Reports

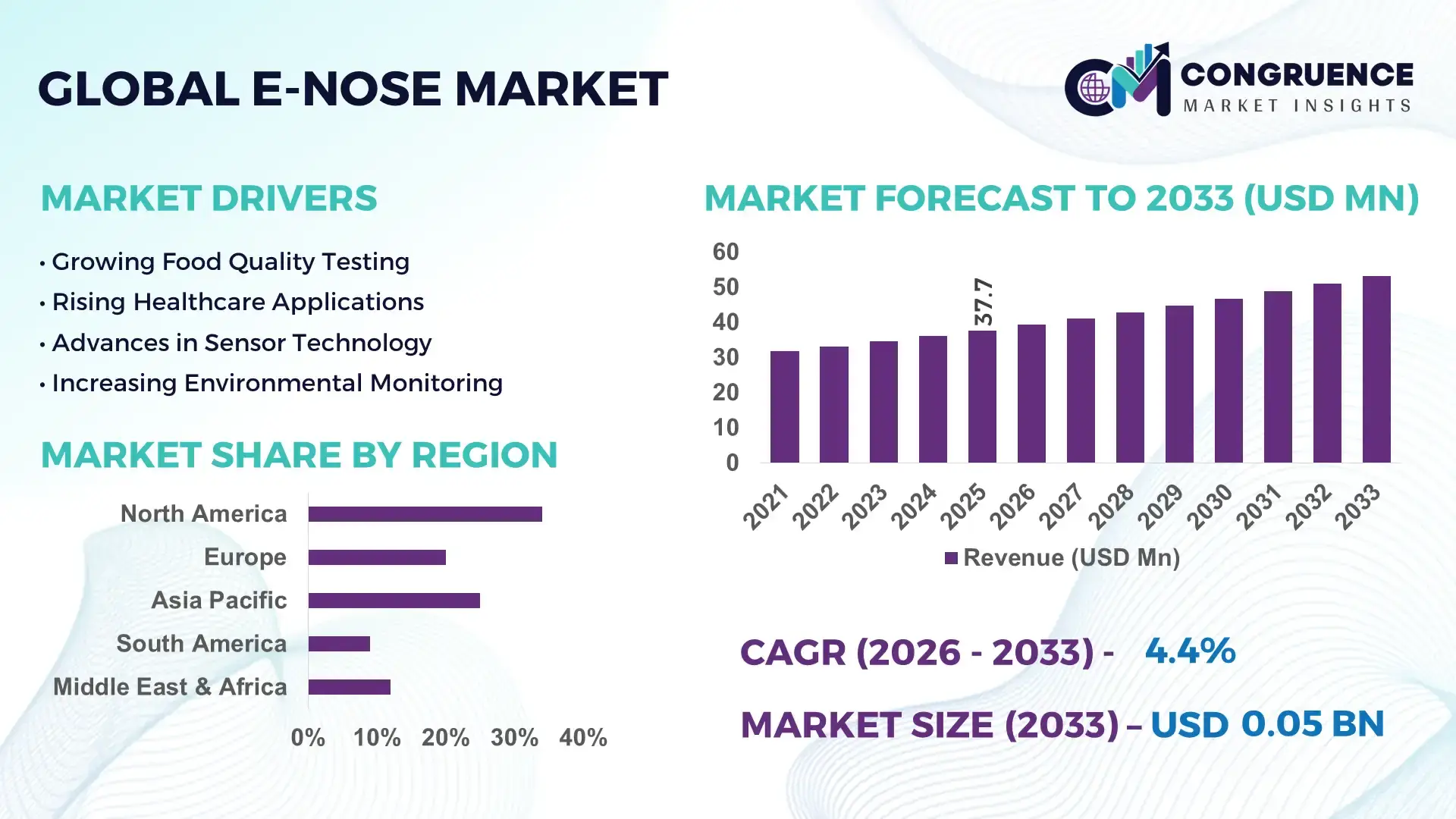

The Global E-Nose Market was valued at USD 37.7 Million in 2025 and is anticipated to reach a value of USD 53.2041292138648 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Rising deployment of AI-integrated gas sensing platforms across food quality inspection, industrial safety monitoring, pharmaceutical validation, and defense-grade chemical detection systems is accelerating commercial-scale E-Nose adoption in high-compliance industries.

The United States dominates the global E-Nose Market with approximately 34% share, supported by over USD 420 million in sensor R&D allocations tied to semiconductor diagnostics, defense screening, and precision food testing programs in 2026. Germany follows with nearly 18% regional concentration driven by automotive emission analytics and industrial automation integration. U.S.-based manufacturers report 22% faster contamination detection efficiency through AI-enabled electronic olfaction platforms amid tighter global chemical safety regulations and post-Red Sea supply-chain diversification strategies.

Companies prioritizing miniaturized sensor arrays, edge-AI processing, and multi-industry calibration capabilities are positioned to secure higher-margin contracts across regulated industrial ecosystems.

Market Size & Growth: USD 37.7 million in 2025 reaching USD 53.2 million by 2033, driven by AI-powered odor analytics and industrial safety automation across high-growth manufacturing sectors.

Top Growth Drivers: Food quality monitoring adoption up 31%, healthcare diagnostics integration rising 27%, and hazardous gas detection deployments increasing 24% globally.

Short-Term Forecast: By 2028, advanced E-Nose systems reduce contamination screening time by 35% and improve industrial inspection efficiency by 28%.

Emerging Technologies: AI-based pattern recognition, nanomaterial sensor arrays, and cloud-connected automation platforms improve detection precision by nearly 30%.

Regional Leaders: North America projected above USD 18 million with defense adoption growth; Europe surpassing USD 14 million through automotive testing; Asia-Pacific exceeding USD 12 million from electronics manufacturing expansion.

Consumer/End-User Trends: Over 42% of food processors now integrate smart odor-detection systems for shelf-life validation and quality assurance workflows.

Pilot/Case Example: In 2026, a pharmaceutical manufacturing pilot reduced volatile compound inspection errors by 33% using multi-sensor E-Nose analytics.

Competitive Landscape: Top companies control nearly 46% market share, with competition centered on portable sensing accuracy, AI integration, and industrial-grade calibration platforms.

Regulatory & ESG Impact: Industrial emission compliance programs improved toxic vapor monitoring accuracy by 26% under stricter environmental surveillance mandates.

Investment & Funding: More than USD 280 million in sensor innovation investments supported strategic partnerships, semiconductor expansion, and smart manufacturing integration in 2026.

Innovation & Future Outlook: Next-generation bioelectronic sensors and edge-AI architectures are increasing real-time detection capabilities by over 32% across decentralized industrial operations.

Advanced E-Nose systems are gaining traction across packaged food verification, medical diagnostics, and smart manufacturing inspection environments where rapid odor profiling improves operational accuracy. AI-enabled nanosensor platforms now deliver nearly 29% higher compound differentiation efficiency compared to conventional gas detection units. Increased localization of semiconductor and sensor manufacturing in Asia-Pacific, alongside stricter industrial emission monitoring frameworks in 2026, is accelerating commercialization and setting the stage for broader strategic deployment discussions.

The E-Nose Market is becoming strategically important as industries prioritize real-time contamination analytics, automated quality assurance, and compliance-driven sensing infrastructure across food processing, pharmaceuticals, and industrial manufacturing. Tightened volatile organic compound monitoring standards in the United States and Europe, combined with supply-chain restructuring after semiconductor shortages, are accelerating investment in localized sensor manufacturing and AI-integrated odor analytics platforms. More than 38% of large food exporters adopted automated olfactory inspection workflows in 2026 to reduce manual testing dependency and improve export-grade consistency.

Advanced AI-enabled E-Nose systems now deliver nearly 30% faster compound recognition accuracy compared to legacy gas chromatography screening in high-throughput environments while reducing inspection-related operational costs by approximately 18%. Japan and South Korea are focusing on compact semiconductor-based sensor integration for electronics and healthcare diagnostics, whereas Germany emphasizes industrial emission monitoring and automotive cabin air analytics. Over the next 2–3 years, portable multi-sensor deployments are expected to exceed 45% of new industrial procurement volumes due to rising demand for edge-based detection capabilities.

In 2026, several pharmaceutical manufacturers integrated E-Nose platforms into cleanroom validation processes, reducing volatile contamination response times by 26%. Companies are expanding partnerships with AI software developers, nanomaterial suppliers, and industrial automation firms to strengthen calibration accuracy and deployment scalability. Businesses securing proprietary sensing algorithms and sector-specific data libraries are expected to gain stronger competitive positioning through faster diagnostics, lower compliance costs, and differentiated industrial analytics capabilities.

Food manufacturers, pharmaceutical producers, and semiconductor facilities are accelerating E-Nose deployment to improve real-time contamination detection and automated quality assurance efficiency. In 2026, AI-enabled sensor systems improved odor classification precision by 31% while reducing manual inspection workloads by nearly 24% across high-volume production environments. Germany’s stricter industrial emission surveillance standards and U.S. pharmaceutical validation upgrades are pushing enterprises toward continuous volatile compound monitoring infrastructure. This shift is directly increasing demand for portable multi-sensor platforms and edge-processing analytics. Companies are responding through nanomaterial sensor investments, localized calibration facilities, and strategic partnerships with industrial automation providers. A key operational advantage is the reduction of product rejection rates by up to 19% in export-oriented food manufacturing facilities using automated olfactory inspection systems.

High-performance E-Nose systems remain constrained by sensor calibration complexity, semiconductor supply volatility, and integration expenses across industrial environments. Advanced gas sensor component costs increased nearly 17% during recent semiconductor allocation disruptions, while calibration maintenance expenses account for approximately 22% of operational deployment budgets in pharmaceutical-grade facilities. China’s export controls on specialized electronic materials and prolonged lead times for microelectromechanical sensors continue affecting production scalability for mid-sized manufacturers. These pressures reduce profitability and slow deployment cycles in cost-sensitive industries. Companies are mitigating exposure through localized sensor sourcing, multi-country supplier contracts, and modular hardware architectures designed to reduce recalibration frequency. Firms adopting software-driven calibration automation are achieving nearly 14% lower maintenance downtime compared to traditional manually calibrated systems.

Portable and cloud-connected E-Nose platforms are opening new commercial opportunities across healthcare diagnostics, smart packaging, and industrial mobility applications. In 2026, compact sensor deployment in non-invasive respiratory screening programs increased by 28%, while smart food packaging integration projects expanded by nearly 21% in Japan and Singapore. AI-driven edge analytics and graphene-based nanosensors are improving detection sensitivity by approximately 33% compared to older polymer sensor configurations. Governments supporting industrial digitalization and environmental monitoring infrastructure are creating new procurement channels for automated sensing technologies. Companies are expanding R&D alliances with medical device developers and industrial IoT providers to commercialize multi-application sensor ecosystems. An emerging strategic opportunity lies in subscription-based odor analytics platforms that generate recurring software-driven inspection revenue alongside hardware sales.

Long-term scalability of the E-Nose Market is challenged by fragmented calibration standards, inconsistent environmental datasets, and integration difficulties across industrial automation systems. Nearly 35% of manufacturers deploying advanced sensing platforms report interoperability issues between E-Nose analytics software and existing factory monitoring infrastructure. Variations in humidity, airborne particulates, and regional operating conditions continue reducing cross-site detection consistency, particularly in large-scale chemical processing facilities in India and Southeast Asia. Additionally, cybersecurity concerns surrounding cloud-connected industrial sensing networks are increasing compliance costs for enterprise deployments. Companies must invest in standardized data architectures, secure edge-processing capabilities, and interoperable software frameworks to maintain deployment reliability. Businesses developing proprietary AI training datasets with adaptive environmental calibration models are expected to secure stronger long-term operational resilience and industrial adoption consistency.

• AI-Calibrated Sensing Expansion Advanced E-Nose manufacturers are integrating edge-AI calibration engines to improve compound recognition accuracy by nearly 32% while reducing false-positive detection rates by 21% in industrial inspection workflows. Food exporters in the United States and South Korea are replacing manual odor validation with automated sensing checkpoints following stricter contamination compliance requirements. Companies are responding through semiconductor partnerships, embedded analytics deployment, and cloud-connected monitoring architectures that shorten inspection cycles and improve operational throughput across high-volume facilities.

• Portable Diagnostics Deployment Surge Portable and handheld E-Nose systems recorded over 28% higher deployment across respiratory screening and pharmaceutical validation programs during 2026 due to rising demand for decentralized diagnostics. Hospitals in Japan are integrating compact olfactory sensing devices into rapid pre-screening workflows to reduce laboratory dependency and improve patient processing efficiency by 19%. Sensor manufacturers are prioritizing battery optimization, wireless connectivity, and lightweight nanomaterial components to support mobile deployment scalability and reduce device maintenance frequency.

• Industrial Emission Monitoring Shift Industrial manufacturers are deploying continuous E-Nose monitoring systems to address tightening volatile organic compound regulations and workplace air-quality mandates. Germany-based chemical facilities reported nearly 24% faster hazardous vapor detection after integrating automated olfactory analytics with factory control systems. This transition is driving increased investment in interoperable software platforms and predictive maintenance integration. Companies are restructuring operational monitoring frameworks to combine environmental compliance tracking with production efficiency analytics through centralized sensing infrastructure.

• Localized Sensor Supply Strategies Semiconductor shortages and geopolitical trade restrictions are reshaping E-Nose component sourcing strategies across electronics and industrial automation sectors. Sensor lead times declined by approximately 16% after manufacturers in India and Taiwan expanded localized microelectromechanical sensor packaging operations during 2026. A non-obvious industry shift is the movement toward dual-supplier calibration ecosystems, allowing enterprises to reduce deployment interruptions and maintain multi-site operational consistency. Companies are expanding regional assembly partnerships and modular hardware designs to strengthen supply resilience and reduce integration delays.

Portable E-Nose systems dominate the market due to their scalability, lower deployment costs, and suitability for field-based inspection across food processing, environmental surveillance, and industrial safety operations. In 2026, portable devices accounted for nearly 36% of enterprise-level deployments as manufacturers prioritized mobility and real-time odor analytics integration. Benchtop systems remain widely adopted in pharmaceutical laboratories and research facilities where high-sensitivity compound analysis and stable calibration environments are operationally critical. Meanwhile, handheld devices are gaining traction in rapid industrial inspection workflows, reducing inspection response times by approximately 23% compared to stationary testing systems.

Wearable and wireless E-Nose platforms represent the fastest-evolving segments, supported by industrial IoT adoption and decentralized monitoring requirements. Wireless systems improved remote monitoring efficiency by nearly 27% in smart manufacturing environments, while wearable olfactory sensors are increasingly used in hazardous workplace exposure monitoring. Companies are responding through lightweight sensor innovation, AI-enabled mobile analytics, and strategic partnerships with automation integrators. Investment priorities are shifting toward compact semiconductor architectures and multi-location connectivity platforms that support scalable enterprise deployment without increasing calibration complexity.

Food Quality Testing remains the leading application segment as food manufacturers intensify contamination control, shelf-life validation, and export-grade quality monitoring processes. In 2026, nearly 44% of commercial E-Nose deployments were linked to packaged food inspection and fermentation monitoring operations. Automated olfactory analytics reduced spoilage detection time by approximately 26% in high-volume dairy and meat processing facilities. Industrial Safety and Environmental Monitoring applications continue expanding steadily as chemical plants and manufacturing hubs integrate continuous vapor detection systems to comply with stricter workplace emission standards and air-quality mandates.

Medical Diagnosis is emerging as the fastest-growing application area due to rising interest in non-invasive respiratory analysis and AI-assisted disease screening workflows. Healthcare institutions in Japan and the United States expanded pilot deployments by nearly 29% during 2026 to reduce dependency on time-intensive laboratory diagnostics. Military Detection applications remain strategically relevant for chemical threat identification and battlefield surveillance, particularly through portable sensing integration. Companies are scaling cloud-connected diagnostics, improving sensor miniaturization, and aligning partnerships with healthcare and defense technology providers to strengthen sector-specific deployment capabilities.

The Food and Beverage Industry represents the dominant end-user segment due to continuous inspection requirements, contamination control mandates, and export-focused quality assurance operations. In 2026, food processors accounted for nearly 39% of total E-Nose procurement activity, particularly across dairy, packaged meat, and beverage manufacturing facilities. Automated odor analytics improved batch validation efficiency by approximately 28% while reducing manual inspection dependency. Industrial Manufacturers also maintain significant adoption levels through hazardous gas detection and process-monitoring integration, especially in Germany’s automotive and specialty chemical production hubs where workplace monitoring regulations continue tightening.

The Healthcare Industry is the fastest-growing end-user segment as hospitals and diagnostic laboratories increase investment in non-invasive respiratory sensing and AI-assisted screening technologies. Clinical pilot deployments expanded by nearly 31% during 2026 as healthcare providers prioritized rapid diagnostic workflows and reduced laboratory congestion. Environmental Agencies are integrating wireless E-Nose networks for continuous air-quality surveillance, while Defense Sector organizations are focusing on portable chemical detection platforms for field operations. Research Institutes remain critical for calibration algorithm development and nanosensor innovation. Companies are targeting these segments through customized sensor configurations, subscription-based analytics platforms, and strategic co-development partnerships with institutional buyers.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

AI-Driven Industrial Inspection Expansion

North America maintains leadership in the E-Nose Market through strong deployment across pharmaceutical manufacturing, packaged food testing, and industrial emission monitoring systems. The region represented approximately 34% of global deployment concentration in 2025, supported by high adoption of AI-integrated sensing infrastructure and advanced semiconductor calibration capabilities. U.S.-based food processing enterprises increased automated odor inspection integration by nearly 29% during 2026 to strengthen export-grade quality compliance and reduce manual testing dependency. Strategic partnerships between industrial automation firms and sensor manufacturers are accelerating deployment of edge-connected E-Nose platforms across multi-site production environments. Companies are prioritizing predictive analytics integration and localized sensor assembly to improve operational continuity and calibration efficiency.

United States Market Outlook: The United States leads regional adoption through strong pharmaceutical validation infrastructure, defense-grade chemical detection programs, and large-scale food manufacturing operations. More than 41% of industrial food inspection facilities upgraded to AI-assisted olfactory analytics systems during 2026 to improve contamination response speed and regulatory traceability. Semiconductor ecosystem strength, advanced industrial automation networks, and federal workplace emission standards continue supporting enterprise-level deployment expansion. U.S. manufacturers are also increasing investments in portable and wireless E-Nose architectures to improve decentralized monitoring capabilities across logistics and manufacturing environments.

Regulatory-Driven Monitoring Modernization

Europe remains a major operational hub for E-Nose deployment due to stringent industrial emission regulations, advanced automotive manufacturing infrastructure, and strong sustainability-focused monitoring initiatives. The region accounted for nearly 28% of global deployment activity in 2025, with Germany, France, and the Netherlands leading industrial sensing integration. Chemical manufacturers across Europe improved hazardous vapor detection efficiency by approximately 24% after integrating automated olfactory monitoring into centralized industrial control systems. Environmental compliance modernization and stricter volatile organic compound surveillance frameworks are driving enterprise investments in continuous monitoring technologies. Companies are strengthening regional partnerships with industrial IoT providers and analytics software firms to improve interoperability and long-term compliance management.

Germany Market Outlook: Germany dominates the European market through its advanced automotive production ecosystem, industrial automation expertise, and strong environmental compliance infrastructure. Nearly 33% of large-scale chemical and automotive facilities in Germany integrated automated air-quality sensing systems into operational monitoring workflows during 2026. Industrial manufacturers are prioritizing edge-connected E-Nose platforms to improve workplace safety analytics and production consistency. Germany’s strong semiconductor engineering capabilities and emphasis on Industry 4.0 deployment continue reinforcing its position as a strategic innovation and calibration center for industrial olfactory sensing technologies.

Semiconductor Manufacturing and Portable Deployment Growth

Asia-Pacific is emerging as the fastest-expanding E-Nose Market due to rapid semiconductor manufacturing expansion, industrial automation upgrades, and increasing deployment of portable sensing platforms across healthcare and food quality operations. The region represented approximately 25% of global market activity in 2025, supported by strong electronics production ecosystems in China, Japan, South Korea, and Taiwan. During 2026, deployment of compact wireless E-Nose systems increased by nearly 31% across industrial manufacturing and diagnostic pilot programs. Companies are accelerating localized sensor packaging operations and AI-integrated portable device production to reduce dependency on imported components and improve supply-chain resilience.

China Market Outlook: China leads regional market concentration through its large-scale electronics manufacturing infrastructure, industrial monitoring expansion, and rapidly growing smart manufacturing ecosystem. More than 38% of newly installed automated food inspection systems in China incorporated integrated olfactory sensing capabilities during 2026. Domestic manufacturers are expanding graphene-based sensor production and cloud-enabled analytics platforms to strengthen industrial self-sufficiency and reduce component sourcing risks. Government-backed digital industrial modernization initiatives and export-oriented quality assurance requirements continue accelerating enterprise adoption across manufacturing and environmental monitoring sectors.

Food Export Compliance Driving Adoption

South America is witnessing increasing E-Nose adoption through food export monitoring, agricultural quality assurance, and industrial safety modernization initiatives. Brazil and Argentina account for the majority of regional deployment activity due to large-scale meat processing and agricultural export operations requiring stricter contamination control systems. During 2026, automated olfactory inspection integration improved batch validation efficiency by approximately 19% across export-oriented food production facilities. Infrastructure limitations and calibration dependency continue affecting deployment consistency in smaller industrial operations, yet companies are expanding regional partnerships with automation integrators and sensor distributors to improve operational scalability and maintenance accessibility.

Brazil Market Outlook: Brazil represents the largest operational market in South America due to its dominant food processing sector, expanding industrial automation investments, and export-focused compliance infrastructure. Meat and beverage manufacturers increased deployment of portable E-Nose inspection systems by nearly 26% during 2026 to strengthen quality traceability and reduce shipment rejection risks in international trade. Industrial enterprises are also adopting continuous workplace air monitoring systems to align with evolving environmental compliance requirements. Local integration partnerships and growing automation investment are improving deployment accessibility across medium-scale manufacturing facilities.

Industrial Modernization and Smart Infrastructure Integration

The Middle East & Africa region is gradually expanding E-Nose deployment through industrial modernization programs, smart city infrastructure investments, and environmental monitoring initiatives. Energy processing facilities and food import inspection systems are becoming major deployment areas, particularly in Gulf economies prioritizing operational digitization. In 2026, industrial monitoring projects integrating automated gas and odor analytics increased by nearly 22% across selected energy and logistics hubs. Infrastructure fragmentation and specialized workforce shortages remain execution constraints; however, governments and industrial operators are increasing partnerships with sensor technology providers and automation companies to improve industrial safety analytics and environmental compliance capabilities.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment activity through large-scale industrial diversification initiatives, advanced energy infrastructure modernization, and increasing investment in environmental monitoring technologies. Industrial operators expanded deployment of AI-enabled air-quality sensing systems by approximately 27% during 2026 across refining and petrochemical operations. Smart industrial city projects and logistics modernization programs are creating additional demand for wireless E-Nose platforms capable of continuous environmental surveillance. Strategic collaboration with industrial automation providers and expanding digital infrastructure investment continue positioning the country as a key regional operational hub for advanced sensing technologies.

The E-Nose Market is led by technology-focused sensing companies competing against industrial automation specialists, semiconductor-integrated sensor developers, and regional calibration providers. Key competition exists between Alpha MOS, AIRSENSE Analytics, Aryballe Technologies, Electronic Sensor Technology, and Owlstone Medical, while Asian manufacturers increasingly challenge premium Western suppliers through lower-cost portable systems and faster customization cycles. The top five players collectively control nearly 48% of global market activity through proprietary sensor architectures, AI-driven analytics, and application-specific calibration libraries. Competition centers on detection precision, response speed, deployment flexibility, and integration efficiency, with advanced AI calibration reducing false-positive rates by approximately 21% and portable deployment costs by nearly 18%. Companies are strengthening positions through vertical integration, semiconductor partnerships, cloud-based analytics expansion, and industrial automation alliances. Technology standardization complexity and calibration reliability remain key entry barriers. Winning requires scalable sensor ecosystems, industry-specific datasets, localized support infrastructure, and continuous AI-enhanced performance optimization across regulated industrial environments.

Alpha MOS

AIRSENSE Analytics GmbH

Aryballe Technologies

Electronic Sensor Technology

Owlstone Medical

The eNose Company

Sensigent LLC

RoboScientific Ltd.

Odotech Inc.

AIRSENSE Technology

Brechbühler AG

Envirosuite Limited

Scensive Technology Ltd.

Smiths Detection Group Ltd.

AI-enabled sensor fusion platforms currently define the technological foundation of the E-Nose Market, particularly across food inspection, pharmaceutical validation, and industrial air-quality analytics. Multi-sensor arrays integrated with machine learning algorithms improve odor classification accuracy by nearly 31% while reducing manual calibration workloads by 18% compared to conventional gas-sensing systems. In 2026, over 42% of newly deployed industrial E-Nose platforms incorporated edge-based analytics for real-time contamination monitoring. Companies benefiting most include semiconductor-integrated sensor developers and industrial automation providers capable of combining predictive analytics with low-latency operational monitoring.

Emerging technologies between 2026 and 2028 are centered on graphene-based nanosensors, MEMS architectures, and wireless cloud-connected detection systems. Advanced MEMS sensor arrays consume less than 10 mW power while improving trace-gas sensitivity by approximately 27% over older metal-oxide sensor configurations. Portable AI-powered E-Nose devices now deliver nearly 30% faster detection response times in decentralized healthcare and industrial safety applications. Adoption is increasing rapidly across Japan, South Korea, and Germany as enterprises prioritize compact diagnostics and scalable industrial monitoring infrastructure.

Disruptive development is shifting toward autonomous calibration engines and embedded spatiotemporal neural networks capable of correcting sensor drift by nearly 85%. Compared with legacy rule-based recognition systems, advanced neural architectures improve multi-odor discrimination performance by approximately 35% in dynamic industrial environments. Companies investing now in proprietary sensing datasets, adaptive AI calibration, and interoperable IoT integration are securing long-term competitive advantages in regulated high-precision monitoring ecosystems.

April 2024 – Owlstone Medical secured USD 6.5 million in funding to expand breath-based infectious disease diagnostics and enhance its VOC Atlas platform, strengthening non-invasive biomarker development capabilities. The initiative accelerated precision diagnostic scalability and expanded clinical partnership activity across respiratory disease screening programs.

October 2025 – Researchers published a universal E-Nose platform capable of identifying 53 odor categories within 7 seconds while achieving 95% classification accuracy through embedded MCU-based AI processing. The development improved real-time sensing performance for robotics, smart manufacturing, and intelligent environmental monitoring applications. Source: sciencedirect.com

August 2025 – Advanced MEMS-based pocket E-Nose systems demonstrated detection limits below 0.5 ppm using ultralow-power nanocomposite sensor arrays consuming less than 2 mW. The innovation significantly improved portable hazardous gas identification efficiency and accelerated miniaturized industrial safety deployment across compact monitoring environments. Source: pubmed.ncbi.nlm.nih.gov

February 2025 – Researchers introduced triplet calibration technology achieving nearly 85% drift-correction accuracy for general-purpose E-Nose systems using fewer calibration odors. The breakthrough reduced long-term calibration instability and improved deployment consistency in industrial food testing and automated environmental sensing applications. Source: elsevier.com

The E-Nose Market report provides detailed analysis across portable, handheld, benchtop, wearable, and wireless sensing platforms, with strategic evaluation of deployment trends across food quality testing, medical diagnosis, industrial safety, military detection, and environmental monitoring applications. The study assesses operational adoption patterns across healthcare institutions, food manufacturers, industrial enterprises, environmental agencies, research institutes, and defense organizations. More than 40% of recent enterprise deployments analyzed in the report involve AI-integrated portable sensing systems designed for decentralized monitoring and automated inspection workflows.

The report delivers region-wise strategic insights covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level operational analysis focused on industrial infrastructure, sensor manufacturing ecosystems, and regulatory modernization trends. It also evaluates emerging technologies including MEMS architectures, graphene-based nanosensors, edge-AI analytics, and cloud-connected olfactory monitoring platforms. Competitive benchmarking, deployment scalability assessment, partnership strategies, and calibration standardization analysis support investment planning, expansion prioritization, and long-term positioning decisions between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 37.7 Million |

|

Market Revenue in 2033 |

USD 53.2041292138648 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Alpha MOS, AIRSENSE Analytics GmbH, Aryballe Technologies, Electronic Sensor Technology, Owlstone Medical, The eNose Company, Sensigent LLC, RoboScientific Ltd., Odotech Inc., AIRSENSE Technology, Brechbühler AG, Envirosuite Limited, Scensive Technology Ltd., Smiths Detection Group Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |