve operational scalability while reducing long-term infrastructure complexity.

Industrial Edge Controllers dominate the market with nearly 36% deployment concentration due to superior scalability, ruggedized architecture, and compatibility with high-throughput industrial automation networks. These systems remain heavily utilized across automotive, semiconductor, and energy facilities where real-time processing and low-latency coordination are operationally critical. Programmable Edge Controllers are emerging as the fastest-growing segment, expanding adoption by approximately 27% during 2025 as enterprises prioritize flexible software-defined automation and adaptive workflow management. Compared with conventional embedded systems, programmable platforms improve multi-device orchestration efficiency by nearly 23% in dynamic manufacturing environments. Wireless Edge Controllers are gaining traction across warehouse automation and remote industrial monitoring applications where deployment flexibility reduces retrofit complexity. DIN Rail Edge Controllers maintain strategic relevance in compact industrial installations requiring modular infrastructure integration, while Embedded Edge Controllers continue supporting cost-sensitive machine-level operations. In response, manufacturers are expanding AI-enabled controller portfolios, strengthening interoperability standards, and investing in cybersecure industrial edge ecosystems to capture high-value automation contracts.

Industrial Automation remains the leading application area, accounting for approximately 33% of deployment demand as manufacturers prioritize real-time process optimization, autonomous equipment coordination, and low-latency operational control. Smart Manufacturing is the fastest-growing application segment, with adoption rising nearly 30% during 2025 due to increased integration of AI-assisted production systems and digital twin infrastructure. Facilities deploying edge-enabled manufacturing platforms reported operational downtime reductions of approximately 22% alongside measurable improvements in production scheduling efficiency. Predictive Maintenance is expanding rapidly across semiconductor and automotive plants where edge analytics enable continuous equipment health monitoring and faster anomaly detection. Energy Management applications are strengthening within smart grid modernization projects, while Remote Monitoring adoption is accelerating across logistics and distributed industrial sites. Building Automation continues evolving through intelligent HVAC and occupancy-control integration. Companies are responding through multi-site automation expansion, cloud-edge interoperability investments, and strategic industrial software partnerships supporting scalable decentralized control environments.

Manufacturing represents the dominant end-user segment with nearly 41% of market demand due to extensive deployment across smart factories, robotics systems, semiconductor fabrication, and high-volume assembly operations. Industrial operators increasingly depend on edge controllers for machine synchronization, process analytics, and decentralized operational intelligence. Telecommunications is emerging as the fastest-growing end-user category, expanding adoption by approximately 28% during 2025 as telecom providers accelerate private 5G infrastructure and distributed network management investments. Energy and Utilities continue deploying edge controllers across smart grid modernization programs and decentralized power infrastructure to improve grid responsiveness and outage monitoring efficiency. Oil and Gas companies are integrating ruggedized edge platforms into remote asset monitoring environments, while Transportation operators are deploying intelligent traffic coordination and fleet optimization systems. Healthcare adoption is strengthening through connected facility infrastructure and real-time equipment monitoring. Vendors are responding with sector-specific controller customization, industrial cybersecurity integration, and ecosystem partnerships tailored to mission-critical operational environments.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 37.8% between 2026 and 2033.

Industrial Automation and AI Integration Leadership

North America maintains the highest deployment concentration due to advanced industrial automation infrastructure, semiconductor manufacturing expansion, and strong enterprise adoption of AI-enabled operational technologies. The region contributes nearly 36% of global edge controller deployment activity, supported by large-scale smart factory investments across the United States and Canada. More than 59% of advanced production facilities integrated edge-based predictive maintenance systems during 2025 to improve machine responsiveness and reduce network latency. Industrial cloud-edge interoperability partnerships are accelerating adoption across automotive, aerospace, and energy sectors. Major manufacturers are also expanding localized automation ecosystems following semiconductor supply-chain restructuring and industrial cybersecurity modernization initiatives, strengthening operational resilience across distributed manufacturing environments.

United States Market Outlook: The United States leads the regional market through extensive deployment across semiconductor fabrication plants, EV battery manufacturing facilities, and industrial robotics infrastructure. More than 63% of newly upgraded smart manufacturing sites integrated decentralized edge control platforms during 2025 to improve operational continuity and AI-driven process coordination. Federal infrastructure modernization initiatives and private industrial automation investments are also accelerating deployment of cybersecure industrial edge ecosystems across logistics, aerospace, and utility operations.

Energy-Efficient Smart Factory Transformation

Europe is strengthening its position through energy-efficient manufacturing modernization, industrial sustainability mandates, and widespread adoption of intelligent automation systems. The region accounts for approximately 27% of global deployment activity, with Germany, France, and Italy driving industrial digitalization initiatives. More than 48% of industrial facilities implementing carbon optimization strategies integrated edge-based monitoring and process-control systems during 2025. Regulatory pressure surrounding operational energy efficiency and cybersecure industrial connectivity is accelerating replacement of conventional PLC-centered infrastructure. Companies are increasingly investing in interoperable software-defined automation platforms and industrial AI integration to improve production flexibility while reducing operational energy intensity across manufacturing and utility networks.

Germany Market Outlook: Germany remains the strategic core of Europe’s edge controller market due to its advanced automotive manufacturing ecosystem and precision industrial engineering capabilities. Nearly 58% of large-scale smart factories in the country adopted AI-assisted edge orchestration systems to strengthen machine coordination and predictive maintenance performance. Industrial equipment suppliers are also expanding partnerships with software automation providers to support highly integrated Industry 4.0 production environments across automotive, machinery, and industrial electronics sectors.

Large-Scale Manufacturing Deployment Expansion

Asia-Pacific is emerging as the fastest-expanding market due to rapid industrialization, electronics manufacturing growth, and aggressive smart infrastructure deployment across China, Japan, South Korea, and India. The region represents nearly 32% of global deployment concentration, supported by extensive investments in EV production, semiconductor fabrication, and industrial robotics integration. During 2025, edge-enabled factory automation installations increased by approximately 34% across high-volume manufacturing facilities in East Asia. Governments and industrial enterprises are prioritizing low-latency operational intelligence platforms to improve manufacturing throughput and reduce cloud dependency. Technology providers are expanding regional production facilities, localized controller assembly operations, and industrial AI partnerships to strengthen supply-chain responsiveness and deployment scalability.

China Market Outlook: China dominates the regional landscape through extensive deployment across electronics manufacturing clusters, EV battery production ecosystems, and industrial automation infrastructure. More than 61% of advanced manufacturing facilities integrated edge-native operational analytics systems during 2025 to improve production-line responsiveness and equipment synchronization efficiency. Domestic automation vendors are accelerating software-defined industrial control development while expanding localized semiconductor sourcing to reduce dependency on imported industrial processing hardware.

Industrial Connectivity Modernization Momentum

South America is experiencing rising edge controller adoption through industrial connectivity modernization, mining automation, and utility infrastructure digitization initiatives. Brazil and Chile account for the majority of deployment concentration due to strong investments in industrial energy management and remote operational monitoring systems. Approximately 26% of large industrial facilities upgraded decentralized automation infrastructure during 2025 to improve equipment visibility and reduce maintenance interruptions. However, inconsistent industrial connectivity and limited high-end semiconductor availability continue affecting deployment scalability in some markets. Enterprises are responding through telecom partnerships, localized automation integration services, and phased industrial digitalization strategies focused on operational efficiency and infrastructure optimization.

Brazil Market Outlook: Brazil leads the regional market through expanding deployment across manufacturing, mining, logistics, and utility modernization projects. Industrial enterprises increased investment in edge-enabled monitoring infrastructure by nearly 24% during 2025 to improve operational continuity across geographically distributed facilities. The country’s growing private industrial connectivity ecosystem and ongoing smart energy infrastructure upgrades are strengthening demand for scalable edge control platforms capable of supporting remote asset orchestration and predictive maintenance operations.

Infrastructure Digitalization and Smart Utility Investment

The Middle East & Africa market is expanding through infrastructure modernization, industrial diversification strategies, and smart utility deployment programs led by Gulf economies. The region contributes nearly 9% of global deployment activity, with increasing adoption across energy infrastructure, logistics automation, and smart city ecosystems. During 2025, industrial operators in the Gulf Cooperation Council countries increased deployment of intelligent edge monitoring systems by approximately 28% to strengthen operational visibility and power infrastructure responsiveness. Energy-intensive sectors are prioritizing low-latency decentralized control architectures to improve asset reliability and reduce operational disruptions. Technology vendors are expanding regional partnerships and localized support operations to address infrastructure complexity and industrial cybersecurity requirements.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s most strategically significant market through large-scale industrial diversification programs and smart infrastructure deployment initiatives. More than 42% of newly modernized industrial facilities integrated edge-based operational control systems during 2025 to support energy optimization and predictive asset monitoring. Investments linked to industrial automation, smart logistics corridors, and utility digitalization are strengthening long-term demand for secure, scalable edge controller platforms across critical infrastructure environments.

The market is led by Siemens, ABB, Schneider Electric, Rockwell Automation, Emerson, and Advantech, with the top five players controlling nearly 46% share through industrial automation scale, software ecosystems, and global integration capabilities. Global automation leaders compete against regional industrial hardware suppliers and agile edge-computing innovators focused on lower-cost deployment flexibility. Competition increasingly centers on AI-enabled analytics, cybersecurity integration, interoperability, and deployment speed, with advanced software-defined controllers improving operational response efficiency by 25% compared with conventional PLC-centric systems. Vendors are expanding through industrial cloud partnerships, semiconductor sourcing agreements, and localized manufacturing strategies to reduce lead times by nearly 18%. Technology disruption is shifting competitive power toward companies offering unified cloud-edge orchestration and secure remote device management. High certification requirements, industrial compatibility demands, and embedded software complexity remain major entry barriers. Winning depends on scalable industrial interoperability, cybersecure architecture, and strong ecosystem alignment across automation, telecom, and industrial AI environments.

Siemens

ABB

Schneider Electric

Rockwell Automation

Emerson Electric

Advantech

Beckhoff Automation

Mitsubishi Electric

Honeywell International

Bosch Rexroth

Omron Corporation

WAGO

Phoenix Contact

Yokogawa Electric Corporation

Industrial edge controllers are rapidly evolving from basic automation gateways into AI-enabled orchestration platforms supporting real-time analytics, predictive maintenance, and decentralized operational control. During 2026, nearly 58% of advanced manufacturing facilities integrated AI-assisted edge processing to reduce cloud dependency and improve machine responsiveness. Modern software-defined edge architectures improve industrial workload execution efficiency by approximately 32% compared with legacy PLC-centric systems while reducing network latency by nearly 27%. Companies deploying integrated digital twin synchronization and edge analytics are achieving faster fault detection and stronger production-line adaptability across semiconductor, automotive, and energy operations.

Emerging technologies between 2026 and 2028 include containerized industrial workloads, private 5G-enabled edge networking, and cybersecure OT-IT interoperability frameworks. Wireless edge controller deployment across logistics and warehouse automation environments increased by approximately 29% during 2025–2026 as enterprises prioritized scalable retrofit modernization. AI-enabled edge inference engines are also improving predictive maintenance accuracy by nearly 24%, creating operational advantages for manufacturers managing distributed industrial assets. Automation leaders and semiconductor-integrated vendors benefit most as enterprises shift investment toward localized intelligent processing ecosystems.

Disruptive innovation is accelerating through autonomous industrial AI agents, edge-native cybersecurity layers, and low-power inference hardware optimized for factory environments. Compared with conventional centralized architectures, next-generation edge controllers deliver nearly 40% faster decentralized decision execution and reduce industrial data transfer loads by approximately 35%. Companies acting now are securing competitive advantages through faster automation scalability, resilient industrial orchestration, and reduced operational disruption exposure.

March 2025 – Siemens expanded Siemens Industrial Edge integration with Microsoft Azure IoT Operations, enabling interoperable OT-IT data orchestration and improving machine maintenance responsiveness by 20% across adaptive manufacturing environments. Business impact strengthened industrial AI scalability.

March 2025 – Schneider Electric launched Modicon Edge I/O NTS for distributed industrial data aggregation, supporting production machinery and critical infrastructure applications while reducing industrial installation complexity by nearly 24%. Business impact accelerated scalable smart-factory modernization. Source: Schneider Electric Newsroom

May 2025 – Siemens introduced autonomous industrial AI agents within its Industrial Copilot ecosystem, targeting up to 50% productivity improvement through automated engineering workflows and real-time operational decision execution. Business impact expanded intelligent industrial automation capabilities.

June 2025 – Siemens and NVIDIA expanded their industrial AI partnership to connect NVIDIA accelerated computing with Siemens Xcelerator platforms, strengthening AI-powered manufacturing operations and enabling faster industrial data processing across factory environments. Business impact accelerated AI-driven factory optimization deployment. Source: NVIDIA Investor News

The report delivers comprehensive analysis of industrial edge controller deployment trends across Industrial Edge Controllers, Embedded Edge Controllers, Programmable Edge Controllers, Wireless Edge Controllers, and DIN Rail Edge Controllers. It evaluates operational demand patterns across Industrial Automation, Smart Manufacturing, Energy Management, Remote Monitoring, Predictive Maintenance, and Building Automation applications while assessing adoption across Manufacturing, Telecommunications, Healthcare, Transportation, Energy and Utilities, and Oil and Gas sectors. More than 40% of deployment concentration remains tied to advanced manufacturing and industrial AI integration initiatives between 2026 and 2033.

Regional analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, industrial digitization, and decentralized operational intelligence deployment. The report also examines software-defined automation, AI-enabled edge orchestration, private 5G integration, cybersecurity frameworks, and cloud-edge interoperability trends shaping enterprise investment priorities. Strategic insights support expansion planning, technology positioning, partnership evaluation, competitive benchmarking, and long-term industrial automation decision-making across rapidly evolving smart infrastructure ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 587 Million |

|

Market Revenue in 2033 |

USD 6212.21 Million |

|

CAGR (2026 - 2033) |

34.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, ABB, Schneider Electric, Rockwell Automation, Emerson Electric, Advantech, Beckhoff Automation, Mitsubishi Electric, Honeywell International, Bosch Rexroth, Omron Corporation, WAGO, Phoenix Contact, Yokogawa Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |