Reports

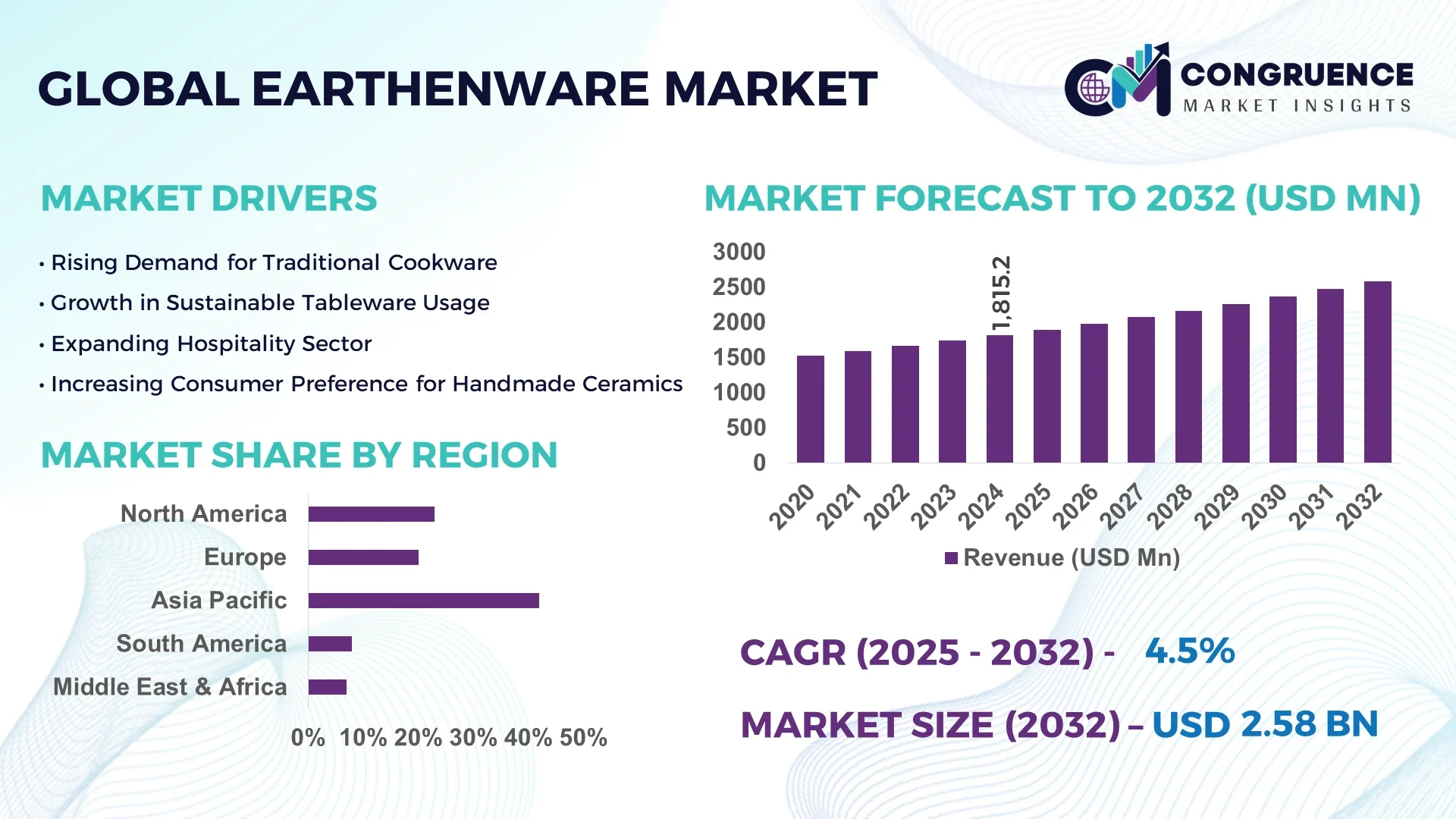

The Global Earthenware Market was valued at USD 1815.16 Million in 2024 and is anticipated to reach a value of USD 2581.34 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China stands as a leading player in the global Earthenware market, boasting a substantial production capacity fueled by significant investments in automated manufacturing facilities. The country’s strategic focus on integrating traditional craftsmanship with modern technological advancements has enhanced the quality and durability of earthenware products, catering to both domestic and international demand. Key industrial applications in China include home décor, cookware, and sanitary ware, supported by a growing middle-class consumer base and expanding export channels.

The Earthenware market encompasses diverse industry sectors such as household ceramics, construction materials, and artisanal goods, each contributing significantly to the overall market revenue. Recent technological innovations, including advanced kiln firing techniques and eco-friendly glazing processes, have enhanced product sustainability and performance. Regulatory frameworks emphasizing environmental protection and resource efficiency are shaping manufacturing practices, while economic drivers like rising disposable incomes and urbanization stimulate demand in emerging regions. Regional consumption patterns reveal strong growth in Asia-Pacific and Latin America, driven by cultural affinity for earthenware products and increasing adoption in modern lifestyle applications. Emerging trends include the fusion of traditional designs with contemporary aesthetics and the use of digital platforms for marketing and distribution, positioning the market for steady expansion in the coming years.

Artificial Intelligence (AI) is reshaping the Earthenware Market by revolutionizing production processes, quality control, and supply chain management. AI-powered systems enable precise monitoring and optimization of kiln temperatures and firing cycles, significantly reducing energy consumption and minimizing defects in finished products. This technological integration improves operational efficiency and product consistency, which are critical factors for manufacturers competing in global markets. In addition, AI algorithms analyze raw material quality and composition, allowing for better control of clay mixtures and glaze formulations that enhance durability and aesthetic appeal.

Furthermore, the Earthenware Market benefits from AI-driven predictive maintenance tools that reduce downtime of critical manufacturing equipment by forecasting potential failures before they occur. This reduces operational costs and improves production timelines. AI also facilitates demand forecasting and inventory management by analyzing consumer trends and purchasing patterns, enabling manufacturers and retailers to align supply with market needs more effectively. Digital platforms enhanced with AI-powered customer insights improve targeted marketing strategies, contributing to increased sales and brand loyalty. Collectively, these AI applications are modernizing the Earthenware Market, fostering innovation, and driving competitive advantages for industry stakeholders while supporting sustainable manufacturing practices.

“In early 2024, a leading ceramics manufacturer implemented an AI-based kiln monitoring system that reduced energy usage by 15% and improved product defect rates by 12%, marking a significant efficiency breakthrough in the Earthenware Market.”

The increasing consumer focus on sustainability is a significant driver in the Earthenware Market. Eco-conscious buyers prefer earthenware products due to their biodegradable and natural composition, boosting demand in household and commercial applications. Manufacturers are investing in environmentally friendly production methods, such as low-energy kilns and non-toxic glazing techniques, to meet regulatory standards and customer expectations. This shift towards sustainable manufacturing has also led to innovation in product design and material sourcing, enhancing market appeal. Data indicates that eco-friendly ceramics account for a growing segment of total earthenware sales, reflecting consumer trends toward green living and ethical consumption.

Despite growth opportunities, the Earthenware Market faces significant restraints due to rising production costs, particularly related to raw materials like high-quality clay and glazing agents. Supply chain disruptions and price volatility in these inputs can increase manufacturing expenses, reducing profit margins for producers. Additionally, energy-intensive kiln operations contribute to overall costs, especially in regions with high electricity prices. Regulatory compliance related to environmental emissions and waste disposal also imposes financial burdens on manufacturers. These factors collectively challenge small and medium enterprises, limiting market entry and expansion capabilities in some regions.

Emerging economies in Asia-Pacific, Latin America, and Africa present substantial growth opportunities for the Earthenware Market due to strong cultural ties and traditional uses of earthenware in cooking, storage, and décor. Rising disposable incomes and urban lifestyle shifts are encouraging adoption of modern designs and multifunctional earthenware products. Additionally, digital commerce platforms are enabling wider reach to consumers in these regions, providing manufacturers with new sales channels. Investment in localized production facilities and innovation tailored to regional preferences can unlock untapped demand, creating a strategic advantage for companies targeting these growth markets.

The Earthenware Market is increasingly challenged by tightening environmental regulations aimed at reducing carbon emissions, hazardous waste, and water usage in ceramic production. Compliance with these standards requires costly upgrades to manufacturing facilities and adoption of cleaner technologies, which may not be financially feasible for smaller producers. Additionally, lengthy approval processes and frequent regulatory changes create uncertainty and operational delays. These challenges can hinder production scalability and slow new product launches. Companies must balance innovation with sustainability mandates while managing the financial and logistical complexities of regulatory adherence.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction techniques is significantly reshaping demand dynamics in the Earthenware Market. Prefabricated earthenware elements, such as tiles and decorative panels, are increasingly manufactured off-site with advanced automation, enhancing precision and reducing labor costs. This trend is especially prominent in Europe and North America, where the construction industry prioritizes faster project completion and cost-efficiency. Manufacturers investing in high-precision cutting and molding machines are experiencing stronger order pipelines, reflecting growing acceptance of modular earthenware components in both residential and commercial building sectors.

• Increasing Use of Eco-Friendly Glazing Technologies: There is a marked increase in the adoption of environmentally sustainable glazing processes within the Earthenware Market. Innovations in low-VOC (volatile organic compounds) and lead-free glazes have allowed manufacturers to meet stringent environmental regulations while maintaining product durability and aesthetic appeal. This trend is accelerating in regions with heightened regulatory scrutiny, such as the European Union and parts of Asia-Pacific, where consumers and policymakers alike demand greener product alternatives.

• Integration of Smart Manufacturing Systems: Smart manufacturing technologies, including IoT sensors and AI-driven process control, are gaining traction among earthenware producers. These technologies enable real-time monitoring of kiln conditions and raw material quality, reducing waste and improving product uniformity. Facilities that have integrated these digital tools report up to 20% improvements in operational efficiency and a significant reduction in production defects, providing a competitive advantage in highly demanding markets.

• Growing Demand for Custom and Artisanal Designs: Consumer preference is shifting toward customized and artisanal earthenware products that blend traditional craftsmanship with contemporary aesthetics. This trend is particularly strong in luxury home décor and boutique hospitality sectors. Manufacturers offering bespoke design services and limited-edition collections are capturing niche markets, leveraging digital design tools and 3D printing to accelerate prototyping and production, which helps meet personalized consumer demands more effectively.

The Earthenware Market is segmented primarily by product types, applications, and end-user categories, each playing a critical role in shaping industry dynamics. Product segmentation includes various forms such as tableware, decorative items, and construction materials, reflecting diverse consumer needs and manufacturing specializations. Application-wise, the market serves sectors including household use, architectural and construction projects, and hospitality industries, highlighting the versatility of earthenware products. End-user insights reveal a broad customer base spanning residential consumers, commercial enterprises, and artisanal craftsmen, with varying demands influencing product innovation and distribution strategies. This segmentation provides decision-makers with a nuanced understanding of market drivers and opportunities across different verticals.

The Earthenware Market includes several product types such as tableware, tiles, sanitary ware, decorative items, and cookware. Tableware remains the leading type due to its widespread use in both domestic and commercial settings, supported by continuous innovation in design and durability that appeals to modern consumers. The fastest-growing segment is earthenware tiles, propelled by increasing adoption in interior design and sustainable construction projects, especially in urban regions seeking eco-friendly building materials. Sanitary ware, though a smaller segment, is gaining traction in developing markets due to rising infrastructure investments and hygiene awareness. Decorative earthenware items, including vases and art pieces, hold niche relevance driven by rising demand for artisanal and culturally inspired home décor. Cookware also remains an essential segment, favored for its heat retention and non-toxic properties, particularly in traditional culinary applications.

Applications of earthenware products are diverse, with household use dominating the market owing to the functional and aesthetic appeal of items such as tableware and cookware. This segment benefits from growing consumer interest in natural and handmade kitchenware. The fastest-growing application is in the construction sector, particularly in eco-friendly and modular building projects, where earthenware tiles and bricks are favored for their thermal insulation and sustainability attributes. The hospitality industry also represents a significant application area, utilizing earthenware for decorative and practical purposes in restaurants and hotels that emphasize authentic and rustic ambiance. Additionally, artisanal crafts and giftware sectors contribute to the market by catering to consumers seeking unique, handcrafted products.

Residential consumers constitute the leading end-user segment for the Earthenware Market, driven by increasing awareness of health-conscious, sustainable household products. These users favor earthenware for its natural materials and traditional appeal, enhancing kitchen and dining experiences. The fastest-growing end-user group is the commercial sector, including restaurants, hotels, and interior designers who integrate earthenware products to enhance ambiance and sustainability credentials. Artisans and small-scale producers also form an important segment, using earthenware for crafting bespoke items and cultural artifacts. Additionally, construction companies are increasingly incorporating earthenware materials into projects, expanding the market’s reach into infrastructure and architectural domains.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, Africa is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific’s dominance is driven by extensive manufacturing capabilities, high domestic consumption, and strong infrastructure investments in countries like China and India. The region benefits from growing urbanization and industrialization, fueling demand for earthenware products in construction and household applications. Africa’s growth is propelled by increasing infrastructure development and rising consumer interest in eco-friendly building materials. Regional government initiatives and expanding trade networks further support market expansion in these areas.

Innovative Technologies Driving Sustainable Earthenware Growth

North America holds approximately 18% of the global earthenware market by volume, supported by strong demand from the construction, hospitality, and home décor industries. Regulatory frameworks aimed at reducing carbon footprints have accelerated the adoption of environmentally friendly earthenware products, with government incentives encouraging sustainable manufacturing practices. Technological advancements such as AI-enabled quality control and digital kiln monitoring have enhanced operational efficiency in production facilities. Additionally, digital transformation initiatives are streamlining supply chains, enabling faster delivery and customization, which further drives market expansion in this mature region.

Embracing Sustainability and Innovation in Earthenware Manufacturing

Europe accounts for about 22% of the global earthenware market volume, with Germany, the UK, and France leading consumption. The market benefits from strict regulatory oversight focusing on environmental compliance and sustainable resource use, enforced by bodies like the European Chemicals Agency. European manufacturers increasingly incorporate low-emission glazing techniques and energy-efficient kiln technologies. The region is also witnessing accelerated adoption of Industry 4.0 solutions, including robotics and IoT, to optimize production. Growing consumer preference for artisanal and eco-conscious products supports niche segments within the market.

Manufacturing Powerhouse Fueling Earthenware Demand

Asia-Pacific leads the global earthenware market with a volume share exceeding 40%, driven by China, India, and Japan as top consuming countries. Rapid urbanization and booming construction sectors have expanded demand for earthenware tiles and building materials. The region also hosts major manufacturing hubs that leverage advanced production technologies, such as automated molding and glazing lines. Innovation clusters in countries like Japan are fostering development of smart earthenware with enhanced durability and thermal insulation properties. Regional emphasis on sustainable infrastructure projects further propels market momentum.

Infrastructure Development Spurs Market Growth

South America holds nearly 8% of the global earthenware market share, with Brazil and Argentina as key players. Increasing investments in infrastructure and housing projects are driving demand for durable and affordable earthenware materials. The regional energy sector also influences market trends, as eco-friendly ceramic materials gain traction in sustainable construction efforts. Trade policies facilitating cross-border raw material flow and government incentives for local manufacturing contribute positively to market growth. Emerging urban centers are adopting earthenware products in commercial and residential projects, further enhancing market penetration.

Modernization and Construction Boom Support Market Expansion

The Middle East & Africa region accounts for approximately 10% of the global earthenware market, with the UAE and South Africa as major growth countries. Demand is primarily driven by expanding construction activities, including residential complexes and commercial infrastructure. Technological modernization, such as the introduction of energy-efficient kiln systems and automation, is improving production capacity and quality. Regional regulations promoting sustainable building materials and international trade partnerships facilitate market development. Additionally, oil & gas sector investments indirectly stimulate market demand through infrastructure upgrades and facility expansions.

China

Holds around 28% market share due to its vast production capacity and robust end-user demand across construction and household sectors.

India

Commands approximately 14% market share, supported by rapid urbanization, strong domestic consumption, and government initiatives promoting eco-friendly building materials.

The Earthenware market features a highly competitive environment with over 120 active companies worldwide, ranging from established ceramic manufacturers to emerging niche producers. Market leaders focus on strategic initiatives such as innovation in sustainable materials, product diversification, and expansion into new geographic regions to maintain competitive positioning. Partnerships and collaborations with technology firms are becoming increasingly common, driving advancements in automation and quality control. Recent product launches emphasize eco-friendly earthenware solutions designed to meet evolving regulatory standards and consumer preferences. Mergers and acquisitions are also shaping the landscape, enabling companies to broaden their portfolios and scale operations efficiently. Innovation trends such as smart manufacturing technologies, including AI-assisted production processes and real-time monitoring systems, are enhancing product quality and reducing operational costs, creating a dynamic competitive arena. Overall, companies that integrate technological innovation with sustainability commitments are well-positioned to lead the Earthenware market.

RAK Ceramics

Villeroy & Boch AG

Kajaria Ceramics Ltd.

Mohawk Industries, Inc.

Ceramic Arts Ltd.

Grupo Lamosa

Johnson Tiles

Somany Ceramics Ltd.

Crossville, Inc.

Terreal

Porcelanosa Grupo

The Earthenware market is increasingly influenced by a range of advanced technologies that optimize production, improve product quality, and enhance sustainability. Automated kiln systems now feature precise temperature control with real-time sensors, enabling uniform firing and reducing material waste by up to 15%. Advanced glazing techniques incorporating nanomaterials improve durability and surface finish, meeting the demand for high-performance earthenware in industrial and consumer sectors. Additionally, 3D printing technology is being adopted for rapid prototyping and small-batch custom designs, which reduces lead times and allows greater product innovation. Digital process monitoring platforms integrate IoT devices to track production metrics, enabling manufacturers to enhance operational efficiency and minimize downtime. Eco-friendly innovations also play a critical role, with manufacturers employing bio-based raw materials and water-saving technologies during manufacturing to meet stricter environmental regulations. Energy-efficient electric and hybrid kilns are becoming standard, cutting energy consumption significantly while maintaining quality standards. These technological advancements collectively drive competitive advantages for manufacturers willing to invest in cutting-edge solutions, positioning them for future growth in the evolving Earthenware market.

In March 2024, Kajaria Ceramics unveiled a new eco-friendly earthenware line utilizing recycled clay and water-based glazes, reducing production waste by 20% and expanding its sustainable product portfolio in response to increasing environmental regulations.

In October 2023, Mohawk Industries invested in a state-of-the-art automated glazing facility, enhancing production capacity by 25% and enabling faster turnaround for customized earthenware orders across North America and Europe.

In January 2024, Villeroy & Boch AG integrated AI-powered quality inspection systems in their German factories, improving defect detection rates by 30% and reducing rework costs through enhanced visual analytics.

In July 2023, Grupo Lamosa launched a digital platform for real-time tracking of earthenware shipments, improving supply chain transparency and delivery reliability for industrial clients across Latin America.

The Earthenware Market Report comprehensively covers a broad spectrum of market segments including various product types such as traditional earthenware, glazed earthenware, and decorative ceramics. It analyzes applications across residential, commercial, industrial, and institutional sectors, highlighting how earthenware products cater to both functional and aesthetic demands. The report provides geographic insights spanning major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional consumption patterns, manufacturing hubs, and trade flows. Technological aspects form a critical part of the report, addressing innovations like advanced kiln systems, 3D printing for custom designs, eco-friendly glazing techniques, and digital process monitoring tools. It also emphasizes emerging niches such as sustainable earthenware manufacturing and integration of smart technologies for quality assurance.

Industry focus areas include construction materials, household goods, tableware, and decorative arts, providing insights into end-user trends and sector-specific demands. Additionally, the report explores regulatory environments, environmental considerations, and investment landscapes shaping the market’s future trajectory. Overall, the scope ensures a thorough understanding of the competitive environment, market drivers, challenges, and growth opportunities for stakeholders, equipping decision-makers with actionable intelligence to navigate the evolving Earthenware market effectively.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1815.16 Million |

|

Market Revenue in 2032 |

USD 2581.34 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |