Reports

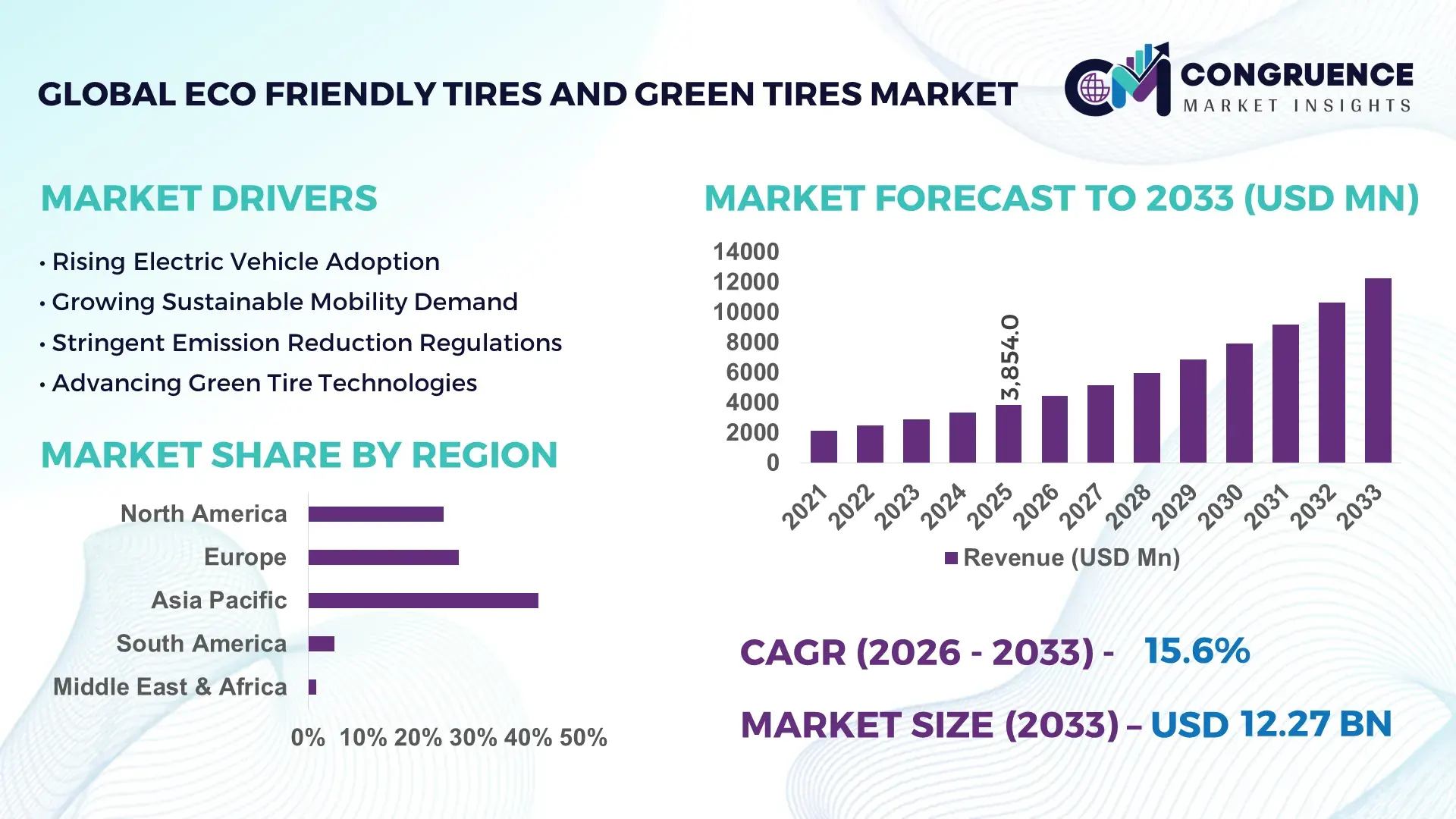

The Global Eco Friendly Tires and Green Tires Market was valued at USD 3,854.0 Million in 2025 and is anticipated to reach a value of USD 12,273.6 Million by 2033 expanding at a CAGR of 15.58% between 2026 and 2033. Growth is being propelled by accelerated adoption of silica-based low rolling resistance compounds, rising sustainable material integration, and stricter vehicle emission compliance standards across automotive manufacturing hubs.

China remains the dominant country in the market, accounting for approximately 34% of global green tire production capacity, supported by investments exceeding USD 2.5 billion in advanced tire manufacturing facilities and sustainable material processing. The country produces over 30 million eco-friendly tire units annually, compared with Germany’s estimated 9 million units, while achieving up to 20% higher adoption of silica-enhanced tread technologies. Growing electric vehicle production and supply-chain localization initiatives following global trade realignments continue strengthening China's leadership position.

The concentration of manufacturing capacity, sustainable raw-material sourcing, and advanced tire technology deployment is reshaping competitive positioning and long-term investment priorities across the industry.

Market Size & Growth: USD 3,854.0 Million in 2025 reaching USD 12,273.6 Million by 2033, driven by low rolling resistance technology, sustainable materials adoption, and EV-focused tire engineering.

Top Growth Drivers: Rolling resistance reduction of up to 30%, recycled-material utilization exceeding 25%, and EV tire demand growth above 20% in key automotive markets.

Short-Term Forecast: By 2028, advanced tread compounds are expected to improve fuel efficiency by 6–8% while reducing tire wear rates by nearly 12%.

Emerging Technologies: AI-enabled tire design, bio-based elastomers, smart sensor integration, and advanced silica reinforcement are accelerating product performance improvements.

Regional Leaders: Asia Pacific exceeds USD 5.0 Billion potential supported by EV expansion, Europe approaches USD 3.0 Billion through sustainability mandates, and North America surpasses USD 2.4 Billion through fleet electrification initiatives.

Consumer/End-User Trends: More than 40% of EV owners prioritize low rolling resistance tires to maximize vehicle driving range and operating efficiency.

Pilot/Case Example: In 2024, advanced silica-compound deployment reduced rolling resistance by nearly 15% and improved fuel economy performance by approximately 4%.

Competitive Landscape: Leading manufacturers collectively control over 45% of market activity, with Michelin, Bridgestone, Goodyear, Continental, and Pirelli driving innovation.

Regulatory & ESG Impact: Vehicle emission regulations have increased demand for eco-efficient tire technologies by more than 18% across major automotive economies.

Investment & Funding: Industry investments surpassed USD 4.0 Billion in sustainable tire materials, manufacturing modernization, and strategic supply-chain expansion projects.

Innovation & Future Outlook: Bio-sourced rubber, circular-economy tire recovery systems, and digital performance monitoring are becoming core competitive differentiators.

Eco Friendly Tires and Green Tires represent a rapidly evolving segment of the automotive value chain, with strong demand emerging from passenger EVs, commercial fleets, and premium mobility applications. Manufacturers are accelerating the use of renewable materials, recycled carbon black, and advanced silica compounds that can lower rolling resistance by nearly 20%. Increasing regulatory scrutiny of vehicle emissions and supply-chain sustainability is also encouraging next-generation tire development, creating a foundation for broader strategic transformation across the sector.

Eco Friendly Tires and Green Tires are becoming strategically important as automotive manufacturers, fleet operators, and tire producers compete on efficiency, sustainability, and lifecycle performance rather than solely on durability. The market is increasingly influenced by supply-chain restructuring, localized sourcing strategies, and stricter environmental compliance frameworks. Manufacturers are integrating renewable feedstocks, recycled materials, and advanced compound technologies to strengthen competitive differentiation and reduce exposure to raw-material volatility.

Advanced silica-based tire compounds can lower rolling resistance by approximately 20–30% compared with conventional tire formulations, delivering measurable gains in fuel economy and electric vehicle range. China continues to lead large-scale production and manufacturing investments, while Germany and Japan remain innovation-focused hubs with higher penetration of sustainable tire technologies. Adoption rates within electric vehicle platforms are growing substantially faster than traditional vehicle segments, creating new opportunities for premium product positioning.

Companies are expanding partnerships with chemical suppliers, recycling firms, and automotive OEMs to secure sustainable material streams and accelerate commercialization. Several leading manufacturers have committed to increasing renewable and recycled content beyond 40% in selected product lines within the next few years. Organizations that successfully combine sustainable sourcing, advanced material science, and production scalability will secure stronger market positioning, operational resilience, and long-term competitive advantage.

Automotive manufacturers are aggressively adopting low-rolling-resistance tire technologies as fuel-efficiency and vehicle-range optimization become core purchasing criteria. Advanced silica compounds can reduce rolling resistance by up to 30%, while selected sustainable-material platforms now incorporate more than 25% renewable or recycled content. China, Japan, and Germany are expanding production capacity for specialized compounds and eco-engineered tire platforms to support next-generation mobility requirements. Stricter vehicle efficiency regulations and growing EV production volumes are creating a direct demand pull for green tire solutions. In response, leading manufacturers are investing in sustainable-material partnerships, dedicated production lines, and advanced R&D programs. A notable strategic outcome is that tire performance and sustainability metrics are increasingly influencing OEM sourcing decisions, elevating green tires from a compliance product to a competitive differentiation tool.

The market continues to face structural pressure from fluctuating prices of natural rubber, specialty silica, and sustainable feedstock materials. Sustainable compounds can increase manufacturing costs by approximately 10–20% compared with conventional formulations, while imported specialty materials expose producers to supply disruptions and logistics constraints. Thailand and Indonesia remain critical natural-rubber suppliers, creating concentration risk across the value chain. Shipping disruptions and procurement uncertainties have increased inventory management complexity for tire manufacturers. To reduce exposure, companies are diversifying sourcing networks, investing in regional supply hubs, and negotiating long-term procurement agreements. A key operational challenge remains balancing sustainability targets with cost competitiveness, particularly in price-sensitive vehicle segments where premium pricing flexibility remains limited.

The strongest long-term opportunity lies in circular manufacturing ecosystems and next-generation material innovation. Several manufacturers are targeting recycled and renewable content levels exceeding 40% in future product portfolios, while recovered carbon black technologies can reduce dependence on virgin petrochemical inputs by nearly 20%. India and China are emerging as strategic hubs for tire recycling infrastructure and sustainable-material processing. New bio-based elastomers, advanced recycling technologies, and digital material-tracking systems are improving resource efficiency across the production cycle. Companies are expanding R&D collaborations with chemical firms, research institutes, and mobility providers to accelerate commercialization. An important strategic insight is that ownership of circular-material supply chains is evolving into a competitive advantage comparable to traditional manufacturing scale and distribution reach.

Achieving large-scale deployment while maintaining durability, traction, safety, and cost efficiency remains a significant execution challenge. Sustainable-material integration above 40% often requires extensive product validation and manufacturing adjustments, increasing development timelines. Premium eco-friendly tire designs can involve testing cycles that are 15–25% longer than conventional alternatives due to performance verification requirements. Germany, Japan, and the United States continue investing heavily in advanced testing and material engineering capabilities to overcome these limitations. Companies must also address production consistency, recycling quality standards, and evolving environmental regulations. The organizations that successfully industrialize sustainable tire technologies without sacrificing performance metrics will strengthen long-term competitiveness and establish leadership positions in the next generation of automotive mobility solutions.

Advanced Sustainable Material Integration Tire manufacturers are increasing the use of recycled and renewable inputs, with sustainable material content reaching 25–35% in several premium product lines. Adoption of recycled carbon black has expanded by nearly 20%, while bio-based elastomer deployment has increased more than 15% across new product launches. Regulatory pressure on lifecycle emissions and raw-material traceability is accelerating material substitution strategies. Companies are responding through long-term supplier partnerships, dedicated recycling agreements, and localized procurement networks that improve supply security while reducing dependency on petrochemical feedstocks.

EV-Specific Tire Platform Expansion Electric vehicle tire programs are becoming a dedicated product category rather than an extension of conventional portfolios. EV-focused tire launches increased by more than 30% over the past two years, while low-noise tread technologies improved cabin noise reduction by approximately 10–15%. Higher battery weights and torque delivery requirements are driving specialized compound and sidewall engineering. Manufacturers are expanding EV-centered R&D centers and co-development partnerships with automotive OEMs to improve vehicle range, durability, and performance consistency.

Digital Manufacturing Optimization Smart manufacturing adoption continues to accelerate, with automated quality inspection systems improving defect detection rates by nearly 25% and reducing production variability by more than 15%. AI-enabled process controls are shortening production adjustment cycles and improving material utilization efficiency. Labor availability constraints and operational cost pressures are encouraging tire producers in China, Germany, and Japan to scale digital factory initiatives. The result is faster production ramp-up, lower waste generation, and stronger operational resilience.

Circular Tire Recovery Ecosystems Tire manufacturers are increasingly moving beyond product sales toward circular recovery models. Recovery and recycling rates have improved by approximately 12–18% across several developed markets, supported by stricter waste-management frameworks and extended producer responsibility programs. A notable shift is the growing integration of recovered materials directly into new production workflows rather than secondary industrial uses. Companies are investing in recycling infrastructure, reverse logistics partnerships, and closed-loop processing systems to strengthen material security and reduce exposure to raw-material price volatility.

Low Rolling Resistance Tires represent the leading segment, accounting for an estimated 42% of total market demand in 2025. Their dominance stems from measurable fuel-efficiency gains, compatibility with both internal combustion and electric vehicles, and straightforward integration into existing vehicle platforms. Fleet operators increasingly prioritize these tires because rolling resistance reductions of 20–30% can translate into lower operating costs and improved energy efficiency. Manufacturers are expanding silica-compound production and advanced tread engineering programs to strengthen performance differentiation and secure OEM contracts. Recycled Material Tires are emerging as the fastest-growing segment as sustainability targets become embedded across automotive supply chains. Several manufacturers have increased recycled and renewable content levels beyond 25% in selected product lines, while procurement teams increasingly evaluate tire suppliers based on lifecycle environmental performance. Radial Tires continue to hold strategic relevance due to superior durability and handling characteristics, particularly in passenger vehicles, whereas Bias Tires maintain niche demand in specialized industrial and off-road applications. Investment priorities are steadily shifting toward material innovation, circular manufacturing, and low-emission mobility solutions that align with evolving vehicle efficiency requirements.

Passenger Vehicles constitute the largest application segment, contributing approximately 55% of overall demand due to high replacement cycles, large global vehicle populations, and increasing consumer focus on fuel efficiency. Eco-friendly tire adoption within passenger cars has accelerated as vehicle owners seek improved mileage and lower environmental impact. OEMs are incorporating low rolling resistance tires into standard vehicle configurations, while premium automotive brands continue introducing sustainability-focused tire specifications. This concentration of demand supports large-scale production economics and continuous product innovation. Electric Vehicles represent the fastest-growing application area as manufacturers develop specialized tires capable of handling higher battery weight and instant torque delivery. EV-specific tire deployments have increased by more than 25% across new vehicle launches, driving demand for advanced compounds and noise-reduction technologies. Commercial Vehicles remain a strategically important segment because fleet operators prioritize operating-cost reductions and tire longevity, while Industrial Vehicles continue adopting eco-friendly tire solutions in targeted applications where sustainability requirements are becoming procurement criteria. Tire producers are responding through dedicated EV product portfolios, OEM partnerships, and digital performance monitoring capabilities.

OEMs remain the dominant end-user segment, accounting for nearly 60% of demand due to large-scale vehicle production programs and growing incorporation of sustainability metrics into supplier qualification processes. Vehicle manufacturers increasingly require tires that support emissions reduction objectives, energy-efficiency targets, and lifecycle performance benchmarks. Long-term supply agreements and platform-wide procurement strategies provide OEMs with substantial influence over product specifications, encouraging tire manufacturers to invest in advanced compounds, lightweight construction, and sustainable material sourcing. Fleet Operators are emerging as the fastest-growing end-user group as transportation companies focus on reducing operating expenses and improving sustainability performance. Fuel-consumption improvements of 5–8% achieved through low rolling resistance technologies are creating measurable economic incentives for large commercial fleets. The Aftermarket segment continues to benefit from rising consumer awareness regarding environmental performance and total cost of ownership, while Government & Public Transport organizations are increasingly incorporating sustainability criteria into procurement frameworks. Companies are tailoring pricing models, service offerings, and performance guarantees to strengthen penetration across these high-value customer groups.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.4% between 2026 and 2033.

North America accounted for approximately 24.6% of the global market in 2025, supported by rapid electric vehicle adoption, fleet sustainability programs, and increasing deployment of low rolling resistance tire technologies. Commercial fleet operators are accelerating replacement cycles to improve operating efficiency, while automotive OEMs are incorporating eco-friendly tires into factory-fitted vehicle platforms. More than 35% of newly launched EV models in the region now feature tires optimized for range enhancement and noise reduction. Tire manufacturers are expanding domestic production capacity and strengthening partnerships with recycling and advanced-material suppliers to secure sustainable feedstock availability. The market is increasingly influenced by lifecycle performance metrics and environmental procurement standards.

United States Market Outlook: The United States remains the regional growth engine due to its large automotive manufacturing base, extensive transportation network, and strong EV deployment activity. More than 15 million commercial trucks operate nationwide, creating significant demand for fuel-efficient tire solutions. Leading tire manufacturers are investing in advanced production facilities and sustainable-material programs, while fleet operators increasingly evaluate tire performance using total cost of ownership metrics. Federal sustainability initiatives and growing corporate decarbonization commitments continue supporting adoption across passenger and commercial vehicle segments.

Europe represented nearly 27.3% of global market demand in 2025, driven by strict environmental regulations, advanced recycling infrastructure, and strong automotive technology capabilities. The region has emerged as a leader in sustainable tire development, with manufacturers increasing recycled and renewable material content across premium product portfolios. More than 30% of sustainability-focused tire innovations introduced globally originate from European production and R&D networks. Regulatory emphasis on carbon reduction and circular manufacturing is encouraging investment in closed-loop recycling systems and advanced material recovery technologies. Automotive OEMs are increasingly integrating eco-friendly tire requirements into vehicle development programs.

Germany Market Outlook: Germany maintains a strategic leadership position through its concentration of automotive manufacturers, engineering expertise, and advanced tire technology research. The country accounts for a significant share of Europe's premium vehicle production, creating sustained demand for high-performance sustainable tire solutions. German manufacturers continue investing in smart manufacturing systems, material science innovation, and tire recycling initiatives. Strong collaboration between automotive OEMs, chemical companies, and research institutions is accelerating commercialization of next-generation tire technologies with improved efficiency and sustainability characteristics.

Asia-Pacific leads the global market with approximately 41.8% share, supported by large-scale tire manufacturing capacity, expanding vehicle production, and increasing adoption of sustainable mobility solutions. The region produces more than half of global tire output and serves as a critical export hub for international automotive supply chains. Investments in advanced manufacturing, automated production lines, and sustainable material processing continue expanding operational capacity. Electric vehicle production growth and localized raw-material availability further strengthen market competitiveness. Manufacturers are scaling green tire portfolios while improving production efficiency through digital factory modernization and supply-chain integration initiatives.

China Market Outlook: China dominates regional activity through its extensive tire manufacturing ecosystem, integrated supply chains, and large electric vehicle market. The country accounts for roughly one-third of global green tire production capacity and continues expanding investments in sustainable manufacturing technologies. More than 30 million eco-friendly tire units are estimated to be produced annually, supported by advanced silica-compound deployment and growing use of recycled materials. Strong government support for EV adoption and industrial modernization reinforces China's position as the primary production and innovation hub within the sector.

South America accounted for approximately 4.8% of global demand in 2025, with adoption increasingly supported by automotive manufacturing modernization and fleet-efficiency initiatives. Regional demand is concentrated in passenger vehicles and commercial transportation sectors seeking lower fuel consumption and improved operational performance. Tire manufacturers are strengthening local distribution networks and expanding access to sustainability-focused product offerings. Infrastructure limitations and economic variability continue influencing deployment rates, yet growing investment in industrial modernization is creating favorable conditions for adoption. Partnerships between regional distributors and international manufacturers are helping improve product availability and technology transfer across key markets.

Brazil Market Outlook: Brazil serves as the largest automotive and tire manufacturing center in South America, supported by extensive vehicle production activity and a well-established industrial base. The country accounts for more than 50% of regional automotive output, creating substantial replacement and OEM demand. Fleet operators are increasingly adopting fuel-efficient tire technologies to reduce logistics costs, while domestic manufacturers continue upgrading production facilities. Expanding sustainability initiatives and growing awareness of lifecycle operating costs are strengthening long-term market potential across both passenger and commercial vehicle categories.

The Middle East & Africa region accounted for approximately 1.5% of global market activity in 2025, supported by transportation infrastructure investments, expanding vehicle fleets, and increasing sustainability awareness. Demand growth is concentrated around logistics, construction, and commercial transportation applications where operating efficiency is becoming a strategic priority. Several countries are integrating sustainability targets into industrial development programs, encouraging adoption of advanced mobility technologies. Tire suppliers are expanding regional partnerships and distribution capabilities to improve market access. Modernization of transportation networks and logistics corridors is gradually strengthening the business case for eco-friendly tire deployment.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market in the region due to large-scale infrastructure development, logistics expansion, and industrial diversification initiatives. Transportation and construction activity continue driving demand for advanced tire technologies capable of supporting intensive operating conditions. The country is investing heavily in mobility infrastructure and supply-chain modernization projects, creating opportunities for sustainable tire adoption. Growing emphasis on efficiency, fleet optimization, and industrial sustainability is encouraging international tire manufacturers to strengthen partnerships and distribution networks within the Kingdom.

The Eco Friendly Tires and Green Tires Market is led by global manufacturers including Michelin, Bridgestone, Goodyear, Continental, and Pirelli, which collectively control approximately 55–60% of global market activity. Competition primarily occurs between global technology leaders and regional cost-focused manufacturers, while OEM-focused suppliers compete against aftermarket specialists for long-term vehicle platform contracts. The basis of competition has shifted toward sustainable-material content, rolling-resistance reduction, and EV-specific performance, with premium green tire products delivering up to 20% lower rolling resistance and 10–15% longer operational life. Companies are expanding recycling partnerships, securing renewable feedstock supply chains, and vertically integrating material sourcing operations. The competitive landscape is increasingly influenced by circular-economy capabilities and advanced compound technologies rather than manufacturing scale alone. High R&D requirements and sustainable-material procurement complexity remain major barriers. Success depends on combining material innovation, supply-chain control, and OEM integration.

Continental AG

Pirelli & C. S.p.A.

Yokohama Rubber Company

Sumitomo Rubber Industries

Hankook Tire & Technology

Nokian Tyres

Toyo Tire Corporation

Kumho Tire

Apollo Tyres

CEAT Limited

Sustainable material engineering remains the most influential technology segment. Manufacturers are replacing conventional petroleum-derived inputs with recycled carbon black, bio-based oils, renewable rubber compounds, and recycled polyester reinforcement materials. Sustainable material content has reached 25–30% in several commercial tire platforms, while selected premium products exceed 50%. Compared with traditional tire formulations, advanced silica-based compounds can reduce rolling resistance by up to 30%, directly improving vehicle efficiency and extending electric vehicle driving range. Premium manufacturers benefit most because material innovation strengthens OEM relationships and product differentiation.

Digital tire technologies are rapidly expanding through embedded sensors, intelligent tire monitoring, and AI-assisted design optimization. Smart tire systems improve predictive maintenance accuracy by approximately 15–20% while reducing unexpected fleet downtime. More than one-third of newly developed EV-focused tire platforms now incorporate digital performance optimization during development. AI-driven simulation tools are also shortening product development cycles and improving compound performance validation, creating operational advantages in speed-to-market and engineering efficiency.

Between 2026 and 2028, circular manufacturing technologies will become a major competitive differentiator. Advanced recycling systems, recovered carbon black integration, and closed-loop material recovery models are expected to improve raw-material utilization by 15–20% compared with conventional supply chains. Companies investing early in sustainable feedstock ecosystems, digital manufacturing, and intelligent tire technologies will secure stronger OEM partnerships, greater supply resilience, and long-term competitive positioning.

July 2024 – Continental AG signed a 10-year agreement with Pyrum Innovations to secure recovered carbon black from end-of-life tires for future series production. The initiative supports a target of more than 40% renewable and recycled material content, strengthening circular-economy integration and raw-material security. Source: www.continental.com

August 2024 – Goodyear Tire & Rubber Company announced a C$575 million modernization and expansion project at its Ontario facility, adding capacity for EV-focused tire production and creating 200 jobs. The investment enhances North American manufacturing competitiveness and supports long-term sustainability objectives.

March 2025 – Continental AG received the Sustainability Award in Automotive 2025 for its UltraContact NXT tire, containing up to 65% renewable, recycled, and certified materials. The achievement demonstrates commercial viability of high-sustainability tire platforms without compromising performance standards.

June 2025 – Continental AG announced plans to increase renewable and recycled material usage by an additional 2–3 percentage points during 2025, building on a 26% average achieved in 2024. The move accelerates sustainable manufacturing adoption and strengthens competitive differentiation in green mobility markets.

The report provides comprehensive analysis of the Eco Friendly Tires and Green Tires Market across key product categories, applications, end-user groups, and major geographic regions. Coverage includes Low Rolling Resistance Tires, Recycled Material Tires, Radial Tires, and Bias Tires, alongside assessment of passenger vehicles, commercial vehicles, electric vehicles, and industrial vehicle applications. The study evaluates adoption patterns, deployment trends, sustainable-material integration, and technology innovation influencing market evolution between 2026 and 2033.

The analysis further examines OEM procurement strategies, aftermarket demand dynamics, fleet operator adoption, and government transportation initiatives. More than 55% of market activity remains concentrated among leading global manufacturers, making competitive positioning, supply-chain control, and material innovation critical strategic variables. The report also evaluates emerging technologies including smart tires, circular manufacturing systems, advanced silica compounds, and recycled-material platforms. Strategic insights support investment planning, market entry decisions, product development priorities, partnership opportunities, and long-term expansion strategies across established and emerging mobility ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,854.0 Million |

| Market Revenue (2033) | USD 12,273.6 Million |

| CAGR (2026–2033) | 15.58% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Michelin; Bridgestone Corporation; Goodyear Tire & Rubber Company; Continental AG; Pirelli & C. S.p.A.; Yokohama Rubber Company; Sumitomo Rubber Industries; Hankook Tire & Technology; Nokian Tyres; Toyo Tire Corporation; Kumho Tire; Apollo Tyres; CEAT Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |